The Week Ahead, Safety Dance, Scary Household Debt, Earnings and Valuation

What a week we had. Ready for another? Here's your five-paragraph order. Would I be surprised to see equity markets contract a bit this week? Of course not.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

"You've gotta ask yourself a question:

'Do I feel lucky?'

Well, do ya, punk?"

- Clint Eastwood as Inspector Harry Callahan (Dirty Harry), 1971

The Week That Was

How do we even begin? What a week.

I started last Monday's Morning Recon note off with the lyrics to the Judas Priest classic, "Some Heads Are Gonna Roll"... and roll they did, but only for a little while. By this past Friday, after rallying to one degree or another on a nearly day-by-day basis, the S&P 500 and Nasdaq Composite were barely down for the week. The Nasdaq 100 was actually green for the week for crying out loud.

Treasury yields plummeted the week prior into last Monday, but then bond traders sold Treasuries all week long after that. No, yields are not yet back where they probably belong, but traders realized that and took action. Did you see the lack of domestic demand for last week's 10-Year Note and 30-Year Bond auctions? Really, what a week.

Let's not forget. We're probably not "okay" just yet. The economy isn't in the clear just because initial jobless claims contracted one week to the next and the services side of the economy showed some growth. Sure, the macro was better last week than it had been the week prior, which is how traders across not just U.S., but global financial markets found themselves in a pickle just a week ago. Would I be surprised to see equity markets contract a bit this week? Of course not.

First there was a full week of soft-looking U.S. macro, including a very weak employment report for July that probably overstated labor market strength. Then there was the surprise rate hike by what appears to be a panicked Bank of Japan. What are they to do? They don't know and neither do I. Japanese inflation is out of Pandora's box and that economy is mired in a state of recession. The yen was marching toward worthlessness, and the BOJ tightened policy in order to put a bid under that beleaguered currency. The BOJ also provided hawkish guidance, while planning to at least halve the pace of their QE (yes, the BOJ is still doing quantitative easing) program.

Oh, and I haven't even gotten to the part here Warren Buffett's Berkshire Hathaway BRK.A BRK.B sold half of that firm's well-known long position in Apple AAPL. Pow! Like a shot, the yen carry trade popped, and traders around the world hit every bid for every asset in sight.

The carry trade, a potential (probable) U.S. recession or at least slow down, and Warren selling shares of Apple. Traders were looking for dark closets to hide in.

Where The Week Went

Some of us added on that overnight weakness last Sunday night into Monday. We couldn't help it. Prices were so dislocated. If you've been punched in the mouth, you know it hurts and will hurt for days, but you fear it less. You can operate under pressure.

Readers may recall that I increased long positions in Nvidia NVDA, Palantir Technologies PLTR and SoFi Technologies SOFI at that time. They all worked out, at least for the short-term. The PLTR really, really worked out, as those earnings juiced that run. Remember, we have trades, and we have investments, but everything can be a trade if you need it to be. Even core names.

By week's end, analysts from JP Morgan JPM estimated that about three quarters of the yen carry trade had already been unwound by Wednesday. I have no idea how they figured that out. Maybe they are about as accurate with their estimates as are Fed economists. Or maybe not. Regardless, it was enough to calm financial markets.

Remember.... SMEAC

You had your five-paragraph order. Were you cool under fire? Yes? Terrific. No? We move on, we slow it down, we act more thoughtfully next time. We never, ever, ever surrender. Right? Not us. Print out the rest of this section and put it up somewhere so you can see it when you start sweating.

1) Understand... Everything is for a reason.

2) Identify... Avenues of approach, threats, targets of opportunity.

3) Adapt... to the changed and fluid environment. Become what the moment requires.

4) Overcome... Find a way, persevere.

5) Carry On... The mission is eternal.

Remember to Get Basic

Print this out too. Great for crisis-level thinking or just thinking in general. When it gets complicated, get simple, get basic. Reduce the peripherals. Focus on:

-- Who has the pricing power?

-- Is there a dominant story?

-- Where is geographic dominance?

-- Seek out strong management. Shun failure.

-- Where is the true value? Where is the value only now, or even not yet inexpensive?

Marketplace

And some sort of important folks who we won't call out, cried out for Uncle Jerome to come running with an emergency rate cut of 50 to 75 basis points within a week of last Monday. Well, week's up.... Feel a little stupid? If you're actually smart, you should.

-- The S&P 500 gained 0.47% on Friday to close the week down 0.04%.

-- The Nasdaq Composite gained 0.51% on Friday to close the week down 0.18%.

-- The Nasdaq 100 gained 0.54% on Friday to close the week up 0.39%.

-- The Russell 2000 gave up 0.17% on Friday to close the week down 1.35%.

-- The S&P Small Cap 600 gave up 0.18% on Friday to close the week down 1.04%.

-- The S&P Mid Cap 400 gave up 0.03% on Friday to close the week down 0.42%.

-- The Dow Transports gave up 0.65% on Friday to close the week down 0.31%.

-- The Philly Semiconductor Index gave up 0.43% on Friday to close the week up 2.21%.

-- The KBW Bank Index gained 0.21% on Friday to close the week up 0.22%.

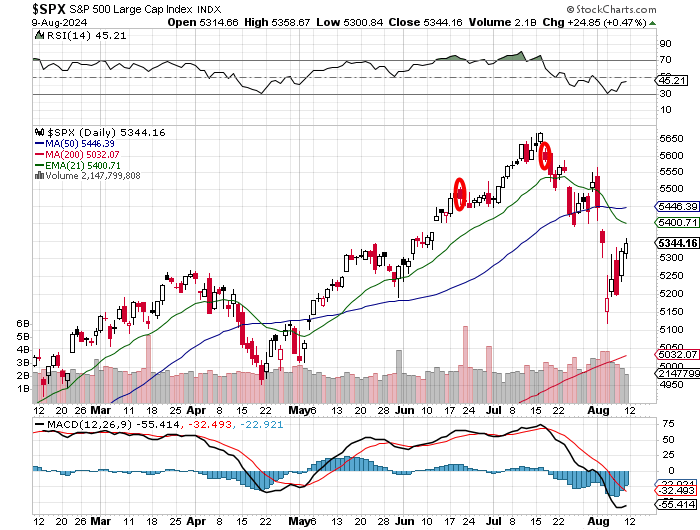

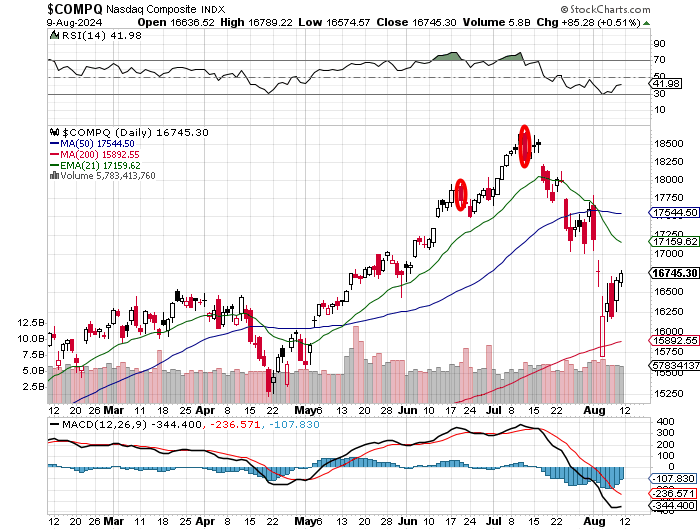

No, there was no rotation. Breadth was not all that great on the "up" days last week. The S&P 500 and Nasdaq Composite both have four-week losing streaks in place. The Philadelphia Semiconductor Index ended what was a three-week losing streak. Funny thing about the Philly Semiconductors... that index is now about 21% off of its early July high, but still up 12% year to date.

The Safety Dance

Readers will see that the S&P 500 has already filled the first of two recently unfilled gaps left in its wake as it collapsed late July into early August. Still, there is nothing to hang on to. Relative strength is relatively weak, and the daily Moving Average Convergence Divergence (MACD) is still cheap horror movie material.

Look how trading volume evaporated on recent "up" days after the big kids sold stock on "down" days. Those big kids might need to see the 50-day simple moving average (SMA) to buy back those shares. Or they'll sell more when the 200-day line cracks. No, they don't feel stupid. They are algorithms. They have no feelings. They have no soul.

On the other hand, the Nasdaq Composite has already tested its 200-day SMA last Monday. That was when the sentient beings took those big kids to school. If only they understood the term "catching a beating."

Truly Scary

The scariest item of the week largely went by unnoticed with all of the alarms and sirens going off up and down Wall Street.

According to the New York Fed's Quarterly Report on Household Debt, U.S. total household debt increased by $109 billion or 0.6% during the second quarter. This brings the number up to $17.8 trillion. Total household debt is up $733 billion, or 4.3% on a year-over-year basis.

Within that number, credit-card balances increased by $27 billion, to reach $1.14 trillion as households are forced to find a way to finance familial standards of living in a very difficult economy for middle-to lower-income households. Aggregate delinquency rates printed at 3.2% for a second consecutive quarter. That said, a whopping 9.1% of all credit-card balances have spent time in delinquency within the past year.

Earnings & Valuation

According to FactSet, for the second quarter, with 91% of companies having already reported, the S&P 500 is expected to sport earnings growth of 10.8% on revenue growth of 5.2%. That's down from 11.5% on 5.3% a week ago. So far, 78% of S&P 500 companies reporting have posted earnings beats while 59% have reported revenue beats.

Interestingly, earnings growth projections for the third quarter have been coming in quite rapidly... to growth of 5.4% from 6.1% last week and from 8.1% at the start of the quarter, with revenue growth of 4.9%. For the full year, projections are for earnings growth of 10.2%, down from 10.9% last week on revenue growth of 5.1%.

For the second quarter, four sectors are running at 15% earnings growth or greater. Those sectors would be Utilities (+20.4%), Technology (+18.7%), Financials (+17.6%) and Health Care (+16.9%). There are two sectors running in a state of earnings contraction for the quarter. Those groups would be Industrials (-0.9%) and Materials (-8.8%). Incredibly, the Communication Services Sector is now running at 4.6% earnings growth for the second quarter after ending the quarter with estimates for growth of 18.4%.

The S&P 500 closed out the past week trading at 20.2 times forward-looking earnings, down from 20.7 times a week ago. This remains well above both the five-year average (19.4 times) and the 10-year average (17.9 times) for the index.

The Week Ahead

I mentioned the New York Fed's quarterly household debt survey above because the week ahead will be all about inflation and the consumer.

Corporate... The sheer number of publicly traded companies reporting drops off precipitously this week. That said, we will have enough high-profile names releasing their digits really over just the middle three days of the work week. On Tuesday morning, we'll hear from Home Depot HD, followed by Cisco Systems CSCO on Wednesday evening. Thursday will be the busy day for earnings this week, with Walmart WMT reporting ahead of the opening bell and Applied Materials AMAT reporting after the close.

The Fed... These guys have been quiet this summer and I suspect that's how it will be until the Kansas City Fed holds its annual clambake at Jackson Hole, Wyoming late next week. This week, we will hear from Atlanta Fed Pres. Raphael Bostic on Tuesday afternoon. Bostic is a voting member of the FOMC this year. We'll also hear from Musalem (St. Louis), Harker (Philadelphia), and Goolsbee (Chicago). None of those three holds voting rights on policy this year, but Goolsbee has been standing in for Cleveland's Loretta Mester who retired in June.

Macro... This will be a heavy week for the macro. July PPI will cross the tape on Tuesday followed by July CPI on Wednesday. I imagine that both of these releases will move the tape. With CPI released first, traders often overlook PPI. I would not expect that with PPI being released first. In addition to the inflation data for July, we'll see July Retail Sales and Industrial Production on Thursday along with both the August manufacturing focused surveys to be released by the New York and Philadelphia Feds. On Friday, July Housing Starts will hit the tape along with the preliminary release for the University of Michigan's Consumer Sentiment survey along with its one- and five-year inflation expectations.

13F Deadline Day...This Wednesday is 13F filing deadline day for hedgies and other institutional managers to make public their positions as of June 30.

Economics (All Times Eastern)

14:00 - Federal Budget Statement (July): Expecting $-254.3B, Last $-66B.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: GOLD (0.27), MNDY (0.56)

After the Close: ALC (0.73)

At the time of publication, Guilfoyle was long NVDA, PLTR, SOFI, WMT equity.