These 4 Small-Cap Stocks Could Benefit From a Broadening Market

A big topic is the recent rotation and/or broadening out of the markets. Here are four investment opportunities in the small-cap space.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Rotation, rotation, rotation. That's what investors and financial pundits are talking about now that the "Magnificent Seven"-driven market is starting to broaden out. What does this mean for the averages in the rest of 2023 and beyond?

What opportunities might investors want to consider in the small-cap space now that those stocks are playing catch up?

Top MoneyShow investing and trading experts weigh in below.

JC Parents All Star Charts

Rotation Is the Lifeblood

I would encourage you to go back and study every bull market in history. Do you know what you'll find? Sectors rotating. And this bull market is no different. In the back half of 2022, almost everything was working. In fact, very few stocks were not working. And then we got sector rotation. The laggards from the back half of 2022 became the new leaders during the first half of 2023. The Nasdaq had its best first six months to a year in history.

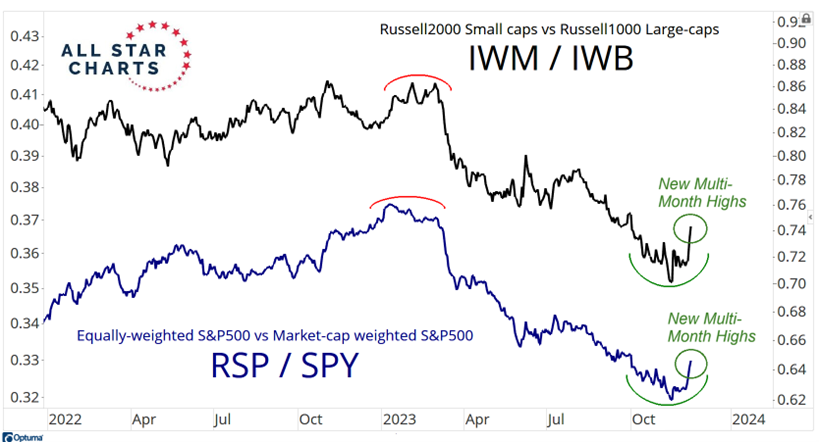

Then this Spring, you got rotation again, back into many of those former leaders from 2022. And that's exactly what's happening here once again. You can see the new multi-month highs in the ratios between Small-caps and Large-caps, as well as in the Equally-weighted RSP vs. Market-cap weighted S&P 500SPY .

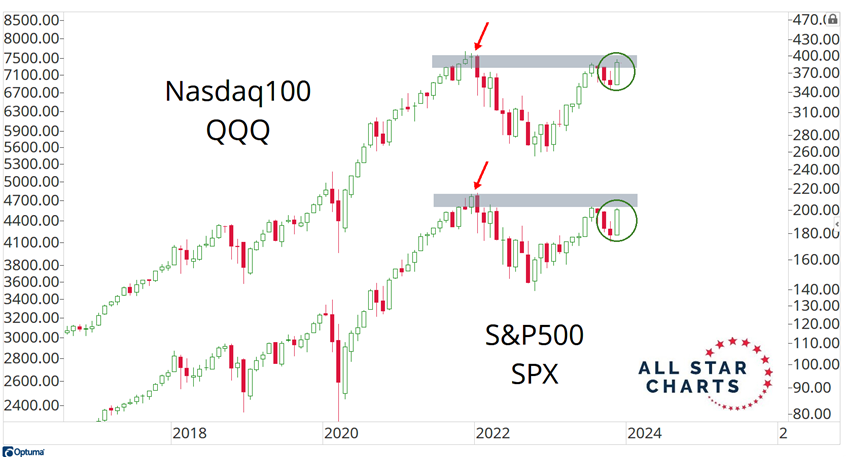

These downtrends throughout most of 2023 are NOT evidence of weak breadth. They were NOT risk-on/risk-off indicators. It's simply a representation of sector rotation. So as these ratios break out to new multi-month highs, you can see in this chart below how the major indexes are back near former all-time highs.

I bet that while the Nasdaq and S&P 500 try to figure themselves out up here near resistance, sector rotation should remain dominant. I would not be surprised to see a similar situation as the back half of last year where most stocks and sectors did well, but the indexes were held back due to their composition. In other words, what drove the outperformance of these indexes for much of 2023, is what held them back in late 2022, and what could slow them down once again.

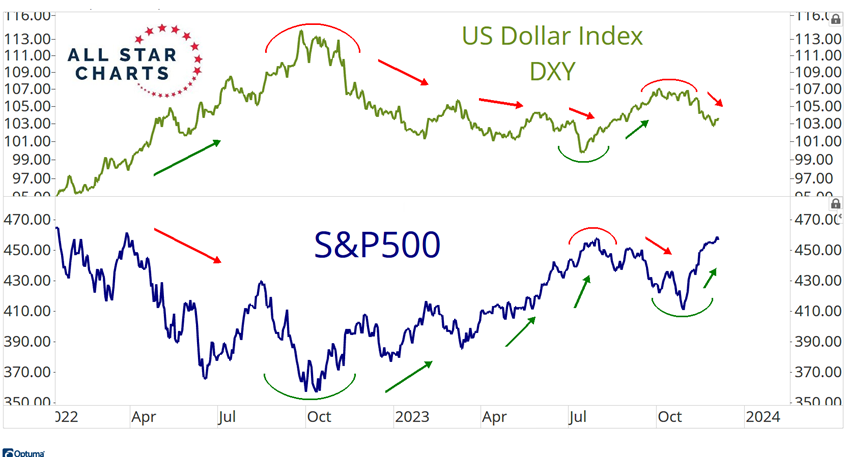

The catalyst is the U.S. dollar. It always was. Dollar up = S&P 500 down. Dollar down = S&P 500 up.

Do you think this is a coincidence? The day the dollar bottomed in July was the day the new highs list peaked on the NYSE. Coincidence? The day the dollar peaked in early October was the day the new lows list peaked on the NYSE. Coincidence? It's all about the dollar. It always was.

Contrary to popular belief, the U.S. Treasury Bond Market is NOT the haven that it once was. And there's no evidence AT ALL that it will be again any time soon. Stocks and bonds are trading together. The safe haven is the U.S. dollar. It continues to prove that it is the only real safe haven. I suspect that it's going to take investors a long time to adapt because as we know, investors hate doing basic math.

Around here we like to count. And if you're willing to count, you'll quickly see how the bond market is NOT a safe haven. I bet that it's going to take the worst investors the longest amount of time to finally figure this out. There's a lot of money to be made here because of the mispositioning from lazy investors not willing to do the actual work. To be clear, I'm not calling anyone out or picking on any group. I'm just presenting the current opportunity for those who are paying attention.

Richard Moroney Upside

Three Small Caps with Big 'Upside'

CarGurus CARG operates an online marketplace that allows dealers and car owners to buy and sell new and used vehicles. Dealers typically pay subscription fees in exchange for having cars listed. The company, which has more than 24,000 paying dealers, also purchases cars directly from consumers and resells them to dealers.

With car inventories now at healthy levels following shortages during the pandemic, many dealers are turning to CarGurus to help boost sales. The company claims to have the most-visited automotive shopping site in the U.S.

Analyst estimates are rising, with the consensus projecting per-share-profit growth of 19% for full-year 2023. Revenue is expected to slump 45%, partly because management has slowed transaction volumes to focus on more profitable and sustainable growth. For 2024, the consensus calls for per-share earnings of $1.28, up 5%.

CarGurus has delivered positive profit surprises in four consecutive quarters, with an average surprise of $0.09, or 54%. The stock earns an Overall Quadrix score of 98 (out of 100), up from 48 at the start of 2023. Both sector-specific Quadrix ranks are above 90. The stock is being initiated with a Buy rating.

Semler Scientific SMLR designs and manufactures healthcare products for the early detection and treatment of chronic diseases, including arterial disease and heart dysfunction. Semler's core cardiac and vascular testing product, which measures blood flow in extremities, is used by health insurers, physician groups, and hospitals.

With a market value of $261 million, Semler is an aggressive holding given its small size and concentrated sales - two customers accounted for nearly 70% of its $57 million in revenue last year. Still, a recurring sales stream and market-share gains should help sustain growth. Semler earns the maximum Overall score of 100 and outstanding ranks for Quality (99) and Financial Strength (93).

One analyst provides sales and earnings estimates for Semler. December-quarter results are projected to show a 39% per-share-profit increase to $0.57, with revenue up 5%. Earnings outstripped expectations by 39% in the September quarter and 34% in the June quarter. Per-share earnings are projected to advance 48% in 2023, followed by 27% growth next year.

Although the stock has rallied 44% over the past three months, its valuation still looks reasonable at less than 12 times estimated 2024 earnings, or 48% below the three-year median trailing P/E of 22. Semler is being initiated as a Buy.

Pent-up global demand to take trips has fueled strong growth at TravelzooTZOO . The company's members-only service offers exclusive deals on flights, hotels, and curated trips. An expansive and growing presence reflects some 30 million members, 8 million mobile users, and 4 million social media followers.

More than 5,000 global travel providers use the company's marketing services, including Alaska Airlines, Hilton Hotels, and Royal Caribbean. Over the past 12 months, Travelzoo delivered per-share earnings growth of 833% on sales growth of 25%. The stock earns an Overall score of 93.

Travelzoo has rallied 100% in 2023 but remains a good value. The stock's trailing P/E ratio of 10 is 57% below its 10-year norm of 23. Three analysts offer sales and profit estimates. While December-quarter earnings per share are expected to be flat, full-year growth is expected to approach 52%.

For 2024, rising analyst estimates call for per-share profits to climb 23% to $1.04, up from a consensus of $0.91 two months ago. Revenue is projected to advance 11%. An aggressive stock, partly because of its tiny market capitalization of $124 million, Travelzoo is being started as a Buy.

Doug Gerlach SmallCap Informer

Allient: Automation and Efficiency

The heart of Allient's ALNT business is motors, but its components are found in many diverse products seeing increased demand, such as robotic surgery, industrial automation, electric motors and vehicles, and space exploration.

We like discovering the "companies behind the companies" -- those businesses that make the components and supplies that are used in products that are used every day across a spectrum of industries, and Allient surely fits the bill.

Revenues have moved on a stable pathway since 2013, growing at 12.6% per year on average but accelerating in the last two years at an average 17.1% pace. Revenues in fiscal 2022 totaled $503.0 million, halfway to the company's goal of becoming a billion-dollar business.

EPS have been less consistent, turning in an overall 11.8% annualized rate of growth in the same period. Results since 2020 have been affected by the pandemic and related factors such as supply chain disruptions, onshoring and reshoring of manufacturing.

Management cautiously points to 2024 with an expectation that the company's growth will return to pre-Covid 2019 patterns. Management cites several factors that present the company with opportunities to grow.

The first, electrification, sees internal combustion engines and hydraulics systems used in transportation being supplanted by the adoption of electrical systems. This includes in defense systems as well as for land, sea, and air networks. This trend is global.

The second factor is energy efficiency. Worldwide, a massive effort is underway to massive effort to reduce energy consumption and operating costs. Today, about 40% of all global electricity consumption is derived from motors, so even minor increases in efficiency can make a big difference.

The third trend is a move towards increasing industrial automation. This addresses an ever more challenging labor environment, advances reshoring efforts that serve regulatory and supply chain interests, and drives overall efficiency and productivity.

The stock was recently selling at a P/E ratio of 18.2, which is 74.0% of its average P/E of the last five years. We calculate that the stock could reach $79 and is a buy up to $38. Our downside price is $24, and the current price represents a reward/risk ratio of 23.5-to-1. The potential total annual return with a small dividend is 24.9%.