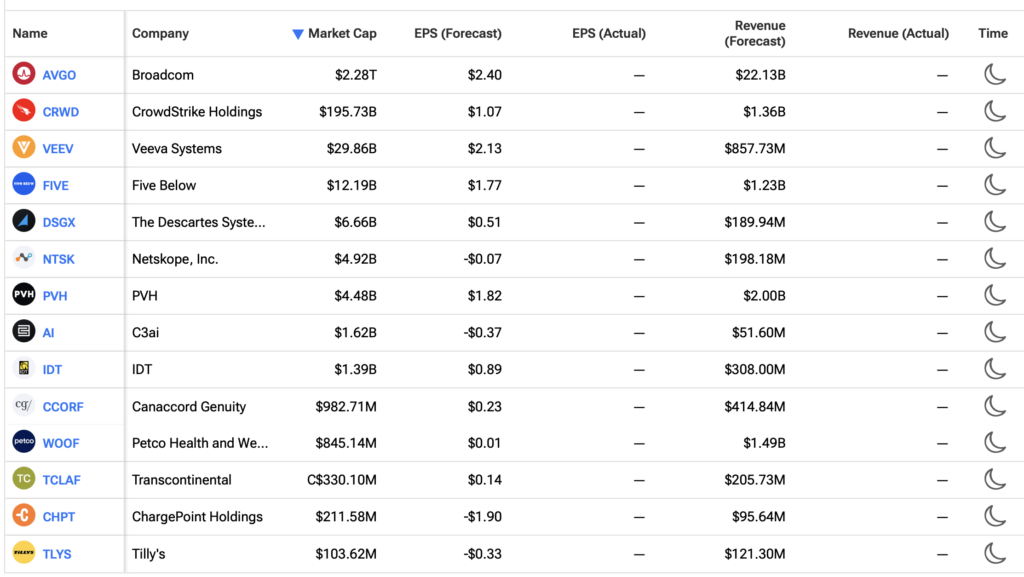

Must Watch Tweet of the Day

Position: None

BY Doug Kass · Jun 3, 2026, 6:00 PM EDT

Position: None

BY Doug Kass · Jun 3, 2026, 6:00 PM EDT

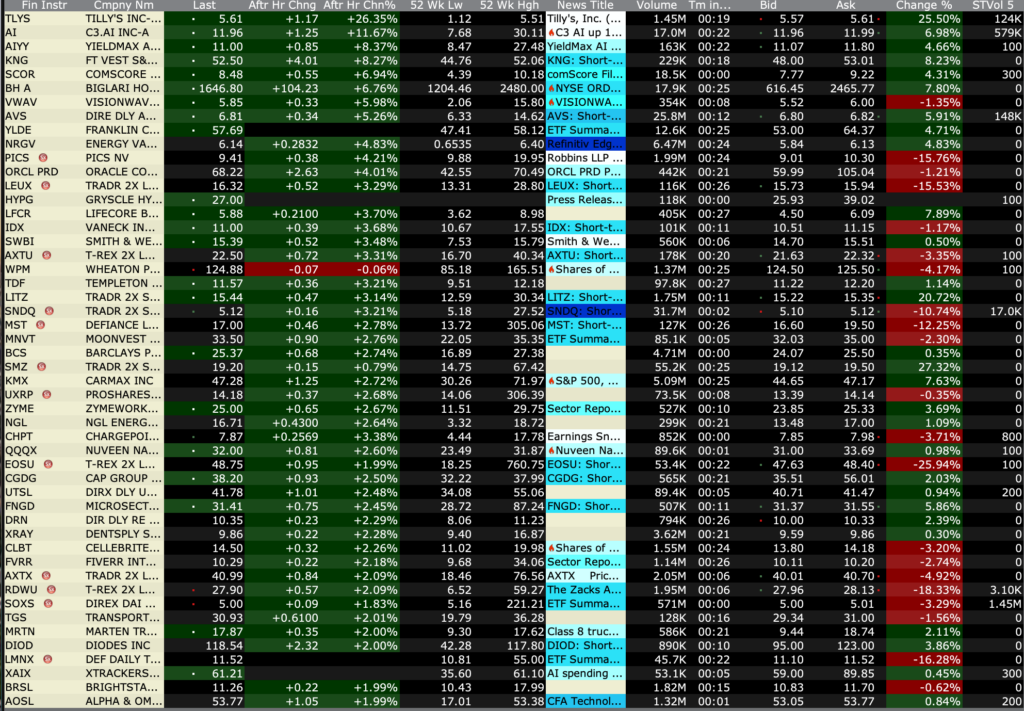

With S&P futures -73 handles (following large declines in reporting companies CrowdStrike (CRWD) and Broadcom (AVGO) I am covering some of my shorts from yesterday and this morning:

* SPY $752.18

* QQQ $741.69

From last night and during Tuesday’s regular trading session:

At 4:55 PM Tuesday I added to index shorts:

Position: Short SPY (L), QQQ (L)

BY Doug Kass · Jun 3, 2026, 5:45 AM EDT

I moved from large-sized to medium-sized.

Position: Short SPY (M), QQQ (M)

BY Doug Kass · Jun 3, 2026, 4:50 PM EDT

Investment short, Sleep Number (SNBR), prepares for a bankruptcy filing.

A perpetual short that never has to be covered!

Position: Short SNBR (VS)

BY Doug Kass · Jun 3, 2026, 4:47 PM EDT

At 4:26 PM:

After-Hours % Advancers

After-Hours % Decliners

Position: None

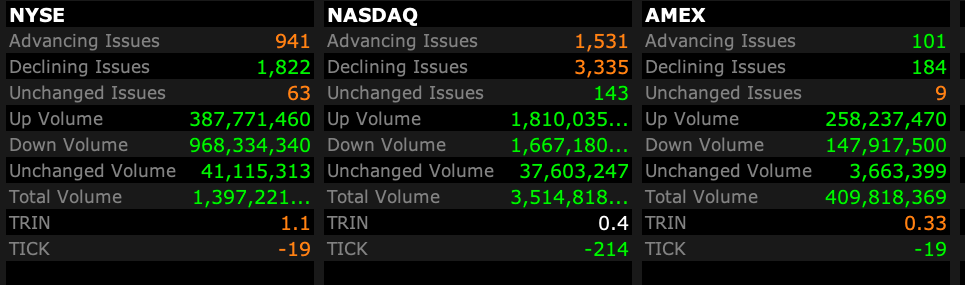

BY Doug Kass · Jun 3, 2026, 4:40 PM EDT

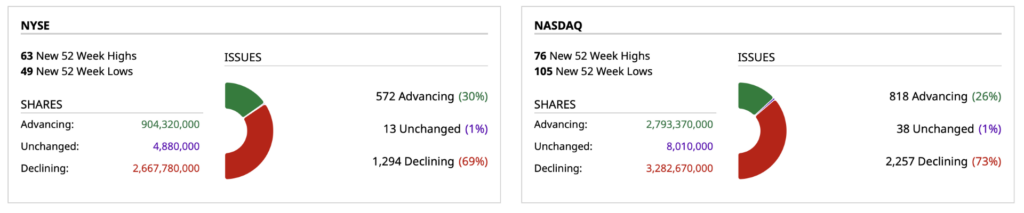

Closing Volume

– NYSE volume 3% below its one-month average

– NASDAQ volume 5% below its one-month average;

– VIX index: up 1.84% to 16.06

Breadth

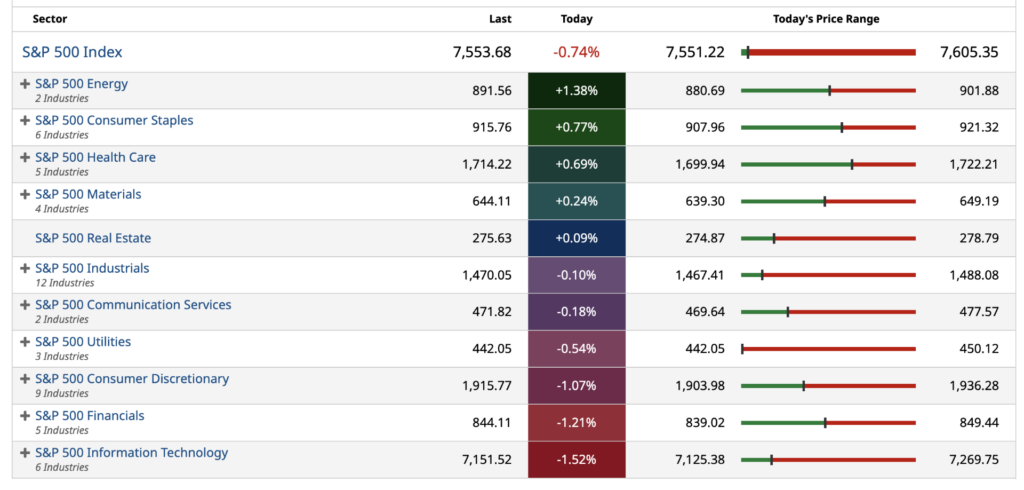

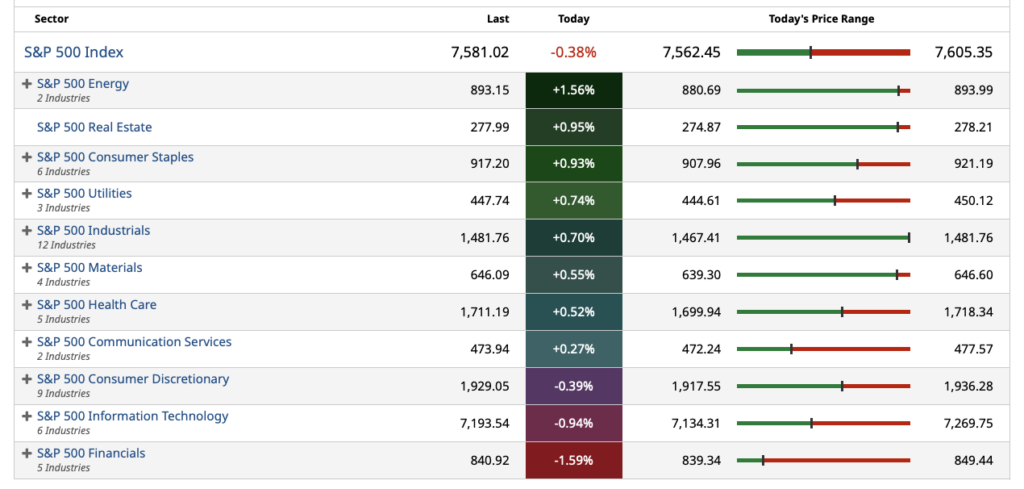

S&P 500 Sectors

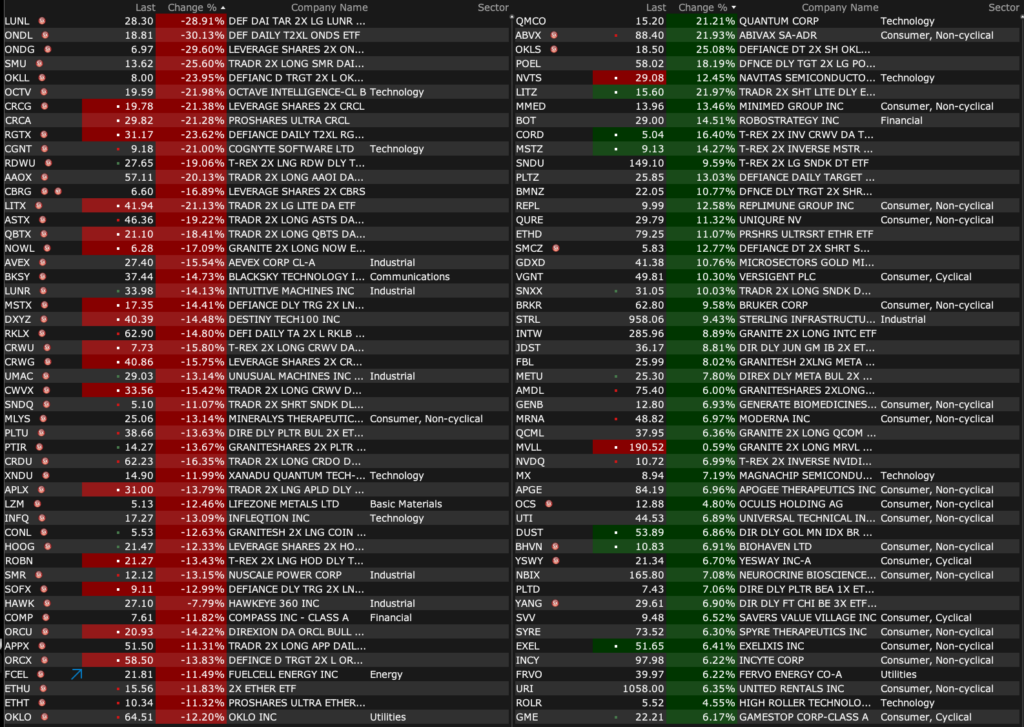

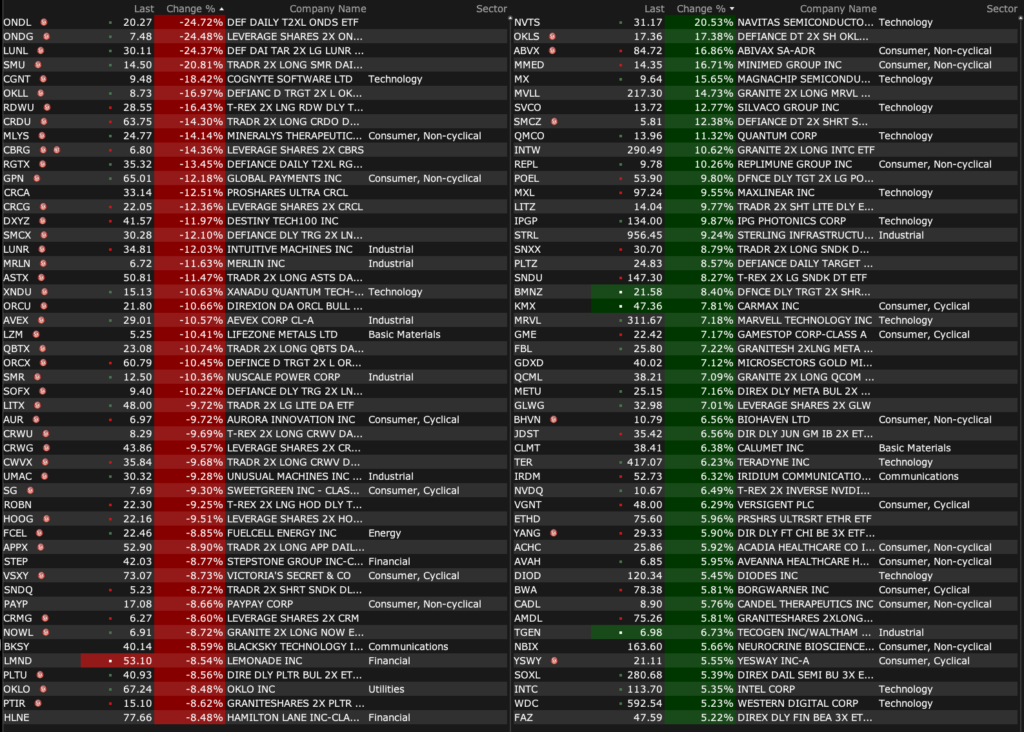

% Movers

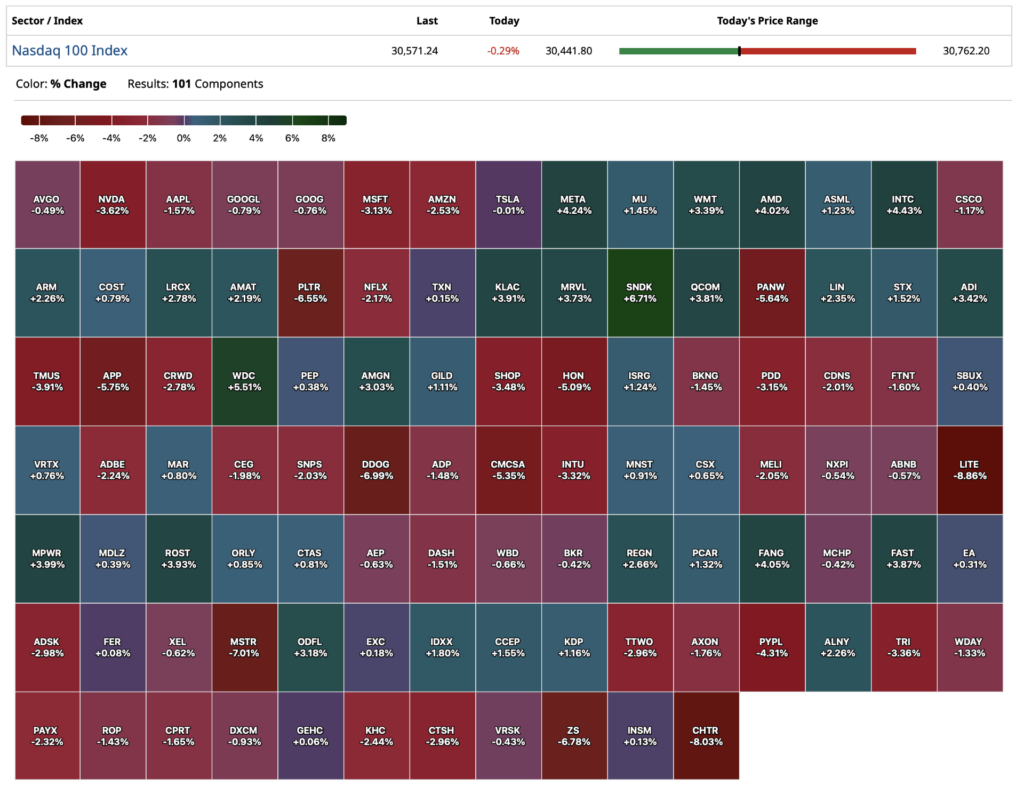

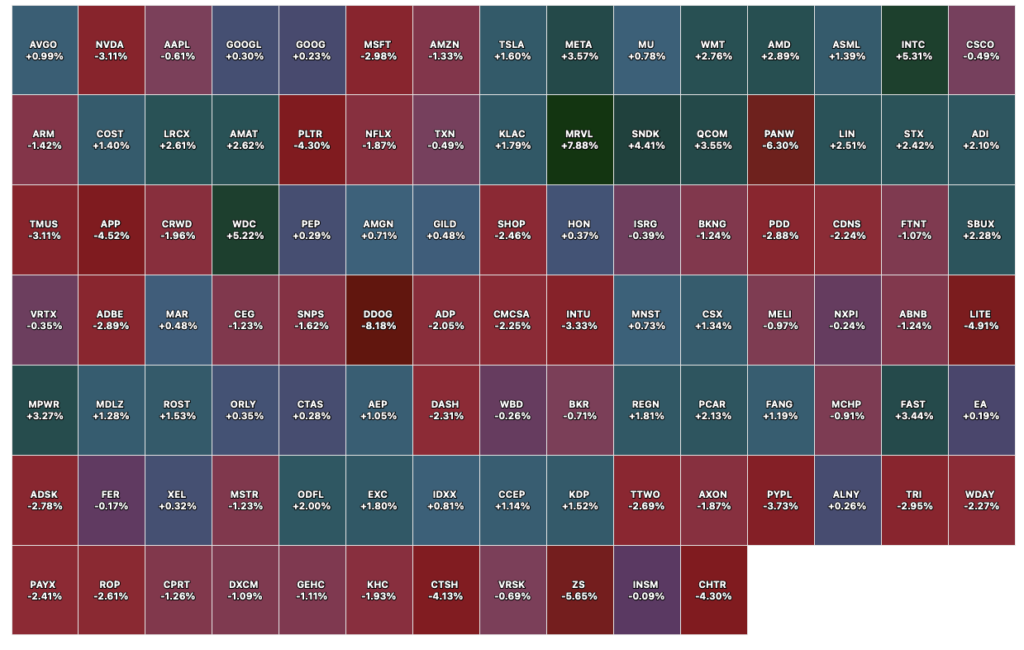

Nasdaq 100 Heat Map

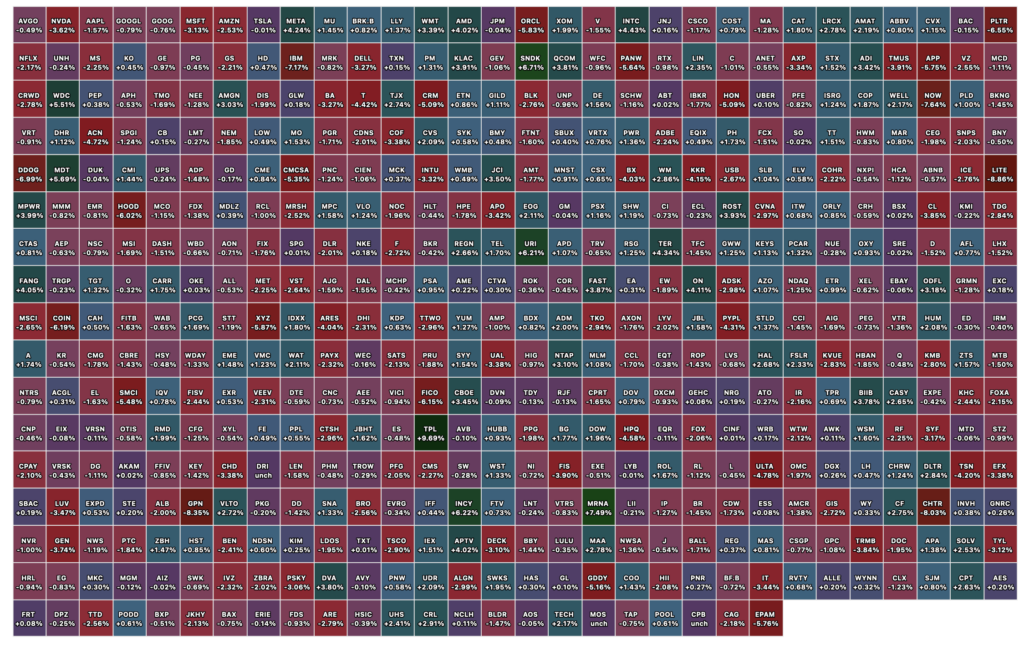

Closing S&P 500 Heat Map

Position: None

BY Doug Kass · Jun 3, 2026, 4:30 PM EDT

BY Doug Kass · Jun 3, 2026, 3:55 PM EDT

I don’t think today’s decline in cannabis stocks makes much sense.

I have gotten aggressive with MSOS on a scale lower.

My average cost is about $4.76

Position: Long MSOS (M)

BY Doug Kass · Jun 3, 2026, 3:52 PM EDT

In one of the first times in a long time, I am adding to my short index position on weakness:

Position: Short SPY (L), QQQ (L)

BY Doug Kass · Jun 3, 2026, 2:26 PM EDT

Position: None

BY Doug Kass · Jun 3, 2026, 2:20 PM EDT

Wolf Street howls to the housing industry…”wait til next year.”

Position: None

BY Doug Kass · Jun 3, 2026, 2:07 PM EDT

I am old enough to remember when Amazon (AMZN) was everyone’s favorite long.

Position: None

BY Doug Kass · Jun 3, 2026, 12:55 PM EDT

Position: None

BY Doug Kass · Jun 3, 2026, 12:05 PM EDT

I bought a hunk of MSOS at $4.82.

Position: Long MSOS (S)

BY Doug Kass · Jun 3, 2026, 11:40 AM EDT

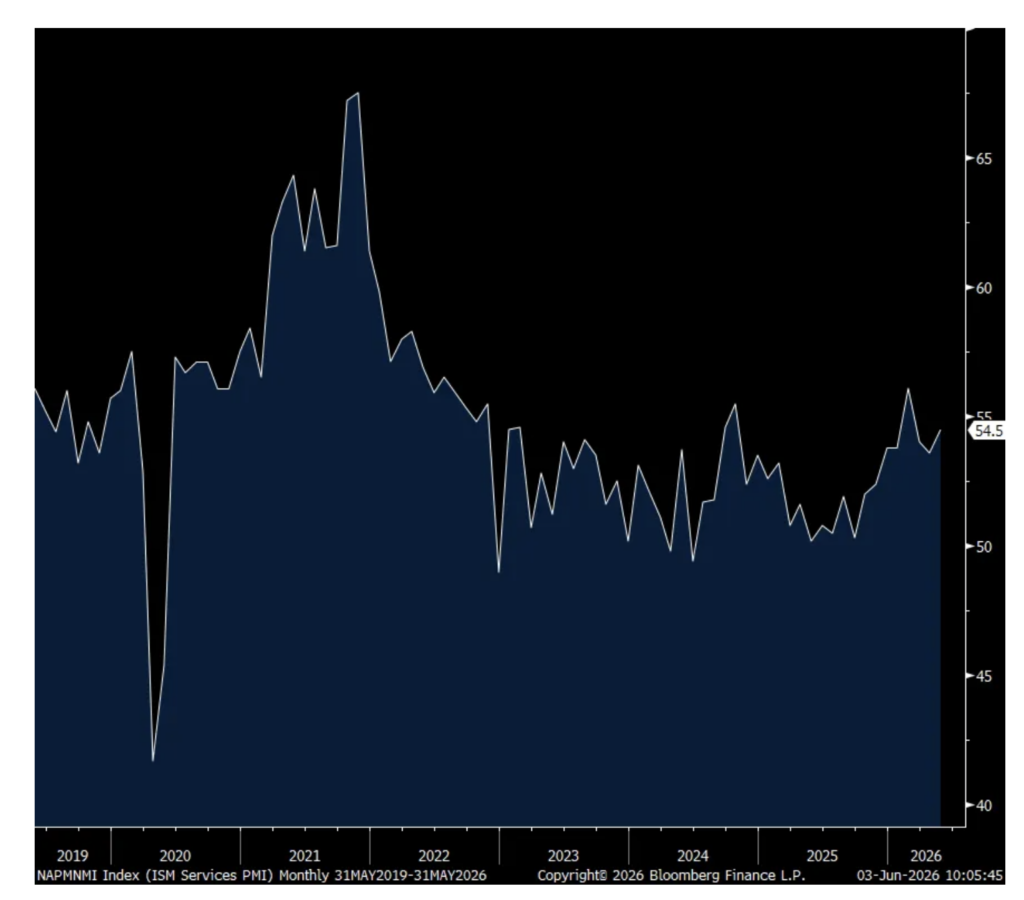

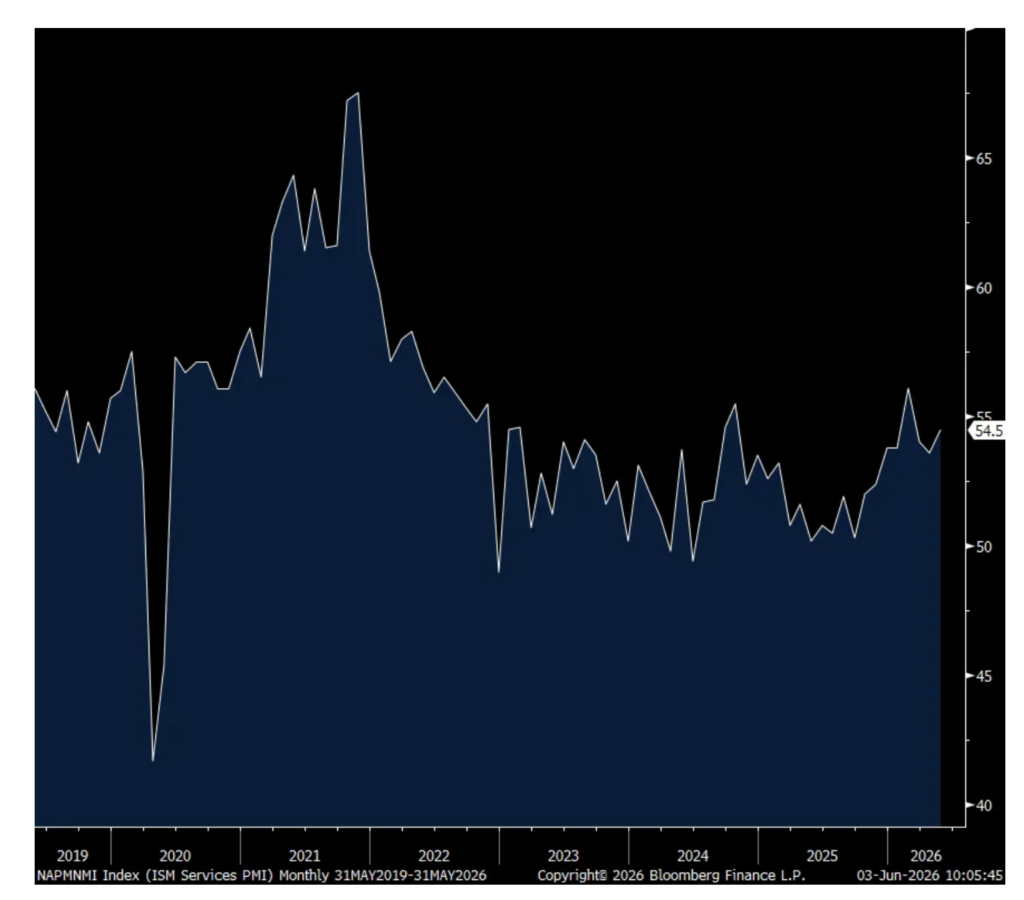

From Peter Boockvar:

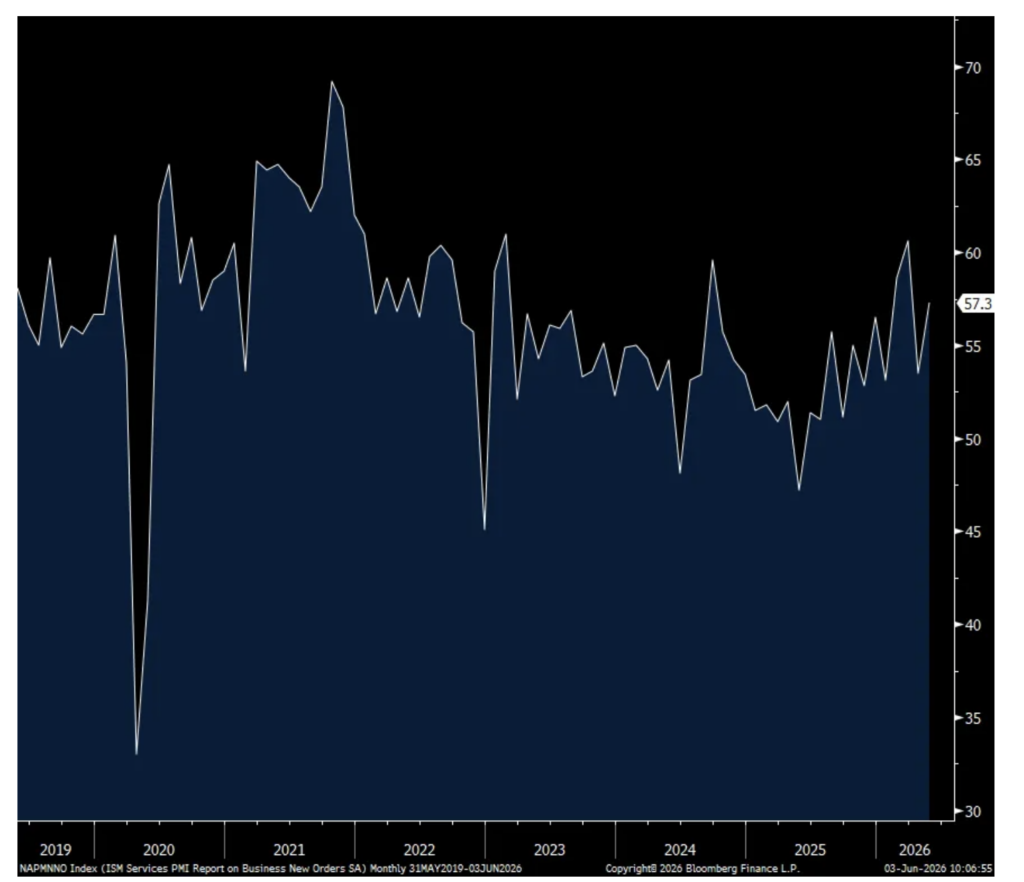

The May ISM services index rose to 54.5 from 53.6 and that was above the estimate of a slight gain to 53.8. New orders rose to 57.3 from 53.5 after falling by 7 pts last month. Backlogs were above 50 for the 4th straight month at 51.3. Likely reflecting the pull forward of ordering I keep hearing about, the inventory component jumped by almost 10 pts to 62.5 matching the highest on record dating back to 1997 with this survey with May 2010 the only other time. I bolded to highlight.

One comment from a respondent of note, “Strong orders fueling need to supply projects as well as replenish stocking inventory.”

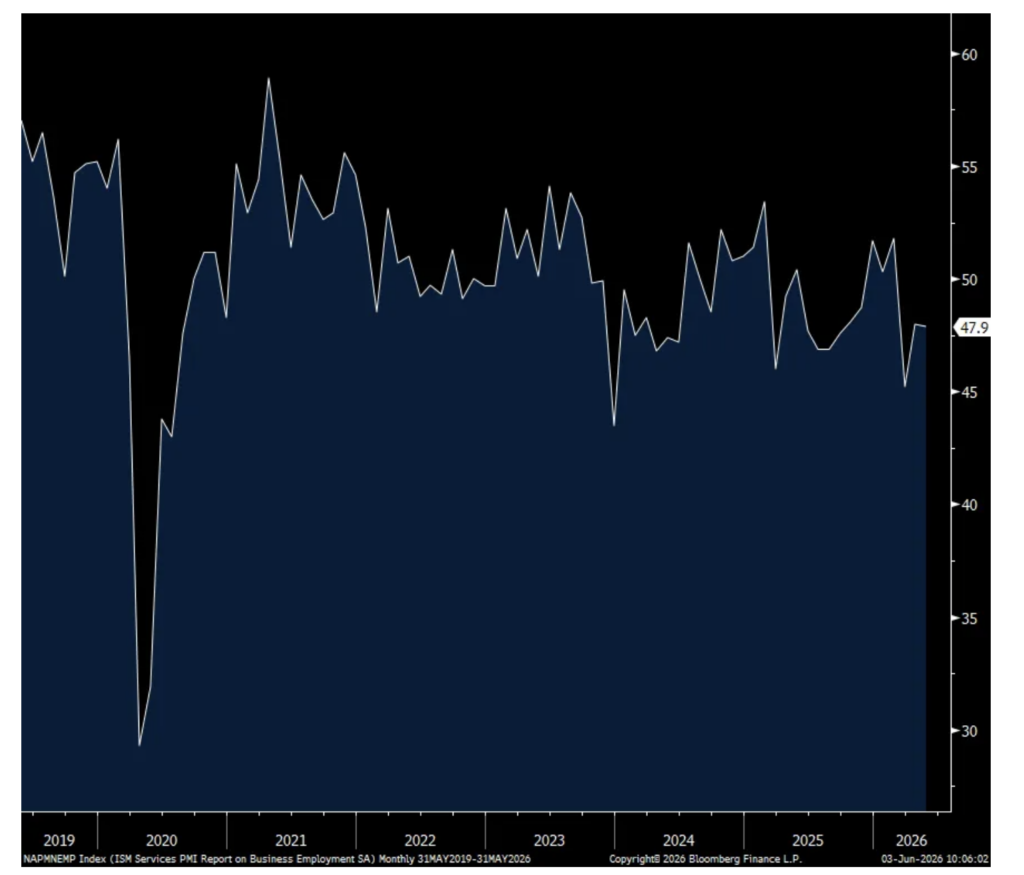

Employment remains a drag coming in at 47.9, little changed m/o/m but below 50 for the 3rd straight month. The ISM said “Respondents commented frequently that their companies had instituted hiring freezes or were not backfilling vacated positions, however, most industries reported that they were holding flat in employment month over month.”

Supplier stress remains but a bit less so as the Supplier Deliveries component slipped to 55.2 from 56.8 and vs 53.9 in February. ISM said, “Comments from respondents include: ‘Freight capacity limitations cited’ and ‘Significant lead times for products like electrical equipment, generators and some mechanical and control systems.’ “

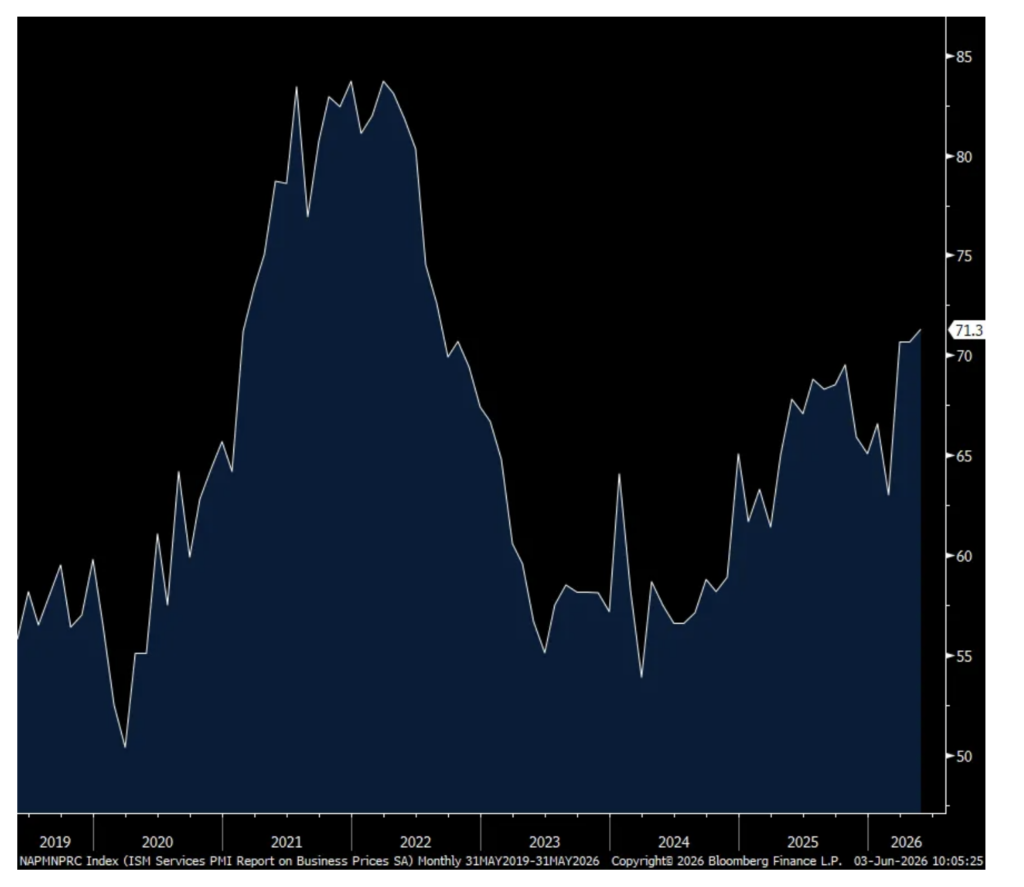

Prices paid remained high, rising by another .6 pts to 71.3 which is the most since August 2022. ISM said, “For the third month in a row, no commodities in the report listed as down in price, with multi month runs of being up in price for aluminum, copper, diesel, gasoline, software licensing and transportation.”

With regards to sector breadth, 17 of 18 industries saw growth in May while just one experienced a contraction, that being in ‘real estate, rental & leasing.’ That compares with 14 industries seeing growth and 3 a downturn.

Bottom line, we know where the strength in the US economy is coming from, AI data centers and all the peripheral beneficiaries, even hotels as workers building the data centers are spending their income, according to Hilton and Hyatt, aerospace & defense, upper income spend and beneficiaries of still massive government spending (defined as a budget deficit as a % of GDP at around 5.5%), particularly healthcare and defense. Here was another respondent comment, “business activity is increasing amid demand for data centers, commercial growth and infrastructure, we are researching increasing generation capacity and new technologies.” And, as stated and seen mostly in manufacturing, the stocking up of inventory is helping too ahead of expected price increases and/or supply issues.

ISM Services

Inventories

Prices Paid

Employment

New Orders

Positions: None.

BY Doug Kass · Jun 3, 2026, 11:30 AM EDT

With the sizable rally in the Nasdaq to positive I have added to my index shorts:

* (SPY) $756.75

* (QQQ) $746.52

Positions: Short SPY L QQQ L

BY Doug Kass · Jun 3, 2026, 11:03 AM EDT

– NYSE volume flat to its one-month average;

– Nasdaq volume flat to its one-month average;

– VIX index: up 1.52% to 16.01

Positions: None.

BY Doug Kass · Jun 3, 2026, 11:01 AM EDT

From 9:39 a.m. ET

Positions: None.

BY Doug Kass · Jun 3, 2026, 10:11 AM EDT

Positions: None.

BY Doug Kass · Jun 3, 2026, 9:59 AM EDT

From Peter Boockvar:

Gold continues to gain as the preferred choice when it comes to the holdings of central banks. The Financial Times is reporting that “Gold replaces US Treasuries as world’s top reserve asset, ECB says.” The piece says “Bullion accounted for 27% of all global central bank reserve assets at the end of 2025, up from 20% a year earlier, according to a report published on Tuesday by the ECB. US Treasuries fell to 22% from 25% over the same period. The share of euro-denominated reserve assets was unchanged at 15%.” This said, “Dollar-denominated assets as a whole still make up the biggest chunk of reserves at 42%, the ECB data showed.” That though compares to about 60% 25 years ago and 50% just a few years ago.

Bottom line, there is a clear diversification of capital flows going on, which is coinciding with a major diversification taking place with regards to trade flows as countries and foreign companies expand the breadth of their trading partners globally. https://www.ft.com

The Bank of Japan might end up raising rates in a few weeks after all. Governor Ueda speaking today for the last time before that meeting said “I think the Bank will continue to raise the policy interest rate at an appropriate pace” and “Based on the data and anecdotal information available thus far, the upside risks to prices appear to be greater overall and are likely to emerge sooner.”

JGB yields are higher in response but the yen is little changed, likely sending the message that they will believe it when they see it.

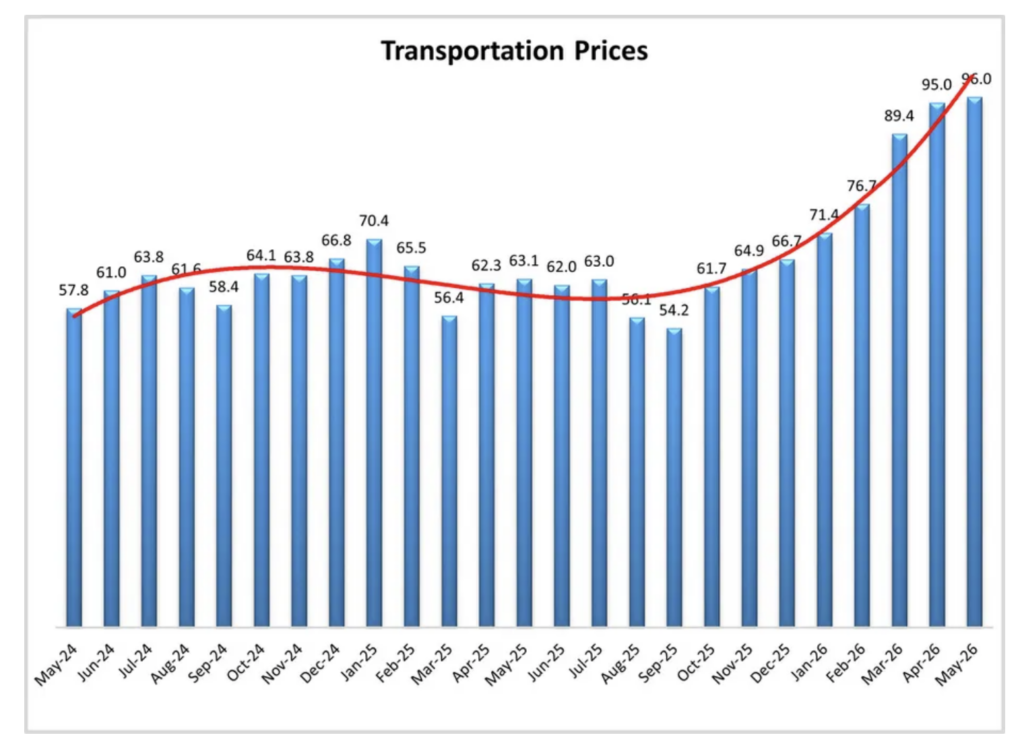

Along with the rising cost of container shipping, along with dry bulk ship, I’ve highlighted multiple times the rising cost of truck transportation. In the May Logistics Managers Index released yesterday, they said this:

“Transportation Prices are up 1 pt to 96, which is the fastest rate of expansion ever recorded for any metric in the nearly ten year history of the index. Transportation Capacity continues to contract quickly at 31.7, and Transportation Utilization expansion remains elevated at 69.5. The transportation market has been tight, with prices growing at an unprecedented rate since the closure of the Strait of Hormuz. The spike in fuel has led to increases for all three of our price and cost metrics, with aggregate logistics costs reading in at 250.9, which is the highest reading since March of 2022.”

Also, and including a point I keep hearing on stock piling, “US supply chains have largely continued operating despite the disruption of 20% of the globe’s oil exports. Upstream firms have pulled inventories forward to curtail future shortages and consolidate shipments, while Downstream firms have kept things leaner in an attempt to mitigate tariffs.”

To some company comments.

Shake Shack lowered guidance right before they spoke at the TD Cowen consumer confidence, its stock fell 8.4% and they said this of note:

“We are seeing some challenges in short to mid term on the cost side. Obviously, I think everyone is aware of the beef prices that we’re battling. They’ve continued to escalate. And we are also seeing fuel surcharge prices on some of our distribution and some of the other input costs in the middle of the P&L.”

“there’s going to be some headwinds in the macro and we acknowledge that. And that’s part of what you see in the update and guidance today reflecting our views on the current cost structure and what our views are just given the competitive landscape and all the things that we know today.”

From Dollar General and whose stock traded down by 3.3% yesterday:

“We grew market share in both dollars and units in highly consumable product sales once again during the quarter, in addition to growing market share in non-consumable product sales.”

Comps grew by 2% “primarily driven by customer traffic growth of 1.4%, and supported by average basket growth of .5 point. Notably, this marks the fourth consecutive quarter of growth in customer traffic as our combination of value and convenience continues to resonate with customers.”

“While there are a variety of puts and takes on customer budgets during Q1, our core customer continues to be financially constrained, as any benefit from tax benefits was largely offset by higher fuel prices and reductions in SNAP benefit payments. Importantly, while there has been a significant reduction in overall SNAP dollars distributed in 2026, we grew share of wallet with SNAP customers during Q1, further demonstrating the strength and relevance of our value proposition.”

“Notably, during the quarter many of our core customers reported cutting back on other household expenses, including food purchases, due to rising gas prices. This pressure has been more pronounced on customers in rural communities as they work to minimize trip distance and make trade-offs in their search for everyday affordability and value.”

And in the search for value by everyone, “we are seeing customer penetration growth across low, middle and high-income segments, as customers across all income cohorts seek value at increasing rates. Notably, across these cohorts, the largest increase in customer count came from the highest income segment, which earns more than $100,000 annually, contributing to a significant increase in trade-in customer households during the quarter.”

From Signet Jewelers, up almost 4% yesterday but after falling by 3% Monday:

“We delivered comp sales growth across every category and most brands this quarter…we continue to see strength in higher end consumer with some of our best performance at higher price points.”

“By category, growth was low single digit for bridal and fashion with stronger growth in watches and services.”

To a question on whether their business has been impacted by higher tax refunds but also higher gas costs and general inflation, the answer was basically no as “We’re much more tied to milestone, whether that’s engagement, gift, holiday, etc…Also tied to a big chunk of our business to a purchase that relies on credit or some form of financing for our customer. And so, bottom line is those kind of short term moves don’t have as big of an impact in our business.”

Victoria’s Secret rallied like a semiconductor stock yesterday, skyrocketing by 47% as while they modestly beat sales estimates, they blew away the operating income forecasts. From them:

“We achieved our 4th consecutive quarter of positive comps with total comp sales increasing 13% and driving total sales growth of 15%. We also saw strength across channels and geographies. We were particularly encouraged by double digit gains in new customer acquisition and continued file growth across all age and income cohorts. In fact, we saw the strongest growth from customers and households earning under $50,000 annually and over $200,000, underscoring the broad resonance of our brands across the consumer landscape.”

“During the quarter, we continued to gain share in intimates, particularly amongst 18 year olds to 24 year olds. Traffic also accelerated from the 4th quarter, reinforcing the momentum we are seeing across the business.”

Ulta Beauty is down a touch pre-market and they said this last night on their call of note:

“growth in the beauty category remains healthy, even as consumers are increasingly value focused…And while we are continuing to monitor how the macro landscape could evolve, we remain execution focused and are confident we will deliver our fiscal 2026 expectations.”

Fragrance was their best selling category in the quarter and “growth was primarily driven by newness from core luxury brands” like YSL, Carolina Herrera and Valentino.

Notwithstanding a good Q1, “we believe it is prudent to take a measured approach to our guidance given the uncertain macro landscape.”

With the average 30 yr mortgage rate staying above 6.50%, at 6.57%, though down from 6.65% in the week before, purchase applications fell for the 4th week in the past 5, down another 2.9%. Refi’s were down by 2.3% w/o/w after dropping by 18% in the week before. We know affordability remains the big problem in the housing market.

Overseas, China’s private sector weighted May services index rose to 54.4 from 52.6 and 2 pts above the estimate. RatingDog said “The faster increase in activity was accompanied by a further acceleration in the rate of growth in new business moving through the second quarter. The rate of expansion in demand for services accelerated for the fourth time in five months and was broadly in line with the long run survey averages. Increased client demand, business innovation and expansion, new client acquisitions, improved market conditions and the development of new projects were all mentioned as sources of new work.”

The revised service PMI’s for Germany, France, Italy and the UK all remained below 50 while Spain just got there at 50.1. The UK was close at 49.3. Not surprisingly, “Cost pressures in the service sector continued to increase, as they now have done in every month since the start of the war in the Middle East. Output charge inflation saw only a fractional uplift from April, however.”

Nothing market moving here but still highlighting the sluggish growth in the region on the service side.

Positions: None.

BY Doug Kass · Jun 3, 2026, 9:45 AM EDT

I covered all of my (MRVL) short at $309.30 (shorted at $336 at 4:15 a.m.) for a quick and good profit.

Position: None

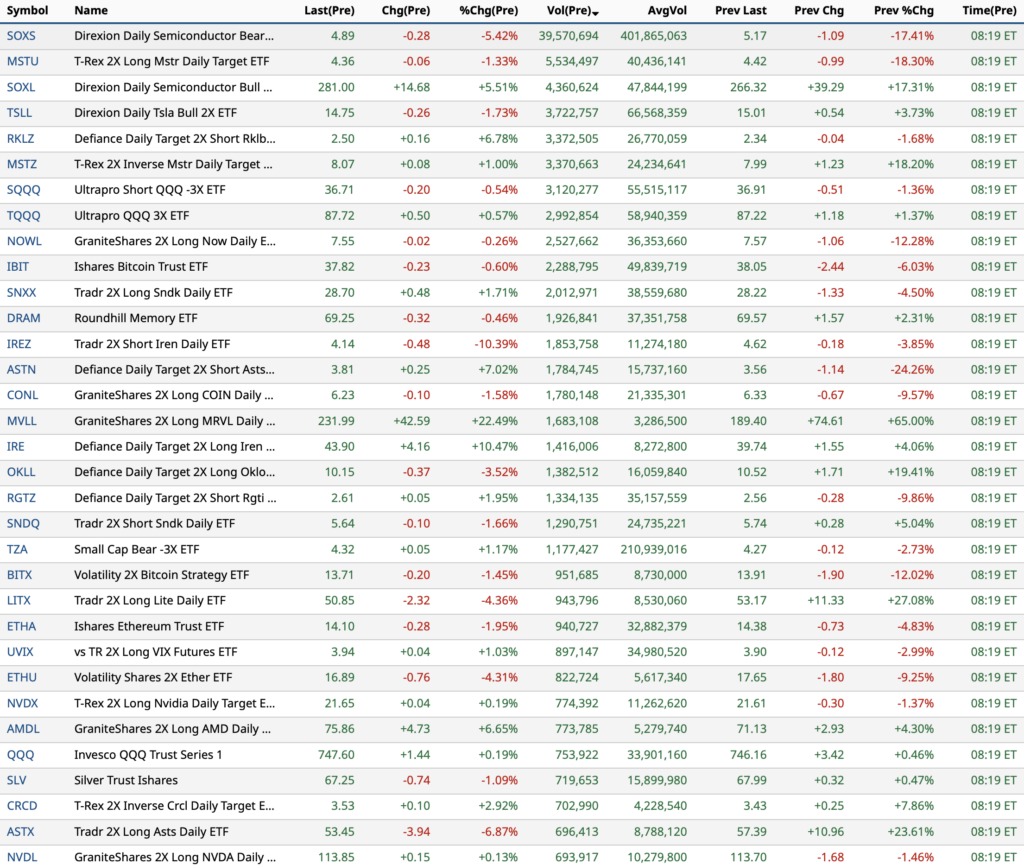

BY Doug Kass · Jun 3, 2026, 9:40 AM EDT

-ABVX +14% (bounce following dropping >40% yesterday following ABTECT data)

-BCHT +12% (announces end of all remaining attempts using IPR petition to challenge patents)

-MRVL +12% (momentum following NVDA CEO endorsement; Evercore conference presentation)

-GME +10% (earnings, color)

-NVTS +10% (shows 800 V-to-6 V DC-DC PDB at NVIDIA AI Factory MGX Ecosystem Showcase)

-RZLT +9.3% (Citizens JMP Securities Raised RZLT to Market Outperform from Market Perform, price target: $11)

-AXSM +6.0% (resolves all SUNOSI patent litigation)

-INTC +6.0% (CFO highlights ramping 18A supply and CPU demand)

-DGXX +5.6% (commits $35M to buy NVIDIA Vera Rubin systems)

-MMED +5.3% (earnings; expands Abbott dual glucose-ketone sensor collaboration for MiniMed smart dosing systems)

-USAR +5.2% (finalizes definitive agreements with US Department of Commerce for up to $1.6B in CHIPS Program funding)

-OLLI +4.6% (earnings, guidance)

-SHW +3.6% (Nippon Paint and Sherwin-Williams desist from acquisition attempt of Akzo Nobel NV)

-M +2.5% (earnings, guidance)

-KBR +2.1% (awarded $8B-ceiling US Govt Antarctic Science and Engineering Support Contract)

-YEXT -21% (earnings, color)

-CGNT -19% (earnings, guidance)

-ARES -6.5% (Partners Group caps private equity fund withdrawals)

-ARDT -6.4% (appoints Dave Caspers President and CEO, effective immediately)

-LUNR -6.3% (files to sell up to $500M in stock)

-GTLB -6.2% (Partners Group caps private equity fund withdrawals)

-KKR -6.0% (Partners Group caps private equity fund withdrawals)

-CXM -5.8% (earnings, guidance)

-HLNE -5.8% (Partners Group caps private equity fund withdrawals)

-THO -5.8% (earnings, guidance)

-APO -5.3% (complete Sale of ALTEMIRA, Leading Pan-Asian Aluminum Packaging Company)

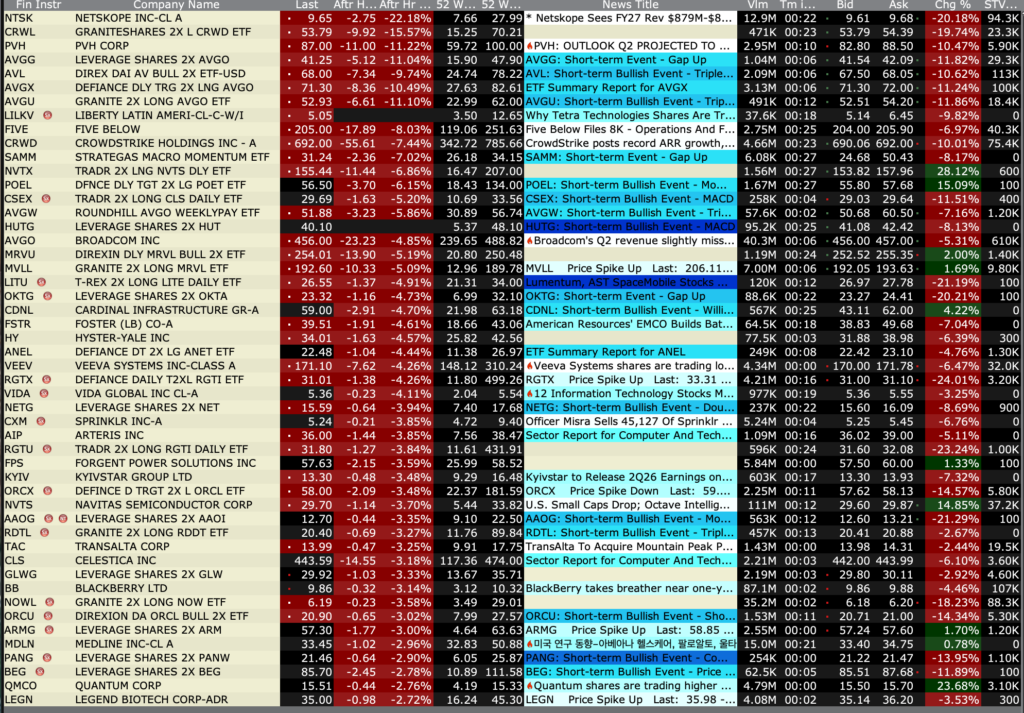

-PANW -3.5% (earnings, guidance)

-ULTA -2.8% (earnings, guidance)

-ODD -2.3% (KeyBanc Capital Markets Cuts ODD to Sector Weight from Overweight)

BY Doug Kass · Jun 3, 2026, 9:35 AM EDT

On strength, over the last few trading days, I have steadily

increased the size of my Index shorts from very small to large sized.

Positions: Short SPY L QQQ L

BY Doug Kass · Jun 3, 2026, 9:10 AM EDT

From Peter Boockvar:

ADP said 122k new private sector jobs were created in May, about as expected and vs 105k in April (revised from 109k initially). Businesses of all sizes added workers with the biggest contributor being those with under 20 employees, adding 49k jobs. Those with 500+ added 40k with more modest gains in between.

Again, the sector with the biggest hiring remains education/health services which hired a net 57k, followed by 36k in trade/transportation/utilities. Financial services, leisure/hospitality and professional/business services also added workers. The ‘information’ sector continued to lose them, by 9k in the month. Construction employment rose by 8k and manufacturing by 3k, partially offset by a 3k person decline in natural resources/mining.

ADP said “The labor market continues to show sustained momentum going into the summer hiring season.” Wage growth was similar to that seen in April with a 4.4% rise for ‘job stayers’ and 6.5% increase for ‘job changers.’ With inflation accelerating, the wage growth needed to offset it is ever more vital.

Bottom line, this brings the 3 month average to 96k vs the 6 month average of 67k and the 12 month average of 59k. ADP doesn’t separate out part time from full time and we’ll get more color on that Friday but overall the pace of hiring has been pretty good over the past three months relative to the more modest pace previously.

The 10 yr yield is knocking on 4.50% again in response, up 1 bp from just prior to the release and up 4.5 bps from yesterday. The 2 yr yield is higher by 3.5 bps today, 1 bp of which was right after the data release.

Positions: None.

BY Doug Kass · Jun 3, 2026, 9:02 AM EDT

Positions: None.

BY Doug Kass · Jun 3, 2026, 8:55 AM EDT

Positions: none.

BY Doug Kass · Jun 3, 2026, 8:41 AM EDT

Knowledge@Wharton Is AI Killing User Experience?

Is AI Killing User Experience? – Knowledge at Wharton

Positions: None.

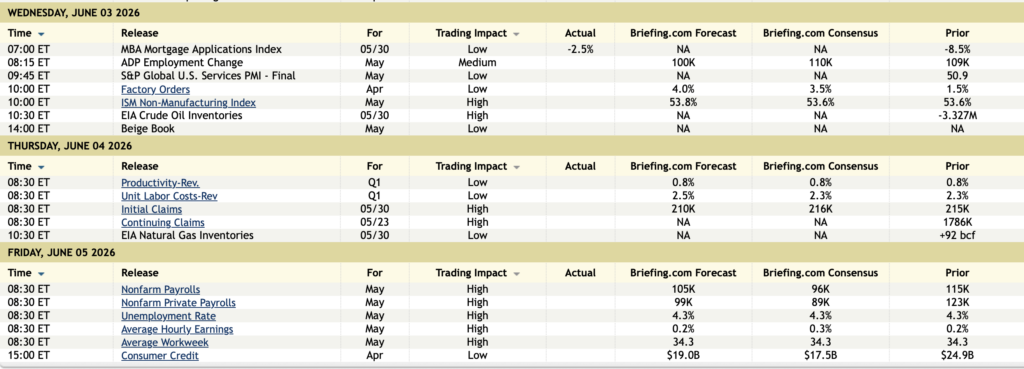

BY Doug Kass · Jun 3, 2026, 8:30 AM EDT

11:30 a.m. Treasury hosts a $69B 17-Week Bill Auction;

2:00 p.m.: Treasury buyback (liq support);

2:00 p.m.: Fed Beige Book

9:00 a.m.: Fed Board Governor Barr (Voter) participates in conversation before the Community Development Bankers Association (CDBA) Peer Forum 2026, Washington, DC (No text. Q&A from moderator. Webcast at https://www.youtube.com/watch?v=TqBUenL–EI);

4:00 p.m.: Fed Bank of Dallas President Logan (Voter) shares insights from her leadership role at the Federal Reserve, being a voting member of the Federal Open Market Committee and perspectives on the evolving economic landscape in a conversation as part of the “Listening in 360 Tour,” El Paso, TX

(No text. Livestream at https://vimeo.com/event/5962846/embed/259f522fb5 OR https://www.youtube.com/live/zc6iogFFkG0)

Positions: None.

BY Doug Kass · Jun 3, 2026, 8:24 AM EDT

Position: None

BY Doug Kass · Jun 3, 2026, 8:00 AM EDT

Position: None

BY Doug Kass · Jun 3, 2026, 7:50 AM EDT

Position: None

BY Doug Kass · Jun 3, 2026, 7:40 AM EDT

Look for more weakness in private equity shares today:

Position: None

BY Doug Kass · Jun 3, 2026, 7:25 AM EDT

Position: None

BY Doug Kass · Jun 3, 2026, 7:10 AM EDT

Talking my book:

Position: None

BY Doug Kass · Jun 3, 2026, 6:55 AM EDT

To be clear, PANW traded +$35 after the EPS release and is now -$50/share lower.

I thought Jim’s dismissal of the reversal was symptomatic of how speculative the market has become — in a “heads I win, tails I win” backdrop.

So I see a different message…. and a more punitive outcome (for the Nasdaq).

Position: None

BY Doug Kass · Jun 3, 2026, 6:45 AM EDT

Position: None

BY Doug Kass · Jun 3, 2026, 6:35 AM EDT

Position: None

BY Doug Kass · Jun 3, 2026, 6:25 AM EDT

Position: None

BY Doug Kass · Jun 3, 2026, 6:15 AM EDT

The S&P Short Range Oscillator remains overbought at 2.97% vs. 3.08%.

Position: Short SPY (L) QQQ (L)

BY Doug Kass · Jun 3, 2026, 6:05 AM EDT

Adding to QQQ short at $747.60. (5:30am)

And…

Dougie Kass

early speculative trading

back shorting MRVL at $336 at 415 AM

Position: Short QQQ (L), MRVL (VS)

BY Doug Kass · Jun 3, 2026, 5:55 AM EDT

At 4:55 PM Tuesday I added to index shorts:

Position: Short SPY (L), QQQ (L)

BY Doug Kass · Jun 3, 2026, 5:45 AM EDT

The S&P Tech sector's trailing 12-month P/E ratio has jumped from roughly 32 to 48 since the 3/30 low.

Upon up listing the dog will start wagging its tail vs the tail wagging the dog. $MSOS

There are a lot of smart people at Google. They have concluded that issuing stock at a 2.5% earnings yield is cheaper capital than issuing 30Y bonds at 5.5-6.0%. Adjust your asset allocation accordingly.

Oppenheimer brings out an interesting point here. If $GOOGL that prints massive FCF is tapping equity markets for $80B it's because credit is drying up. The private credit canary in the coal mine just died. The fact that their raise includes a massive $40B ATM and a $10B private

S&P 500 is up 9 days in a row and 9 weeks in a row. One of the strongest, most unrelenting rallies in history.

Paul Tudor and Ray Dalio both hit bottom - Tudor lost 60% of client money, Dalio borrowed $4K from his father - now they run two of the greatest funds - on one couch, together they held a workshop on how to trade right now they said "the system is broken" 37-min masterclass Show more

Stan Druckenmiller made 1 trade - earned $1B destroying the UK economy, Paul Tudor made 1 trade - earned $100M predicting Black Monday on one JPMorgan stage they showed for the first time exactly how they made $1.1B in 24 hours 35-min from the two greatest traders alive - how

Just to clear the record: Palo Alto did NOT miss the high expectations. Stock up tremendously ahead of the report, was up huge then gave it. Usual pattern for this one...

The embedded tweet could not be found…

The redemption issue in developed market private credit just won't go away, at least as yet: Partners Group is the latest investment manager forced to cap redemptions at 5% after facing large Q2 withdrawal requests from its $9 billion fund. The fallout: The stock tumbled nearly Show more

Goldman Sachs on AI: "We now expect a combined $5.3 trillion of capex spending for the four largest hyperscalers from FY2025 to FY2030 (Meta, Microsoft, Amazon, and Alphabet). We highlight a baseline aggregate capex estimate of $7.6 trillion between 2026 and 2031, across Show more

Semiconductor Stocks are now trading 73% above their 200-day moving average, the largest margin since the Dot Com Bubble 🤯👀

Almost there...

Another way to frame today's valuation backdrop: Investors are currently receiving less earnings yield from stocks than they can get from bonds. The equity risk premium recently fell below -0.85, among the lowest readings in decades.

BREAKING: The US technology sector has rallied +42% over the last 2 months, the largest 2-month gain in 24 years. This also marks the 2nd-strongest rally this century, surpassing even the +40% gain seen during the 2000 Dot-Com Bubble. The surge has been largely fueled by chip Show more

hard to make all these numbers square

🦔IBM CEO Arvind Krishna says AI is "not a bubble" then estimates the industry needs $6 to $8 trillion in total capex for data center and chip buildout. To recover that over seven years, companies would need $1 to $2 trillion in new annual revenue. Krishna says he doesn't believe