Betting on a Rate Cut Might Not Be the Consensus, But Here’s Why it’s Likely

My interest rate projection appears to go against the grain.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It was only after my Thursday CNBC interview that I realized how non-consensus was my view that we are still more likely to get a cut than a hike this year.

We already argued, and it seems to be the case, that Kevin Warsh’s first Federal Reserve meeting removed much of the tail risk to the long end. But I think he plans to cut in September, and that the data, especially the data he chooses to focus on, let that happen.

Iran Attacks Resume, But Ceasefire Not Officially Broken

But first, back to Iran.

There were attacks from both sides, starting on Friday, but “surprisingly,” just as stock futures opened Sunday night, both sides have re-iterated their focus on concluding the memorandum of understanding (MOU) with a deal.

For now, my working assumption is that new round of attacks will not derail the discussions and that both sides were merely “flexing” to remind the other side of why they are at the table. If the ceasefire breaks down and the hostilities escalate and the oil trade is once again disrupted, then the odds of a September rate cut look bleak, but for now, that is not our base case on Iran.

There are two things that have not gotten the attention they deserve in respect to oil prices:

- The U.S. drained the strategic petroleum reserve (SPR) rapidly and to its limit, which kept oil prices capped, but that ability is largely gone, so something needed to be done.

- Providing sanction relief to Iranian oil may be as important as re-opening the Strait of Hormuz. Providing sanction relief not only brings more Iranian oil to the market than before, but it let’s them move the oil they were already sending (above sanctioned limits) with a higher degree of flexibility and transparency.

We covered Iran, Russia/Ukraine, Cuba and China in a recent podcast with Admirals Joyner and Whitworth: “Around the World Podcast” (iTunes and Spotify).

Iran remains fragile, but both sides seem to need the economics of what the ceasefire is providing, if not the economics of a full deal.

Questioning the AI Growth Story

We continue to see two economies: the AI and data center economy and the rest of the economy. The former has been generating the jobs, the growth and the earnings. The SOX Index (Philadelphia Semiconductor Index, as though anyone, anywhere doesn’t know what the SOX is at this time) hit a high on Monday before dropping almost 10% from there. We have started to see credit spreads widen too, for the big AI/data center issuers. Keep an eye on how credit markets are viewing this industry, as they seem to be showing some signs or being tired, if not concerned.

Micron’s (MU) earnings call helped generate a rebound on Thursday, but that proved to be short lived.

Questions are swirling around the spending. The cost of the buildout (more on that later); the utility of AI versus the cost of using AI. At some level, is the cost of using AI rising even faster than the benefits? I’m seeing some charts showing that token spending has dropped quite a bit in the past month (need to verify the accuracy of those charts), but it is believable.

The growing angst about AI and robotics (in our AI revolution pieces) continues to grow and is something the AI companies need to aggressively address before it becomes a problem (via legislation or taxes, for example).

This isn’t a debate that will be answered today, but it does seem the market is starting to rethink valuations. Stories were circulating that OpenAI may delay its highly anticipated IPO from this year into 2027. Since there is no official timetable, it is difficult to evaluate the veracity of such news, but it did little to help market sentiment.

Also, several people sent me links to news about an election in Utah and loss on their support of data centers. The AI revolution is a real risk to growth and possibly profitability (politicians may want to generate some tax revenue, etc).

I think the industry has to do an even better job of trying to address concerns, as politicians seem to be one of the bigger risks to their growth.

The Data Source Task Force

I think we will see a cut in September because:

With the war ending, inflation pressures will ease.

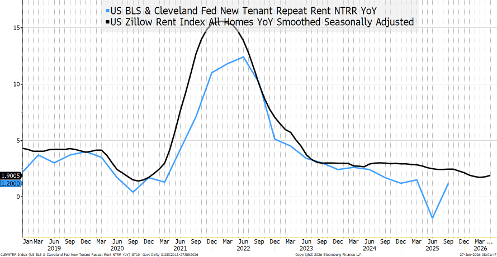

With “new” sources of data, it is easy to find data that seems reliable, that points to a much better inflation story than some of the existing data. I’ve mentioned “truflation” multiple times in the past. The truflation “core” is running at 1.5% and has been for months. When (AAPL) stock drops on a price increase, you know the market doubts the ability to pass on costs to the consumer. Finally, the Cleveland Fed has an estimate based on reality, of shelter inflation, that seems much more realistic than Owners Equivalent Rent (OER) used in CPI. It tracks Zillow and does not paint a story that housing inflation is a problem (unlike the OER).

Trump, and the entire administration, want rate cuts and they might be patient with Warsh, but ultimately he will be under pressure to deliver.

I think we have had “garbage in” turning to “garbage out” in the Fed for some time. Had Team Transitory relied on “better” (more accurate) data, it would have been much quicker to end easy money!

As mentioned at the start, given the response to my CNBC interview, so many people think Warsh is set to hike. I think not only the data, but the data we choose to use (which seems more accurate), will pave the way for a rate cut.

And keep an eye out on the AI/data center valuation story. I expect those sectors to come under pressure again this week.