Alphabet/Google Breakup? CPI Day, Risk-On Feeling, Doom & Gloom Forecasts

Should Google fear the reaper? And is the stock a buy here? Short-term, CPI will tell Wednesday's tale. It may or may not lean towards supporting short-term rate cuts. Long-term? Well...

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Now I know

I know that it's true

Don't say that this is the end

Instead of breaking up I wish that we were making up again

— " Breaking Up is Hard to Do" Greenfield, Sedaka (Neil Sedaka), 1960

DOJ Considering Splits-Ville for Alphabet

Tuesday afternoon, Bloomberg News ran a story reporting that the U.S. Department of Justice was considering a number of options, including the breakup of Alphabet GOOGL after a court decision last Monday ruled "that Google had illegally monopolized the markets of online search and search text ads." The shares fell overnight by as much as 2.5% but have rebounded to some degree as I work on this morning note through the dark hours. Both the DOJ and Alphabet/Google declined the opportunity to comment.

The ruling, made by Judge Amit Mehta of the U.S. District Court for the District of Columbia, found that Google had made $26 billion in payments to other companies to make its search engine the default option on smartphones and web browsers, which effectively blocked competitors from participating in these markets successfully.

A ban on such contracted exclusivity could very well be part of any resolutions as could the sharing of data by Google with competitors, but divesting the larger firm into separate businesses remains a possibility. If such a solution were to come to pass, the units most likely to be separated could be the Android operating system and/or the Chrome web browser. The AdWords platform that Google uses to sell text advertising could also be a target.

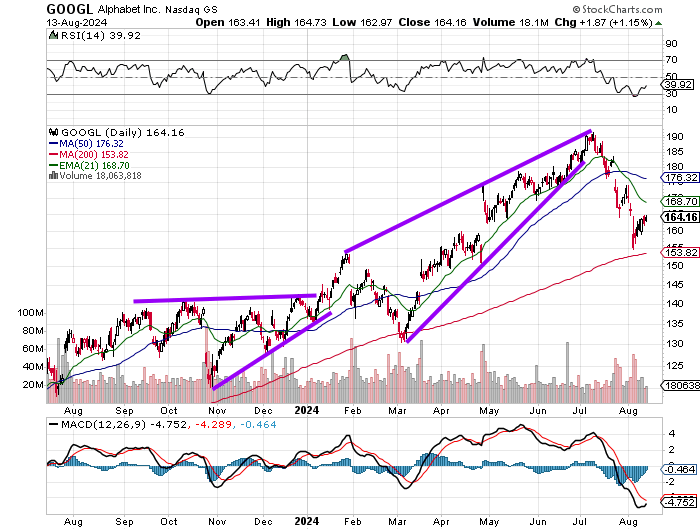

Readers will see that GOOGL has followed a bullish breakout from an ascending triangle pattern with a bearish breakdown following a rising wedge pattern. With these patterns apparently working like a charm technically for traders, all eyes are on what develops next.

The shares have found support at the 200-day simple moving average (SMA) and are now mired in between that line and its 50-day SMA. Traders really are thinking of those two lines as upside and downside pivot points with both a weak reading for Relative Strength and an awful, but possibly turning daily Moving Average Convergence Divergence (MACD) staring them in the face.

Is the stock a "buy" here? Perhaps if there is a breakup and enough of what made these businesses so profitable in the first place is left intact. Perhaps not if the legal fees mount and the businesses are handicapped whether or not they remain in-house or not. I'm not interested until one of those lines cracks.

Tuesday's Grace

Tuesday was a special day for our marketplace. The cooler-than-expected readings for both headline and core PPI on both a month-over-month and annual basis, unleashed a risk-on feeling that permeated both equity and Treasury markets, at least for a few hours, while leaving crude out of the joyful mix. The runway towards rate cuts runs clear into September from here, with the obvious potential for possible roadblocks apparent as soon as this morning's July CPI data, tomorrow morning's July Retail Sales data and next week's clown show in Jackson Hole.

The Nasdaq Composite ripped for a gain of 2.43% for the session, with the S&P 500 trailing behind at +1.68%. Starbucks SBUX led the S&P 500 for the day, gaining a whopping 24.5% after hiring Brian Niccol away from Chipotle Mexican Grill CMG to be the firm's next CEO. CMG, for that matter, was the S&P 500's worst performer on Tuesday, surrendering 7.5%. I got short SBUX equity on Tuesday and remain so. Every single mid-major to major U.S. equity index that I track closely gained at least 1% on Tuesday, with the Philadelphia Semiconductor Index out in front, up 4.18%, led again by Nvidia NVDA. The Dow Transports were the laggard, up exactly 1%.

Ten of the 11 S&P sector-select SPDR ETFs ended the day in the green with six of those ten up at least 1%. Technology XLK led the way, up 3.07%, while Energy XLE was the day's only loser as the threat of an expanded Middle East conflict hangs over those markets.

Minty Fresh

Winners beat losers by roughly 4 to 1 at the NYSE and by about 5 to 2 at the Nasdaq. Advancing volume took a commanding 79.3% share of composite NYSE-listed trade and a 73.2% share on composite Nasdaq-listed activity.

Now, this is the most interesting takeaway from Tuesday's trade. Aggregate trading volume was up 8.6% day over day across NYSE-listed securities and up 11.8% across Nasdaq-listed securities. Trading volume was also up 8.6% day over day across the constituency of the S&P 500.

Meaningful? Tuesday was the first day more active than the day prior since the panic driven August 5 massacre. Does that mean that the pros who literally had their faces melted ten days ago (including weekends) are sheepishly crawling back into their long positions at higher prices than they were liquidated at? Probably to some degree. The trading volume is still not where it was on those three successive beatdowns that only culminated on August 5.

Short-term, the CPI will tell Wednesday's tale. It may or may not lean towards supporting short-term rate cuts. Long-term? We have problems, and those rate cuts, while welcome, will be akin to putting lipstick on a pig. Oh, so pretty.

Doom & Gloom

On Tuesday, models released by both Goldman Sachs GS and JP Morgan JPM showed that the markets-implied likelihood of an economic contraction or recession had increased quite materially. Goldman's model has apparently increased the probability for a U.S. recession from 29% to 41%, while JP Morgan's model now shows a 31% chance for such a contraction, up from 20%.

As reported by Bloomberg News, rate markets are pricing in much higher probabilities for recession. According to Goldman's models, the 12-month forward implied change in the Fed Funds Rate alone is itself implying a 92% probability for recession. According to JP Morgan's models, the move in the yield for the U.S. 5-Year Note implies a 58% chance for an economic reversal.

I do not believe we, here at Market Recon and TheStreet Pro, were credited with being light years ahead of nearly everyone else on these likelihoods, though we clearly were. I say "nearly" everyone else, because as far as I know, Stephanie Pomboy of MacroMavens has been out in front of everyone preaching her brand of macroeconomic common sense. Now stop what you're doing and raise a glass of orange juice or cup of "Joe" to Stephanie.

Oncoming Train

Just a couple of hours away. CPI-day. Whoop-de-"darn"-doo.

So, the month-over-month data should accelerate just a bit, while the year-over-year data cool just a smidge. Meanwhile, we all know that back at the ranch, honest economists, you know, the ones that don't pretend GDI doesn't exist, prepare for an overt reacceleration in consumer prices at least due to base effects if not anything else, this autumn. All that matters, though, is getting to September 18 and getting rate cuts started ahead of the U.S. election.

Just snap that rubber band on, flick those veins, enter and squeeze. Oh, yeah. The junkies up and down Wall Street will roar in delight.

(Don't Fear) The Reaper

All of our times have come

Here but now they're gone

Seasons don't fear the reaper

Nor do the wind, the sun or the rain

We can be like they are

— Roesner (Blue Oyster Cult), 1976

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.55%.

07:00 - MBA Mortgage Applications (Weekly): Last 6.9% w/w.

08:30 - CPI (July): Expecting 0.2% m/m, Last -0.1% m/m.

08:30 - Core CPI (July): Expecting 0.2% m/m, Last 0.1% m/m.

08:30 - CPI (July): Expecting 2.9% y/y, Last 3.0% y/y.

08:30 - Core CPI (July): Expecting 3.2% y/y, Last 3.3% y/y.

10:30 - Oil Inventories (Weekly): Last -3.728M.

10:30 - Gasoline Stocks (Weekly): Last +1.34M.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: EAT (1.72), CAH (1.73)

After the Close: CSCO (0.85), STNE (1.52)

At the time of publication, Guilfoyle was long NVDA equity; short SBUX equity.