A Math Problem From the Bureau of Economic Analysis and a Word Problem for the Fed

Apparently, suddenly, those GDP, GDI numbers add up ... so why the big rate cut? Also, a look at Wells Fargo, and a prayer for Hurricane Helene's victims.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Hurricane Helene -- the storm that we've all been tracking for several days now, made landfall late Thursday evening in Florida's "Big Bend" region as a Category 4 hurricane. Winds at the time were whipping around at 140 mph. Helene was the strongest hurricane to hit the Big Bend on record, though it was the third significant hurricane to hit the region in 13 months. There are reports of tremendous suffering due to the storm surge along Florida's panhandle, around the bend and down the Florida peninsula's western shoreline.

Then there is the historical flooding up through that part of Florida into the western parts of Georgia, South Carolina, North Carolina, and eastern Tennessee as well as parts of Alabama and even Virginia due to unrelenting rainfall. I am sure by now that the damage has spread beyond those areas just mentioned. On the east coast of Florida, where I am, we were lucky. I have power, and I only lost a large branch of my Southern Oak that hit but appears to not have damaged my home. If you're reading this, I hope that means that you too, have power this morning and are able to work rather than recover.

Before we proceed with our daily routines, as if nothing just happened ... let's take a moment to think of, and if so motivated, say a prayer for the welfare of those suffering and the safety of those still in peril as this storm continues to pound those living in its path.

Not What I Expected: GDP, GDI Surprise

Color me surprised. I have written it and said it publicly many times. Conceptually and algebraically, GDP (gross domestic product) and GDI (gross domestic income) must equal out and one acts as a check upon the other. When the two are far apart, the Fed encourages those discussing economic growth to not rely upon one or the other, but to average the two.

I had told you that the math did not add up (on that, I was correct), and that GDP from the start of 2023 would have to be revised towards GDI as the two told different stories. What I did not see coming was an upward revision to both GDP and GDI that would improve the way the past couple of years look in hindsight. GDP and GDI would end up closer together, which was necessary, but it was the GDI that underwent the larger and surprisingly upward revision.

For the second quarter, the Bureau of Economic Analysis confirmed GDP growth of 3.0% quarter over quarter at a seasonally adjusted annual rate, while GDI was revised up to growth of 3.4% from the previous revision of just 1.3%, I kid you not. This was the result of a sizable boost to the BEA's input for inflation-adjusted disposable income. The savings rate for that quarter was increased from 3.3% to 5.2%. Again, I kid you not.

For the first quarter, GDP was revised to quarter-over-quarter (SAAR) growth of 1.6%, up from 1.4%, while GDI was revised from growth of 1.4% to growth of 3.0%. Incredibly I am not done. The full year of 2023 was revised, as well. This kind of comprehensive revision is performed annually, so the fact that we are going back and "redoing" past math is not a surprise. What is surprising to me is the direction and size of these revisions as they do not match the anecdotal evidence and periodical data that we have worked off of and traded off of for years now.

On that note, for the full year of 2023, GDP growth was revised to 2.9% from 2.5%, while GDI growth was revised from 0.4% to 1.7%. That takes growth for 2023 from 1.45% done the Fed's way of averaging the two up to 2.3%. GDP growth for the full year of 2022 was revised as well, from 1.9% to 2.5% as 2022 GDI growth was taken from 2.1% to 2.8%.

It's really quite incredible. According to the data, the economy has been much stronger than what we were told, and we, or at least I did not trust what we were told at the time. Do we trust the data now? I think, while as economists, we should always check the data. I did know the math was off a rough 18 months before the BEA acknowledged it. As a trader, what have I always preached?

We trade the environment provided, not the one we want, or the one that we think should exist. Therefore, the data are the data, and the algorithms that control price discovery do not recognize opinion. They only read and react to data. My friends and relatives all tell me how tough it is out there and have been telling me this since the start of 2023. I do not doubt their sincerity. Someone else out there must be doing better than just fine. That's all.

That Does Beg the Question ...

Why on earth, if the economy is this strong, is the Fed easing policy and cutting short-term interest rates? No wonder, they still have not adequately explained themselves. Powell did not touch policy in his address on Thursday. There clearly is, if these numbers are on the up and up, no reason whatsoever, to ease policy.

Why on earth, if the economy is this strong, is the Fed easing policy and cutting short-term interest rates?

About Time...

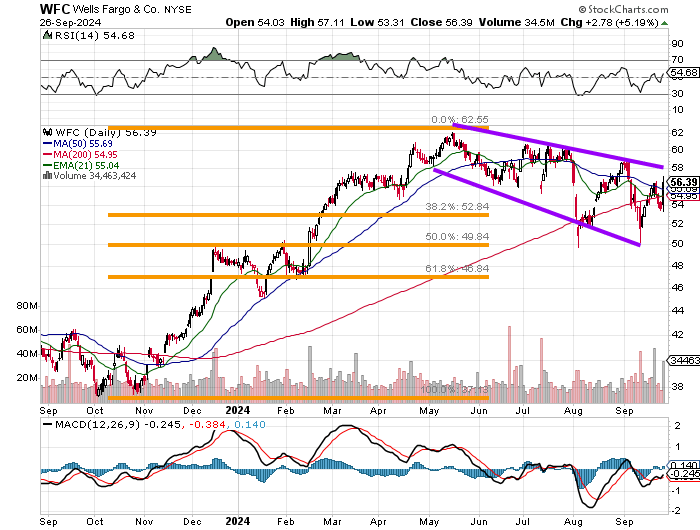

Bloomberg News broke the story on Thursday that Wells Fargo WFC had submitted a third-party review of the bank's risk and control overhauls to the Federal Reserve Bank for the central bank's analysis and, we hope, approval. This is why shares of the San Francisco-based money center bank soared 5.2% on Thursday.

A best-case result for Wells Fargo would be the eventual removal of the asset cap imposed by the Fed on Wells Fargo by Janet Yellen's Fed after a series of scandals under a completely different management team had damaged the bank's reputation. This submission is a sign of progress, and was necessary after stories had recently made the rounds that Wells Fargo had suffered some regulatory setbacks. Should the approximate $1.95 billion cap be lifted, it is likely a 2025 story at the soonest. Still, any progress is welcome. It has been six years.

Readers will see that Wells Fargo has found support twice in 2024 at the "half-way" back retracement level of the October 2023 through May 2024 rally. The stock then developed a falling wedge pattern, which is a pattern of bullish reversal. The downward sloping line of resistance is currently at $58, so there is some wood to chop to the stock's immediate front. That said, WFC took back its 21-day exponential moving average, 50-day simple moving average, and the 200-day simple moving average, all in one session on Thursday. The key is at this time to hold those lines going into the weekend. I remain long this stock with a $69 target price.

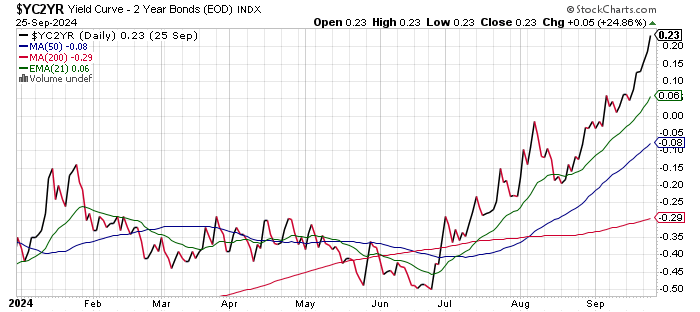

The rapidly steepening yield curve would be a driving force behind an improved outlook for net interest margin, which is something Wells Fargo is more reliant upon than are some of the other large money centers. Yes, I know. Many of the banks have projected a narrowing net interest margin is a rate cutting environment. While cognizant of this expectation, I might argue that should the long end of the curve be left exposed to the forces of free market price discovery while the Fed pressures short-term rates, in an over-indebted federal and corporate environment, the opposite may just play out.

Anyone Else Notice What Happened in China?

On Thursday, the Pentagon confirmed reports that a Chinese Navy nuclear powered submarine sunk at a shipyard in the inland city of Wuhan back in May or June. It remains unclear if the sub was carrying nuclear fuel at the time.

Elsewhere at Oracle

On Thursday, Oracle ORCL announced that Advanced Micro Devices AMD had been selected to provide Instinct MI300X accelerators to power its new OCI Compute Supercluster Instance. The Oracle Cloud Infrastructure Supercluster provides a high-performance AI environment for training, tuning and deploying generative AI models.

This is a large win for AMD. On Thursday, the Philadelphia Semiconductor Index popped for a gain of 3.47%, leading U.S. major and mid-major equity indexes on what was a strong session on elevated trading volume. Micron MU led the semis on Thursday, gaining 14.73% after releasing both strong earnings and strong guidance. AMD gained 3.38% for the day. I remain long AMD and short MU.

Note To Readers: I'm on the Diary

If you want to hang out or trade ideas with myself or with Doug's crew, I will be subbing for Doug Kass at his Diary today.

Economics (All Times Eastern)

08:30 a.m. - Personal Income (Aug): Expecting 0.4% m/m, Last 0.3% m/m.

08:30 - Consumer Spending (Aug): Expecting 0.3% m/m, Last 0.5% m/m.

08:30 - PCE Price Index (Aug): Expecting 0.2% m/m, Last 0.2% m/m.

08:30 - Core PCE Price Index (Aug): Expecting 0.2% m/m, 0.2% m/m.

08:30 - PCE Price Index (Aug): Expecting 1.7% y/y, Last 1.7% y/y.

08:30 - Core PCE Price Index (Aug): Expecting 1.6% y/y, Last 1.5% y/y.

10:00 - Wholesale Inventories (Aug-adv): Expecting 0.2% m/m, Last 0.2% m/m.

10:00 - U of M Consumer Sentiment (Sep-F): Flashed 69.0.

10:00 - U of M One Year Inflation Expectations (Sep-F): Flashed 3.1%.

10:00 - U of M Five Year Inflation Expectations (Sep-F): Flashed 2.7%.

1:00 - Baker Hughes Total Rig Count (Weekly): Last 588.

1:00 - Baker Hughes Oil Rig Count (Weekly): Last 488.

The Fed (All Times Eastern)

13:15 - Speaker: Reserve Board Gov. Michelle Bowman.

Today's Earnings Highlights (Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle was long WFC, AMD equity. Short MU equity.