Time to Get Back Into This Low-Priced Uranium Stock?

Here are my thoughts on this small-cap name that may operate in the epicenter of the next hot industry.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Energy Fuels UUUU has been an on-again, off-again trading vehicle for the "Stocks Under $10" crowd. The company, which explores for and mines uranium in the states of Colorado, Arizona, Wyoming and New Mexico, reported earnings last week.

They didn't exactly kick any doors in. However, the fact remains that the large campuses being built for AI-supported data centers by the mega-cap hyper-scalers will likely require nuclear power if there is to be enough power available and available at an affordable price.

For Energy Fuels' third quarter, which ended September 30, Energy Fuels posted a GAAP loss of $0.07 per share on revenue of $4.047 million. That's right. Just $4 million. This is indeed a small company. A small company that is not yet profitable and wears a market cap of over $1 billion.

These top and bottom-line results disappointed analysts, while that paltry revenue print was only "good" enough for "growth" of -63.1%.

That Said...

During the quarter, Energy Fuels signed a fourth long-term contract with a U.S. utility. This contract calls for delivery of 270,000 to 330,000 pounds of uranium between the years 2026 and 2027 and then potentially an additional 180,000 to 220,000 pounds by 2029.

Operations

For the period covered, revenue generation dropped from $10.987 million to $4.047 million. Out of that came costs of $1.847 million and operating expenses of $14.113 million. This left it with an operating loss at $11.913 million, which was down versus the year-ago comparison of -$6.944 million.

After accounting for other income and losses (I don't see info on interest or taxes), net income attributable to shareholders printed at -$12.06 million, down from $10.563 million. That's right, last year the firm had some non-operating income that pushed that statement of operations into profitability. That left GAAP per fully diluted share at -$0.07, down from $0.07.

Fundamentals

For the first nine months of the year, Energy Fuels has generated operating cash flows of $7.988 million. Out of that came capex spending of $20.684 million, leaving year-to-date free cash flow of -$12.696 million. The company obviously did not return any capital to shareholders.

Turning to the balance sheet, the company ended the period with a cash position of $148.609 million and inventories of $35.91 million. That put current assets at $193.923 million. Current liabilities add up to $10.768 million, none of which is debt. That puts the its current ratio at an extremely muscular 18.0 and its quick ratio at 14.7. This company can meet its obligations.

Total assets amount to $400.404 million and that includes no intangibles. Total liabilities less equity comes to $23.717 million. Guess what? No long-term debt either.

Energy Fuels has a balance sheet for the ages and can burn cash for a long time if need be.

Wall Street Weighs In

This week, five-star rated (by TipRanks) analyst Joseph Reagor of Roth MKM reiterated his "hold" rating, while cutting his price target price to $5.50 from $6.00.

That same day, four-star rated analyst Heiko Ihle of HC Wainwright reiterated his "buy" rating, while raising his target to $11 from $10.75.

My Thoughts

Okay, gang, if we're in this one, we're either trading short-term or if investing, then speculating. The company has not been making money or generating positive cash flows.

That said, they may operate in the epicenter of the next hot industry. The balance sheet is a work of art. These guys can burn cash for a very long time before it starts to matter.

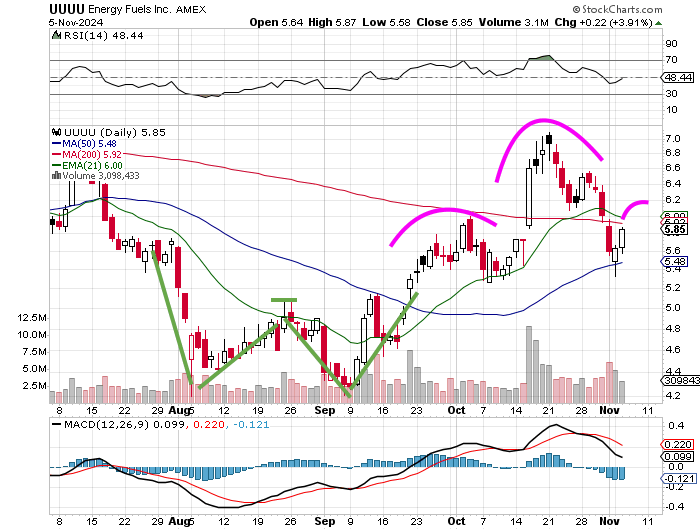

I do like the series of higher lows that the stock has made since early September when it broke out from a double-bottom reversal pattern. I like an improving reading for Relative Strength.

I don't like the look of the daily Moving Average Convergence Divergence (MACD), and I don't like the potential for a developing head-and-shoulders pattern to come to completion.

I like the idea of investing in this stock. I think, however, that I might wait until it retests that 50-day simple moving average (SMA) to see if the head-and-houlders pattern is for real. If not, I think it will be a buy on upward momentum above its 21-day exponential moving average (EMA).

At the time of publication, Guilfoyle had no positions in any securities mentioned.