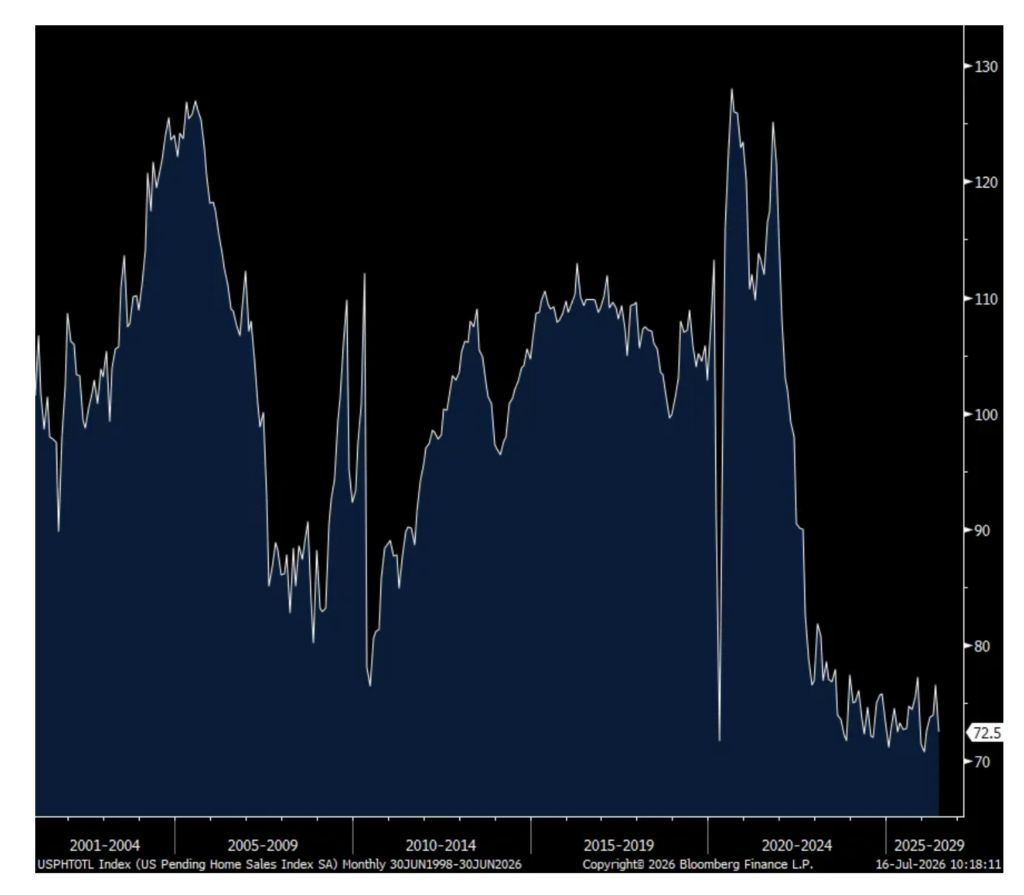

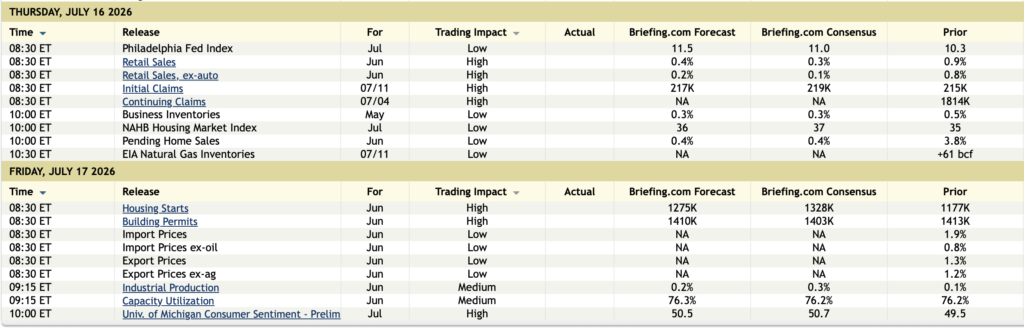

The housing market remains the challenged part of the US economy. Pending home sales in June fell 5.4% m/o/m, well worse than the estimate of a drop of .5% and offsets the 3.5% rise in May and takes the index to a 5 month low and just off a record low for this index. There was little change in mortgage rates in June but did lift off the early part of May.

The NAR said “The highest mortgage rates in nearly a year and the record-high national median home price together are contributing to a tepid housing market that is especially difficult for first-time homebuyers. However, job gains can help support housing demand.”

I’m not sure why the NAR added this to their press release as we know that pending home sales measures just contract signings but they did say “Pending contracts are only suggestive of upcoming closed deals and do not align perfectly, due to fallout rates and contract contingencies.” Maybe they are seeing something?

Pending Home Sales

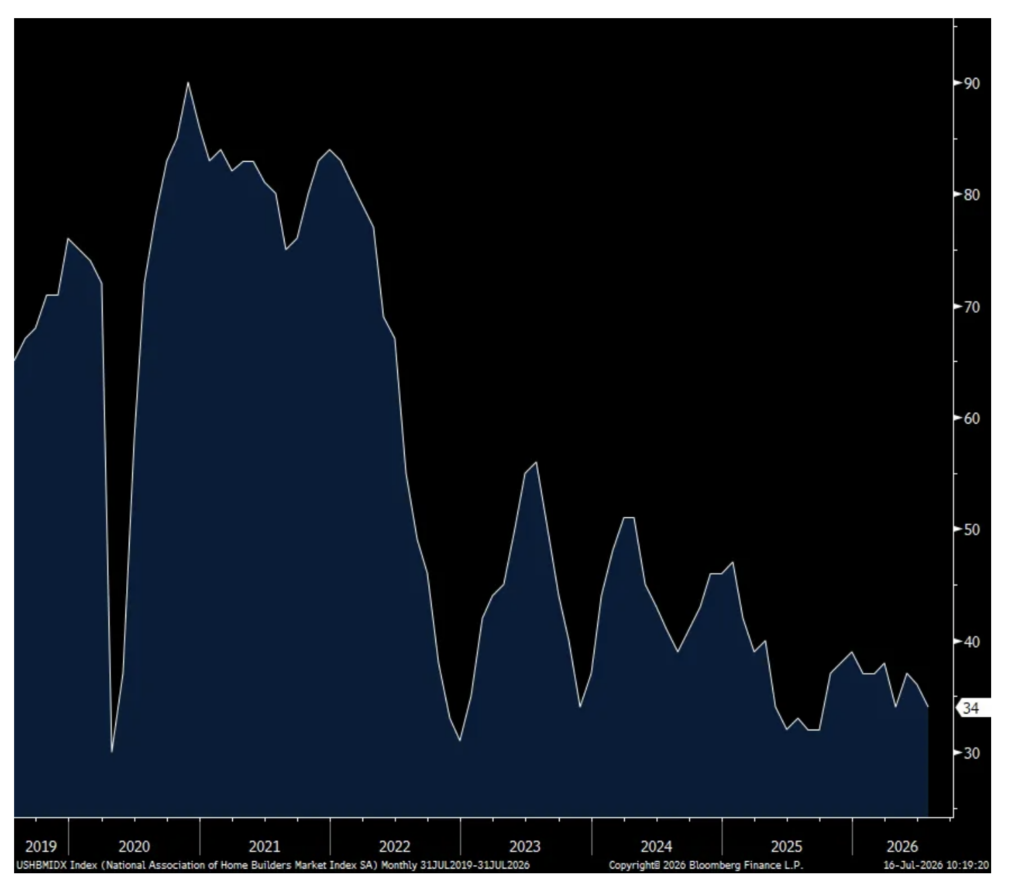

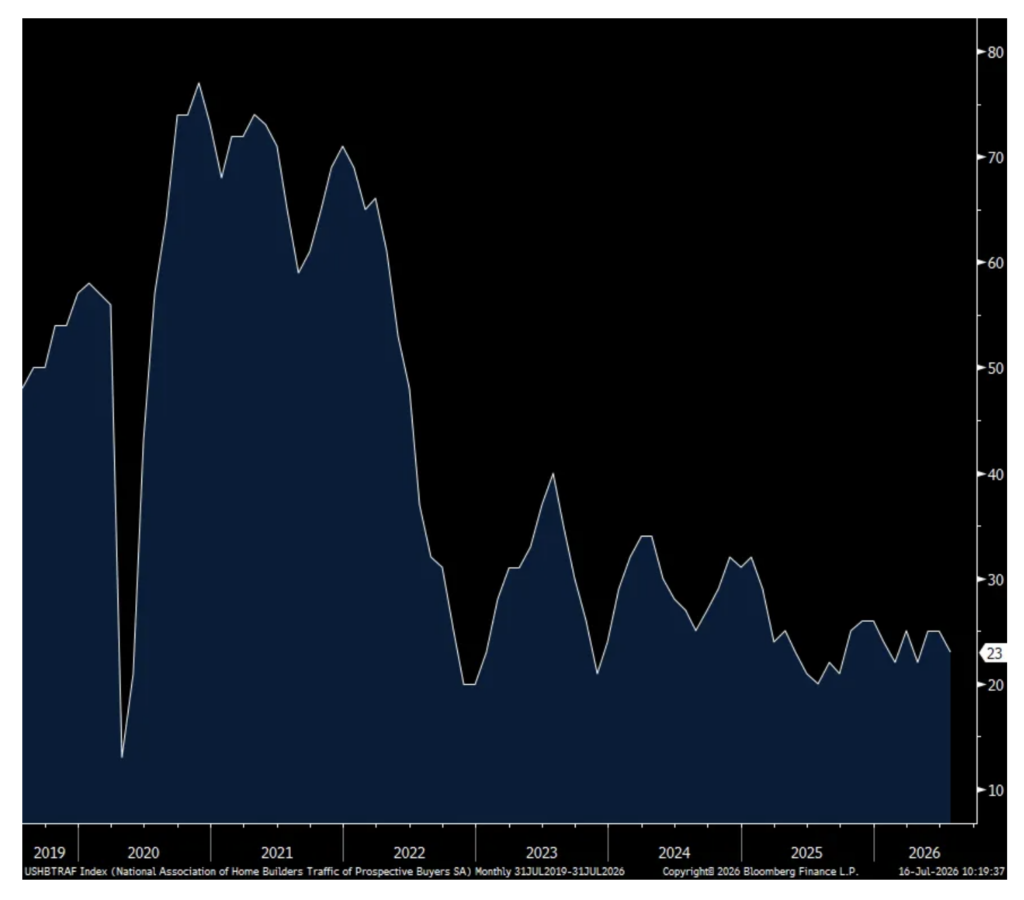

Home builders still remain sour with the July NAHB builder sentiment index falling 2 pts m/o/m to just 34 and well below the 50 breakeven. The estimate was 35. Prospective buyers Traffic fell 2 pts to just 23.

The NAR said “Many potential buyers remain on the sidelines as they wait for lower mortgage rates, more certainty on inflation and a clearer economic outlook…With the HMI below 40 for 15 straight months, affordability remains the home building industry’s primary challenge, as elevated mortgage rates, costly land, rising material prices, and persistent skilled labor shortages continue to affect the market.”

And to the extent builders are trying to drive sales, “The latest HMI survey also revealed that 37% of builders cut prices in July, up from 35% in June and 32% in May. The average price reduction was 6% in July, the same rate as the previous month. The use of sales incentives was 63% in July, up slightly from 62% in June, and marking the 16th consecutive month this share has reached 60% or higher.”

There is hope with the newly passed housing bill, “The recently enacted 21st Century ROAD to Housing Act contains important provisions on land-use and zoning, regulatory reform and financing tools that address obstacles facing builders and buyers, but these reforms will take time to implement.” But, we know that a lot of zoning and regulatory reforms need to take place at the local and state level.

Bottom line, as said above and something we know, housing remains the downer in the US economy and according to the NAHB makes up about 15-18% of the U.S. economy all in.

PPI vs CPI/Beige Book/Kospi, BoK/Earnings/French 10 yr yield at 17 yr high

As of June, we now have PPI running about 200 bps higher than CPI which means there is a profit margin squeeze for some going on. Conagra is a perfect example of that, a stock we own, that said yesterday “Total inflation, inclusive of both core inflation and gross tariffs, remained elevated in Q4 at approximately 6.5%. We saw sustained inflation in areas including beef and edible oils, as well as more recent increases in areas related to crude oil and logistics.”

Luckily for them they’ve been able to offset some of this via productivity gains and tariff refunds and some price increases but not all of it as adjusted operating margins fell 215 bps y/o/y. “Going forward, we see an opportunity to better balance the volume and margins…This includes implementing strategic pricing actions in several areas of the portfolio including frozen, as we look to set a foundation for profitable growth moving forward.” ‘Strategic pricing actions’ imply higher prices but with volumes still subdued, we’ll see what they can get away with.

Point here again is that just by looking only at CPI and/or PCE, you are not getting the full inflation picture without combining PPI.

The Fed’s Beige Book talked about this yesterday. On the cost side, “Non-labor input costs increased for a variety of industries—including services, construction, and manufacturing—and reflected in part higher costs for energy, transportation, and raw materials. Some contacts tied these cost increases to the conflict in the Middle East; others mentioned tariffs.”

And the extent of the pass through, “Consumer prices continued to rise, and a few Districts said contacts saw greater price sensitivity among their customers. A couple of Districts reported that selling prices grew less than input costs over the period, crimping margins. Expectations for price growth over the coming months varied across Districts, with contacts in some expecting inflation to continue at its current pace, while contacts in others expected inflation to slow, in part due to falling fuel prices.”

This was specifically from the NY region, “The pace of selling price increases remained at the high end of the moderate range, while input prices continued to rise strongly. Rising fuel prices continued to drive widespread increases in the costs of freight and other inputs more generally. Tariffs also continued to exert upward cost pressures. One upstate New York manufacturer reported ongoing increases in steel and aluminum costs due to tariffs, while another expected some relief from high tariffs when temporary tariffs expired and tariff refunds were received. Another upstate New York manufacturer said they had implemented large price increases and were adding additional time for delivery for anything not in stock. Separately, an upstate New York-based technical consulting firm reported sharp price increases for memory and storage components driven by elevated demand from data center buildouts. Many businesses were continuing to pass along cost increases to customers, though some firms were concerned about consumer pushback. Contacts anticipated some slowing in the pace of input price increases in the coming months.”

Broadly from the Fed’s Beige Book, it still sounds like a 2%ish economy. “Economic activity increased at a slight to moderate pace in eleven of twelve Federal Reserve Districts in late May and June, while one District reported no change. The pace of growth was quite close to that of last period, when activity expanded in ten Districts, was flat in one, and down in one.”

Some more, “Consumer spending edged up as higher prices, particularly for fuel, dampened sales in other categories. Several Districts noted declines in spending on discretionary items or trading down to more affordable varieties.”

“Tourism was up, with some Districts receiving a boost from World Cup visitors.”

“Auto dealers reported little change in sales, but spending on repairs grew as consumers held onto vehicles for longer.”

“Manufacturing production grew modestly to moderately in most Districts, led by stronger orders from the data center, machinery, and defense sectors. Manufacturers in several Districts said supply chain issues were more common.”

“Construction and real estate activity increased slightly overall, with several Districts noting growth in data center building.”

“Transportation activity increased modestly amidst ongoing supply chain changes related to higher tariffs and the conflict in the Middle East.”

The labor market was mixed but a bit better than the prior report, “Employment rose on balance, with five Districts showing modest, moderate, or solid gains in employment, and with seven Districts experiencing little to no change. In the previous report, only one District had modest, moderate, or solid employment gains.”

“Employment rose in a variety of industries, including manufacturing, construction, and retail. Skilled workers were difficult to find in a range of fields, notably technicians and tradespeople. Though there were reports of lower employment in a couple of Districts, the declines were small.”

“Wage growth was modest to moderate in most Districts, though two saw only slight wage increases. Some wage increases were attributed to increased competition for skilled workers. A few Districts noted that firms had increased their usage of AI, either in the hiring and screening of potential employees or to boost worker productivity.”

Shifting to stock market sentiment, I mentioned Monday that the Citi Panic/Euphoria index is well into euphoric and yesterday’s Investors Intelligence survey is now knocking on the door of extreme bullishness that I define as a 40 point spread between Bulls and Bears. Bulls rose to 55.5 from 53.9 while Bears fell to 16.7 from 17.3. Today’s AAII survey saw Bulls jump by 8.6 pts to 44.9, matching the highest since April while Bears dropped by 4.3 pts to 32.9, the least since early February. The CNN Fear/Greed index at 47 is the only gauge not offsides here as it’s in the neutral camp.

Bottom line, strictly from a sentiment standpoint, the above is a yellow light.

I thought the Chinese DRAM maker CXMT was going public this week but it will instead be next week in Shanghai, not Hong Kong. As a reminder, they have 8% of the DRAM market for a company that only began 10 years ago. What they are going after is to mostly increase the share they get from China customers that currently mostly do business with Samsung and SK Hynix but the whole world is their oyster. As Chinese companies first prioritize market share over profit margins, ignore their competitive threat at your equity peril.

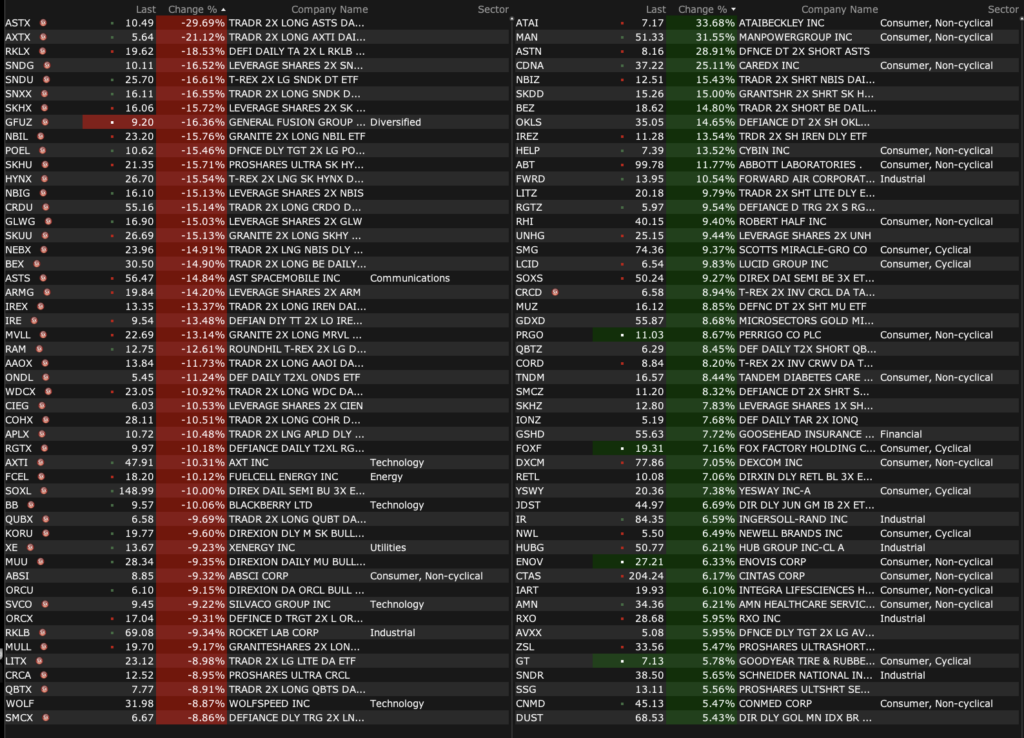

Speaking of chips, South Korea is taking steps to cool down the speculation as their Financial Services Commission is temporarily stopping new issuance of single stock leveraged ETFs. There are already a bunch out there so market players will still have plenty of ways to bet but the scrutiny of these products is obviously rising.

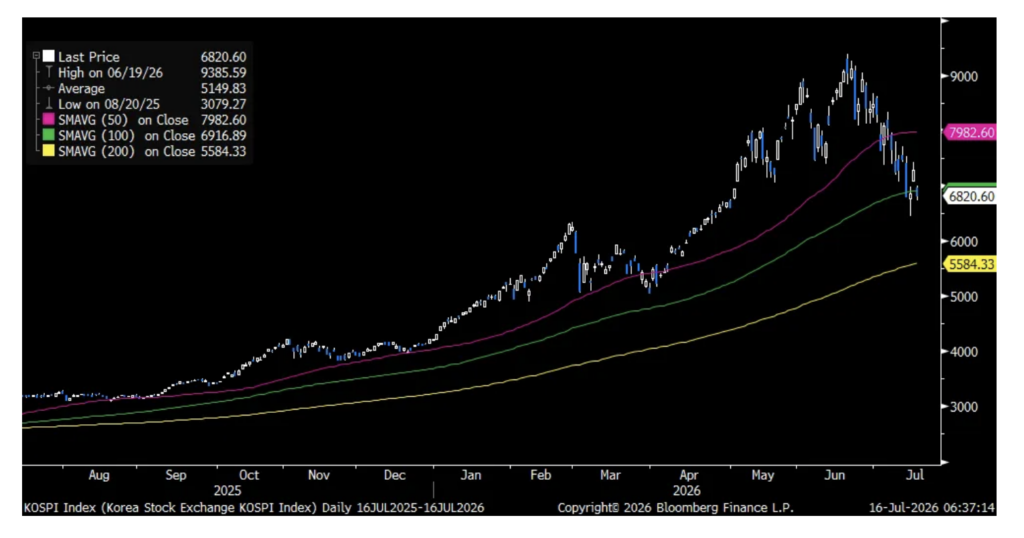

Combine this with a Bank of Korea rate increase to 2.75%, as expected, and the Kospi was down 6.4% overnight, lowering its year to date gain to ‘just’ 62% after being around a double at the highs. The index is now sitting on its 100 day moving average, down 27% from its peak. And more rate hikes are possibly to come, “The next several policy meetings are all live. We’ll keep all options open and base our decisions on the incoming data…We will respond until we are confident that inflation is converging stably to the target.” And the value of the Korean won is now a factor in policy, “The won has stabilized somewhat compared with a few weeks ago, but it still remains weak, keeping import prices elevated.”

Kospi

The Bank of Canada yesterday left its overnight rate unchanged at 2.25% as fully expected. They said in their statement, “Growth is picking up and inflation is projected to ease gradually from its recent spike.” They mentioned the Middle East and that “The path for global inflation is highly dependent on how the conflict unfolds.” Going forward, it seems that the BoC is on hold for now.

To some earnings releases and calls.

The high end continues to do well as heard from Richemont with “Strength across all regions led by local demand, with double digit increases in the Americas, Asia Pacific, Japan and Europe…return to growth in Middle East & Africa.”

“The Group’s four Jewelry Maisons – Buccellati, Cartier, Van Cleef & Arpels and Vhernier – posted a remarkable combined 24% rise in sales, marking a 7th consecutive quarter of double digit growth. Both jewelry and watch lines performed strongly.”

From JB Hunt, that is up pre-market and benefiting from the sharp rise in trucking prices:

“It is increasingly clear that the freight market has changed. Capacity has tightened across the industry, as safety focused enforcement and broader supply pressures continue to affect available truckload capacity. We saw that tightening build throughout the quarter, including the noticeable step change around the annual road check event in early May that has persisted.”

“While demand is improving gradually, the current market tightness is being driven primarily by supply conditions…As a result, several industry indicators, including higher tender rejections, higher spot pricing and lower driver employment, moved towards levels not seen since 2021 and 2022.”

From United Airlines, down pre-market:

“Based on oil prices as of July 14th, United expects nearly $6 billion in added fuel expense for full year 2026 compared to the expectation at the start of the year. In the second quarter fuel expense was up $2.3 billion, or 84% y/o/y and the Company recovered approximately half of this increase. In the third quarter the Company expects to recover approximately 80% to 90% of the increase, and 100% by the fourth quarter.”

With respect to the revenue drivers, “Premium revenue was up 16% compared to the 2nd quarter of 2025, revenue from Basic Economy was up 11%, loyalty revenue was up 11% and cargo revenue was up 23%.”

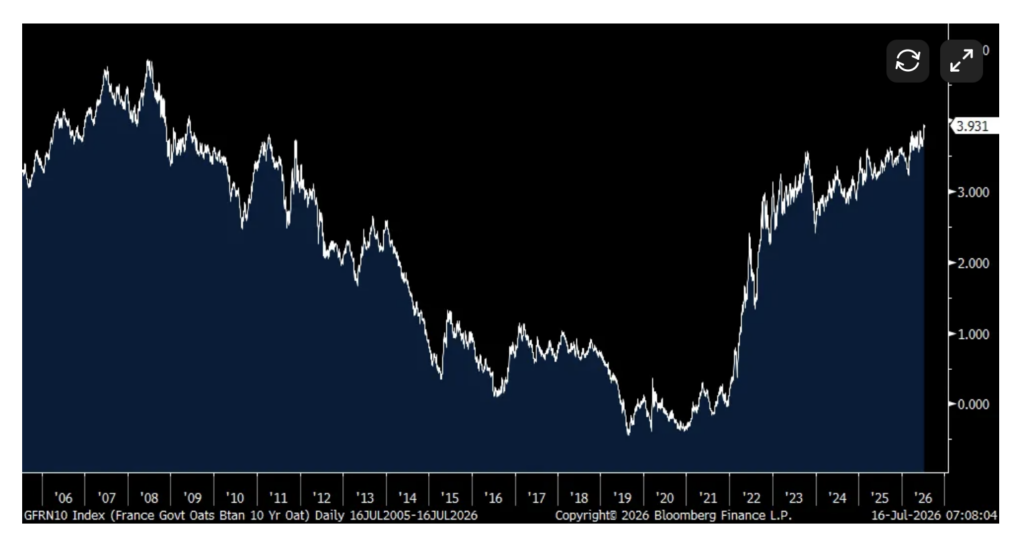

Finally, I’ll continue to harp on the rise in long term rates in developed markets. The French 10 yr oat yield is trading today at the highest level since 2009. It’s not because the French economy is booming. Debts and deficits now matter. The German 10 yr yield is just 6 bps from a 15 yr high.

11 am.: Treasury Announces a TIPS and Bond Auction

11:30a.m.: Treasury hosts a $110B 4 and a $100B 8 Week Bill Auction;

2:00 p.m.: Treasury buyback (liq support)

Fed Lineup

12:30 p.m.: Fed Bank of Dallas President Logan (Voter) participates in question-and-answer session sharing insights about her leadership role at the Federal Reserve, her experiences as a voting member of the Federal Open Market Committee and her perspectives on the evolving economic landscape in a Fed Listening Tour event, Houston, TX (Text and livestream available. Audience Q&A expected);

1:25 p.m.: Fed Bank of Kansas City President Schmid (Non-Voter) speaks on the Federal Reserve, monetary policy and the economic outlook before the Federal Reserve Bank of Kansas City Economic Forum, Grand Island, NE. (Embargoed text and livestream available. Audience Q&A expected);

7 p.m.: Federal Vice Chair Jefferson (Voter) speaks on “Navigating Economic Shocks” in conversation at Stanford University, Stanford, CA ; Livestream at https://stanford.zoom.us

-ATAI +34% (confirms to be acquired by Lilly for $6.75/shr plus CVR worth up to $2.50/shr to advance treatment-resistant depression therapies)

-DSGR +25% (agrees to be acquired by LKCM Headwater for $35.00/shr in cash)

-GHRS +15% (higher in sympathy with ATAI)

-MAN +14% (earnings, guidance)

-CMPS +8.5% (reports Phase 2 COMP360 support analysis in PTSD; higher in sympathy with ATAI)

-ABUS +7.8% (files three international lawsuits against Pfizer/BioNTech over COVID-19 vaccine LNP patents; receives $178M from Moderna, plans up to $230M share repurchases)

-UNH +6.8% (earnings, guidance)

-ARTL +6.4% (reports nonclinical ART26.12 data in osteoarthritis pain)

-JBHT +6.1% (earnings, color)

-HUM +5.4% (higher in sympathy with UNH)

-ABT +3.8% (earnings, guidance; investigating cyber incident in Cancer Diagnostics business)

-BIDU +2.4% (seeking dual-primary listing in Hong Kong)

Downside:

-ASTS -13% (prices $1B 1.625% convertible senior unsecured notes due 2034 at $79.57/shr conversion price)

-FEIM -11% (earnings, color)

-TSM -4.3% (earnings, guidance)

-UAL -3.6% (earnings, guidance)

-ETSY -2.7% (BTIG Cuts ETSY to Neutral from Buy)

-GE -2.6% (earnings, guidance)

-LULU -2.0% (Truist Cuts LULU to Sell from Hold, price target: $94 from $115)

Subscriber Comment of the Day: Rolf Is on the ‘Money’

Rolf expresses himself and a view on hyperscaler ROIC more precisely than I ever could:

Dougie Kass 35m ago

uber guy on cnbc talking about commoditization of ai – a concern of mine as it relates to adequate roic on large hyperscaler ai spend

ReplyShare

rolf thrane just now

AI hyperscaling resembles other capital-intensive industries where the only defensible advantage is money—which, by most schools of economic thought, is not a competitive advantage – actually the opposite . Industries requiring enormous capital investment generally produce low returns on capital: airlines, automobiles, shipping, and so forth.

rolf thrane

7m ago

strong ROI rule 1) No competition, rule 2) Low to moderate capital intensity, rule 3) remember rule 1 and 2

I am surprised that there was very little discussion in the business media yesterday that the PPI (printed yesterday morning) is about 200 basis points higher than the CPI (printed the day before).

This means that companies’ input costs are higher than they are charging — and margins are threatened.

This is contrary to the core and foundational bullish investment case that margins will continue to expand.

Expect the Massive Performance Schism Between Hyperscalers and Semis to Narrow Soon

* This divergence has defined the market over the past several weeks…

The divergence between hyperscalers (from the bottom left to the upper right) and memory/semis (from the upper left to the bottom right) is growing extreme.

Over the last two days I have been reducing my high-beta, high-tech short basket (principally of memory and semi stocks).

From yesterday:

The Casino Is Open

The imbalance and spastic relationship between memory/semis (weak) vis-à-vis hyperscalers (strong) continue today.

Like a baby splashing in a bathtub, the situation is changing daily.

Tough to evaluate and trade on an intraday basis.

I am long (AMZN), (GOOGL) and (MSFT) and I am short a basket of semis and memory stocks (e.g (MU) (SNDK) (INTC) (AMD) (AMAT).

Positions: Long AMZN VS GOOGL VS MSFT VS; short MU VS SNDK VS INTC VS AMD VS AMAT VS

South Korea launched 16 single-stock leveraged and inverse ETFs tracking Samsung and SK Hynix on May 27, 2026, and within a month, they had grown to ~$9.1 billion in assets.

I will admit I’m continually shocked how little anyone is discussing OpenAI’s direct risk to the future of Oracle – especially as Oracle stock is so crucial to the paramount/WBD closing in September! https://t.co/qKkWv5ctEz

I will admit I’m continually shocked how little anyone is discussing OpenAI’s direct risk to the future of Oracle - especially as Oracle stock is so crucial to the paramount/WBD closing in September!

Ed Zitron

@edzitron

OpenAI's collapse threatens to destroy Oracle, with its credit rating recently downgraded by S&P Global specifically because it's building $340bn+ of data center capacity for a company that can't afford them, and nobody else exists to pay otherwise.

wheresyoured.at/the-openai-bub…

🚨KOREAN RETAIL INVESTORS ARE GETTING WIPED OUT:

South Korea launched 16 single-stock leveraged and inverse ETFs tracking Samsung and SK Hynix on May 27, 2026, and within a month, they had grown to ~$9.1 billion in assets.

Seoul-listed SK Hynix 2x long leveraged ETF, the Show more