All Eyes on Jackson Hole, Heading into Cash, Losers Beat Winners

As the economic world's attention turns to Jerome Powell's speech from Wyoming, more than a few investors have been raising cash.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Zero Dark Thirty. Quiet. Even earlier, even quieter out west. August. Every August. Late in the month. The landscapes are majestic, the trout are swimming. The warm jackets betray the summer season and signal the coming of autumn. Cowboy hats lend some levity to the moment at hand. A tradition dating back to 1978, year of the New York Yankees and Pittsburgh Steelers. The Kansas City Fed hosts and has hosted some of the most powerful central bankers in the nation and the world. That world, in turn, focuses on the mountain resort town of Jackson Hole, Wyoming for just a few days.

Today, Jeffrey Schmid welcomes Fed Chair Jerome Powell to the podium surrounded by financial media types. Past regional presidents have reached near-celebrity status in welcoming Powell and other Fed chairs on past Friday mornings of this annual event. Recent names such as Esther George and Tom Hoenig come to mind as do Janet Yellen, Ben Bernanke and Alan Greenspan.

Today Is That Day

At 10 a.m. or so, Eastern Time, Fed Chair Jerome Powell will stand before a few dozen financial journalists in his field of vision, and tens of millions of Fed watchers out of his sight. What he says will impact not just a few hundred million here in the US, but most of the human population in one way or another. The world has been expecting an inflection point, here at Jackson Hole today, as the head of the Federal Reserve Bank almost certainly will signal a shift in policy from a higher for longer stance on short-term interest rates to the start of what many expect to be a new cycle of easier money.

Will Powell signal an initial rate cut on September 18, 2024 of 25 or 50 basis points? My thought is that his speech will not be that detailed. The theme of this year's symposium is "Reassessing the Effectiveness and Transmission of Monetary Policy." If the chair feels that he needs to buy time, he can fall back on that theme and risk disappointing financial markets. It felt like a number of portfolio managers and traders were trying to front-run such disappointment on Thursday.

We all know that consumer level inflation is cooling. That said, inflation is running hotter than the Fed's target, and cumulative inflation over the past three years is still the stuff of cheap horror movies. We all know that demand for labor is cooling. In a rude slap to the face, this week, we learned without a shadow of doubt that labor markets were never even close to as hot as we once thought, as we were led to believe. Though a few of us did know better. Hopefully, Powell, at least privately, knew better.

For today is Friday. A day, like any other day. Before lunchtime on the east coast, the entire financial landscape of a nation and maybe a planet could change, unlike the eternally beautiful landscape of the Teton Mountain Range standing above a valley. A valley where a handful of economists and policy makers have gathered.

They Said What?

On Thursday, a few central bankers met with the financial press. One day ahead of Chair Powell's main address.

Boston Fed President Susan Collins said, "I do think that recalibrating begins to be important, but I would envision doing that gradually. There isn't a preset path."

Philadelphia Fed Presisdent Patrick Harker said, "In September we need to start a process of moving rates down. We need to start bringing them down methodically."

But...

Kansas City Fed President Jeffrey Schmid said, "It makes sense for me to really look at some of the data that comes in the next few weeks. Before we act — at least before I act or recommend acting — I think we need to see a little bit more."

How interesting is all of this? Collins, whom I still don't know as well as I do most central bankers, seems ready to start cutting rates, as does Harker, whom I have never really thought of as a dove nor a hawk, but as a pragmatist. Then there is Schmid, who is still sort of new in his position and whose policy views I would not know from a hole in the wall. So, how interesting is it that Schmid would come off as the hawk of the group, in the fine tradition of both of his immediate predecessors at the helm in Kansas City? That would be noted hawk Esther George and the less-than-truly Keynesian economist Tom Hoenig.

Heading into Cash

Just as interesting as what these Fed heads said on Thursday was the news that another $24.9 billion had been stashed in U.S. money market funds during the week through August 21, 2024. The data comes from data provided by the Investment Company Institute, which I read about at the Bloomberg News website.

This brought inflows for the month of August up to $106 billion and a record $6.25 trillion in these funds in aggregate. It is believed that there was a push to capture the last bit of lofty yields paid for short-term dough ahead of Powell's speech and ahead of the September FOMC policy meeting. I will admit to having raised some cash this week myself. Just a little risk management.

Marketplace

On Thursday, it looked like more than a few of us were raising cash levels. Not only did Treasury yields back up — the U.S. ten-year and two-year notes to 3.87% and 4.03%, respectively — but equities were slapped around as well. The S&P 500 gave up 0.89%, as the Nasdaq Composite surrendered 1.67%, the worst day for that index since the panicked beat-down of August 5, 2024.

Among mid-major to major equity indices, only the KBW Bank Index closed in the green. The rest of the indices in our field of view went south for the day, led by the Philadelphia Semiconductor Index. That index took a beating of 3.44% as Intel INTC was beaten severely, down 6.12% on news that board member Lip-Bu Tan, former CEO of Cadence Design CDNS, had stepped down from that seat. A plethora of high-profile chip stocks gave up 3% or more for the Thursday regular session.

Seven of the 11 S&P sector SPDR ETFs closed out Thursday in the red, led lower by Technology XLK and the Discretionaries XLY. Those two finished down 2.3% and 1.73%, respectively. The REITs XLRE led the winners, up 0.61% for the day, but performance was fairly evenly split between defensive sectors and the cyclicals. Growth type sectors had a tough day.

Breadth

Losers beat winners by a two-to-one margin at the NYSE and by about nine-to-four at the Nasdaq. Advancing volume took a 27.7% share of composite NYSE-listed trade and a 36.6% share of composite Nasdaq-listed activity. Aggregate trading volume was a bit quirky. Again. Activity across was down 4.4% day over day for both NYSE-listings and the membership of the S&P 500. The S&P 500 still has not reached its 50-day trading volume simple moving average since August 8, 2024. That's ten straight regular trading sessions of decreasing trade. That said, aggregate trade across Nasdaq-listings was up 6.3% day over day. The Composite has not hit its 50-day trading volume SMA since August 9, 2024.

Question?

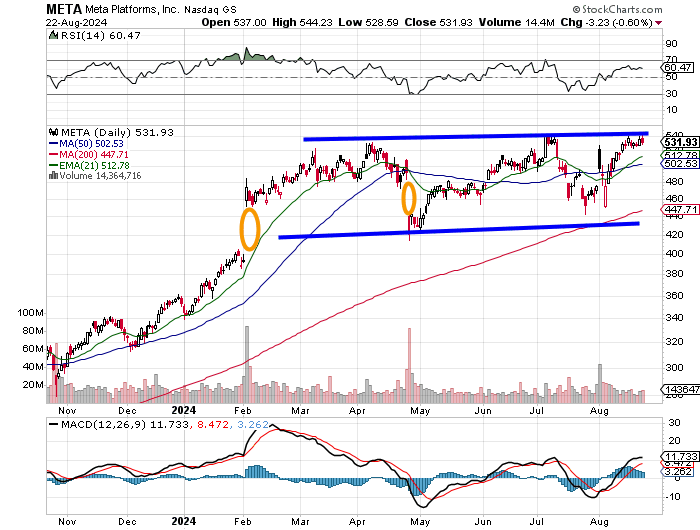

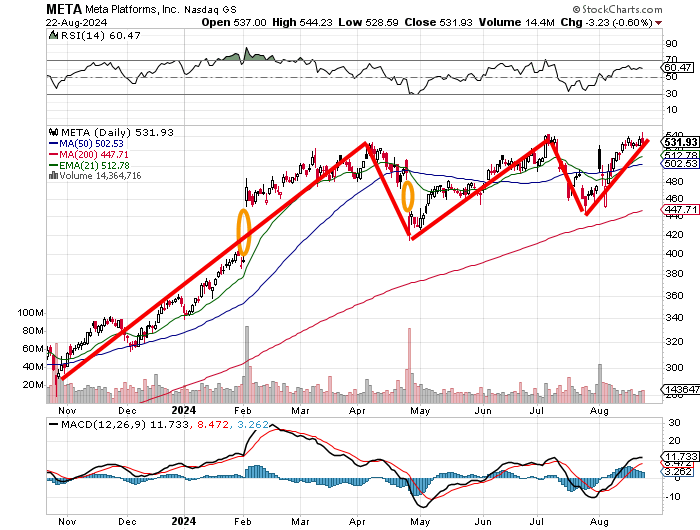

The stock is Meta Platforms META. Do you see a stock trying to break out to the upside from a basing period of consolidation?

Or do you see a stock forming a nearly perfect triple top bearish reversal?

I'm really not sure. If you're in this one, understand that the stock is at a point of inflection going forward. Both of these outcomes will be easy to explain in hindsight. The road not taken will then be forgotten eternally.

Economics (All Times Eastern)

10:00 - New Home Sales (July): Expecting 629,000, Last 617,000 SAAR.

13:00 - Baker Hughes Total Rig Count (Weekly): Last 586.

13:00 - Baker Hughes Oil Rig Count (Weekly): Last 483.

The Fed (All Times Eastern)

All Day - Jackson Hole Economic Symposium.

10:00 - Speaker: Federal Reserve Chair Jerome Powell.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: BKE (.80)

At the time of publication, Guilfoyle had no positions in any securities mentioned.