Masonite Opens the Door for Investors

Here's why this stock is primed for a catch-up move higher.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

One of my favorite techniques for ferreting out bargain stocks is finding shares that do not currently reflect value that has already been created.

Masonite International DOOR falls into that category right now after falling sharply over the preceding couple of months. There was zero bad news on Masonite to account for that selloff.

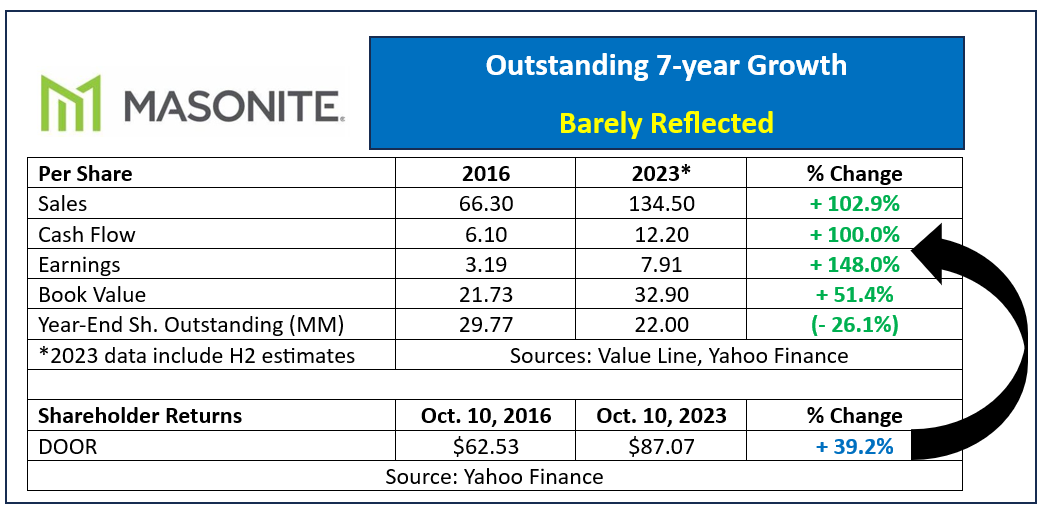

The table below shows the progress DOOR made since 2016 across all major business metrics. Per share sales, cash flow and earnings all at least doubled. Book value rose greater than 51% despite buybacks which trimmed outstanding shares by over 26%.

Amazingly, we can now own DOOR for less than 39% more than it fetched exactly seven years earlier.

Getting much more value at a large discount is a great thing for today's buyers.

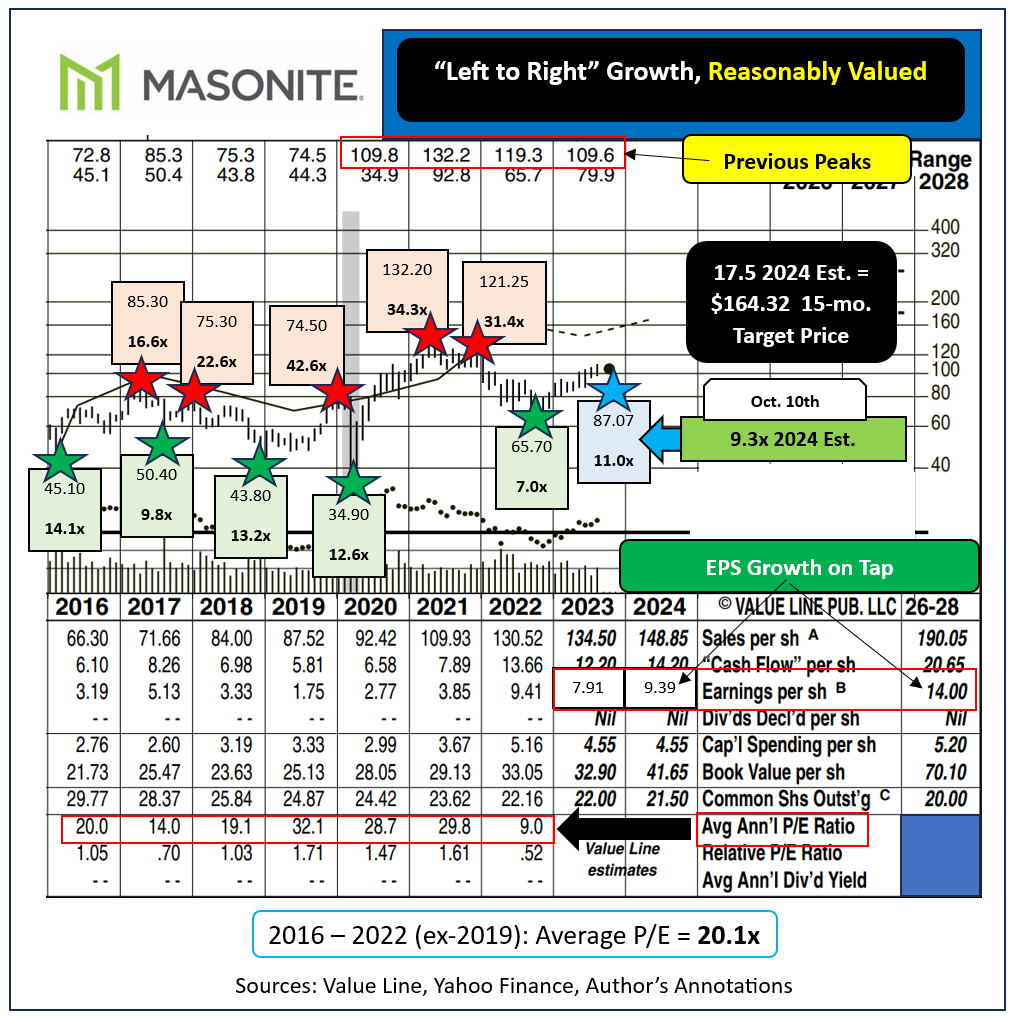

What is Masonite worth?

Since 2016 a typical multiple has run about 20.1-times earnings. Best buying opportunities (green-starred below) all occurred when DOOR was available at discounts to that average multiple. Four of DOOR's five "should have sold" moments (red-starred) took place when the shares fetched above average valuations.

Assume just a partial reversion to the mean price-to-earnings of 17.5 and you come up with a Dec. 31, 2024 target price of $164.32. That implies 15-month upside potential of 88.7% on this good-quality name.

That goal is not far fetched. DOOR topped out north of $132 during 2021 on final EPS of just $3.85. It offered traders chances to sell above $109 during each of the past four years including 2023 year to date. DOOR changed hands near $110 less than two months ago.

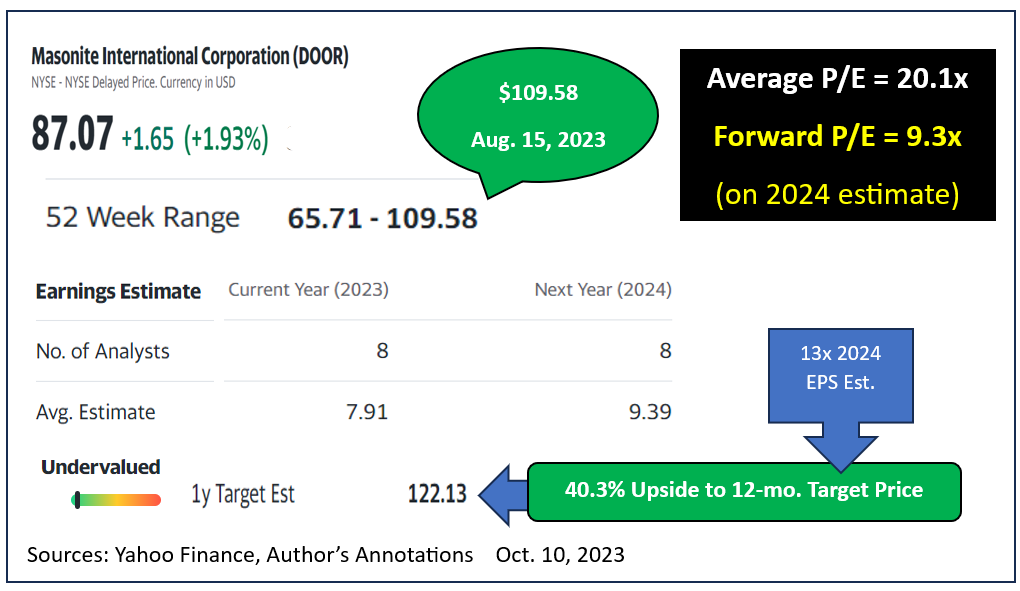

Yahoo Finance calls the stock undervalued while seeing a rebound to $122.13 by this time next fall. Reaching that target would deliver a solid 40.3% 12-month return.

Morningstar research rates Masonite as a 4-star, out of 5, buy. It deigns to provide year-ahead goal pricing but calls present-day fair value $102.95.

That goal appears quite conservative seeing as DOOR traded well above that price each year since 2020.

GuruFocus also shows Masonite as underpriced. They see fair value as $117.56, about 35% higher than its Wednesday quote.

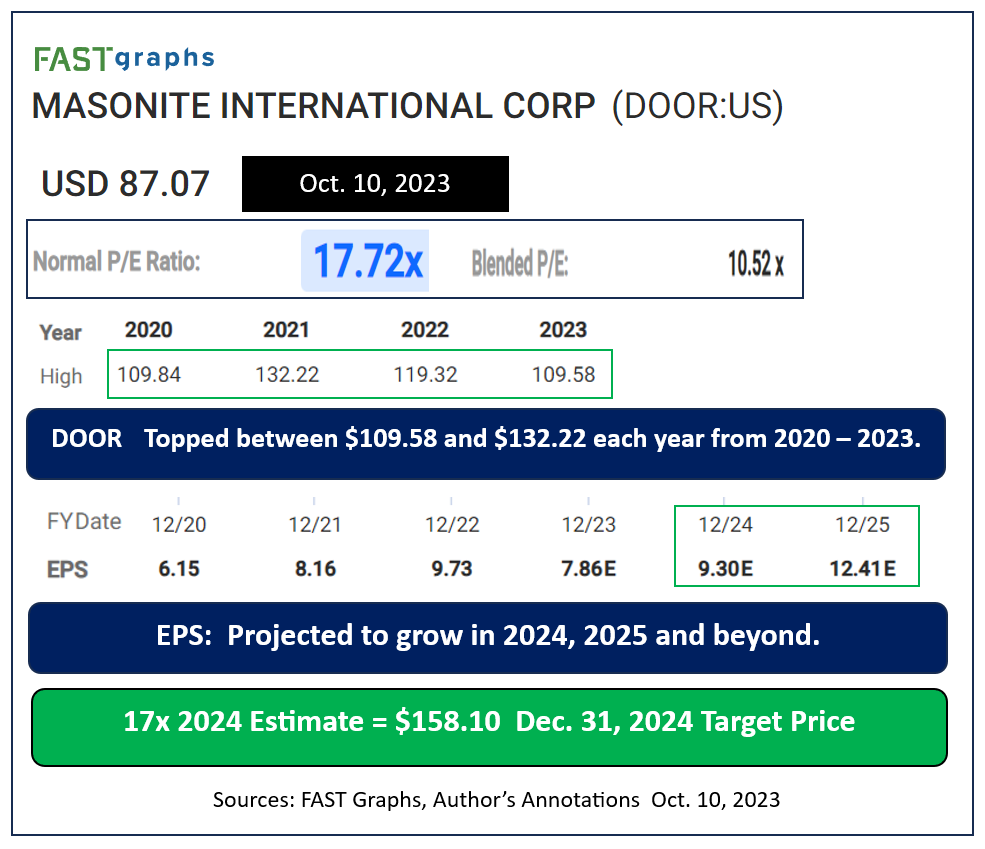

Quantitatively based FAST Graphs' projected end of 2024 target price comes out to $158.10 based on a 17 multiple on its 2024 EPS estimate. Getting to that price would make for a greater than 81% rise.

If DOOR posts the earnings growth expected in 2024 and pops up to 20-times earnings it could be $186 by the end of next year. That would translate into better than a double.

No matter which research proves most accurate it appears highly likely that Masonite will recover nicely from it temporarily depressed valuation.

Options are available as far out as April 19, 2024 if you'd like to short puts or buy calls to participate in DOOR's upside potential over the coming 6-plus months.

At the time of publication, Price was long DOOR shares, short DOOR options.