A Cautionary Tale, 'Insane' Blackwell Demand, Nvidia and AMD Breakout?

Let's discuss the tentativeness in the market, including the suddenly strong dollar. Plus, Jensen Huang wows them again, a tale of two potential AI-related breakouts, and more.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Caution. Tentative might be the right word. For there certainly seemed to be a hesitancy or lack of confidence in the trade of U.S. equities on Wednesday.

A day after Iran had launched its largest attack on Israel in history, quite unsuccessfully, I might add, oil traded much higher with front-month Brent (December) reaching above $74 per barrel and front-month WTI (November) moving past $71 per barrel. Both have held those gains overnight despite a suddenly strong U.S. Dollar Index.

The "dixie," which traded just above 100 on Monday, is at the point very early on Thursday morning where it won't take much to touch the 102 level. It's been more than six weeks since the greenback was so valuable versus that basket of reserve currency peers.

It is not just one reserve currency that's up against the dollar this week. The dollar is up against the euro, up against the yen, up against the pound, up against the Swiss franc, and up against the Canadian dollar. The U.S. dollar is also up against the currencies of key trading partners such as the Chinese yuan and Mexican peso, though those two are not part of the index.

What gives?

Some stronger-than-expected domestic macroeconomic data and an increase in inflationary forces (geopolitical risk, punishing organized labor strikes, the impacts of Hurricane Helene) that might impact the ability of the FOMC to be as dovish as they have intended to be.

Oddly, or maybe naturally, as the U.S. dollar has served as a safe-haven currency during this time of heightened geopolitical tension, U.S. Treasuries have struggled, and even sold off a little. Perhaps not because U.S. sovereign debt has lost its safe-haven value (though considering U.S. debt levels, this eventuality is a "when" and not an "if") but is more a reaction to Fed Funds futures markets in Chicago reflecting a more hawkish path for U.S. short-term interest rates going forward.

This morning, those futures markets are pricing in a 66% probability for just a 25-basis point rate cut for the November 7 FOMC policy decision, and a 34% likelihood for a 50-basis point cut. That's a reversal from just a few days ago. That said, these markets are still pricing in a 62% probability for 75-basis points worth of rate cuts by year's end.

A lot in terms of expectations for monetary policy and currency exchange rate valuations is likely riding on this Friday's BLS September employment surveys, as flawed as we know them to be.

That Said...

On Wednesday, ADP reported a net 143,000 private sector jobs were created in September. Though not an eye-popping number, this was considerably better than the 125,000 or so that Wall Street was looking for and up sharply from the revised August print of 103,000.

More signs of caution... all of the gains made can be attributed to larger employees. Small businesses (defined by ADP as employers of less than 50 individuals), which in aggregate, have always been the largest employers in the U.S., have now shown negative job creation for three consecutive months.

A Hawkish Turn

Richmond Fed President Tom Barkin, who votes on policy this year and did vote for a 50-basis point rate cut in September, spoke on Wednesday. He has appeared, at least to me in the past, to be quite pragmatic on policy. Barkin sounded as if he does actually see the worm starting to turn as do we. Remember, I have been telling you that consumer-level inflation on a year-over-year basis, had very likely bottomed in September for 2024. Inflation will start to rise, I believe as soon as October, and on into the first half of 2025.

From Wilmington, North Carolina, Barkin said, "It remains difficult to say that the inflation battle has yet been won." Barkin added, "Victory means different things to different people, and — while we have made real progress — there remains significant uncertainty on both inflation and employment."

Barkin cited certain concerns... "Recent union actions or a pullback in labor supply" and of course... "Deglobalization could increase import Prices" and "The conflict in the Middle East could worsen."

Separately, interviewed on Bloomberg TV a day after his firm's investor day, Apollo Global Management APO CEO Marc Rowan was also cautious. Rowan commented: "Financing is available, real estate prices are going up. It is not clear we need more rate cuts." Then he almost scolded the Federal Reserve, adding, "To the extent we accelerate the economy and have to go in the other direction, that would not be a good day."

'The Fonz' Wows Them Again

You guys see or hear that Jensen Huang interview on CNBC late Wednesday? I had just come in from playing some less-than-serious post-closing bell pickleball and I noticed the Nvidia NVDA CEO on my screen. "The Fonz" was wearing his leather jacket, but no shades. What he said was music to investors' ears. Huang has a knack for that.

The CEO said, "Blackwell is in full production. Blackwell is as planned, and the demand for Blackwell is insane." I thought of Crazy Eddie for a moment. Huang added..."Everybody wants to have the most, and everybody wants to be first."

He did not stop there. "We're updating our platform every single year. If we can increase the performance, like we've done for Hopper and Blackwell, we're effectively increasing the revenue or throughput for our customers on these infrastructures by a couple to three times each year."

Hmm, hyper-scalers are estimated to spend roughly $160 billion on AI infrastructure for 2024 by year's end.

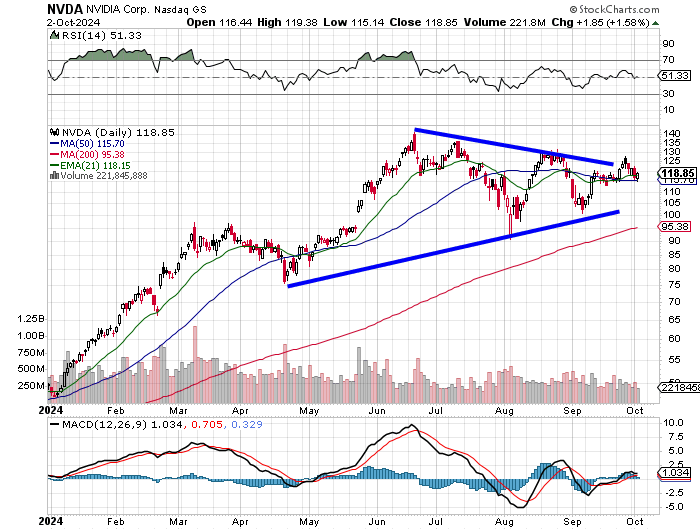

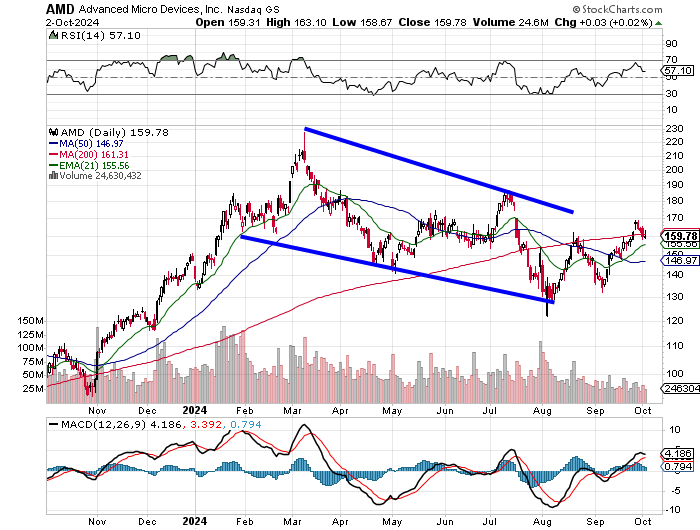

A Tale of Two Potential AI-Related Breakouts

Our favorite and second favorite AI-capable chip-designing stocks are near technical breakouts, or breakdowns. Both of these stocks are at the point on their charts where to go higher they will have to exit the pattern that they have been trading in.

Nvidia NVDA threatens to break out of a long pennant pattern, making use of its 50-day simple moving average (SMA) as support and exhibiting a daily Moving Average Convergence Divergence (MACD) with all three components above the zero-bound and with the 12-day line above the 26-day line.

Advanced Micro Devices AMD appears to be trying to break out of a falling wedge pattern (which is a pattern of bullish reversal) that has morphed into a double-bottom pattern (also a pattern of bullish reversal). Here too, the daily MACD is supportive of an attempted move to the upside, but crucially... the stock is fighting to hold on to its 200-day SMA. As we know, this line can force risk managers to pressure portfolio managers into making decisions based on fear, so this is key to watch today. AMD is trading below that line but has not lost contact.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 220K, Last 218K.

08:30 - Continuing Claims (Weekly): Last 1.834M.

09:45 - S&P Global Services PMI (Sep-F): Flashed 54.4.

10:00 - ISM Non-Manufacturing Index (Sep): Expecting 51.5, Last 51.5.

10:00 - Factory Orders (Aug): Expecting 0.1% m/m, Last 5.0% m/m.

10:30 - Natural Gas Inventories (Weekly): Last +47B cf.

The Fed (All Times Eastern)

10:40 - Speaker: Atlanta Fed Pres. Raphael Bostic.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: STZ (4.08)

At the time of publication, Guilfoyle was long NVDA and AMD equity.