How to Optimize Your Retirement Portfolio After BlackRock Income Warning

The easy era may be fading but there are key ways to prepare your post-retirement income accordingly.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

For the past few years, cash has been ascending the throne. If it’s not quite king, it’s definitely royalty.

According to the Investment Company Institute, money market fund assets grew by $122.35 billion to $7.75 trillion for the week ending Wednesday, May 6.

Now, with expectations for lower rates, retirees and pre-retirees holding a cash hoard face a new problem: How to replace that income without taking on too much risk or triggering higher taxes.

That means maximizing yield is taking a back seat to optimizing after-tax income and flexibility.

Right now, the biggest risk may not be low income, but relying on a single strategy.

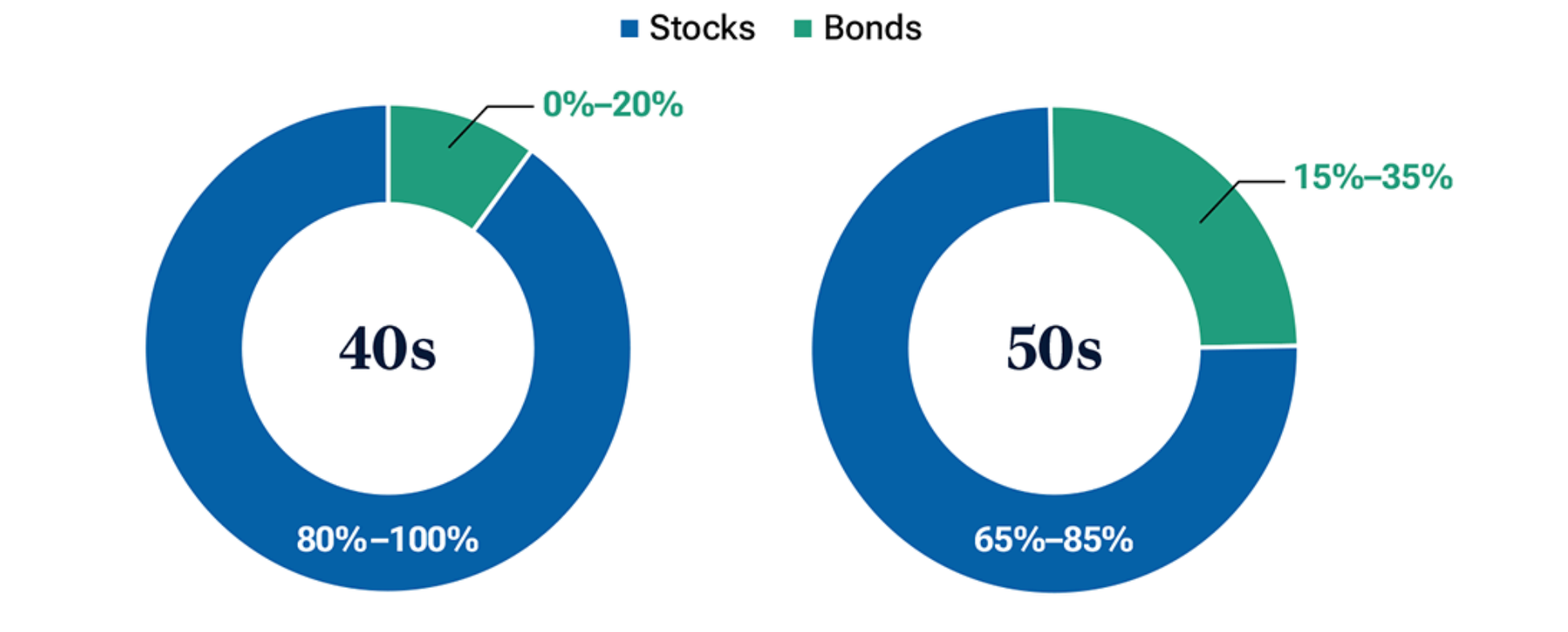

Same Old, Same Old

The typical retirement portfolio mix may look something like this.

T. Rowe Price

If your portfolio still looks like the chart on the left as you approach retirement, you're carrying the income volatility of someone with 20 more years of paychecks ahead of them. That's the gap most retirees discover only when they start drawing income.

Components often include:

- Old faithful: an S&P 500 index fund

- Dividend ETFs concentrated in a handful of high-yield sectors

- Mega-cap tech ETFs with big S&P overlap

- A pile of cash generating strong yields (hopefully)

That mix might look diversified on paper, but in practice it often leans heavily on a narrow set of drivers: U.S. large-cap stocks, a few high-yield sectors and whatever cash is paying at the moment.

It held up during the AI-driven rally, when mega-cap tech giants did most of the heavy lifting.

But retirees need income for decades, and typical income portfolios aren’t built for one type of market environment. If you need a new roof this year, a new car next year, your daughter is getting married and you’re planning a big trip, you don’t really care that market leadership has rotated. You do care that rates have moved, and that your portfolio isn’t rewarding you the same way it once was.

That’s why some strategists are urging investors to broaden their approach.

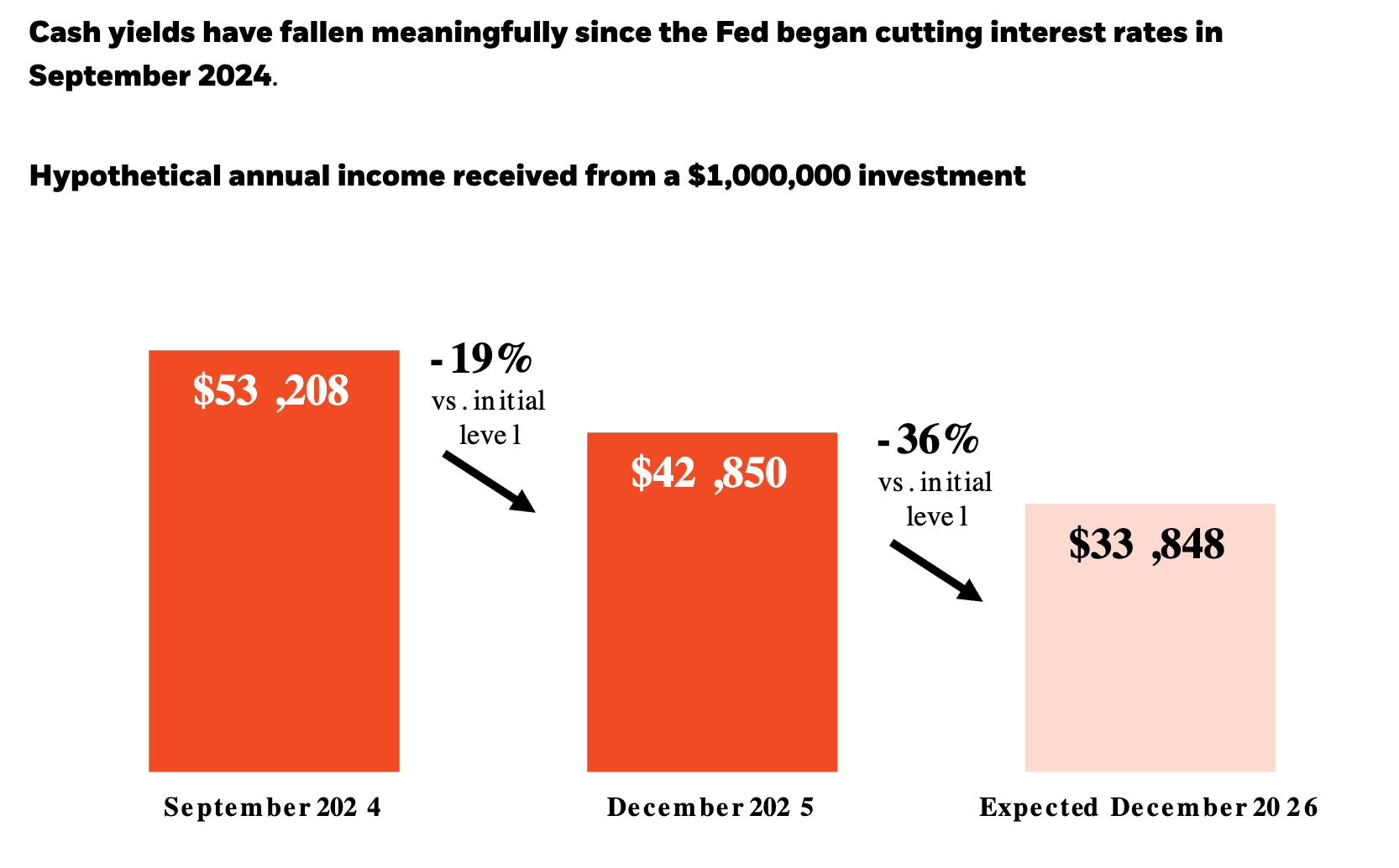

This chart from BlackRock illustrates how much annual income a retiree could generate from a $1 million cash allocation as short-term interest rates decline.

BlackRock

If you've built your retirement income plan around the 2024 column, you're already living in the 2025 column, but the 2026 column is where the math gets uncomfortable.

Review what you have in cash today. The drop from the first bar to the third is roughly what your annual income from that cash will fall by. Then figure out what other assets you can use to make up the difference.

Income Drop on the Way

In its 2026 Income Outlook, BlackRock says retirees are at a key inflection point, noting that there is around $9.1 trillion in money market funds worldwide.

But that cash isn't paying what it used to, and could fall further. The firm's own chart shows the income drop coming. The question is what fills the gap.

Cash generated unusually strong income during the recent high-rate environment, helping explain why many retirees piled into money market funds and other short-term holdings.

But the chart also shows how quickly that income can fall once the Fed starts cutting rates.

Income Optimization: Taxes and Flexibility

Remember, in retirement, it’s all about keeping the money to fund your needs. Managing taxes is insanely important, but so is creating the right mix to optimize your return. It’s a balancing act, which is different for everyone. High yield doesn’t always mean better outcomes, especially after taxes.

Retirees may improve income sustainability by blending:

- Roth withdrawals for tax control: Useful if you're managing IRMAA brackets, doing Roth conversions over a series of years or want to leave tax-free assets to your heirs.

- Taxable accounts for flexibility: Great if you need access to capital for lumpy expenses (that new roof, wedding or car) without triggering a forced retirement-account distribution.

- Municipal bonds or tax-aware fixed income: Helpful if you're in a high federal bracket, live in a high-tax state, or want income that doesn't push you into the next IRMAA tier.

- Dividend growth rather than just high yield: Good solution if you have a long retirement horizon and care more about income that keeps pace with inflation than the highest current payout.

None of these is a panacea for everyone, but they are all tactics that can be applied, depending on your situation.

That leads to this idea: There’s a broader shift away from one-size-fits-all retirement formulas. I recently read something in Kiplinger’s that’s relevant.

“Retirement income can't depend on the market being up every year. It depends on having multiple income sources that also act as buffers against bad markets,” wrote Devon Albarez, a financial advisor at Integrity Financial Group in Grand Rapids, Michigan.

And I’d add, it can’t depend on too big a chunk of cash safely tucked away in a ridiculously high-yielding savings account. Those rates are still high by historical standards, but lower than a year ago. The good times won’t last forever.

Beyond Cash & Dividend Stocks

Most retirees default to dividend stocks or even Treasuries for income. But there are other tools that might be worth a look.

1) Short-duration bonds

Instead of stretching for yield in long bonds, shorter-duration exposure can:

- Reduce volatility

- Preserve liquidity

- Allow for easy reinvestment if rates change

2) Options-income strategies

Covered-call and buffered ETFs can:

- Generate income

- Reduce volatility

- Smooth withdrawals

However, if you go into these vehicles or other income-forward investments, remember there’s limited upside. That is often confounding to investors with an equity focus (which is nearly everyone) or who like to trade.

You might also introduce more tax complexity by creating non-qualified income and short-term gains. These are taxed at higher ordinary rates than dividends or long-term capital gains.

The retirement income risk in 2026 isn't a low-income environment. It's getting caught in one strategy when the environment changes.

Related: Japan Stocks Burst Back After Latest Yen Intervention