A CD-Like Yield Plus Outstanding Upside Potential

This stock has reliably sold off then rebounded seven times since 2014. The present-day bargain price is almost certain to be a temporary stop on the road to much higher prices.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

One of my favorite investment themes is buying shares of firms which have already created value which is not being reflected in their share price.

Carter’s CRI is America’s largest branded marketer of apparel for babies and children. They sell through almost 800 domestic and 54 Mexican outlets under the Carter’s and Osh-Kosh banners. Walmart WMT, Target TGT also sell Carter's products in the mass market arena.

International licensing agreements account for about 14.6% of total sales.

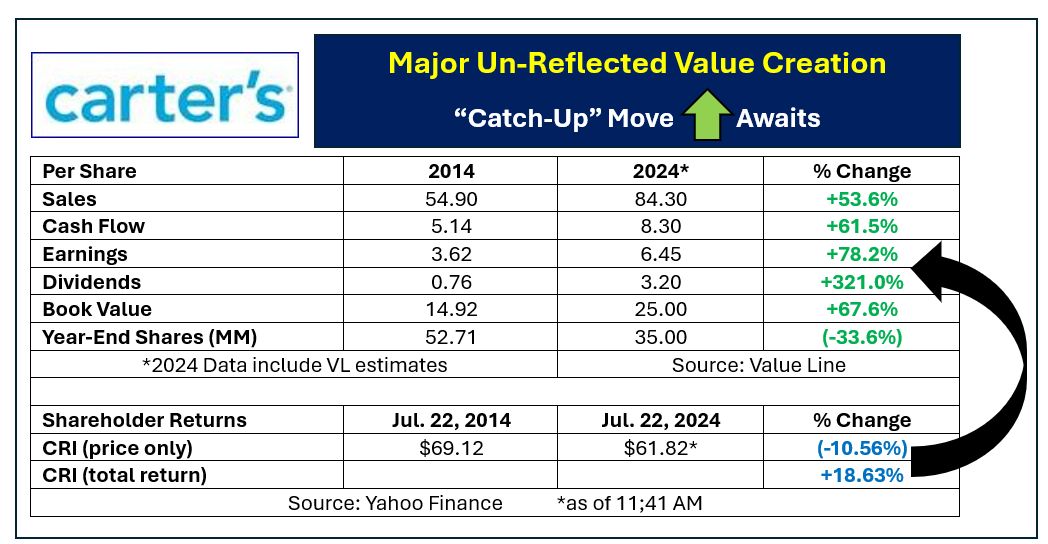

Over its most recent decade Carter’s posted solid growth across all major business metrics. Almost 34% of all shares outstanding were retired through buybacks as well.

You would think that numbers like those shown below would have led to a much higher share price. Instead, recent stock price weakness (CRI peaked at $116.90 in April of 2021) has given investors a fabulous entry point at south of $62.

On a share-price only basis CRI is now priced around 10.6% lower than it sat exactly 10 years earlier.

When value is much higher but the shares are lower the typical resolution between price and value is for a “catch-up” move higher to arbitrage away the discrepancy.

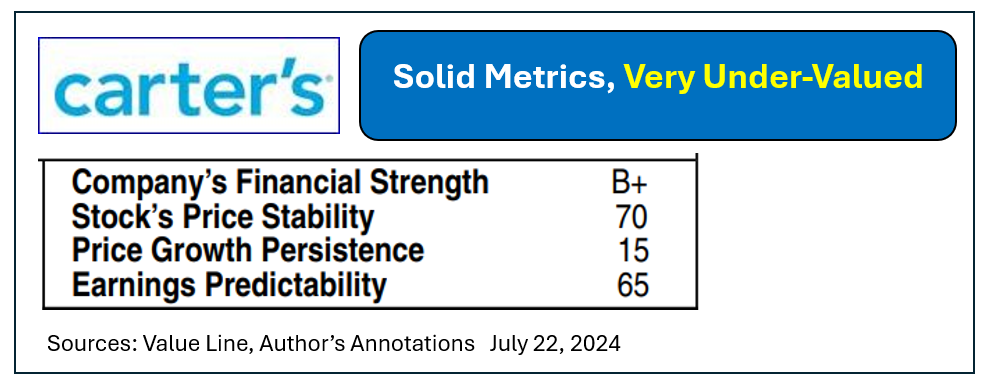

Carter’s business metrics look good. Value Line rates their financial strength as B+ while noting the stock’s 70th percentile stock price stability and better-than-average earnings predictability.

The stock’s extremely low score for price growth persistence will grate on long-term holders but beacons value seekers who do not yet have positions.

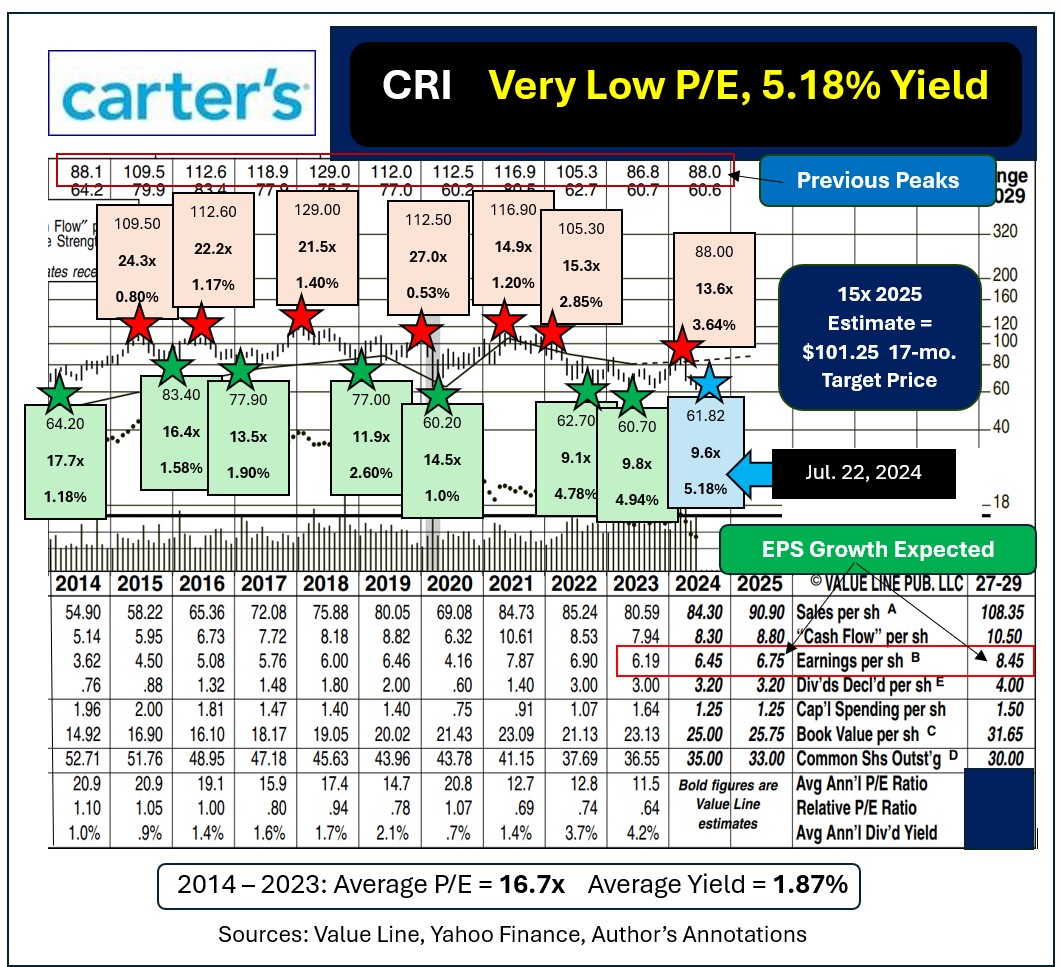

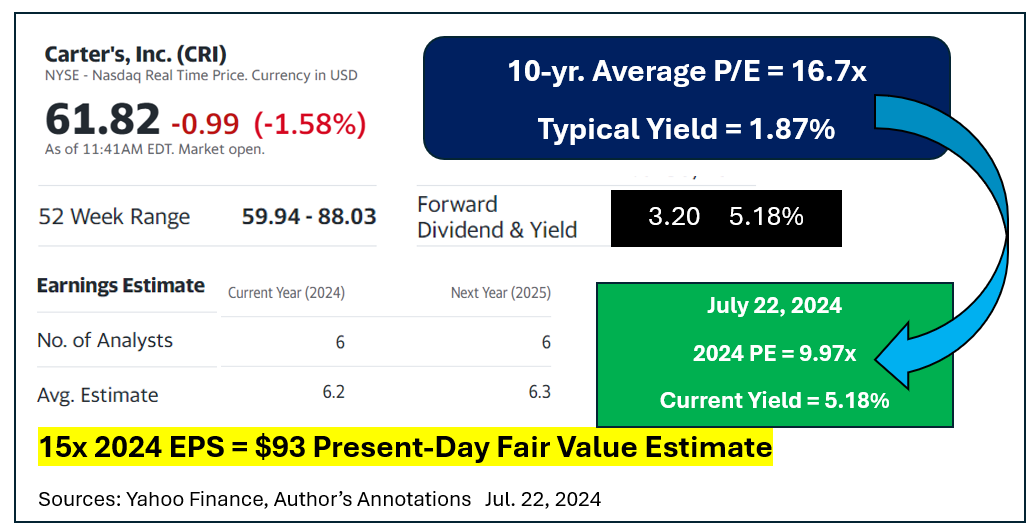

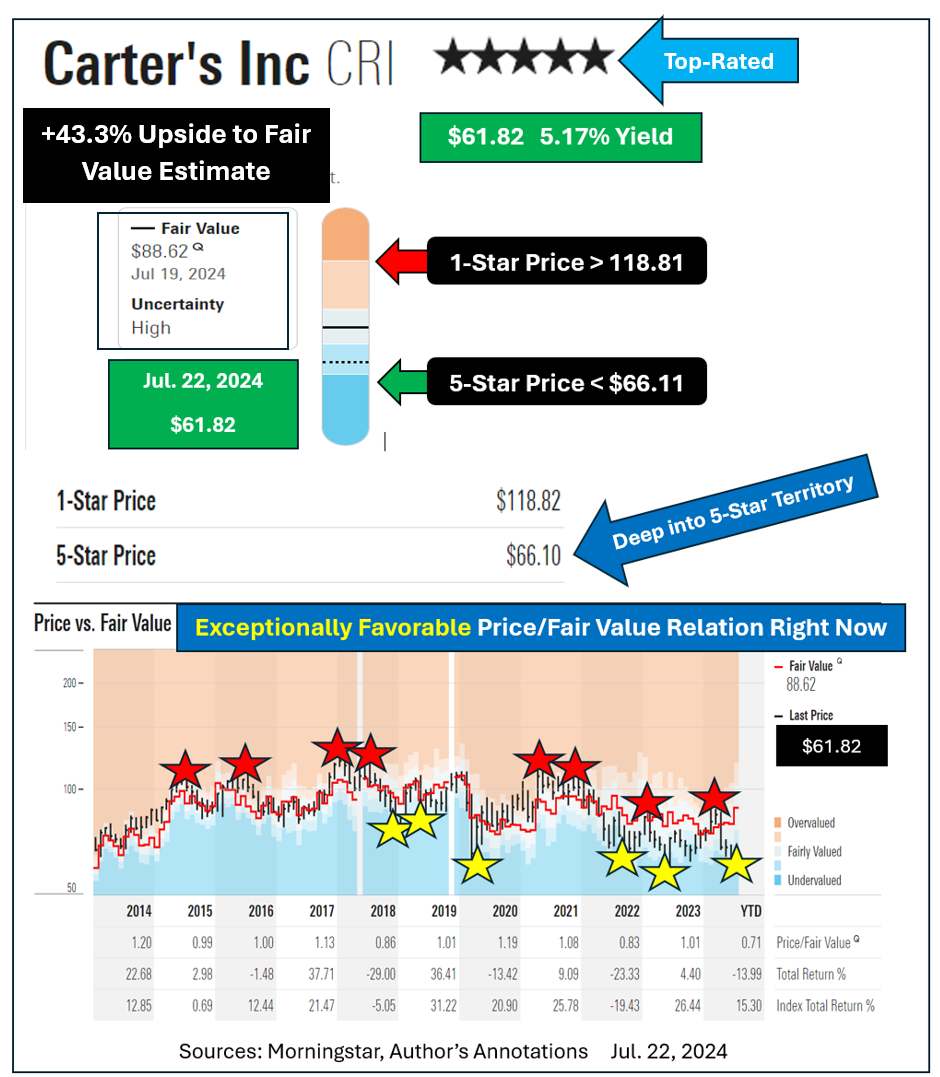

CRI’s 10-year average multiple has run about 16.7x accompanied by around 1.87% in yield. As of midday on July 22, 2024 those figures were 9.6x Value Line’s 2024 EPS estimate along with a fine 5.18% in current yield.

What Is CRI Worth?

A rebound to a still-lower-than-average 15x next years estimated EPS would take Carter’s shares up to north of $101 by the end of 2025. That suggests potential 15-month total return of about 70%.

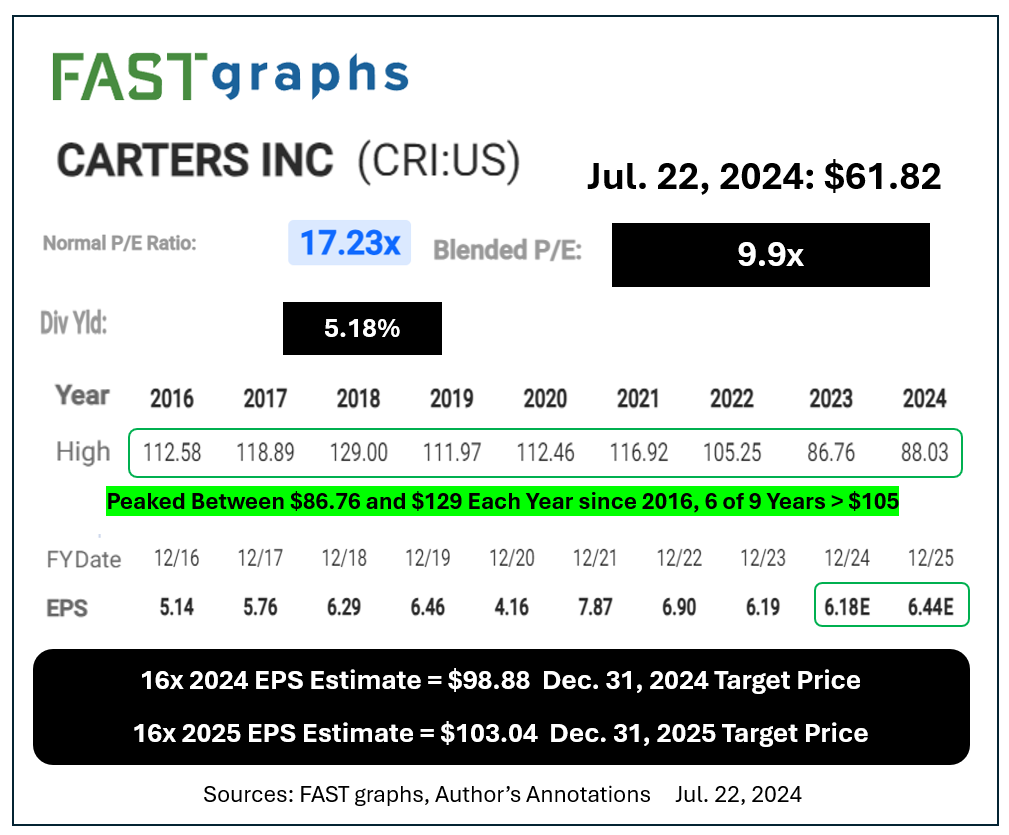

That is far from an upper limit. CRI topped out at from $105.30 to $129.00 during each of the eight years stretching from 2015 through 2022 on similar earnings to what is expected this year and beyond.

The current P/E is way lower than most of CRI’s best buying opportunities (green-starred below), all of which led to sharp rebounds in the share price.

The Covid-panic low of $60.20 quickly gave birth to a 14-month rally to $116.90. 2002’s nadir of $62.70 in October saw CRI jump up to $86.80 by February 2023. Four months later CRI dipped to $60.70. By March of this year Carter’s was back up to $88.

CRI has reliably sold off then rebounded seven times since 2014. The present-day bargain price is almost certain to be a temporary stop on the road to much higher prices once again.

Don’t simply trust my judgment on this.

Yahoo Finance sees EPS of $6.20 and $6.30 for CRI in 2024 and 2025. Simply going back to a more typical valuation would justify a $93 present-day fair value.

Research from Morningstar labels the stock a 5-star best buy. They call present-day fair value for CRI as $88.62 per share. That implies greater than 43% in potential upside plus the generous 5.18% dividend yield.

Morningstar’s chart of price to fair value clearly shows that Carter’s has almost never sold for a larger discount than it does today.

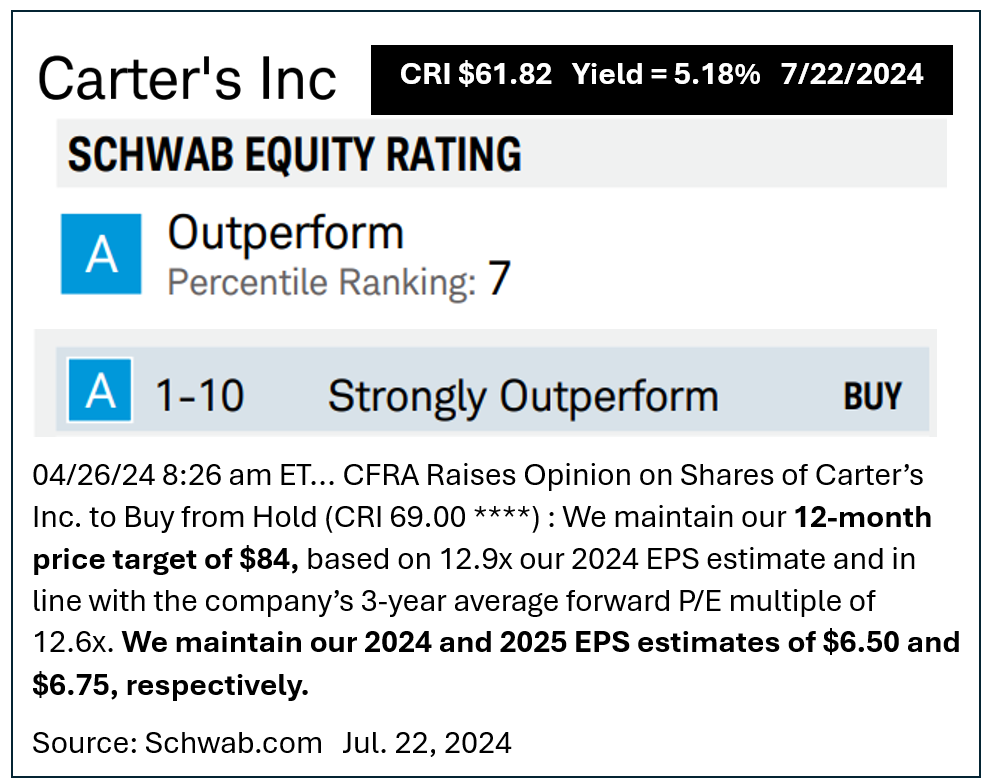

Charles Schwab’s research calls CRI an “outperformer” while holding onto an $84 year-ahead price target.

That goal appears over-conservative as it represents a final price of less than 12.5x their own EPS estimate for 2025.

Quantitatively based research from FASTgraphs also favors Carter’s shares. They see a normalized P/E for CRI of 17.27x versus its current blended P/E of 9.9x.

Reverting to a still below average 16x multiple suggests an end of 2025 goal of $103.04 as reasonable.

Risk-to-reward on Carter’s is extremely favorable. Its shares are near decade-long lows and nowhere near the stock’s annual peaks. CRI’s yield is 87.3% above normal.

Even the lowest of the goal prices on CRI from all sources shown would deliver excellent total return from today’s depressed quote.

Carter’s is a high-yielding, low-risk stock which is suitable for almost anybody’s account.

More Paul Price:

- Short-Term Variations Make Us Crazy. They Also Create Opportunities.

- Investing Is a Marathon. Trading Is a Sprint.

- Fun Facts That Help Investors Make Money

At the time of publication, Price was long CRI shares, short CRI March 2025 expiration date puts.