Are We Just Killing Time Before We Take the Plunge?

With the market mired in complacency, let's look back to April and June to see what could shake us out of this. Plus, a reminder of an old Wall Street adage at this time of year.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

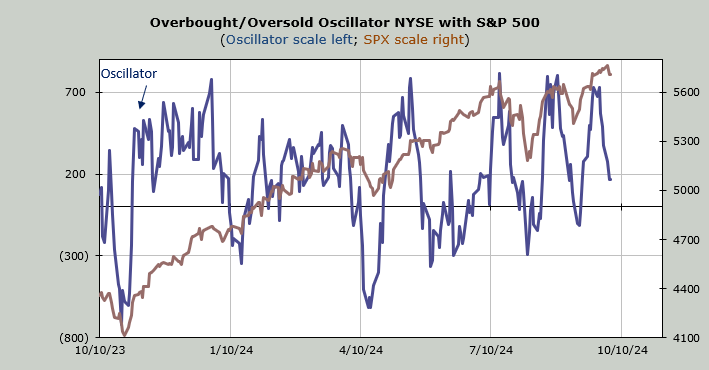

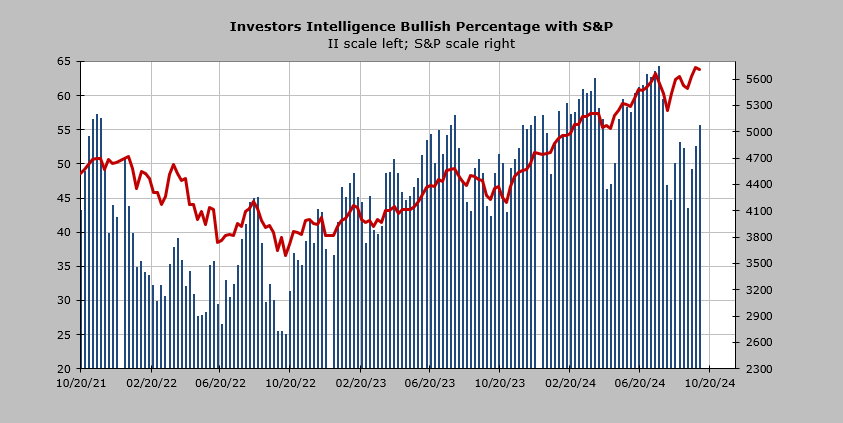

The S&P 500 has gone nowhere since the Fed meeting. The Nasdaq has gone nowhere since June. Yet since the Fed meeting the Investors Intelligence bulls are up six points to 55%. I think that spells complacency.

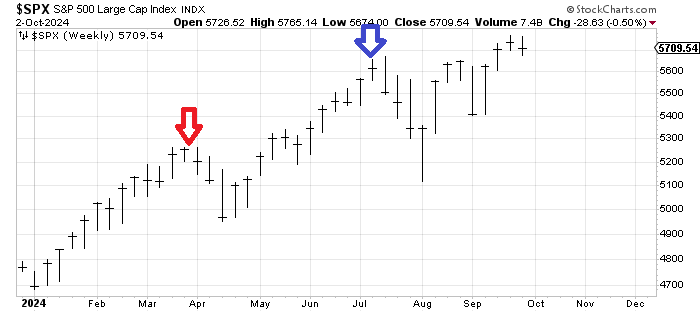

Sometimes it is easier to see the market on a weekly chart instead of the usual daily charts I show here. So once again let’s look at the chart of the S&P, but this time we’ll do something different. We’re going to count the weeks that it took for the correction in April and July to complete.

In mid-March the S&P got to 5250. The next week it toyed around up there but made very little progress. The next week it toyed there as well. Then the next two weeks saw the 5% correction (red arrow) in the chart below.

July saw something different. We got to 5650 and on the daily chart we did not retreat immediately but the very next week the S&P began its trip down. We saw three weeks of decline. The final week we saw a plunge to take the S&P down about 10%.

September’s decline was different because all we did was rally back to July’s high before we came down for a week (blue arrow)

But what’s the common theme here? Time. It takes time to get oversold. And that we tend to plunge at the end. That plunge at the end is typical because by the time a week or two of downside has been with us folks are starting to feel uneasy. Thus the plunge at the end is what tends to turn sentiment from uneasy to bearish. That plunge at the end is what tends to get the indicators toward an oversold condition.

And that plunge at the end is typically when the narrative changes. It’s when the "news" comes out that scares folks. And please don’t ask me what the news will be because my answer, as always will be, if we knew it already it would be priced in.

So far, all we’ve done is spend two weeks marking time. I would not consider Monday’s decline the sort of plunge that gets us oversold.

The plunge at the end — at least in these instances — did not see those Investors Intelligence bulls at 55% but rather closer to 43%. That’s quite a difference.

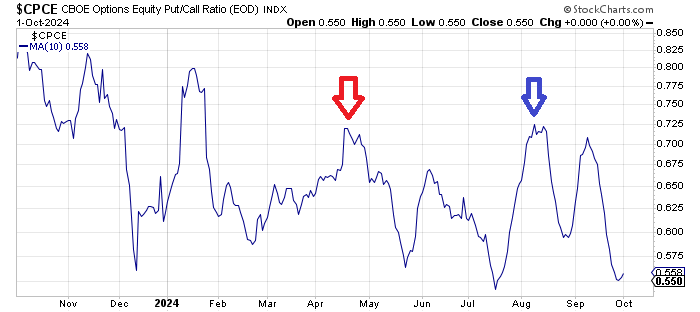

Those plunges at the end did not see the 10-day moving average of the put/call ratio at 0.55 where it is now but rather well over 0.70 (arrows on the chart).

I don’t have a strong view on what the market will do day to day here because it has been so choppy but I do sense to get those indicators to change the market is going to need more than just a chop sideways. Because that will not change sentiment.

Rosh Hashanah, the Jewish New Year, begins Thursday. First let me wish all who observe a Happy New Year. But next let me remind you that there is an old adage in the market: "Sell Rosh Hashanah and buy Yom Kippur." Yom Kippur is still 10 days from now.