TJX Might Have Yesterday's Fashions, but Its Earnings Are Stylin'

Here's how I'd play this stock (and I am playing it) after its second-quarter beat.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Early on Wednesday morning, the trio of American retailers ... Macy's M, Target TGT and the TJX Companies TJX all reported second-quarter earnings.

I was tempted to cover Target in this piece, after seeing that stock trade 14% higher ahead of the U.S. open, but decided to go with TJX. Why? Well, Target is still trading closer to the lows of its range, while TJX is up 4% ahead of the open and trading closer to the top end of its chart. In addition, I came in long TJX, and I have written articles this year in support of that name. I figured a follow-up for those that may have followed me into this name might be more beneficial to readership.

For the three-month period ended Aug. 3, TJX posted a unadusted earnings per share of $0.96 on revenue of $13.468 billion. These top- and bottom-line numbers both beat Wall Street's expectations, while the sales print reflected year-over-year growth of 5.6%. The EPS print was up from the year-ago comparison of $0.85. Comp store sales increased 4%, which exceeded the company's plans and was entirely driven by an increase in customer transactions. Wall Street had been looking for comp sales growth of only 2.8%.

The CEO: 'Outstanding'

"Our overall comp sales growth was entirely driven by customer transactions, which increased at every division," said president and CEO Ernie Herrman in the press release. "The performance of Marmaxx, our largest division, was outstanding, with a comp sales increase of 5%. With our strong second quarter results, we are raising our full-year guidance for both pretax profit margin and earnings per share."

About That Guidance...

For the current quarter, TJX is planning comp store sales to rise 2% to 3%, pretax profit margin to land at 11.8% to 11.9%, and diluted earnings per share to print at $1.06 to $1.08. That's a little on the conservative side, given that Wall Street was looking for $1.10.

For the full year, TJX is projecting comp store sales growth of 3%. Pretax profit margin is seen at 11.2%, and the full year diluted EPS is now projected at $4.09 to $4.13. While that may look a little light as Wall Street is projecting $4.13, we know that management is conservative, and this is up from prior guidance of $4.03 to $4.09.

Surprisingly Strong Fundamentals

For the first six months of the fiscal year, TJX has generated operating cash flow of $2.366 billion. Out of that came capital spending of $982 million, leaving free cash flow of $1.384 billion (+9.3% y/y). Out of that number, the company repurchased $1.086 billion worth of common stock and dished out $803 million in cash dividends to shareholders. Yeah, I don't like to see returns to shareholders outweigh free cash. I have my eyes on that.

Turning to the balance sheet, the company's cash position stands at $5.25 billion, and merchandise inventories of $6.47 billion. This brings current assets to $12.89 billion. Current liabilities add up to $10.621 billion, which is largely accounts payable and lease liabilities. No short-term debt. That makes the current ratio 1.21, and its quick ratio 0.60. These ratios may look pedestrian to the untrained eye, but they are actually quite strong for a large retailer.

Total assets amount to $30.555 billion; the number includes only the tiniest amount of goodwill. More than 99% of all assets are tangible. Total liabilities less equity comes to $22.773 billion. This includes long-term debt of $2.864 billion, which is something the retail giant could take care of out of pocket. This is an unusually strong balance sheet, retailer or not.

My Take: Lookin' Good

I am impressed. TJX is executing at a high level. The quarter was strong as the U.S. consumer has started to show some cracks in the armor. This is the retailer's forte. TJX caters to budget-conscious consumers by buying surpluses of slightly out-of-season brand name goods from retailers and wholesalers with imbalanced inventory stocks. As we see credit delinquency rates rise, and labor markets toughen, TJX should excel, which is the primary reason I have been in this stock all year. Remember, I follow gross domestic inventory as closely as I follow gross domestic income, and GDI has indicated a much tougher U.S. economic reality than has GDP since the start of 2023.

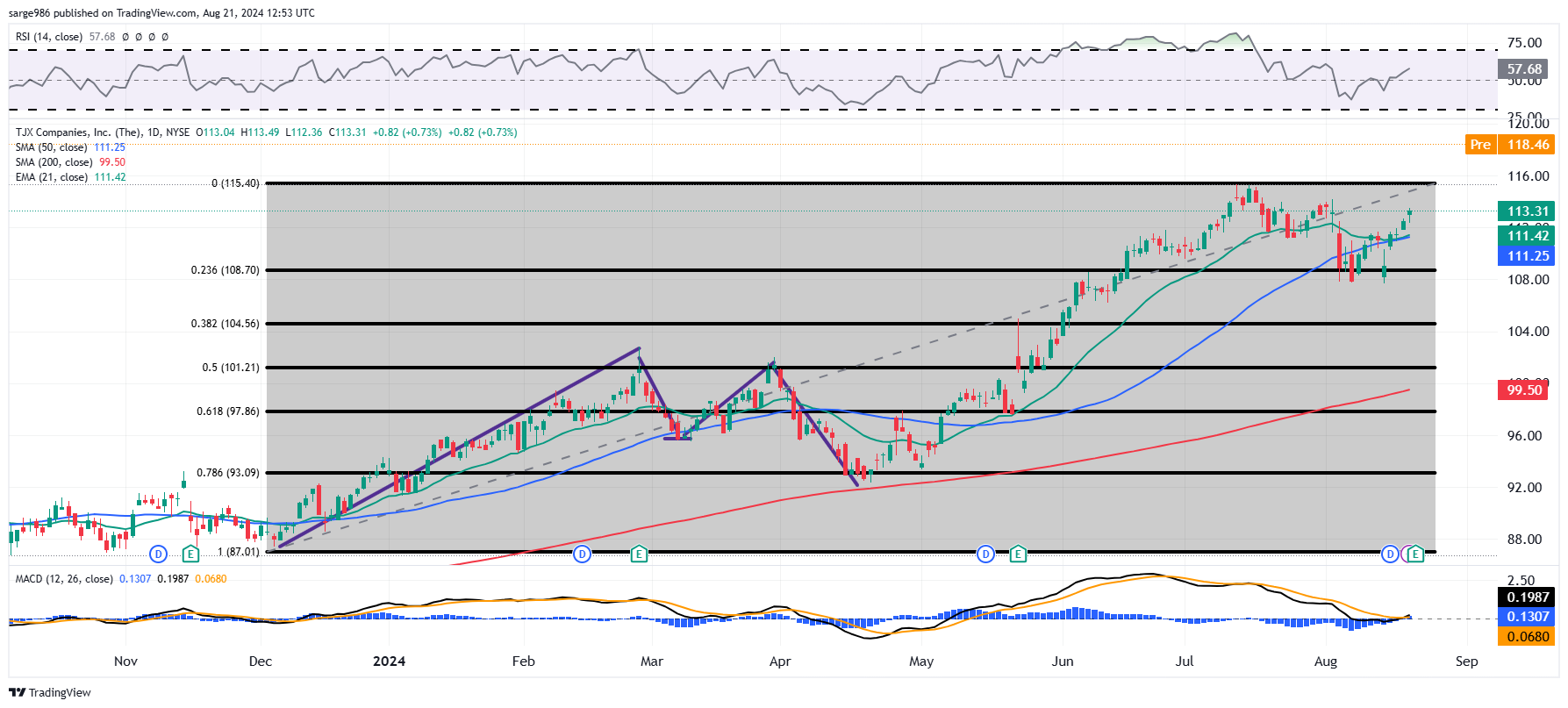

Readers will see that TJX went through a double-top reversal earlier this year, which worked less well that someone using that downside pivot to set a target probably would have liked. Going back to the liftoff in late 2023, the stock peaked at $115 in July. Over the next month and change, TJX went through a basing period of consolidation making use of the 23.5% Fibonacci retracement level of that late 2023 into July 2024 rally as support.

TJX is likely to at least try to break out of that basing period this morning, making use of that July apex as a pivot. A take and hold of that spot could unleash considerably higher prices for TJX (my biased opinion) in this tough (again, my opinion) economic environment.

TJX Plan

Target Price: $133

Pivot: $115

Add: Down to $108 support

Panic: Loss of 200-day simple moving average (currently $100)

At the time of publication, Guilfoyle was long TJX equity.