A Farewell to Pres. Carter, Charting Santa's Rally, and Previewing the Week Ahead

Let's see why the Santa Claus rally isn't quite dead yet, and why the former president should be remembered for the great man he was.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

A great man passed away on Sunday. He died at the age of 100, at his home, in the state of Georgia. President James Earl Carter Jr or "Jimmy" was a graduate of the United States Naval Academy, a peanut farmer, and a former governor. He had been elected the 39th president of the United States in 1976. His term was not one of the better four year stretches in U.S. history. While he was key to bringing a lasting peace to the relationship between Israel and Egypt, the late 1970s were known domestically for runaway consumer-level inflation, very high interest rates and rising unemployment.

After the global embarrassment of the Iran hostage crisis in 1979, there was no way Carter could recover politically, and in 1980, he was defeated in his bid for re-election in a landslide by Ronald W. Reagan, who became the 40th U.S. president. Reagan took 44 states in the electoral college that year, leaving Carter with just six, plus the District of Columbia. Carter landed just 41% of the popular vote that year after taking slightly more than 50% four years earlier.

No, President Carter was never thought of as an especially effective president. He was, however, universally thought of as a very good human being and perhaps the very best former president in modern U.S. history. Carter, who was awarded the Nobel Peace Prize in 2022, spent the decades following his time in office advocating for human rights, building homes for those less fortunate, working toward eradicating disease, and generally working on advancing varied humanitarian causes.

I choose not to remember the president that left office in January of 1981 on this first full day following his death. I choose to remember the deeply religious man who was by all accounts a great family man, who spent an incredible 77 years as half of a married couple that would set an example for all other married couples to follow, and a man that given his platform, lived his core beliefs and made a positive impact literally everywhere he could. Rest in peace, Mr. President. You've done well here on earth.

Market Impact

As for market impact, when a former U.S. president passes, there has traditionally been, and I would expect that there will be, a National Day of Mourning. U.S. financial markets, out of respect, typically do not open on such days.

The Week Past

For equities, the past week, which really amounted to just three-and-a-half regular trading sessions spread out over five days, closed on weakness what had been a strong start to the Santa Claus rally period. There was weakness in U.S. Treasury markets as the Ten-Year Note paid as much as 4.63% late Friday and the Two-Year Note paid 4.33%. On that, U.S. Treasury debt securities have shown some moderate strength overnight Sunday into Monday morning.

Concerning the macro, November durable goods orders badly missed expectations, but within that report, core capital goods orders were strong. November new home sales printed up from October, but below consensus view. The Conference Board's consumer sentiment survey fell well short of projections and printed down sharply from October. Late in the week, initial jobless claims remained in check, meaning that jobs are not yet being lost in huge numbers, continuing jobless claims hit a post-pandemic high. The implication there is that once an individual loses a job, finding a new one is becoming increasingly difficult.

Friday was a tough day, as trading volumes remained light, but there was definitely some movement in capital flows. As certain funds more than likely used the time to reallocate exposure, this movement probably had a greater impact on the headline equity indexes than it might have at any other time. Still, these changes in allocation are often made quarterly or semi-annually and done so at or around the turn of the page of the calendar. This week we'll probably see more of this, but we'll also see trading volumes increase. Though there is also a holiday this week, traders tend to return to work this week, especially those with children as elementary school kids will return to class this Thursday.

Marketplace

Among the major to mid-major U.S. equity indexes last week:

- The S&P 500 gave up 1.11% on Friday but still closed the week up 0.67%. The S&P 500 is up 25.18% year to date.

- The Nasdaq Composite gave up 1.49% on Friday but still closed the week up 0.76%. The Nasdaq Composite is up 31.38% year to date.

- The Russell 2000 gave up 1.56% on Friday, still closing the week up 0.1%. The Russell 2000 is up 10.73% year to date.

- The Dow Transports gave up 0.46% on Friday but closed the week up 0.87%. The Dow Transports are up just 0.83% year to date.

- The Philly Semiconductors gave up 1.01% on Friday, still closing the week up 3.18%. The Philly Semiconductors are up 22.69% year to date.

On Friday, all 11 S&P sector SPDR exchange-traded funds closed in the red, with Consumer Discretionaries XLY and Technology XLK both giving up more than 1% for the session. Energy XLE closed down just 0.01% on Friday.

For the week, six of the eleven S&P sector SPDR ETFs closed in the green, despite Friday's sell-off. Nothing really moved all that far over the week, as Health Care XLV led the winners, up 0.69% and the Staples XLP lagged behind at -0.8%.

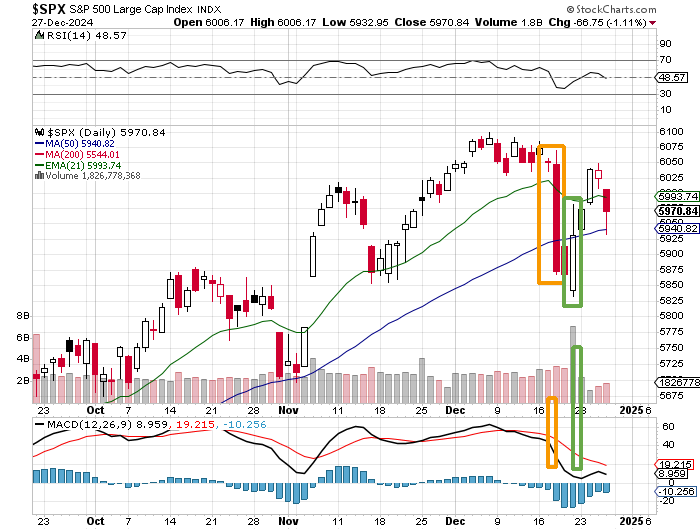

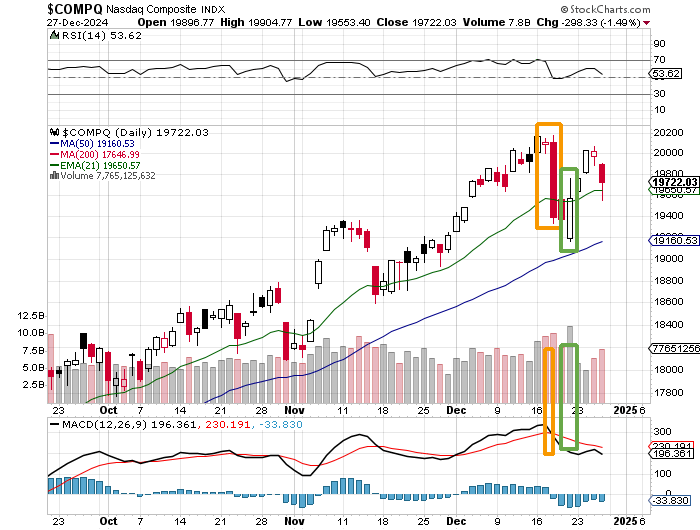

Santa's Rally Lives, For Now

The Santa Claus Rally isn't quite dead. At least not yet. Check out these charts:

Readers will see that while the S&P 500 closed out the week on a two-day losing streak, that the last sale remained well above the lows of the Friday prior to last Friday. That was where the index experienced its upward change of trend on greatly increased trading volume. The daily Moving Average Convergence Divergence is still postured quite bearishly, but we'll see this week, just how key that support that showed up on Friday at the S&P 500's 50-day Simple Moving Average was.

Here, readers will see that the Nasdaq Composite found support at its 21-day exponential moving average on Friday rather than its more important 50-day simple moving average. Is this a negative, because that 50-day line still has to be tested, or a positive, because this index is simply in better shape than the S&P 500? That is the question heading into the new week.

The Week Ahead

There's not a lot on the schedule again this week, though, with more bodies aboard, there should be more activity. For a second consecutive week, there are no significant quarterly corporate earnings set for release. Last week, there were no Fed speakers to be found, or heard from. This week, I only saw one on the schedule at this time. Richmond Fed Pres. Tom Barkin will speak on Friday.

The macro will be on the light side as well. December Jobs Day will not occur until next Friday. That leaves the Chicago PMI this morning, the Case-Shiller and Federal Housing Finance Agency's housing price index tomorrow, the weekly report on jobless claims on Thursday and the ISM Manufacturing Index for December on Friday. That's about it.

Economics (All Times Eastern)

09:45 - Chicago PMI (Dec): Expecting 42.7, Last 40.2.

10:00 - Pending Home Sales (Nov): Expecting 0.8% m/m, Last 2.0% m/m.

10:30 - Dallas Fed Manufacturing Index (Dec): Expecting -0.4, Last -2.7.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle had no position in any security mentioned.