Big Day, Big Data: CPI Expectations, Quantum Update, Charting Disney and More

Let's dissect what to expect for the consumer price index, look at Fed Funds futures markets, and check on market trends.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We're here again. Early morning. The day of the week we're focused on. Every week seems to have one. This week it's the consumer price index. Last week, the focus was on Friday's November employment report. Next Wednesday, the Federal Open Market Committee will make its next decision on monetary policy. It seems like everything currently plays into what the Fed may or may not do, especially when we are in between corporate earnings seasons like we are now.

The CPI lands at 8:30 a.m. ET. Yes, the Fed claims to follow the personal consumption expenditure price index, which is released toward the end of the month, but the rest of the world follows CPI more closely than PCE. I am sure those Fed officials who comprise the FOMC do as well, just more quietly.

Readers will see below that I am looking for a headline CPI growth of 2.8% on a year-over-year basis. Consensus is for growth of 2.7%. This comes after October's print of 2.6% and September's 2.4% print. Please recall that since those September numbers were released, I have been writing that September was the low for headline CPI, at least for a while. Consumer-level inflation has clearly accelerated, while not quite running red hot.

Readers will also see that I am looking for core CPI growth of 3.3%. I am in line with the consensus view there and that would be a continuation of October's 3.3% pace, which was in line with a 3.3% print for September. Core inflation bottomed over the summer at 3.2%. That's really not that close to 2% if one really thinks about it. Was moving toward an easier policy a central banking mistake? Not if the idea was to goose the economy or slow the broad decay of labor markets. So far, the Fed seems to have accomplished that, though it is early to announce, "mission accomplished."

Yes, moving toward easier policy was a mistake if the idea was to get consumer-level inflation down to 2%, especially if the focus is on core consumer inflation. Does a hot print this morning rattle a few cages at the Fed? By hot, I don't mean 2.7% headline growth. I mean the 2.8% I am looking for or maybe even warmer than that. That should slow the Fed down. You've seen profit taking and risk management take center stage so far this week. That came ahead of this morning's report and was precisely meant to get ahead of the Fed.... just in case.

Ahead of November CPI

As we traverse the zero-dark hours on Wednesday morning, Fed Funds futures markets trading in Chicago are pricing in an 86% probability for a quarter-percentage point rate cut a week from today when the FOMC gets together. Then another rate cut is not priced in until March with a last rate cut for the cycle priced in for July. As you rise the Fed's target range for the Fed Funds Rate stands at 4.5% to 4.75%. At the moment, these markets see the terminal rate at 3.75% to 4%.

Glancing over at the gross domestic product, the Bureau of Economic Analysis will revise their third-quarter print for the final time next Thursday, the day after the Fed's dog-and-pony show. After the first revision, third-quarter GDP growth stands at 2.8% quarter-over-quarter seasonally adjusted annual rate. That's better than decent. Readers are reminded that ultimately, GDP and gross domestic income must reconcile and Q3 GDI growth in the second estimate was a little slower at 2.2%.

As for the current quarter, the Atlanta Fed's GDPNow model currently sports robust looking growth of 3.3%. Just remember that the St. Louis Fed's model stands at growth of just 1.3% and these models have been close to equal in terms of accuracy over the past year. At least one of them is way off course.

Marketplace

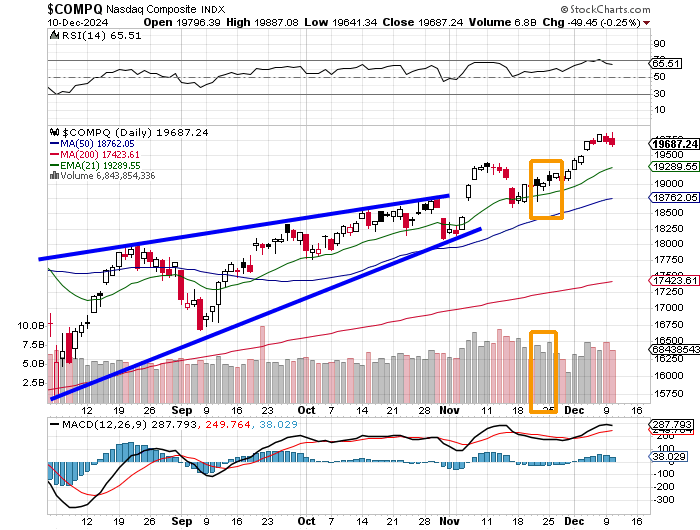

Equity markets showed some caution on Tuesday ahead of these numbers. Both the S&P 500 and the Nasdaq Composite posted a second straight red candle day, though neither was beaten down too severely. The S&P 500 gave up 0.3% as the Nasdaq Composite gave back 0.25%. Almost the entire spectrum of major to mid-major equity indices traded lower, led in that direction by the Philadelphia Semiconductor Index.

That index suffered a beatdown of 2.47% as Micron MU and Broadcom AVGO were slapped around to the tune of 4.59% and 3.98% respectively. Broadcom is set to report this Thursday afternoon, and Micron is up next week. The Dow Transports put some green on the screen, as Alaska Airlines ALK soared 13% after raising guidance at its Investor Day.

Eight of the 11 S&P sector SPDR exchange-traded funds shaded into the red on Tuesday with three of these funds giving up 1% or more for the session. The REITs XLRE led the way lower at -1.62%. Communication Services XLC was easily the performance leader for the day at +1/57%. That was on the strength of Alphabet GOOGL, which gained 5.59% as the quantum computing chip news from Monday seemed to sink in.

Breadth was weak on Tuesday. Losers beat winners by a rough 5 to 3 at the NYSE and by about 3 to 2 at the Nasdaq. Advancing volume took just a 32.7% share of composite NYSE-listed trade and a 43.9% share of composite Nasdaq-listed activity. The one saving grace might be that trading volume was significantly lower in the aggregate on Tuesday than it had been on Monday across the listed securities of both exchanges.

Understand the Trend

That for both the S&P 500 and the Nasdaq Composite that Tuesday, due to its lower volume did not confirm a downward change of trend. Readers will correctly see Monday as a potential "Day One" on elevated volume. Now, we wait to see if there is to be a confirmation. Of course, this morning's CPI shows up as if on cue as a possible catalyst. We'll likely know more in a few hours.

Quantum Week

On Monday, Alphabet's Google unveiled its new quantum computing chip known as "Willow" and the smaller stocks already in the quantum computing space reversed lower off of what had been a solid morning and closed much lower. On Tuesday, Alphabet shares traded higher, but so did these stocks. Led by Rigetti Computing RGTI: That name was up 45.2% (which means it was up two bucks). Following Rigetti was Quantum Computing Inc QUBT, D-Wave Computing (QBTS). IonQ IONQ closed lower on the day.

Elsewhere on the Market ...

- General Motors GM is up almost 2% overnight after announcing that the firm will half funding for its Cruise robotaxi division. The restructuring, according to CEO Mary Barra, is expected to save the company $1 billion annually.

- Beleaguered pharmacy chain Walgreens Boots Alliance WBA soared 17.7% on Tuesday after news broke that the firm has been in talks with New York-based private equity firm Sycamore Partners to sell itself and ultimately taken private.

- News broke that Outgoing U.S. Pres. Joe Biden plans to block the $14.1 billion acquisition of US Steel X by Japan's Nippon Steel on national security concerns once the CFIUS (Committee on Foreign Investment in the United States) refers the deal back to him with their view on the deal. Incoming President Donald Trump has also indicated that he would oppose this deal. US Steel stock gave up 9.7% on Tuesday.

A Pirate's Life for Me

Look who's trying to add a handle to a cup pattern? None other than the Walt Disney Company DIS. This moves the pivot from the left side of the cup to the right side of the cup. Now, obviously, we don't have a breakout just yet. The stock has come nicely off of the lows, but this is when it gets tough. We don't yet know the depth of the handle, but I would look to the 21-day exponential moving average as a potential first stop on the way down.

Other than that, relative strength is still strong, and the stock has just experienced a "golden" crossover by its 50-day simple moving average over its 200-day SMA. The daily Moving Average Convergence Divergence indicator has turned bearish, but that is expected when cup patterns try to become the more bullish cup with handle patterns. Should this turn out to be a handle and not an actual longer-term sell-off, and then a run be made at pivot, a target price of $141 would not be unreasonable.

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.69%.

07:00 - MBA Mortgage Applications (Weekly): Last 2.8% w/w.

08:30 - CPI (Nov): Expecting 0.3% m/m, Last 0.2% m/m.

08:30 - Core CPI (Nov): Expecting 0.3% m/m, Last 0.3% m/m.

08:30 - CPI (Nov): Expecting 2.8% y/y, Last 2.6% y/y.

08:30 - Core CPI (Nov): Expecting 3.3% y/y, Last 3.3% y/y.

10:30 - Oil Inventories (Weekly): Last -5.073M.

10:30 - Gasoline Stocks (Weekly): Last +2.362M.

13:00 - Ten Year Treasury Note Auction: $39B.

14:00 - Federal Budget Statement (Nov): Last $-257B.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

After the Close: ADBE (4.67), NDSN (2.59)

At the time of publication, Guilfoyle was long QUBT, QBTS equity.