Good News on Trulieve

Good news from Trulieve (TRLV) after the close.

Trulieve Announces Planned Termination of Executive Automatic Securities Disposition Plan

Position: Long TRLV (S)

BY Doug Kass · Jun 26, 2026, 5:04 PM EDT

Good news from Trulieve (TRLV) after the close.

Trulieve Announces Planned Termination of Executive Automatic Securities Disposition Plan

Position: Long TRLV (S)

BY Doug Kass · Jun 26, 2026, 5:04 PM EDT

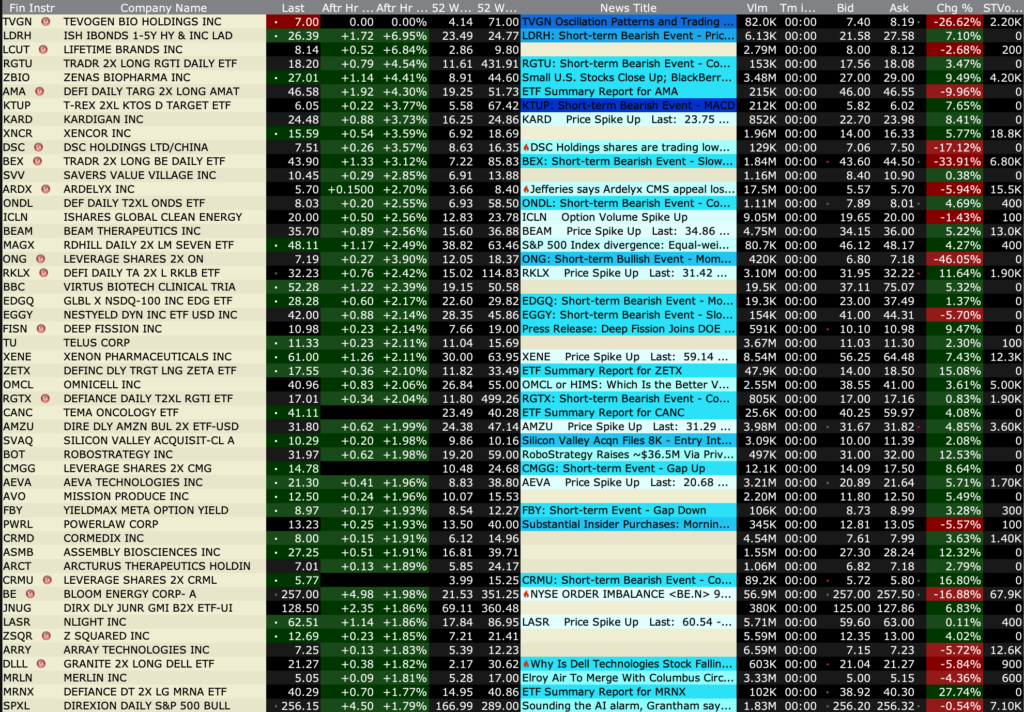

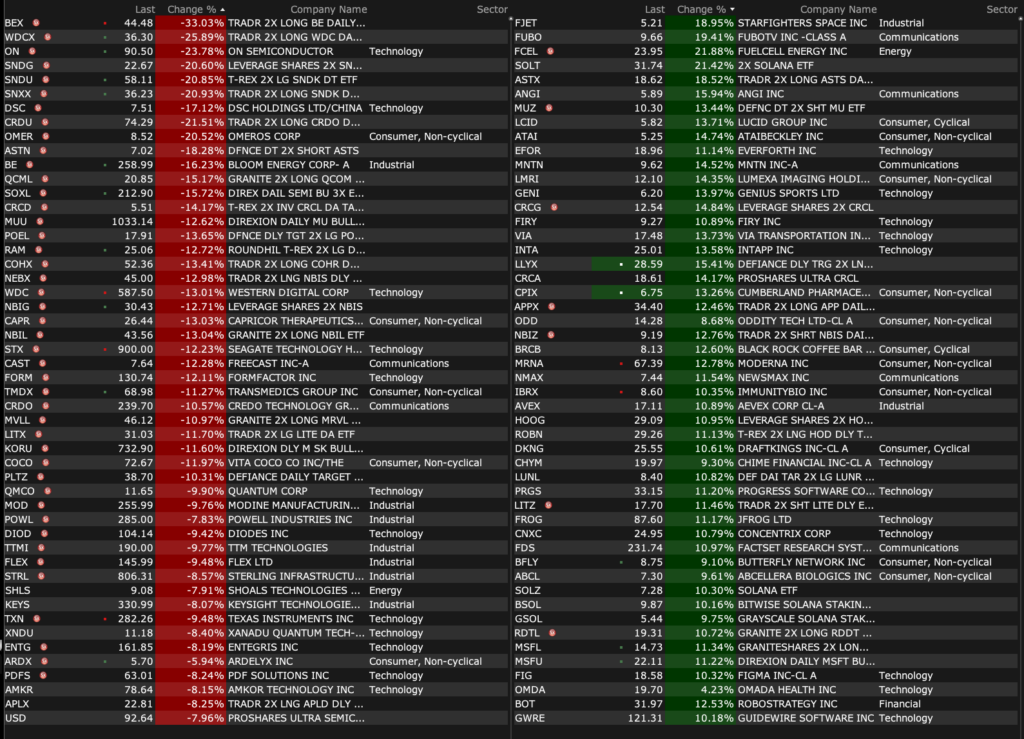

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · Jun 26, 2026, 4:45 PM EDT

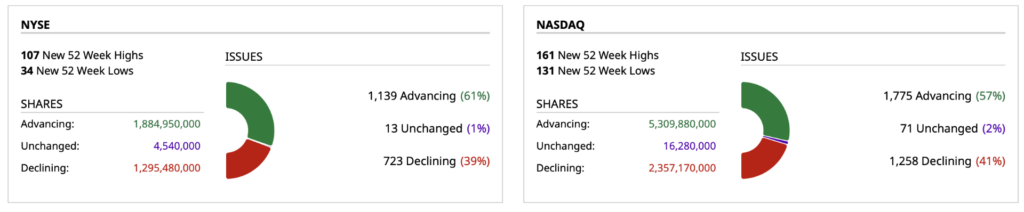

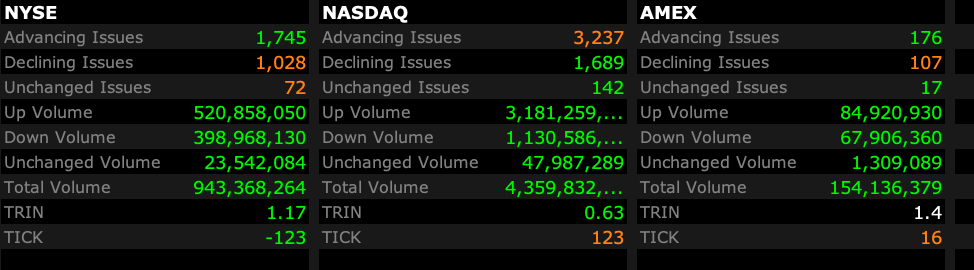

Closing Volume

– NYSE volume 11% below its one-month average

– NASDAQ volume flat to its one-month average

– VIX index: down 2.54% to 18.41

Breadth

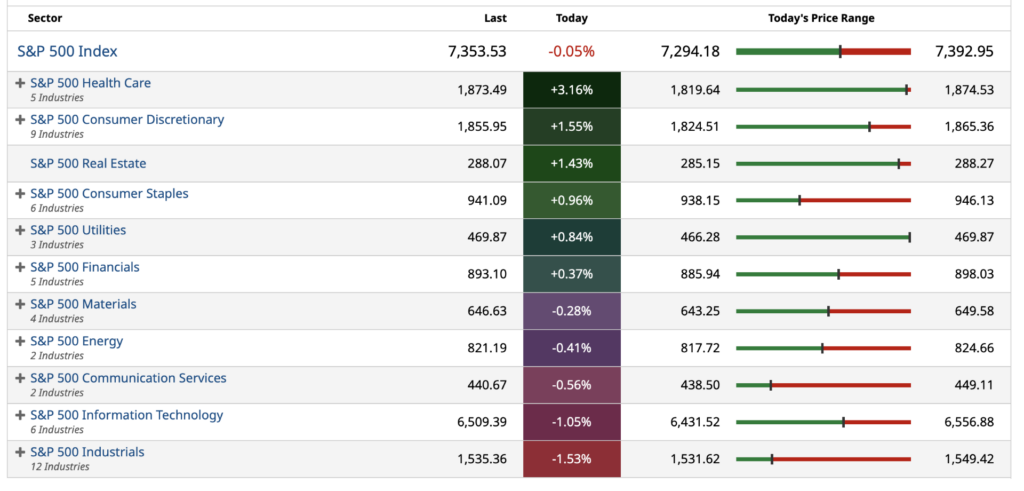

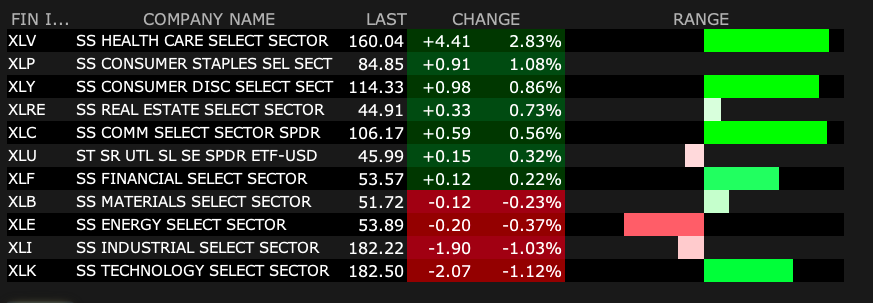

S&P 500 Sectors

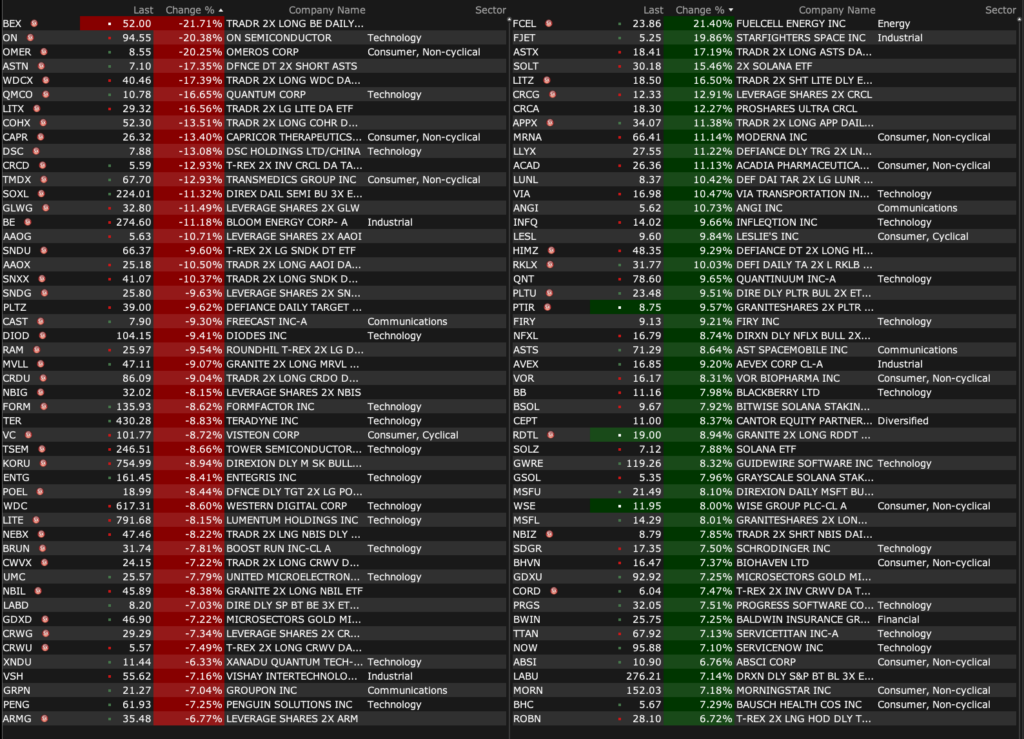

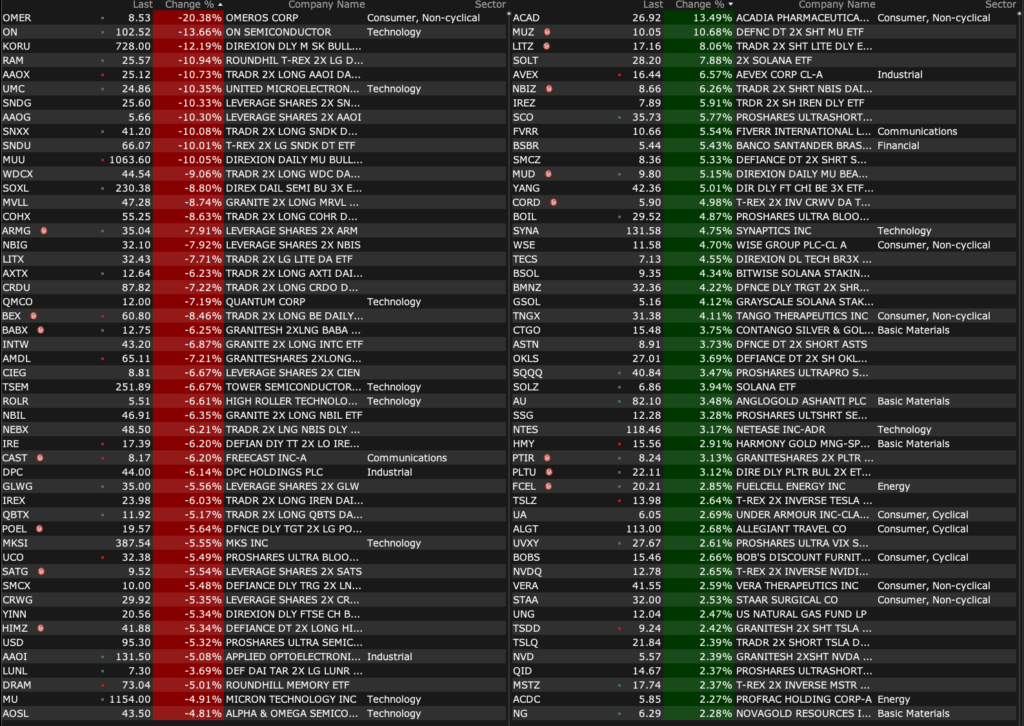

% Movers

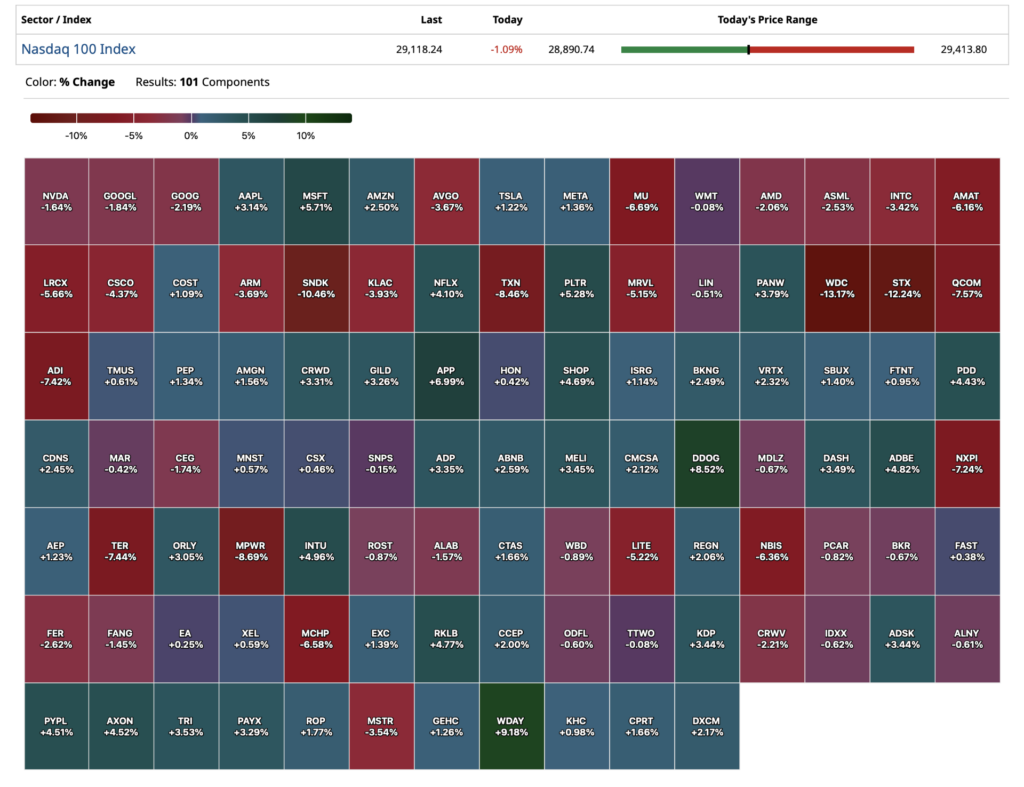

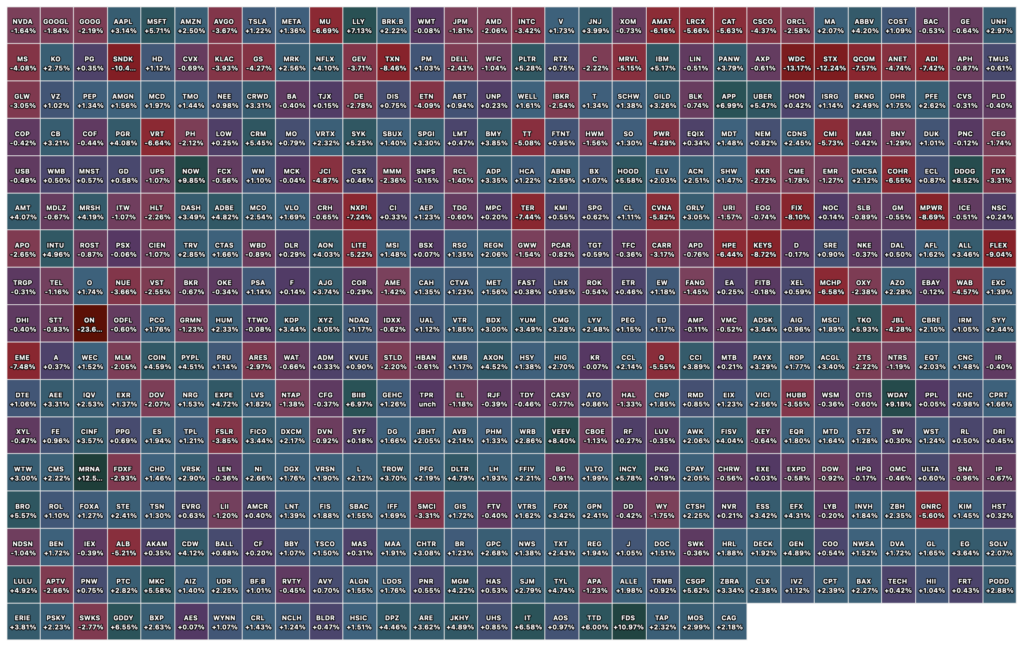

Nasdaq 100 Heat Map

Closing S&P 500 Heat Map

Position: None

BY Doug Kass · Jun 26, 2026, 4:30 PM EDT

Huge moves in memory, semis and some members of Mag 7 based on rebalancing.

Position: None

BY Doug Kass · Jun 26, 2026, 4:04 PM EDT

From Peter Boockvar:

Positives,

1) Initial jobless claims totaled 215k, 10k below expectations and down from 227k. Because of the holiday, we’ll combine this with next week’s print to smooth it out. Until then, the 4 week average of 224k is little changed with the previous week.

2) May personal income rose .7% m/o/m after no change in April and above the estimate while spending was higher by .7% m/o/m as expected when including the revision in the prior month. The savings rate at 3% combines this, unchanged with April but at the lowest level since June 2022.

3) Core durable goods orders in May rose 1.6% m/o/m, well above the estimate of up .6% and follows a .7% fall in April (revised down from 1%) . Shipments of core goods were as expected though.

4) The S&P Global manufacturing PMI rose again to 55.7 from 55.1. S&P Global said, “While there is better news from the manufacturing sector, we remain concerned as factory growth continues to be temporarily buoyed by inventory building amid supply fears. Supply delays grew more widespread in June.” With pricing, “Although manufacturing input cost inflation moderated from May’s recent peak, it was the second highest for almost four years.” Prices charged were little changed m/o/m but at one year highs.

5) Still bouncing along record lows but June UoM consumer confidence did lift to 49.5 from 44.8 in May and vs 49.8 in April “as gas prices moderated” they said. “Still, sentiment remains in unfavorable territory at 13% below the February 2026 reading prior to the start of the Iran conflict, and nearly 20% less than a year ago. The cost of living remains at the forefront of consumers’ minds; for the third straight month, over half of consumers spontaneously mentioned that high prices are weighing down their personal finances.”

6) The US crude oil rig count continued to rise as of 6/26 with an increase of 7 rigs to 440, the most in a year.

7) The June KC manufacturing index rose to 11 from 8. The estimate was 6.

8) From Micron: “DRAM and NAND industry demand continues to significantly exceed industry supply. We expect tight conditions to persist beyond calendar 2027, as a result of AI driven demand across all segments, coupled with structural supply…We are excited to announced that we have now signed 16 strategic customer agreements or SCAs, which we expect will fundamentally transform our business model. The memory industry has been structurally transformed by the proliferation of AI.”

9) From Darden Restaurants: On their consumer, “we really haven’t seen a whole lot of change, based on what we’ve been saying for the last couple of quarters. Consumer spending remains pretty resilient. Overall, the mood with consumers is still a little cautious. But as we’ve said a couple of times before, the weaker consumer sentiment hasn’t necessarily translated into reduced spending. A little bit different this quarter, our casual brands saw an increase in visits y/o/y from all income groups, including the bottom quartile. Some of that might have been tax refunds, but they did see some increase y/o/y from all income groups. We did see a little softness in guests under 35.”

10) From Commercial Metals: “As related to end markets, the outlook continues to be positive. More than 50% of the IIJA (Infrastructure Investment and Jobs Act) funding is yet to be spent, supporting highway construction and general infrastructure spending across our core markets remaining steady. While residential demand remains broadly subdued, pockets of resilience persist in markets such as Charlotte and parts of the Mid-Atlantic. Multi family construction continues to outperform and is expected to remain stronger than single family. For non-residential markets, demand is increasingly being driven by a growing pipeline of large scale megaprojects. Investments across data center, semiconductor capacity and energy networks are driving a multiyear pipeline of construction activity with a significant concentration of these projects in our Sunbelt and East Coast footprints.”

11) From FedEx: They saw 14% revenue growth, “supported by yield strength across all services, and volume growth aligned with our commercial strategy. This growth includes a 5 percentage point benefit from fuel price driven surcharge revenue.” To what I keep hearing about order pull forwards and have been highlighting here, “I do think that there’s a little bit of inventory buildup and restocking going on, but phenomenal, successful quarter.”

12) From FedEx Freight: “As expected, volume was softer y/o/y. However, trends have improved sequentially. We’re encouraged by these early signs that demand may be stabilizing for our services, supported by improving manufacturing indicators, truckload trends, and higher y/o/y contractual increases.”

13) The June German IFO business confidence index rose a touch to 85.6 from 85 and about as expected but only a bit off its recent lows. Most of the gain was in the Current Assessment component with Expectations up slightly. The IFO said simply, “Firms perceive business environment as less uncertain. German companies are hoping for geopolitical tensions to ease.” Manufacturing expectations improved but the current situation was a touch lower and “The number of new orders declined again.” With German services, “the business climate improved…The transport and logistics sector was able to continue its recovery. In tourism, by contrast, the situation remains difficult.” In trade, “the road to recovery is still long” and in construction, “Many companies complain about a lack of orders.”

14) Japan’s PMI rose for both with manufacturing at 54.9 vs 54.5 and services increasing to 51.8 from 50.0. S&P Global said, “it is important to note that the current period of growth is partly being driven by stock piling efforts amid the war in the Middle East, and these efforts are likely to fade in the months ahead as warehouses fill and cost pressures bite…Furthermore, the latest PMI survey signaled the sharpest rise in input costs for nearly four years in June. Subsequently, the rate of selling price inflation eased only slightly from May’s survey record as many firms looked to pass on higher expenses to clients.”

15) Australia saw a gain in both too with manufacturing at 51.2 vs 50.7 and services about at the flat line at 49.9 vs 48.7 in the month before.

16) India’s weakened a bit but still remains strong with manufacturing at 54.5 vs 55 and services at 57.3 vs 59.8.

17) The strength in the June Eurozone composite index m/o/m was in manufacturing with it at 51.3 vs 51.6 in the month before. The services component remained below 50 but rose to 48.9 from 47.7. The combined composite index is at 49.5, up 1 pt. Germany’s composite index came in at 48 with a 46.8 print in services while manufacturing was exactly at 50. France’s service index lifted to a still weak 47.4 from 44.3 while manufacturing rose 1 pt to 50.7. On the services side for the Eurozone, tourism and leisure related industries saw “signs of recovering demand after the initial disruptions from the war in the Middle East.” In manufacturing, it “continues to benefit from inventory building as customers front run future price rises or supply issues amid ongoing supply fears linked to the war.” With pricing, “Encouragingly, lower energy prices are already filtering through to businesses and rates of input cost and selling price inflation have moved lower in June as a result, hinting at a potential peaking of the recent price spike.”

Negatives,

1) In May, the headline PCE rose .4% m/o/m and 4.1% y/o/y while the core rate was higher by .3% m/o/m and 3.4% y/o/y. Both about as expected due to rounding and up from 3.8% and 3.3% y/o/y gains seen in April.

2) Continuing claims, delayed by a week, totaled 1.821mm, up 21k w/o/w. That’s the highest since March but still well off its recent highs.

3) The June Philly services index remained deeply negative at -25.8 vs -23.6.

4) Strange to see the notable price rises in electronic products from Apple and Microsoft after getting used to persistent price declines, which marks the history of technology.

5) Hopefully we’ll get some relief soon with the Strait reopening but at least thru 6/25, container shipping prices continue to jump. The Shanghai to NY trip rose another 5.6% w/o/w, up for an 8th straight week to $7,149 for a 40 foot container. That’s the highest since last June. The price for the route to LA rose by a similar amount and less so to Rotterdam.

6) New home sales in May totaled 580k, 60k below expectations and down from 626k in April. That’s just 4k from the least since 2022. About all of the weakness was in the West region. Months’ supply rose to 10.3 from 9.3.

7) With little change in the average 30 yr mortgage rate at 6.59%, purchase applications fell .6% w/o/w but up 2.8% y/o/y. Refi’s rose 3% w/o/w after a 4.5% drop in the week before and higher by 17% y/o/y.

8) The June Richmond manufacturing index fell to 4 from 13.

9) The US May goods trade deficit was much wider than expected at $105.8b, $20b more than expected with an unexpected 5.4% decline in exports. Expect Q2 GDP estimates to get cut after this.

10) From Kroger: “The customer is under pressure. Higher gas prices and reduced SNAP benefits are squeezing budgets. Customers are managing spend carefully and shopping with real intent. That pressure is showing up in the market. Food-at-home growth decelerated 100 bps compared to the last quarter. Encouraging news is that our work on affordability is starting to resonate and you can see it in the data…Traffic is up. Customers are coming through our doors more often, which tells me our value messaging is starting to land…Food inflation came in at the low end of our expectations, down sequentially from the fourth quarter. Egg deflation was a meaningful headwind to identical sales without fuel, representing 64 bps of pressure…Looking ahead, we expect inflationary pressure to increase as the year progresses, reflecting the broader macro environment.”

11) From KB Homes: “Although buyers continue to demonstrate the desire for homeownership and the ability to qualify, consumer confidence remains low, driven by a variety of factors, from elevated mortgage interest rates and affordability pressures to rising inflation and geopolitical uncertainties. We continue to attract a healthy level of traffic to our communities, signaling both consumers’ interest in purchasing a home and the appeal of our locations and products, and our cancellation rate was stable, reflecting high quality, committed buyers who can close. However, market conditions precipitated a less than optimal conversion of traffic to sales as many consumers lacked the confidence to purchase, resulting in a community absorption rate of four net orders per month.”

12) From Carnival: “while we are incredibly resilient to major external shocks, we are not immune, and near term disruption can affect the timing of results, especially when it persists for an extended period of time. Accordingly, our second quarter operational outperformance and accelerated cost efforts are offsetting the moderation we’ve incorporated into our back half outlook given the impact of the prolonged conflict. Specifically, this moderation was concentrated on our European deployments, particularly in the Med region, which were closest to the conflict. And it was further exacerbated by elevated airfares and reduced international flight capacity for North American guests. So yes, this did put a bit of a dent in our trajectory.”

13) From Accenture: With regards to corporate IT budgets, “Even with AI, they’re spending it differently, but they haven’t been increasing.” Also of note from their call, “we were impacted by the conflict in the Middle East. We saw a revenue impact of approximately $100 million compared to our expectations, which was all consulting type of work, split evenly between the direct impact on our Middle East business and indirect effects outside of the region. In the last few weeks of the quarter, we saw this indirect impact globally in products and to a lesser degree in resources, mostly in discretionary spend.” As an example of the ‘indirect impact’, “some of the industries are dealing with kind of longer-term issues, so think about automotive, where we have a large presence. They were already challenged. And now with the higher gas prices, that’s added to it.”

14) The June Tokyo CPI rose 1.7% headline y/o/y and 1.9% ex food and energy, both one tenth above expectations and helped by consumer energy subsidies.

15) The trimmed mean CPI in May in Australia was higher by 3.6% y/o/y vs 3.4% in April and one tenth above the estimate.

16) The UK June PMI was little changed at 49.4 vs 49.7 in May. Manufacturing was 53.1 vs 53.9 while services came in at 48.7 vs 49.3. “Price pressures remain elevated as companies point to the energy shock and supply squeeze from the war in the Middle East as exacerbating existing cost pressures from government policies” but they also said “Some of the war related price pressures have started to moderate, however, largely thanks to lower energy prices.” S&P Global also mentioned the same factor lifting manufacturing, “as demand here is being temporarily buoyed by the building of safety stocks amid ongoing war related supply worries.”

17) Maybe that pull forward has run its course as the June UK CBI industrial orders index softened to -45 from -41 and CBI said “Manufacturers are facing an increasingly difficult trading environment, with order books now at their weakest since 2020 and output continuing to fall. While selling price expectations have eased from their peak in May, they remain elevated, highlighting the cost pressures still facing the sector.”

18) Agree with how he ran monetary policy or not, we lost an economic and finance legend in Alan Greenspan.

Position: None

BY Doug Kass · Jun 26, 2026, 3:48 PM EDT

Position: None

BY Doug Kass · Jun 26, 2026, 3:23 PM EDT

Riddle me this, Bitcoiners:

To give you a sense of how bad an asset allocator Strategy’s (MSTR) Michael Saylor is… he started buying Bitcoin at $11,000.

The current price is $60,000 but he has an unrealized loss of over $15 billion.

Position: None

BY Doug Kass · Jun 26, 2026, 2:10 PM EDT

Professor Galloway’s No Mercy No Malice:

World Cup Experience – by Scott Galloway – Prof G Media

Position: None

BY Doug Kass · Jun 26, 2026, 1:25 PM EDT

My Trade of the Week, Trulieve (TRLV), is +6% today to $9.05.

From earlier this week:

Trulieve’s (TRLV) shares have been under pressure because of the malaise in the cannabis space and the proposed sale of 2.5 million shares by the company’s founder, Kim Rivers.

As expressed in my cannabis update yesterday, I believe an extraordinary reward vs. risk exists today.

As to Trulieve, based on Rivers’ SEC reporting I believe she is close to completing her sales (which were previously planned for in a filing).

After she completes those sales I expect the company to implement their authorized company buyback.

I would further note that a large portion of the cannibas company’s operations are medical-use based, which has already been rescheduled.

Position: Long TRLV (S)

BY Doug Kass · Jun 24, 2026, 10:10 AM EDT

Position: TRLV (S)

BY Doug Kass · Jun 26, 2026, 1:07 PM EDT

Position: None

BY Doug Kass · Jun 26, 2026, 12:50 PM EDT

BY Doug Kass · Jun 26, 2026, 12:37 PM EDT

‘Forget it, Jake. It’s Chinatown’

– Chinatown Forget it Jake, it’s Chinatown.

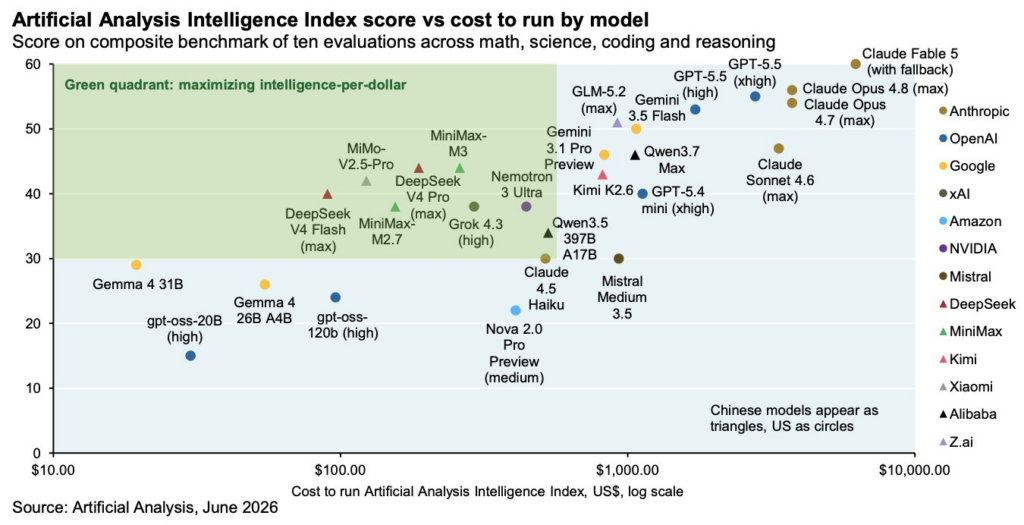

As more biz moves to China, the core problem is they all have no business model. To grow, they have to give it away. That requires infinite financing, which does not exist, even for money-making businesses. Nobody should really finance anything with these economics, which are price-to-profit, too expensive for anyone to use it (it becomes more expensive than human labor), price-to-grow, it loses $1 for every $1 of revenue. This is a pure commodity industry. Business is moving to lower-cost Chinese models for a reason. Some 98%-99% as good at 2% of the price. The low-cost player in a commodity industry wins. This industry is the definition of commodity. Highly undifferentiated, all about capital. Even Microsoft (MSFT) is thinking of using the Chinese (Deepseek) now for Copilot. MSFT sees the writing on the wall. See tweet and subtweet. The first part about Anthropic begging the government for money comes from a credible source:

This was forwarded to me by Jim Chanos:

If you haven’t seen it yet, this graphic from Artificial Analysis (via JP Morgan) has gone viral overnight. It highlights the cost-benefits of the cheaper (primarily) Chinese open-source models for inference tasks. OpenAI may already be feeling this pressure. And if normal tech-deflation hits token prices…will hardware/AI infrastructure be next?

Position: MSFT VS

BY Doug Kass · Jun 26, 2026, 11:55 AM EDT

– NYSE volume 22% below its one-month average;

– Nasdaq volume 13% above its one-month average;

– VIX index: up 2.12% to 19.29

Positions: None.

BY Doug Kass · Jun 26, 2026, 11:30 AM EDT

I sold some MSFT (MSFT) (+$16) $368.85

Position: Long MSFT VS

BY Doug Kass · Jun 26, 2026, 11:10 AM EDT

Positions: None.

BY Doug Kass · Jun 26, 2026, 11:00 AM EDT

I have a research call between 11 a.m. and noon.

Positions: None.

BY Doug Kass · Jun 26, 2026, 10:51 AM EDT

Positions: None.

BY Doug Kass · Jun 26, 2026, 10:08 AM EDT

Positions: None.

BY Doug Kass · Jun 26, 2026, 9:39 AM EDT

From Peter Boockvar:

I will be taking next week off for the first time since December and writing sporadically, if at all. Most likely the latter. Happy 250.

I expressed yesterday that I felt it was much more informative to value a highly cyclical business relative to sales rather than earnings to get a fuller picture of the multiple. After hearing again yesterday that Micron was cheap, trading at only 7x earnings, I want to highlight that Toll Brothers was trading at 6x earnings in 2006. I heard then it was cheap. After falling by 75% by late 2008, its stock was trading at 30x earnings. For a highly cyclical business, it was thus better to sell perceived ‘cheap’ and buy ‘expensive.’ To also say again, this is no advice or opinion on where Micron and other memory/storage stocks go as maybe the strategic customer agreements being signed smooth out the business volatility and a higher multiple is deserved but just trying to recommend a broader way to value stocks such as this.

While some investors now are seemingly waking up to the fact that hyperscaler free cash flows are disappearing, I want to point that this started in Q4 2025 when Oracle was punished when investors realized how exposed they are to OpenAI, along with raising its CapEx plans to 75% of revenue (now at 100%) from 10% in 2022, something I’ve been pointing out for many quarters now. Meta has crushed it revenue wise over the past three quarters because of its robust base business but investors have punished the stock after each reporting period because the CapEx figures keep going up. Dot, dot, dot, you get the point again. We are in the midst of a major transition from what was market leadership over the past 15 years to eventually something else. These mega cap tech stocks, incredible companies that have had historic market performance are going to go from growth stocks to value I believe, and that evolves over time but marked by years of underperformance relative to other things.

With respect to the Apple product price increases reported yesterday, I just wanted to put percentage changes behind the absolute price changes. The MacBook Neo, its new laptop, is seeing a price increase of 17%. The MacBook Air is rising in price by 18%. The 14 inch MacBook Pro will cost 18% more while the 11 inch iPad Pro is going up by 20% and the iPad Air will be higher in price by 25%. The history of technology on pricing is deflation, always has been and always will be and what makes this price increases eye popping, but we are just in one of those cyclical periods where it’s not for reasons we’re all well aware of.

I wanted to do a quick stock market sentiment check because the Investors Intelligence survey is getting very close to be extreme as I define a 40 point spread between Bulls and Bears. Bulls rose to 55.8 from 51.9 (as of last Friday) while Bears dropped to just 17.3 from 21.2. Those are levels last seen back in February. In the AAII retail investor survey, Bulls rose by 8.3 pts to 44.9, the most since late April while Bears fell to 36.1, the least since mid May. The Citi Panic/Euphoria index remains well in Euphoria at .82, double the threshold of .41. The only metric that is the reverse of the above is the CNN Fear/Greed index which was 25 yesterday, ‘Extreme Fear.’

Darden reported yesterday and because of its wide breadth of restaurant chains in terms of customers served, it’s always a helpful call to go through. They say, “Full service dining is a variety seeking category, and we have a collection of brands that give us reach across multiple dining occasions, guest demographics, price points, geographies, and cuisine types.” The stock was little changed and they said this:

“Several of our brands enjoyed record performance on Mother’s Day, including the highest ever traffic day at Olive Garden and LongHorn Steakhouse.”

Olive Garden saw 4% comp gain, “which is above the high end of Darden’s long-term framework. LongHorn delivered same restaurant sales growth of over 7% for the year (and 9.5% for the quarter helped by higher beef prices but still providing value at this chain), reflecting their focus on food quality and execution.” This chain contributes almost half of Darden’s operating profit and 42% of sales.

Yard House had a comp gain of 5.6%.

Their fine dining division which includes Capital Grille, Ruth’s Chris Steak, Seasons 52 and Eddie V’s saw a slower comp gain of 1.9%.

They believe the key to their success has been pricing their menu below inflation “over time to preserve our value proposition and support traffic.”

They said with respect to food and beverage expenses that were flat, “commodity inflation of approximately 3% and unfavorable mix was fully offset by pricing.” They saw total labor inflation of 3.2%.

On their consumer, “we really haven’t seen a whole lot of change, based on what we’ve been saying for the last couple of quarters. Consumer spending remains pretty resilient. Overall, the mood with consumers is still a little cautious. But as we’ve said a couple of times before, the weaker consumer sentiment hasn’t necessarily translated into reduced spending.”

“A little bit different this quarter, our casual brands saw an increase in visits y/o/y from all income groups, including the bottom quartile. Some of that might have been tax refunds, but they did see some increase y/o/y from all income groups. We did see a little softness in guests under 35.” This helps to explain why other chains that cater to younger consumers are seeing slower comp growth.

Commercial Metals in its earnings call gave a good lay of their land:

“As related to end markets, the outlook continues to be positive. More than 50% of the IIJA (Infrastructure Investment and Jobs Act) funding is yet to be spent, supporting highway construction and general infrastructure spending across our core markets remaining steady. While residential demand remains broadly subdued, pockets of resilience persist in markets such as Charlotte and parts of the Mid-Atlantic. Multi family construction continues to outperform and is expected to remain stronger than single family.”

“For non-residential markets, demand is increasingly being driven by a growing pipeline of large scale megaprojects. Investments across data center, semiconductor capacity and energy networks are driving a multiyear pipeline of construction activity with a significant concentration of these projects in our Sunbelt and East Coast footprints.”

In the KC manufacturing survey seen yesterday for June they asked a special question to manufacturers “about their ability to pass through prices and supply chain change expectations.” This were the results:

1)38% of firms reported that they are currently able to pass through 0-20% of the higher costs from inputs and labor.

2)10% of firms are able to pass through 20-40%.

3)10% are able to pass through 40-60%.

4)11% can pass through 60-80%.

5)19% can pass through 80-100%.

6)4% can pass through more than 100%.

7)8% of firms had to decrease prices.

The 12 month outlook for price changes is not much different and this spells to me like a margin squeeze with only 23% being able to pass on most of their cost pressures. This also gets to my point that just looking at consumer prices does not give the whole inflation picture and we must too watch PPI. I hope Kevin Warsh and Co believe the same because running monetary policy on just one side and not both would be treating a patient with only signals from half the body.

The June Tokyo CPI rose 1.7% headline y/o/y and 1.9% ex food and energy, both one tenth above expectations and helped by consumer energy subsidies. The 2 yr yield was unchanged in response but the BoJ has more reason to hike rates from its current 1.00% level. The yen is slightly higher as the US dollar is broadly weaker today.

BY Doug Kass · Jun 26, 2026, 9:30 AM EDT

-ILLR +55% (enters Definitive Agreement to acquire $411M of financial exposure to SpaceX)

-QUCY +30% (approves acquisition of equity stake in SpaceX)

-SHPH +24% (United Dogecoin purchases Dogecoin miners and secures renewable energy data centre site)

-TII +22% (signs lease with US Army for graphite processing)

-ACAD +16% (CHMP recommends marketing authorization for DAYBU (trofinetide) in Rett syndrome neurobehavioral symptoms)

-CNVS +12% (earnings, guidance)

-APOG +9.1% (earnings, guidance)

-SYNA +4.9% (ON Semi acquires Synaptics in all-stock deal at ~$7B enterprise value)

-XNET +3.4% (authorizes $20M share repurchase program)

-DKNG +2.5% (launches proprietary prediction markets exchange DKeX)

-ON -14% (acquires Synaptics in all-stock deal at ~$7B enterprise value)

-QMCO -9.1% (earnings, guidance)

-SNDK -5.8% (profit-taking)

-TOYO -3.8% (closes $50M registered direct offering of 4.5M shares and warrants at $11.00/shr)

Positions: None.

BY Doug Kass · Jun 26, 2026, 8:50 AM EDT

Positions: None.

BY Doug Kass · Jun 26, 2026, 8:42 AM EDT

Chart from 7:49 a.m. ET.

Positions: None.

BY Doug Kass · Jun 26, 2026, 8:32 AM EDT

11:30 a.m.: Fed Bank of Minneapolis Kashkari (Voter) takes part in panel discussion at the 2026 Bankof Korea International Conference;

Sunday June 28: 12:35 p.m.: Fed Bank of Richmond President Thomas (Non-Voter) participates in”The Future of Economic Mobility: Built by Hand, Empowered by Opportunity” panel before the Aspen Ideas Festival hostedby the Aspen Institute, Aspen, CO (No text. No livestream)

Positions: None

BY Doug Kass · Jun 26, 2026, 8:23 AM EDT

* Sail on Silver Girl

When you’re weary, feeling small,

When tears are in your eyes, I will dry them all;

I’m on your side. When times get rough

And friends just can’t be found,

Like a bridge over troubled water

I will lay me down.

Like a bridge over troubled water

I will lay me down.

Simon and Garfunkel, Bridge Over Troubled Water

Position: None

BY Doug Kass · Jun 26, 2026, 7:30 AM EDT

The problem with shorting (or buying indices) late in the day or in the evening — as I often do — is that the fate of the general market’s opening is determined by the overall movement memory stocks.

And to predict/guess the opening price of MU, SNDK, AMAT, AMD, INTC is a “fool’s errand.”

The market has no memory from day to day.

Position: None

BY Doug Kass · Jun 26, 2026, 7:15 AM EDT

You can makes this up:

Position: None

BY Doug Kass · Jun 26, 2026, 7:00 AM EDT

BY Doug Kass · Jun 26, 2026, 6:45 AM EDT

As I wrote yesterday, it is astonishing that the markets have, until recently, ignored the clear transformation from capital light to capital intensive occurring in most Mag 7 constituents.

Hyperscalers (“check writers”) vs. Chips (“check receivers”):

Remember the debates with some subscribers in the Comments Section in which my concerns were dismissed by glibly repeating AI responses to AI skepticism and/or by the notion and defaulting argument that the stocks are buys and holds (and investors should be unconcerned with shifting (fundamental) sands and weakening absolute and relative stock performance?

In contrast I have provided opinions of skeptics (Marcus et al) combined, especially in my first 100-150 “More Tales” with my own primary analysis (though recognizing that I am not a technology specialist). I did so because I thought there was value to a skeptical view — at a time in which such gross overweight of Mag 7 was an accepted condition in business media discussions and in portfolios writ large.

It was lonely living outside the herd and opposing “Group Stink” but look at the share price falls since:

META $780 to $545

AMZN $275 to $225

MSFT $550 to $335

GOOGL $410 to $330

I have been writing about elevated multiples (discounting only bullish outcomes), the evisceration of free cash flow at Amazon (AMZN), Microsoft (MSFT), Google (GOOGL), et al and the mismatch between immediate revenue recognition (at Nvidia (NVDA)) and the deferral of costs (unrealistic and lengthy depreciation schedules) incurred by the hyperscalers, but it wasn’t until a few months ago that the markets began to catch on to the jig.

And, since then its been a developing period of absolute and relative performance for Mag 7. Now that the narrative has changed and many have accepted and are concerned about the multiple head winds I related in “More Tales” and in other columns — the stocks may have finally discounted these concerns. I purchased Google, Microsoft and Amazon over the last two trading sessions.

Here’s more:

Position: Long AMZN (S), GOOGL (S), MSFT (S)

BY Doug Kass · Jun 26, 2026, 6:30 AM EDT

Position: None

BY Doug Kass · Jun 26, 2026, 6:00 AM EDT

The S&P Short Range Oscillator moved into a greater overbought at 2.65% vs. 1.85%.

Position: None

BY Doug Kass · Jun 26, 2026, 5:45 AM EDT

This is what’s causing Anthropic to aggressively beg for govt protection (see below). Customers are finding cheaper alternatives. Keeping employees requires continuing ultra-rich secondaries ($$$) that are dependent on revenue growth. When you can’t win on the field go to DC.

UBS says 60% of companies now watching AI budgets are moving to cheaper models and open-source Chinese models The pressure is coming from extreme bills, including users spending up to $35K/month, teams exceeding quotas by 200%, and companies cutting internal AI tools from 5 to

This is what’s causing Anthropic to aggressively beg for govt protection (see below). Customers are finding cheaper alternatives. Keeping employees requires continuing ultra-rich secondaries ($$$) that are dependent on revenue growth. When you can’t win on the field go to DC.

UBS says 60% of companies now watching AI budgets are moving to cheaper models and open-source Chinese models The pressure is coming from extreme bills, including users spending up to $35K/month, teams exceeding quotas by 200%, and companies cutting internal AI tools from 5 to

We keep hearing "genius, this" and "genius" that about these ai people; it doesn't take a genius to see that wrecked balance sheets aren't signs of success if there is NO payoff in sight. Either merge--this government will bless it--or slow it or stop it. That' what this week's Show more

JUST IN: Michael Saylor's 'Strategy' currently has a $14,000,000,000 unrealized loss on its Bitcoin investment. Tom Lee's 'Bitmine' currently has a $10,500,000,000 unrealized loss on its $ETH investment.

Michael Saylor is one of the biggest fraudsters in the financial markets. He will eventually face criminal charges, file for bankruptcy, and spend the rest of his life behind bars. He is this era’s version of Bernie Madoff. His playbook, which I exposed over 12 months ago, is Show more

DEA Will Highlight Testimony On Marijuana's Medical Benefits In Rescheduling Hearing, New Filing Shows: A doctor called by the government will testify that cannabis "provides a medical benefit to pain patients." marijuanamoment.net/dea-will-highl…

“If there is a deflation of the AI bubble, the optimists say that the new infrastructure will remain even if the companies do not — just as railways survived the 19th-century railway bust. However, this fails to reckon with the reality of depreciation (few pieces of silicon hold Show more

Same vibes

Volatility tests every capital structure. Strategy remains focused on Bitcoin, disciplined capital allocation, credit quality, and long-term value creation. We appreciate our investors and will continue to execute with transparency and resolve. $MSTR

The @CNBC Panelist Said What? (Issue #3) Our third issue of this series deals with not only an epic investing boner but also the tendency of Fin TV panelists to rationalize share price declines ("I am averaging down"... considerably) - in a heads I win, tails I win mentality Show more

The @CNBC Panelist Said What? (Issue #2) Our second issue of this series involves a glib and overly confident @cnbc panelist who has consistently been wrong footed in his recommendations, particularly of his favorite and most repeated and most heavily weighted longs (he gave us

The prime question I have for all of the business media's venues and platforms... Why did you all wait to discuss the potential impact of the huge AI spending extravaganza on free cash flow for the hyperscalers? Why did you all wait to discuss the margin ramfications of ever Show more