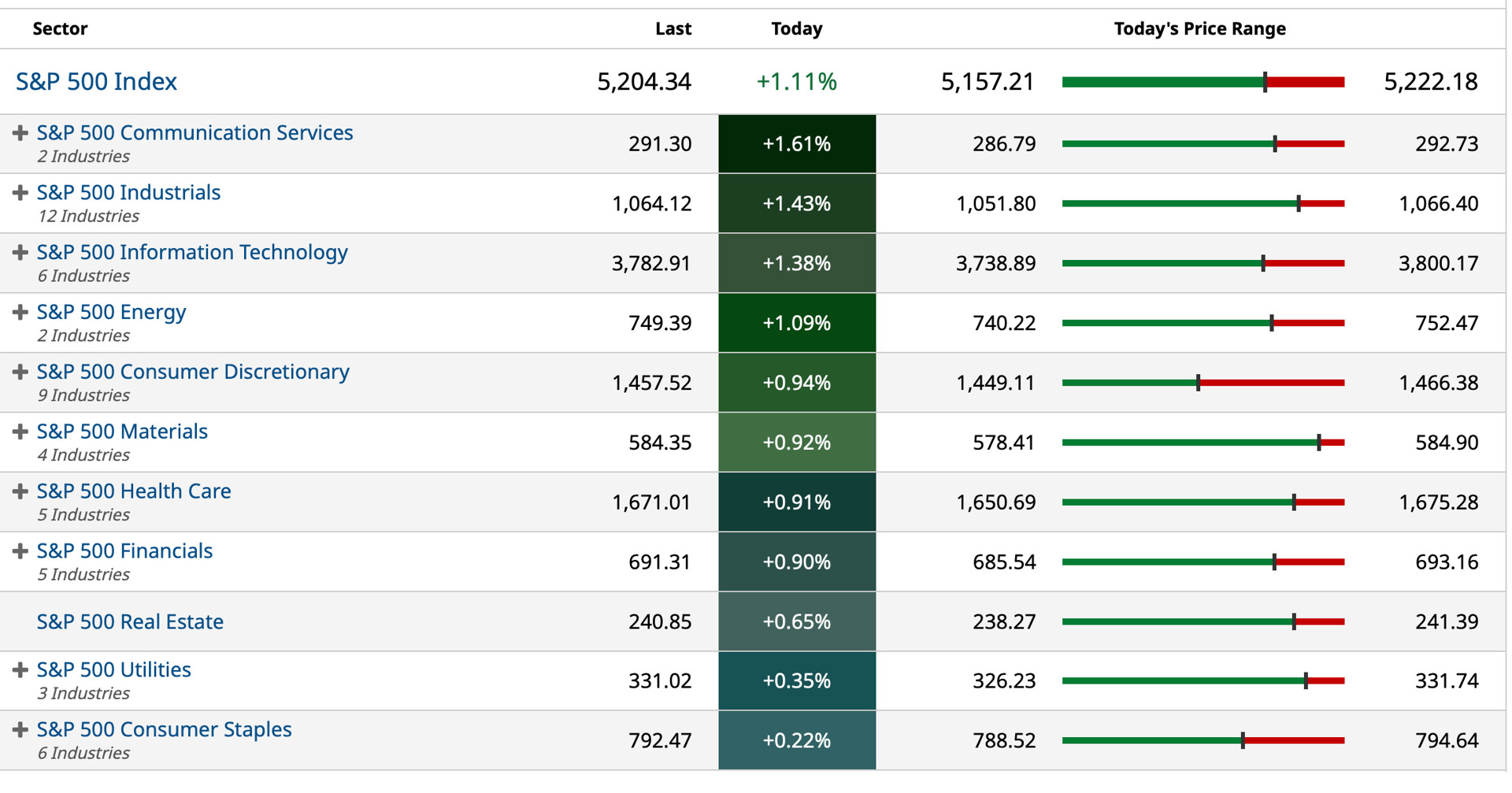

S&P 500 Sector Indices

* At the close...

BY Doug Kass · Apr 5, 2024, 4:35 PM EDT

* At the close...

BY Doug Kass · Apr 5, 2024, 4:35 PM EDT

From Peter Boockvar:

Succinct Summation of the Week’s Events:

Positives,

1)March payrolls grew by 303k, 89k more than expected with 232k of that being from the private sector. Also, the two prior months were revised up by a combined 22k. The household survey showed strength too, rising by 498k after 4 months in the past 5 of declines but all came from those aged over 55 and under 25. There was a drop in household employment for those aged 25-54, the key working cohort. The labor force was up by a similar amount, by 469k and the mix put the unemployment rate at 3.8% vs the 2 yr high of 3.9% last month. Also, hours worked ticked up to 34.4 from 34.3 and better than the estimate of no change. Average hourly earnings rose .3% m/o/m as expected but February was revised up by one tenth. The y/o/y gain was 4.1%. Average weekly earnings were higher by 4.1% too. The labor force participation rate rose two tenths to 62.7%, though still below the February level of 63.3%. The 25-54 age category saw a one tenth drop in its participation rate to 83.4% but above the February 2020 level. Job leavers as a % of unemployed, measuring quits essentially, rose to 12.7% from 11% in February and 12.8% in January. Again, most of the jobs, 2/3 of which, came from 3 groupings, leisure/hospitality, private education/health and government with gains of 49k, 88k and 71k respectively. Construction too helped, rising by 39k but tough to say how many of which were government induced with the IRA and Chips Act encouraged projects. For the private sector, the 3 month average is now 212k vs the 6 month average of 183k and the 12 month average of 189k.

2)ADP said a net 184k private sector jobs were created in March, 34k more than estimated and follows a gain of 155k in February (revised up by 15k). Most of the jobs came from medium and large companies with just 16k coming from small ones. On wages, for ‘job stayers’ they grew by 5.1% y/o/y, the same pace seen last month. Wages for ‘job changers’ spiked by 10% y/o/y and a notable rise from the 7.6% y/o/y gain in February. ADP said “The three biggest increases for job-changers were in construction, financial services, and manufacturing.” Smoothing out the monthly volatility in the data, the 3 month average is 150k vs the 6 month average of 137k and the 12 month average of 204k.

3)Continuing claims fell by 19k w/o/w to back under 1.8mm at 1.79mm.

4)The March ISM manufacturing index finally got back to a 50 handle for the first time since October 2022 at 50.3 vs 47.8 in February and 49.1 in January. That was 2 pts above expectations. Breadth improved slightly as 9 industries of 18 surveyed seeing growth vs 8 in February while 6 said their business contracted vs 7 in the month before. The balance saw no change in business.

5)The S&P Global manufacturing index fell a touch to 51.9 from 52.2, though above 50 for a 3rd straight month.

6)Here's an update on shipping rates as they continue to moderate after the spike seen off the lows in January. The World Container Index trip from Shanghai to Rotterdam for a 40 ft container averaged $3,078, down $81 on the week. That's still about double the 2023 year end rate but off the January highs of $4,984. The Shanghai to LA route, the price fell $121 to $3,704 for the week ended 4/4. It started the year at $2,100 and touched $4,344 at the end of January.

7)From Conagra: Benefiting from eat at home, “trends in consumption across our key domains reinforce our confidence in even further volume recovery...And encouragingly, that momentum has continued in Q4, driven by frozen."

8)The March Hong Kong PMI got back above 50 at 50.9 from 49.7. S&P Global said "The renewed rise in new orders was especially noteworthy, marking only the 2nd time that new business has increased in the past 9 months. Furthermore, cost pressures eased for Hong Kong SAR private sector firms with average input prices rising at the slowest rate in three years. Output price inflation was also modest despite rising from February. That said, sentiment remained weak with the level of pessimism heightening from February. This showed that firms are not yet convinced of a sustained rebound in output."

9)China's private sector Caixin services PMI rose a touch to 52.7 from 52.5 and better than the estimate of no change. Caixin said "Faster new business growth underpinned the latest acceleration of services activity expansion. The rate of new business growth was solid and the quickest since last December. Anecdotal evidence revealed that improvements in underlying demand conditions and business development efforts helped to boost the rise in new work." As for the outlook, "Surveyed companies expressed confidence for the coming year, keeping the gauge tracking business expectations about future activity in expansionary territory. However, the reading was below its historical average."

10)The private sector focused Caixin March manufacturing PMI was little changed, though still higher than 50 at 51.1 from 50.9 in February. Caixin said "This was driven by greater inflows of new work, including from abroad. In turn, Chinese manufacturers increased production, while also raising their purchasing levels amid improved optimism. That said, a cautious stance was maintained with regards to staffing levels." Also, input costs fell for the 1st time in 8 months. Of note too, "Overall optimism among Chinese manufacturers improved for a 3rd straight month in March...The level of business confidence was the highest seen since April 2023."

11)The March China manufacturing component got back above 50 at 50.9 from 49.1 in February and above the estimate of 50.1.

12)With regards to the Chinese consumer, Macau said March casino revenue rose 53.1% y/o/y which was above the estimate of 49.2%.

13)Singapore continues to be a standout in Southeast Asia as its PMI printed 55.7, though down 1.1 pts m/o/m. S&P Global said "Singapore's private sector continued to expand at a solid pace in March, extending the strong growth conditions seen throughout the first quarter of 2024. Notably, forward looking indicators including new orders and backlogs of work continued to rise at steep rates, hinting at sustained business activity growth in the coming months."

14)Indonesia's PMI was above 50 at 54.2 from 52.7 and continues to be an economic bright spot in the region. The Philippines too was above 50 at 50.9 vs 51.

15)The Q1 Japanese Tankan manufacturing index was little changed at 11 vs 12 in the quarter before but 1 pt above the estimate and the outlook rose 2 pts. The service sector index and outlook both exceeded expectations. For small business, the manufacturing index and outlook were around zero but services outperformed.

16)The March Eurozone's services PMI was revised to 51.5 from 51.1 and up from 50.2 in February. S&P Global said, "The improvement in new orders was confined to domestic markets, however, as new export business continue to fall (albeit only marginally)." Employment did rise for a 38th straight month but did slow." Price pressures did ease "but remained steep overall." With respect to expectations from here, "The outlook for business activity over the next 12 months improved for a 4th month in a row."

17)The Eurozone March manufacturing PMI was revised slightly higher to 46.1 from its initial print of 45.7. Germany's manufacturing sector remains deeply in a recession at 41.9 while Italy's is back above 50 at 50.4 and France sits at 46.2. S&P Global said this, "In the first quarter, the pace of the decline in incoming orders slowed considerably. However, there are still significantly fewer orders coming in than in the previous month. It is therefore to be expected that the industry is on the verge of surpassing the longest contraction spell for incoming new orders in the survey history, which was 25 months during the euro crisis in 2011 to 2013. This does not speak for a quick turnaround in activity."

18)The UK services PMI for March was revised to 53.1 vs 53.4 initially and down from 53.8 in February. It's however been above 50 for 5 consecutive months "supported by sustained improvements in new order intakes...Survey respondents once again commented on a turnaround in business and consumer spending, despite constraints on clients' budgets from strong inflation and elevated borrowing costs." Input costs "continued to rise sharply" but prices charged did slow. "However, this index only edged downwards since last summer and it remains well above the long-run trend, therefore adding to signs of sticky inflationary pressures in the domestic economy so far this year."

19)The March UK manufacturing PMI is doing better than its bigger European peers Germany and France. It's index was revised to 50.3 from 49.9 initially and up from 47.5 in February. S&P Global cited stronger domestic demand for the uplift and the outlook rose to an 11 month high. The caveat, "Potential blockers remain such as continued weak export performance and supply chain stresses, with the neighboring EU market the main drag on overseas demand and the Red Sea crisis still impacting supply chains. Signs from the survey that the impact of both of these factors is easing is therefore welcome news."

20)March CPI in Eurozone rose 2.4% headline y/o/y and 2.9% core, both one tenth below expectations and each down 2 tenths from the month before. A slowdown in the pace of gains in non-energy good prices drove the deceleration as service prices rose 4% y/o/y for a 5th straight month.

21)India’s manufacturing and services composite index was revised up to 61.8 from 61.3 initially for March, up from 60.6 in February. Services led the way but manufacturing was strong too.

Negatives,

1)In the household survey, all the jobs continue to come in part time, not full, with many for those under the age of 24 and those over 55.

2)Job openings in February totaled 8.756mm, about as expected and little changed with January’s figure of 8.748mm. These are the smallest amount of job openings since early 2021, though still above the pre Covid level of about 7mm. That said, I do believe there is a lot of double/triple counting now due to work from home capabilities. The hiring rate was 3.7% vs 3.6% in January and 3.7% in December (was 3.9% in February 2020). The quit rate held at 2.2% for a 4th straight month but at the lowest since March 2018 not including Covid.

3)Initial jobless claims rose to 221k from 212k, 7k more than anticipated and the prior week was revised up by 2k.

4)The March ISM services PMI fell by 1.2 pts m/o/m to 51.4 and that was below the estimate of a slight gain to 52.8. That’s also a 3 month low and the 2nd lowest print since May 2023. In contrast to the BLS report, Employment was up .5 pt but at 48.5 is below 50 for the 3rd month in the past 4 and follows a below 50 print seen in manufacturing. Breadth weakened too as 12 of 18 industries saw growth vs 14 in February and 4 reported a contraction vs 3 last month.

5)The S&P Global services March PMI index was 51.7 vs 52.3 in February and also a 3 month low. Of note, they saw a much different inflation picture than ISM. S&P Global said “Both input costs and output costs increased sharply in March, often as a result of rising wages. In fact, the respective rates of inflation quickened to six and eight month highs to rise further above pre-pandemic averages.” Add in their manufacturing index and they said this, “Rising raw material and fuel prices are also adding to cost burdens, which is in turn driving average selling prices for goods and services higher at a rate not seen since July of last year. Both manufacturers and services providers alike are seeing intensifying cost and selling price inflation rates, which is likely to feed through to higher consumer price inflation in the near term.”

6)March auto sales were weaker than expected totaling 15.49mm SAAR, below the estimate of 15.85mm. For perspective, sales were 17.5mm in March 2019.

7)Weekly mortgage applications were down slightly w/o/w with purchases flattish and refi’s lower by 1.6%. The average 30 yr mortgage rate is back to a one month high according to Bankrate.

8)For the week ended 3/20, C&I loans outstanding fell for the 5th week in the past 6 and at $2.739 Trillion, is at the smallest level since September 2022.

9)From Paychex: "The macroeconomic and labor market remains challenging for small and mid sized businesses. A tight job market for qualified workers, reduced access to affordable growth capital, and inflationary pressures continue to be headwinds for small businesses. Our small business employment watch continues to show moderation in both job growth and wage inflation. But however, a relatively stable macro environment. The softening in hiring we started to see in the 2nd quarter continued in the third quarter. There is more choppiness in hiring across all customer segments and industries now. Our clients tell us they still can't find qualified employees and are not willing to hire just anyone at higher wage rates, especially in areas with recent minimum wage increases and aggressive legislative changes."

10)From Lamb Weston: "Turning now to the demand environment. Overall, global French fry demand remains resilient, but we believe it's currently at or below the historical annual growth rate of about 2% to 4%. According to restaurant industry data providers, restaurant traffic trends in the US have been generally flat to slightly down during the past six to nine months, as consumers continue to adjust to the cumulative effect of inflation on menus." Bottom line from Lamb Weston, "So, on the one hand, fries remain as popular as ever with consumers. But on the other hand, consumers are going out to eat less often. Because of these trends, we're taking a cautious view of the consumer."

11)From Ulta Beauty: "Economically, there's kind of mixed data points around the economic situation for the majority of consumers with healthy employment rates, wage growth, but also pressures that we see with rising credit card debt, student loan dynamics, other pressures that we certainly within our guests. Then more broadly, we know what's going on in the world around us, whether it's some of the political challenges, global complex and then our political environment here as we go through an election year. So it just creates this soup of activity for our consumers that they're trying to navigate through… What we've seen so far is a slowdown in the total category across price points and segments. That's a bit earlier and a bit bigger than we thought. Still growing, still a lot of engagement, all those things that I've had, but we've seen this growth rate come down probably faster than we anticipated."

12)From Dave & Busters: "the choppiness we've seen is really from a visitation perspective. But once people are in the door, they're still spending at the same levels they've always spent. The dwell times are just the same as they were before. So it's really more of that visitation aspect of it than it is anything else...We've seen a little bit of weakness on the lower income consumer. But at the same time, we've seen strength on the higher end consumer. And everybody in between is kind of acting in their normal fashion."

13)From PVH: "Since we spoke in December, we have seen consumer sentiment further slow across Europe, especially in our two biggest markets, Germany and the UK, and we have seen our wholesale partners there become even more cautious." It's Asian business was good and in North America, retail did ok while wholesale was soft as said. And bottom line in terms of their guide, "we have taken a cautious approach to planning 2024 due to the softening consumer backdrop we saw in January and February in a conservative wholesale environment."

14)From MSC industrial: "growth has not yet inflected in our core customer base in the face of a sluggish macro environment, particularly in our heavy manufacturing end markets. This can be evidenced in the performance of our top 100 national accounts where only 45 were growing last quarter. As a result, revenue growth to data has been below our expectations…From an end market perspective, we experienced acute demand softness in heavy manufacturing verticals including end markets and tiered suppliers that support the earlier stages of production in automotive.""

15)German factory orders and French industrial production were both lighter than forecasted.

16)Most other manufacturing PMI's in Asia remained below 50 and thus still in contraction but the outlook has improved. South Korea's, 49.8 vs 50.7, Japan 48.2 vs 47.2, Australia 46.8 vs 47.8, Taiwan 49.3 vs 48.6, Vietnam 49.9 vs 50.4, Thailand 49.1 vs 45.3, and Malaysia 48.4 vs 49.5.

17)South Korean March exports grew by 3.1% y/o/y, just below the estimate of up 4.2% but semi exports were particularly strong, higher by 36% y/o/y.

18)With respect to stock market sentiment, we’ve entered flashing red bullish extremes in the Citi Panic/Euphoria index and the nearly 50 pt Bull/Bear spread from Investors Intelligence. Tough to time, but important to recognize.

BY Doug Kass · Apr 5, 2024, 4:27 PM EDT

- NYSE volume 369M shares, 16% below its one-month average;

- NASDAQ volume 3.70B shares, 10% below its one-month average

- VIX: down 1.35% to 16.13

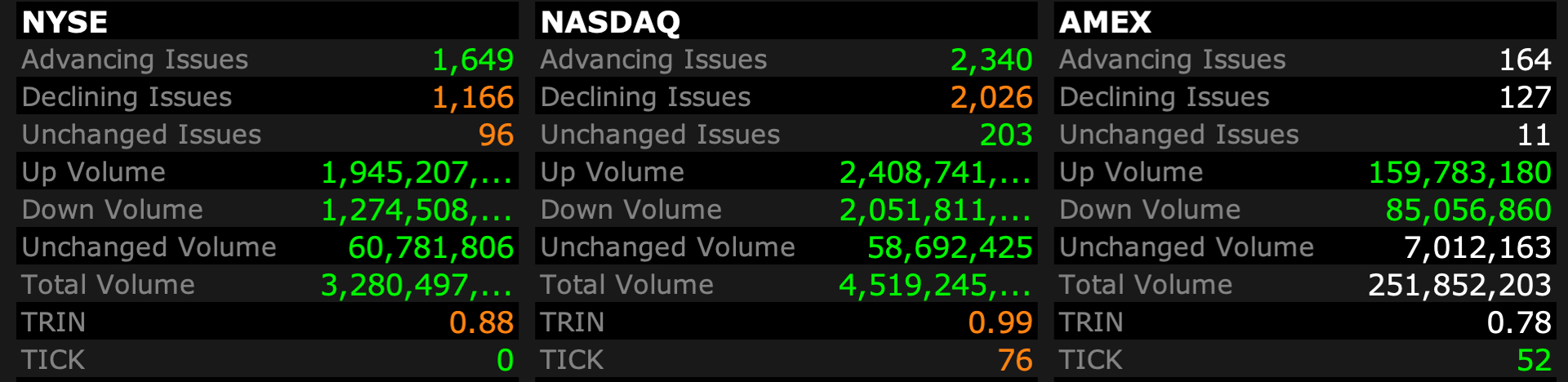

Market Breadth

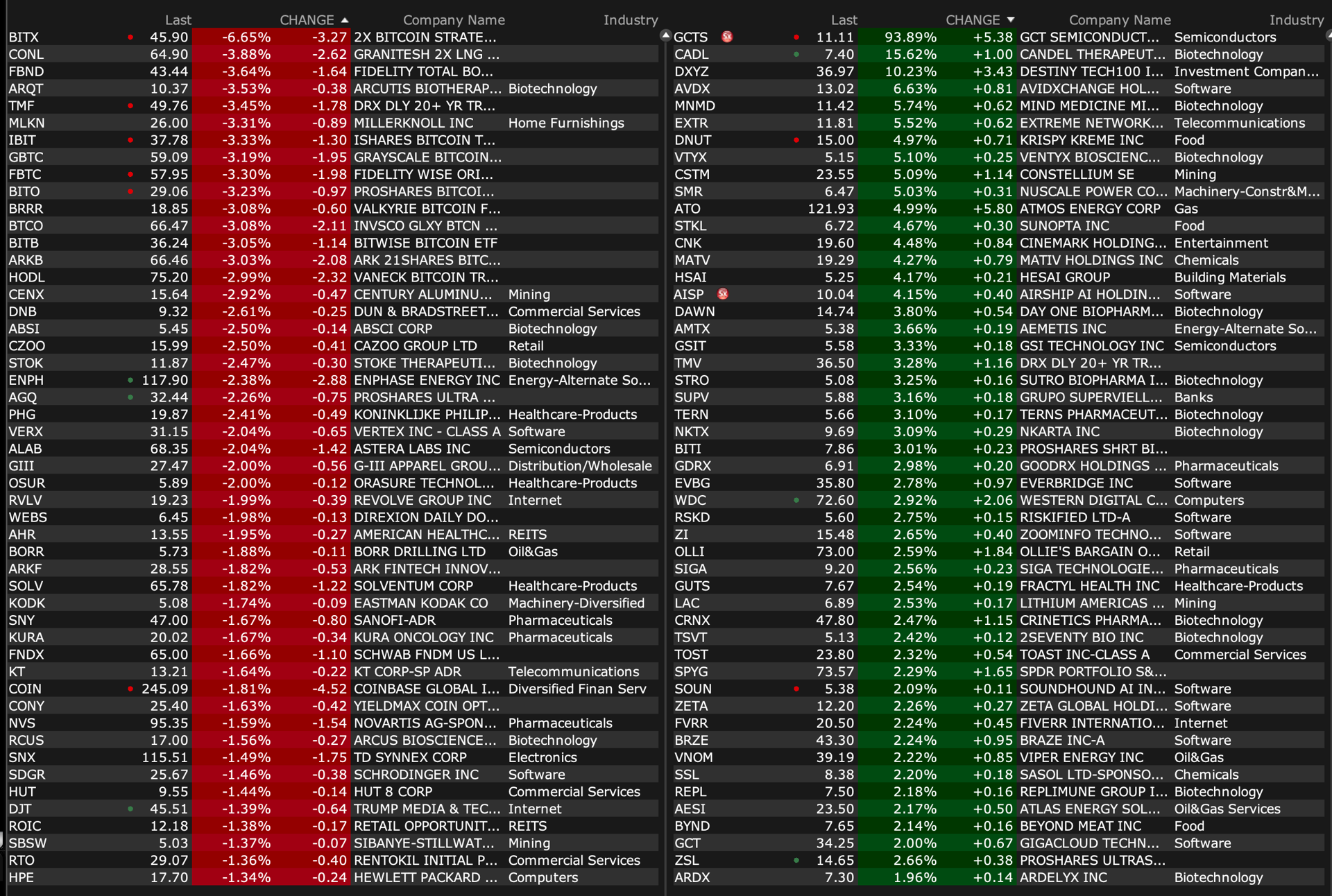

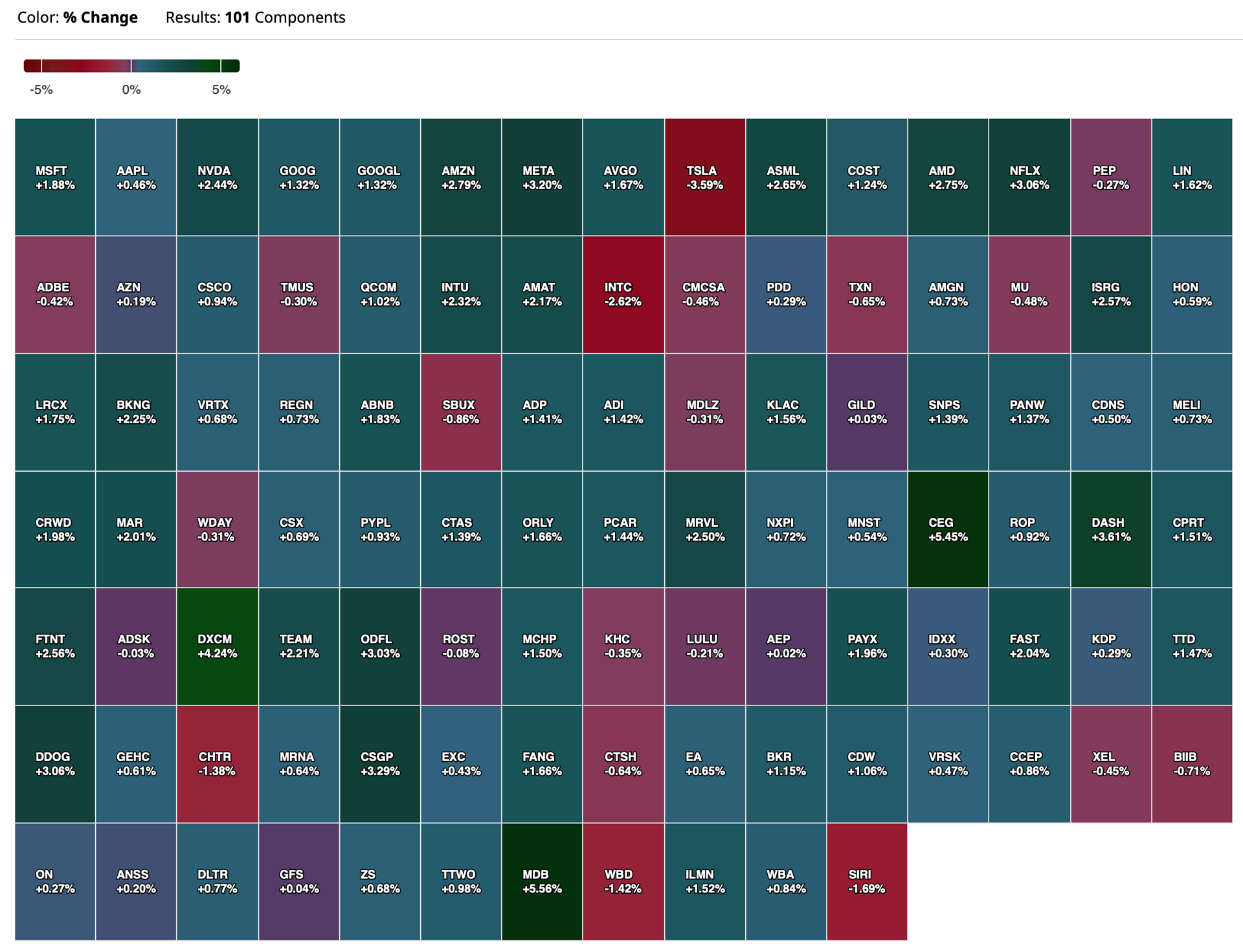

Nasdaq 100 Heatmap

BY Doug Kass · Apr 5, 2024, 4:18 PM EDT

Wolf Street howls about the economic data.

BY Doug Kass · Apr 5, 2024, 4:07 PM EDT

Back short SPY $518.82 and QQQ $440.85.

BY Doug Kass · Apr 5, 2024, 4:00 PM EDT

I will be out of the office at a lunch with some friends.

Radio silence for the next ninety minutes.

BY Doug Kass · Apr 5, 2024, 12:15 PM EDT

Really good:

rolf

1) Known Knows - Inflation and valuations

2) Known Unknowns - Economic Growth - Most economists got the last year wrong so Fin TV commentators talk about Goldilocks

3) Unknown Unknowns

BY Doug Kass · Apr 5, 2024, 12:00 PM EDT

With S&P cash +60, I'm getting a bit more serious in the short side now.

BY Doug Kass · Apr 5, 2024, 11:58 AM EDT

As promised —with S&P cash +33 handles — I am back shorting Index calls and moving up my short exposure.

Selling May SPY and QQQ (in the money) calls short.

Also expanding my straddles.

BY Doug Kass · Apr 5, 2024, 10:21 AM EDT

* Many of our previous concerns were adopted yesterday by many market participants...

Several factors contributed to Thursday's market schmeissing — and conspicuous reversal from the early morning highs.

I would note that most, if not all of these reasons (mentioned below), have been expected by us and were at the core of our adding to our short exposure in equities:

* Geopolitical tension (Middle East). (This has been a dominant theme of ours)

* The escalation of tension between Iran and Israel has served to buoy oil prices and fan more inflationary fears.

* The likelihood of higher for longer — and less Fed easing than the consensus expects. (Another core expectation)

* Interest rates have been climbing for several months (the 10-Year U.S. note broke the prior resistance at 4.33% this week) — no longer ignored by the markets. (The equity risk premium, as noted earlier in the week, is at the thinnest level in sixteen years.)

* Accumulating signs of "slugflation" (sticky inflation and slowing economic growth and corporate profits).

* Recognition that the CRB has been on a higher path for weeks.

* All-time highs in silver and gold.

* Market breadth has been deteriorating. (The market, despite protestations from the bullish cabal, has not broadened out).

* We have warned that when energy is a market leader — it is generally a characteristic of a maturing bull market.

* Valuations are extended (having moved into the 95% tile), leaving little room for error.

* Finally, as noted in my Diary and by Peter Boockvar, investor sentiment had moved into a bullish extreme (nary a bear was to be found in recent weeks) — as many historical market valuation metrics have moved into the 95% tile.

There is always a reasonable chance that markets ignore risks — even on a prolonged basis (as we have recently learned).

Unfortuantely, the expiration date is uncertain and to an extent unknowable.

This helps to explain why I almost always "average into" positions — in the recognition that I can not (nor can anyone else) forecast bottoms and tops!

BY Doug Kass · Apr 5, 2024, 10:15 AM EDT

* I moved to medium-sized long on Viking Therapeutics VKTX.

* I am no longer net short the Indices — reduced short Index calls and have straddles on.

I plan to re-short any rally.

Lesson learned recently... Bull markets die hard.

BY Doug Kass · Apr 5, 2024, 9:55 AM EDT

From Peter Boockvar:

The jobs headline looks great but contributes to more confusion when adding other things so help me out.

I will start this rundown on the jobs data by saying I and we should have no idea what the influence in the official jobs data of the massive immigration that has occurred of late. Do we know how many jobs are getting filled by legal immigrants as if they are illegal, I doubt someone is answering the BLS surveys? An employer is not telling the BLS, ‘yeah, we just hired a bunch of illegals.’ And I doubt the BLS is calling new immigrants (legal or not) asking about their work status since they would be tough to locate. I’m not saying there is not an impact but trying to quantify it I find to be extraordinarily difficult.

March payrolls grew by 303k, 89k more than expected with 232k of that being from the private sector. Also, the two prior months were revised up by a combined 22k. The household survey showed strength too, rising by 498k after 4 months in the past 5 of declines. The mix though of this is important to note. All came from those aged over 55 and under 25. There was a drop in household employment for those aged 25-54, the key working cohort. The labor force was up by a similar amount, by 469k and the mix put the unemployment rate at 3.8% vs the 2 yr high of 3.9% last month.

Also, hours worked ticked up to 34.4 from 34.3 and better than the estimate of no change. Average hourly earnings rose .3% m/o/m as expected but February was revised up by one tenth. The y/o/y gain was 4.1%.

The labor force participation rate rose two tenths to 62.7%, though still below the February level of 63.3%. Job leavers as a % of unemployed, measuring quits essentially, rose to 12.7% from 11% in February and 12.8% in January.

Again, most of the jobs, 2/3 of which, came from 3 groupings, leisure/hospitality, private education/health and government with gains of 49k, 88k and 71k respectively. Construction too helped, rising by 39k but tough to say how many of which were government induced with the IRA and Chips Act encouraged projects. Manufacturing saw no growth in jobs as did ‘information’ on the service side. Temp help was shed again, by 1k while there was a slight add for financial services. Retail trade added 18k vs 23k in February and vs 17k in the month before. Trade/transport added 27k jobs.

To smooth out the data, and I’m going to take out the government jobs and focus here on the private sector so we can compare to ADP, the 3 month average is now 212k vs the 6 month average of 183k and the 12 month average of 189k. This compares with ADP which is at 150k, 137k and 204k respectively so at least out to 6 months, ADP is well under what the BLS is saying. Adding to the confusion, the key age group of 25-54 saw a household survey job decline.

So bottom line, with all these differentiating data points, I can’t honestly give you a conviction filled bottom line on the state of the labor market. Way too many confusing signals so help me out if you can.

Either way, Treasuries are responding to the headline figure and the 2 yr yield is up to 4.70%, up 5 bps in response while the 10 yr yield is higher by 6 bps to 4.38%. Rate cut odds for June are about 50/50 and 100% by July for 25 bps. There is now only a 50/50 chance of a 3rd rate cut by yr end with November 100% priced for a 2nd one.

BY Doug Kass · Apr 5, 2024, 9:45 AM EDT

8:30AM: Federal Reserve Bank of Boston President Susan Collins (Non-Voter) gives welcome remarks before virtual Conference on the Financial Stability Implications of Stablecoins hosted by the Federal Reserve Bank of Boston (Prepared text TBD);

9:15AM: Federal Reserve Bank of Richmond President Thomas Barkin (Voter) speaks before the Greater Baltimore Committee "Pulse Check: The Scorecard Summit 2024,” Linthicum Heights, MD (Text available. Audience Q&A expected. No separate media Q&A);

11:00AM: Fed Bank of Dallas President Logan (Non-Voter) speaks before an event hosted by the Duke University Department of Economics, Durham, NC (No livestream. Moderated Q&A follows. Text available. No media Q&A);

12:15PM: Fed Board Governor Bowman (Voter) speaks on "Risks and Uncertainty in Monetary Policy: Current & Past Considerations" before the Shadow Open Market Committee Spring Meeting, NYC (Text available. Q&A from moderator. Webcast available)

BY Doug Kass · Apr 5, 2024, 9:35 AM EDT

Upside:

-FAAS +42% (momentum)

-GRIN +26% (announces selective capital reduction for shares to be cancelled at $14.25/shr)

-TARA +20% (announces positive three-month data from TARA-002 clinical program in NMIBC; announces alignment with FDA on registrational path forward for IV choline chloride in patients dependent on parenteral nutrition and an oversubscribed $45M private placement financing)

-KRUS +6.0% (earnings, guidance)

-DNUT +5.3% (Piper/Sandler Raised DNUT to Overweight from Neutral, price target: $20)-LFLY +5.0% (NY court strikes down cannabis ad ban)

-CNK +4.5% (Wells Fargo Raised CNK to Overweight from Underweight, price target: $23)

-WDC +3.4% (hearing Rosenblatt Securities Inc. Raised WDC to Buy from Neutral, price target: $115)

-OCGN +3.3% (announces positive data and safety monitoring board review; Initiates enrollment in medium dose for OCU410, a Modifier Gene Therapy, in Phase 1/2 ArMaDa Study for Geographic Atrophy)

-OLLI +2.6% (Loop Capital Raised OLLI to Buy from Hold, price target: $90)

Downside:

-ABIO -6.8% (CEO to step down amid merger plans)

-ATUS -5.1% (Wells Fargo Cuts ATUS to Underweight from Equal Weight, price target: $1 from $2)

-PLUG -3.8% (CitiGroup Cuts PLUG to Sell from Neutral, price target: $2)

-JBT -3.0% (executes definitive transaction agreement related to JBT’s previously announced intention to make a voluntary takeover offer for all of the issued and outstanding shares of Marel [MAREL.IS] at ~€3.5B)

BY Doug Kass · Apr 5, 2024, 9:24 AM EDT

BY Doug Kass · Apr 5, 2024, 9:14 AM EDT

BY Doug Kass · Apr 5, 2024, 9:10 AM EDT

From Peter Boockvar:

Outside of pizza, what's better than French fries?/The Fed should be OUT of the business of dictating the fed funds rate/Kishida chimes in

Let's provide more evidence of a mixed economy, especially with the consumer. From the potato maker Lamb Weston:

After going thru their execution troubles with a new ERP system, "Turning now to the demand environment. Overall, global french fry demand remains resilient, but we believe it's currently at or below the historical annual growth rate of about 2% to 4%. According to restaurant industry data providers, restaurant traffic trends in the US have been generally flat to slightly down during the past six to nine months, as consumers continue to adjust to the cumulative effect of inflation on menus."

Here's more, "QSR traffic during the third quarter was flat versus a prior year after growing modestly during the first half of fiscal 2024. Several QSRs have attributed this to less visits by lower income consumers as their disposable income has been more affected by the overall inflationary environment. Meanwhile, traffic at full service restaurants has declined each quarter during fiscal 2024."

As for their international business, "Outside the US, restaurant traffic continued to increase versus the prior year in most of our key markets, but growth has also slowed sequentially from our fiscal 2nd quarter. Similar to the US, we believe traffic in these markets is also affected by consumers adjusting to the cumulative effect of inflation, as well as other macro headwinds."

Bottom line from Lamb Weston, "So, on the one hand, fries remain as popular as ever with consumers. But on the other hand, consumers are going out to eat less often. Because of these trends, we're taking a cautious view of the consumer."

A beneficiary of people eating less in restaurants and more at home is Conagra (a cheap stock we own) and the largest maker of frozen foods you can find at supermarkets, among other places. They also make snacks like Slim Jim and popcorn. They said this about their top line and volume growth, "which again saw sequential improvement driven by our brand building investments in key areas." Volumes and sales though were still down y/o/y.

"Additionally, trends in consumption across our key domains reinforce our confidence in even further volume recovery...And encouragingly, that momentum has continued in Q4, driven by frozen."

Here is what they said on the inflation situation where they got 4% from price, "Obviously inflation has slowed, but we're still in an overall inflationary environment. And some things more recently have inflated, and that has led to taking come price, so you get the benefit of that. But, there's a lag effect." Their inflation rate as a percentage of cost of goods sold in the quarter was 2.9% and they expect around 3% for the full year. They see inflationary pressures in tomatoes, and "more broadly in vegetables, in sweeteners, starches. We have some inflationary areas. These things ebb and flow."

Also with inflation, "We still have inflation in our manufacturing operations, both with our labor and overhead, and transportation. It's relatively flat, a little bit inflationary."

While there was a ton of Fed speak this week, I'll just mention Neel Kashkari's comments for a quick moment as it got some press yesterday. For my long term readers, you might know that I've been a critic of his views over the years so I take what he says with a grain of salt, especially in years where he doesn't vote like this year. Back on November 14th, 2021 he was on Face the Nation at a time when the Fed was just beginning to taper QE (so still doing it) and rates were STILL at zero and thus the Fed was dramatically behind the curve. Margaret Brennan asked him, "Neel, core inflation is at a 30 year high. Do you think we are at the peak or is it going to get worse?" He answered by acknowledging the high inflation (which got even higher in 2022) and mentioned the fiscal demand surge on one hand and supply challenges on the other but said "The good news is both of those should be temporary...But it's important from the Fed's perspective that we don't set long term monetary policy and adjust too much based on temporary factors, even if those temporary factors take a little bit longer than we expect...You know, the Federal Reserve, when we adjust monetary policy, it acts with a lag. And so, if we overreact to a short term price increase that can set the economy back over the long term." Understand that October CPI had just printed 6.2% and they still had rates at zero, only to finally raise them in March 2022 after February 2022 CPI got to 7.9%.

This is what he said yesterday, "In March I had jotted down two rate cuts this year if inflation continues to fall back towards our 2% target. If we continue to see inflation moving sideways, then that would make me question whether we needed to do those rate cuts at all."

My main point here is not to pick on Kashkari, it's more to highlight how treacherous the situation is when we are relying on Fed members to sit around a big table in DC and try to pick what they think the right interest rate should be. It's blatant price fixing the most important price out there. It's really hard to do and why the Fed should be OUT OF THIS BUSINESS and the markets should set the overnight rate instead. Sometimes the market will get it wrong but the beauty of markets is that it readjusts quickly to any mistakes. Well intentioned members at the Fed do not.

The only thing of note economically in Asia was the March Hong Kong PMI which got back above 50 at 50.9 from 49.7. S&P Global said "The renewed rise in new orders was especially noteworthy, marking only the 2nd time that new business has increased in the past 9 months. Furthermore, cost pressures eased for Hong Kong SAR private sector firms with average input prices rising at the slowest rate in three years. Output price inflation was also modest despite rising from February. That said, sentiment remained weak with the level of pessimism heightening from February. This showed that firms are not yet convinced of a sustained rebound in output."

I'm still sticking with our longs and believe the Hong Kong stock market has bottomed.

Of note too, we now have the Prime Minister of Japan Fumio Kishida that is chiming in on the yen. "It's important for currencies to move in a stable manner based on fundamentals, and excessive volatility is not desirable. The government is watching the FX market with a sense of urgency, and we will act appropriately against excessive moves without ruling out any options." No response though by the yen which is unchanged as are JGB yields.

In Europe, while dated data, German factory orders and French industrial production were both lighter than forecasted while better than estimated in Spain. Spain has been one of the few bright spots in the European region and has outperformed economically its bigger peers.

BY Doug Kass · Apr 5, 2024, 9:00 AM EDT

* Risk happens fast

* For the first time since January, the Oscillator has moved into negative territory

* Bond yields fell on Thursday in a "flight to safety" but have turned by (by 2-3 basis points) today

* The U.S. dollar is stronger against the yen

* Oil is up again (+$0.35) after this week's ramp higher

* Gold is up following a move to all-time highs (silver has been turbocharged!)

* Bitcoin is -$1,500 in a risk-off atmosphere

* Chart of the Day (from Hedgeye)

“Monday mornin' feels so bad

Ev'rybody seems to nag me

Comin' Tuesday I feel better

Even my old man looks good

Wed'sday just don't go

Thursday goes too slow

I've got Friday on my mind”

- The Easybeats, “Friday on My Mind”

"Workin' on our night moves Trying to lose the awkward teenage blues Workin' on our night moves In the summertime And oh the wonder Felt the lightning And we waited on the thunder Waited on the thunder."

- Bob Seger, "Night Moves"

This daily Futures feature is like inside baseball. I try to show you and write about what I believe thoughtful hedge fund managers are looking at when they awake -- let's call it our normal routine -- setting the stage for their strategy for the day. The market is a complicated mosaic and the more info you have, the better trader and investor you will be!

The market (and money) never sleeps -- and neither do I, it appears! I have previously described the importance that overnight futures trading hold for me here. It is a guidepost to my strategy in the regular trading session. Moreover, the overnight/early morning futures hold opportunities as they are (1) inefficient, though liquid and (2) it seems fear and greed are often exaggerated outside the regular trading session. I frequently try to capture those efficiencies by trading actively both in the pre- and after-market sessions.

Here are brief observations I wanted to highlight and provide a summary of overnight price movements in various asset classes:

* Stock futures were a bit higher overnight. S&P futures peaked at +17 and bottomed at -6. Nasdaq futures peaked at +71 and bottomed at -18. At 7:21 a.m. ET, S&P futures were +15 and Nasdaq futures were +62.

* Commodities were mixed with Brent crude +$0.32 after a stellar run higher.

* The S&P Short-Range Oscillator moved into negative territory for first time since late January at -0.31% vs. 2.09%.

* The VIX is at 16.62 (+0.09). I re-established some straddles on the recent VIX run over 15 and added yesterday after the spike in volatility.

* The U.S. dollar is stronger against the yen.

* Overnight, the inversion of the 2s/10s Treasuries curve is flat at -33 basis points

* Gold is +$3.60 and sits at $2,312. Turbocharged silver (on everyone's radar now) is -$0.40 to $26.85.

Here is a synopsis of some of my columns I believe were important, or in the event you were out for the day and/or did not read my Diary. The principal intent is to review the logic of my market moves and other factors:

Will Investors' Intelligence Become an Oxymoron?

Watching in Awe (the strength did not continue!)

Here were yesterday's trades:

* Covered SPY and QQQ common shorts on market schmessing (I had shorted some SPY and QQQ on the pre-morning spike!):

Premarket Trading

* Of a 4:01 a.m. kind...

I have moved from very small SPY/QQQ common shorts to small size in premarket trading.

* SPDR S&P 500 ETF (SPY) $521.32

* Invesco QQQ Trust (QQQ) $444.06

Also, I added to AdvisorShares Pure US Cannabis ETF MSOS on weakness. And I increased the size of my straddles (with higher VIX).

BY Doug Kass · Apr 5, 2024, 8:29 AM EDT

As promised, with the increase in volatility (on Thursday), I added to my index straddles.

BY Doug Kass · Apr 5, 2024, 7:50 AM EDT

* A brief discussion of my strategy in the sector...

* I remain a $9-$9.50 buyer of AdvisorShares Pure US Cannabis ETF MSOS

Cannabis equities made an early-morning high Thursday but prices fell dramatically in the afternoon:

Several factors contributed to an outsize drop in cannabis stocks yesterday:

1. Confusion in New York regulatory actions

The New York regulatory situation has been a confusing mess for some time, so I discount this as a continuing issue.

2. More negative comments from Florida Governor DeSantis (a repeat of his previous position, so really not new), but I have been always concerned about the November vote:

The purest Florida play, Trulieve Cannabis TCNNF, fell by about 12% on the session, reflecting specific Florida concerns.

3. A risk-off market, which took down many high-octane sectors, such as cannabis.

4. Normal profit taking after swelling sector optimism, after a swift runup in MSOS et al.

From Wednesday:

APR 3, 2024 11:24 AM EDT

The Latest on Cannabis Stocks

As expected, cannabis stocks have been sold off (a bit!) after the Florida news -- (MSOS) is now under $10 after trading close to $11 last week:

My Cannabis Comment of the Day (April 1, 2024)

With (MSOS) trading at $10.65:

I wouldn't be surprised if we see a sell on the news now on MSOS - after the initial bump higher as expected.

There is still a lot of heavy lifting for voters to approve the measure on the ballot.

I am a $9-$9 1/2 buyer of MSOS.

I previously had taken gains in some individual stocks, among them Green Thumb Industries GTBIF and Curaleaf CURLF.

On yesterday's large sector selloff, MSOS fell back into my buying range and I began to add to my position at around $9.25. I plan to continue to add on weakness.

Also, subject to market conditions I may begin to buy back the CURLF and GTBIF I had previously sold.

BY Doug Kass · Apr 5, 2024, 7:36 AM EDT

“I think investors always learn the lessons of the recent past. And that is the lesson.”

- Seth Klarman

Bonus - Here are some great links:

The Fed is not cutting three times in 2024

BY Doug Kass · Apr 5, 2024, 7:10 AM EDT

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Apr 5, 2024, 6:47 AM EDT

From "Jazzy" Jeff Hirsch:

With the Seasonal MACD Sell signal for DJIA and S&P 500 triggering on the prior day, Jeff focused on the transition the portfolios will be undergoing in anticipation of the “Worst Months” along with a recap of the major seasonal patterns that we have been following recently.

In closing Jeff reiterated that we remain bullish for the full year, but with bullish sentiment soaring to multi-year highs, sizable “Best Months” gains in the portfolio, and a Fed that does not appear to be in any hurry to reduce rates, that the market appears vulnerable to some profit taking and even a mild pullback in the near-term.

Paltry “Worst Months” in Election Years

In the following table the “Worst Months” performance of DJIA, S&P 500, and NASDAQ have been separated by year of the four-year-presidential-election cycle going back to 1951 for DJIA and S&P 500 and 1971 for NASDAQ. NASDAQ’s “Worst Months” are July through October compared to May to October for DJIA and S&P 500. In 18 election year “Worst Months” periods, DJIA has averaged a meager 0.68%. S&P 500 is modestly better +2.28% while NASDAQ’s average is under just 0.49%. Frequency of gains or percentage of time higher in election years “Worst Months” ranging from 61.1% by DJIA to 77.8% for S&P 500.

Despite gains occurring frequently in election year “Worst Months,” average performance for either a four- or six-month period is rather disappointing. Of the 18 election years, only two produced double-digit gains, 1980 and 2020. In 1980 a mild bear ended on April 21 and in 2020 the pandemic induced bear market bottomed on March 23. This year has been the exact opposite with five straight months of gains and well-above average gains in Q1. Two wars raging, elevated geopolitical tensions, an uncertain Fed as inflation’s retreat slows, and a volatile presidential election. Overall risk is high while historically the reward has been lackluster during the “Worst Months.”

Because of the elevated level of risk that has been historically observed during the “Worst Six Months” of the year and its historically tepid returns, reducing long exposure and developing a defensive strategy is the approach we are taking in the Almanac Investor Stock and ETF Portfolios. We do not merely “sell in May and go away.” Instead, we take some profits, trim or outright sell underperforming stock and ETF positions, tighten stop losses and limit adding new long exposure to positions from sectors that have a demonstrated a record of outperforming during the “Worst Months” period. This week’s Seasonal MACD Sell Signal for DJIA and S&P 500 marks the start of a transition to a more cautious stance.

For those with a lower risk tolerance or a desire to take a break from trading, the “Worst Months” are a great opportunity to unwind longs and move into the relative safety of cash, Treasury bonds, gold and/or some combination of traditional defensive assets. Holding cash finally earns something other than zero. Preservation of capital may be more important than growth; the “Worst Six Months” are a good time to simply step aside if you prefer. August, September and/or October have provided some excellent buying opportunities in recent years and could do the same again this year.

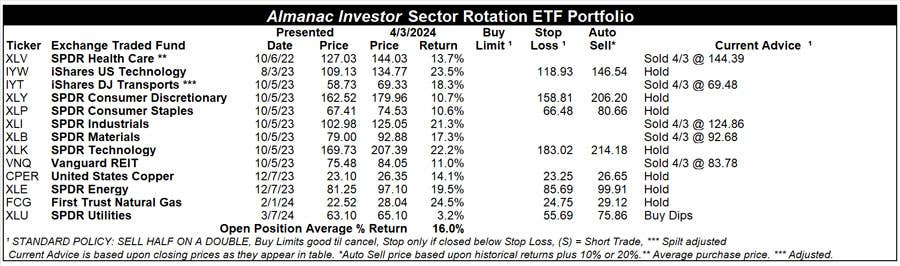

Sector Rotation ETF Portfolio Updates

In accordance with Tuesday’s Seasonal MACD Sell signal email Issue, SPDR Health Care (XLV), iShares DJ Transports (IYT), SPDR Industrials (XLI), SPDR Materials (XLB) and Vanguard REIT (VNQ) have been closed out of the portfolio using their average prices on April 3. The average gain across these five positions was 16.3% excluding dividends and trading costs. The largest gain was 21.3% by XLI while VNQ produced the smallest advance at 11.0%. All five of these ETFs are correlated to Sectors that end their historically favorable period in May. In addition to the seasonal factors, a rising crude oil price has historically been a negative on Transports, and to a lesser degree Industrials and Materials. Rate uncertainty and a rising 10-year Treasury yield was also weighing on Real Estate while parts of the Healthcare sector were hit earlier this week with disappointing Medicare Advantage plan payments.

Crude oil hitting a 6-month high is supporting SPDR Energy (XLE). Summer driving season is just around the corner which suggests demand will be rising while geopolitical events are escalating fears of supply disruption. XLE was up 19.5% at the close on April 3, and is closing in on its auto-sell price of $99.91. Officially, we will heed our policy if that price is reached, but as an alternative to outright selling, one could utilize a trailing stop approach.

Despite the struggles of natural gas, First Trust Natural Gas (FCG) is performing even better, up 24.5%. FCG’s holdings provide a fair amount of exposure to crude oil. As long as crude oil is climbing FCG is also likely to continue to rise. Should it reach its auto-sell price, it could be handled like XLE.

Except for SPDR Utilities (XLU), all positions in the Sector Rotation portfolio are on hold. Please note that some stop losses have been updated to account for gains since the last update.

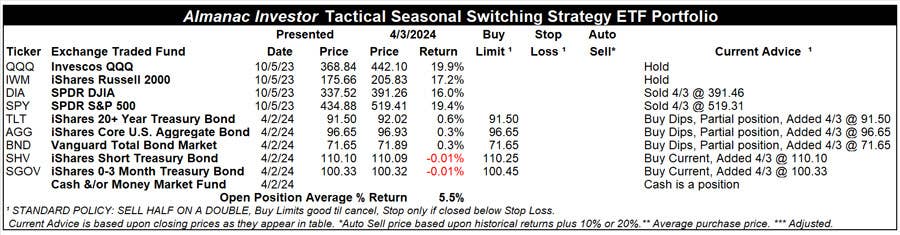

Tactical Seasonal Switching Strategy ETF Portfolio Updates

In accordance with Tuesday’s Seasonal MACD Sell signal email Issue, SPDR DJIA (DIA) and SPDR S&P 500 (SPY) have been closed out of the portfolio using their respective average prices from April 3. DIA was sold for a 16.0% gain and S&P 500 had a 19.4% advance, excluding dividends and any trading costs. NASDAQ’s Seasonal MACD Sell signal has not triggered. Invesco QQQ (QQQ) and iShares Russell 2000 (IWM) are on Hold. From now until sometime on or after June 3, 2024, the earliest date that NASDAQ’s Seasonal MACD can trigger, we will be transitioning to a more cautious stance in the portfolios.

Part of this transition is reducing exposure to DJIA and S&P 500 correlated holdings and moving into bond ETFs, cash, and money market funds. Accordingly, we have added positions in TLT, AGG, BND, SHV, and SGOV to the portfolio as detailed in Tuesday’s Seasonal MACD Sell email. SHV and SGOV can be considered at current levels. TLT, AGG, and BND have exposure to long-dated Treasury bonds that have historically exhibited more price volatility than short-dated funds such as SHV and SGOV. Should economic data support the Fed cutting rates in June, TLT, AGG, and BND could enjoy solid price appreciation, but if the Fed is forced to delay reducing rates, and/or if inflation and growth accelerate, they could easily suffer losses. Due to this uncertainty, SHV and SGOV are currently our preferred bond ETFs.

As a reminder, traders/investors following the Best 6 + 4-Year Cycle switching strategy detailed on page 64 of the Stock Trader’s Almanac 2024 do not need to heed this Seasonal MACD Sell signal for DJIA and S&P 500. However, it is still a good reminder to review existing holdings and consider a cautious stance.

BY Doug Kass · Apr 5, 2024, 6:30 AM EDT

From JPMorgan:

US: Futs are higher pointing to a bounce back from yesterday’s late day slide; SPX traded in a 2% range. Yesterday’s sell-off had a number of reasons offered for the move (Middle East Escalation, Oil Price Spike, No Rate Cuts, etc); the moves appeared to be a flight to safety, so likely all of the above. Now, we have seen the first week of the year where the SPX has lost at least 70bps twice and is the first time since the week of Oct 23, 2023 whose close that Friday market the bottom before this current rally. Pre-mkt, bond yields/USD are stronger, cmdtys higher led by Energy products and base metals. In Eqys, Mag7 and Semis are higher pre-mkt; Samsung earnings may aid the move. From a macro perspective, NFP is the focus, Feroli is below the Street seeing +200k vs. +214k survey vs. +230k BBG’s whisper ; +275k prior.

and..

EQUITY AND MACRO NARRATIVE: A quick recap on the sell-off we experienced yesterday afternoon from my colleague Marissa Gitler: Chain market reaction …

· Crude spike (Middle East escalation)

· translated to a VIX spike, and equity selling

· Appeared to be more of stock flush than futures driven- the ES imbalance didn't indicated selling, but TICK index hit -1450

· Although Mester and Kashkari were both on the tape right - fixed income markets didn't begin to move until after equities sold off (and they didn't say anything all too meaningful for the narrative)

To add to Marissa’s work, if this were an adjustment of Fed expectations due to higher growth, the market moves do not support that hypothesis with bonds catching a bid and Cyclicals sold off aggressively. If this were a risk-off move, then it seems unlikely that NVDA should be down 3+%. Interestingly, Bitcoin and its related ETFs were up on the day; IBIT +4%. The moves feel similar to what we experienced on Tuesday but a bit more aggressive, essentially a flight to safety given with a geopolitical hedge.

Today’s focus is on the NFP print and associated labor market details. Feroli’s complete preview is highlighted below and have re-posted two bullet points from yesterday’s Morning Briefing.

· WHY THE PRINT MATTERS – A tight labor market/wage inflation are key drivers of sticky core inflation. So, an above expected print could lead to increased nervousness around inflation levels at a time when commodity prices are rising and may not hit a price ceiling until Q3. The impact could be similar to what the market has witnessed in 2023 and on Mon/Tues where higher bond yields drive stocks lower. The previous Average Hourly Earnings YoY print was 4.3% and we may need to get to 3 – 3.5% for the Fed to feel comfortable cutting rates.

· WHY IT DOESN’T – In Powell’s press conference at the March 20 Fed Meeting he said that a strong, or even strengthening, labor market would not, by itself, warrant a delay to rate cuts.

Aside from NFP, Eric Beinstein and team have updated their 24Q1 credit fundamentals note and the TL; DR version is that fundamentals are not only strong but are improving. A detailed summary of the credit note is provided below and two other tidbits that you may find interesting are (i) in the post-COVID era, we have seen ~20% of HY market cap upgraded to IG/HG; and (ii) this is the first Fed tightening cycle where net interest expense has decreased rather than increased.

BY Doug Kass · Apr 5, 2024, 6:15 AM EDT

For the first time since January 23, 2024, the S&P Short Range Oscillator moved into negative ground last night — dropping from 2.09% to -0.31%.

In part, this helps to explain this move late yesterday:

I have covered the balance of my SPY and QQQ common shorts at $513.27 and $435.56, respectively.

(These shorts were my Trades of the Week a few days ago).

I remain net short SPY and QQQ via short calls.

I also have June straddles on which I plan to expand tomorrow morning.

BY DOUG KASS APR 4, 2024 5:22 PM EDT

BY Doug Kass · Apr 5, 2024, 6:10 AM EDT

BY Doug Kass · Apr 5, 2024, 5:57 AM EDT

Wolf Street howls about the Fed's balance sheet.

BY Doug Kass · Apr 5, 2024, 5:50 AM EDT