Thursday’s After-Hours Advancers and Decliners

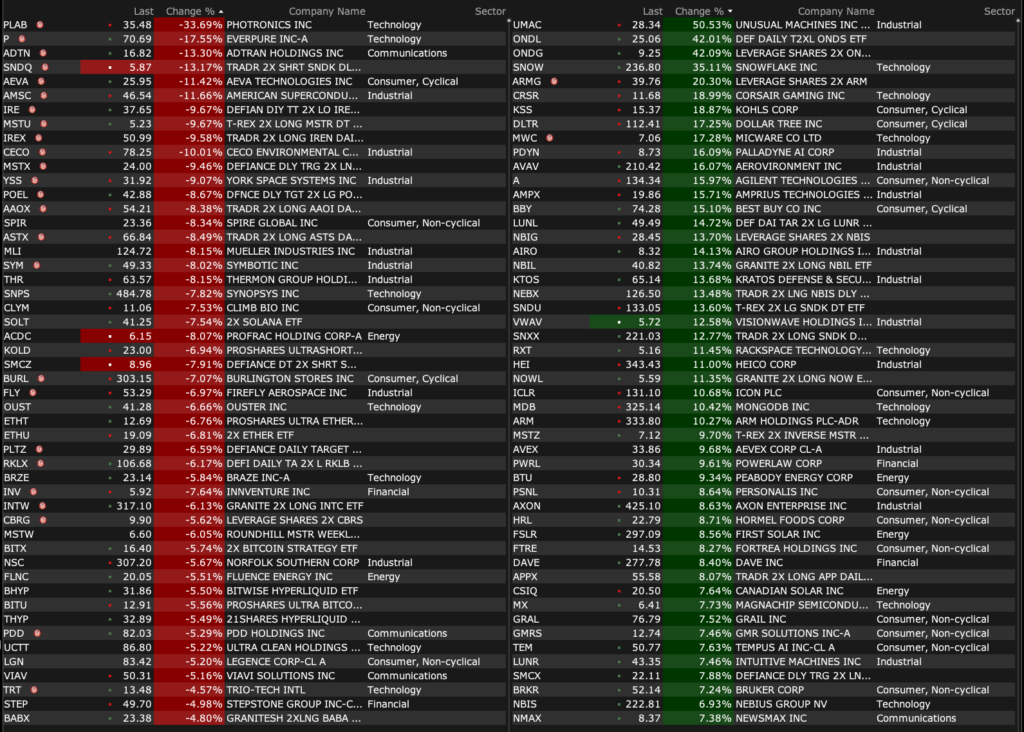

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · May 28, 2026, 4:40 PM EDT

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · May 28, 2026, 4:40 PM EDT

Closing Volume

– NYSE volume 6% below its one-month average

– NASDAQ volume 2% below its one-month average

– VIX index: down 3.62% to 15.70

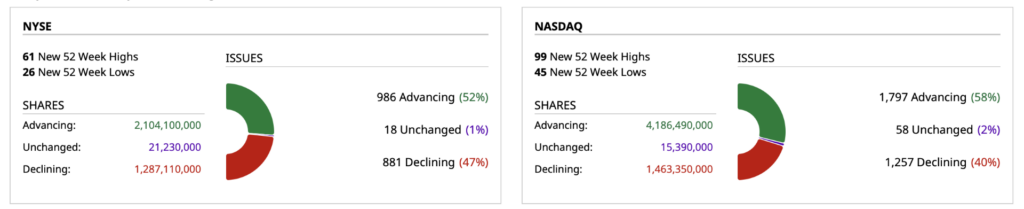

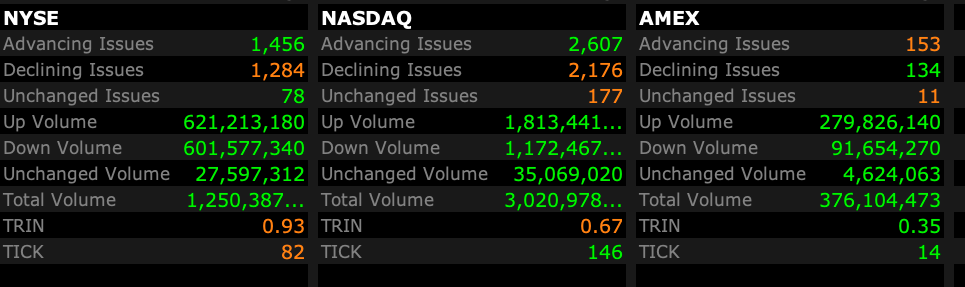

Breadth

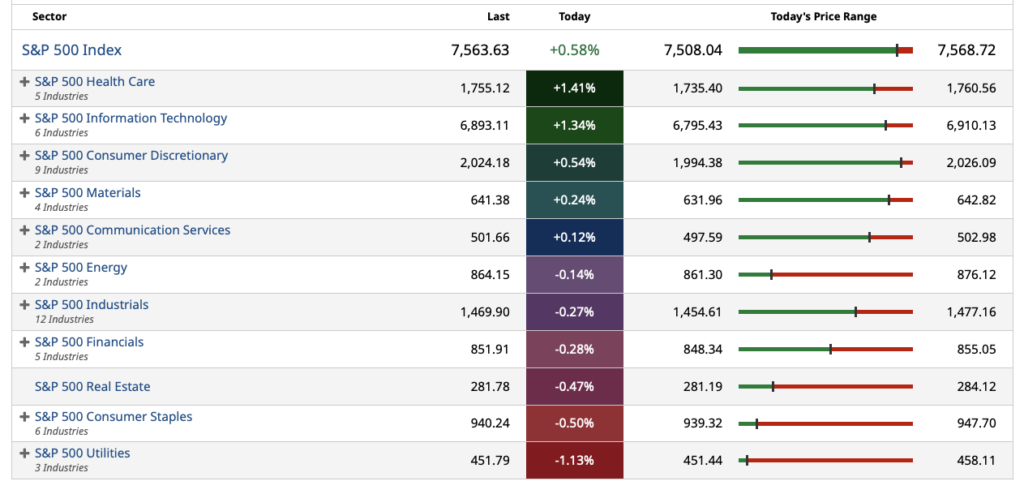

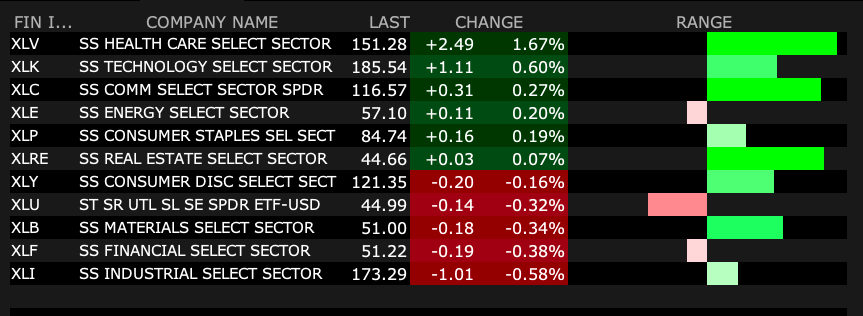

S&P 500 Sectors

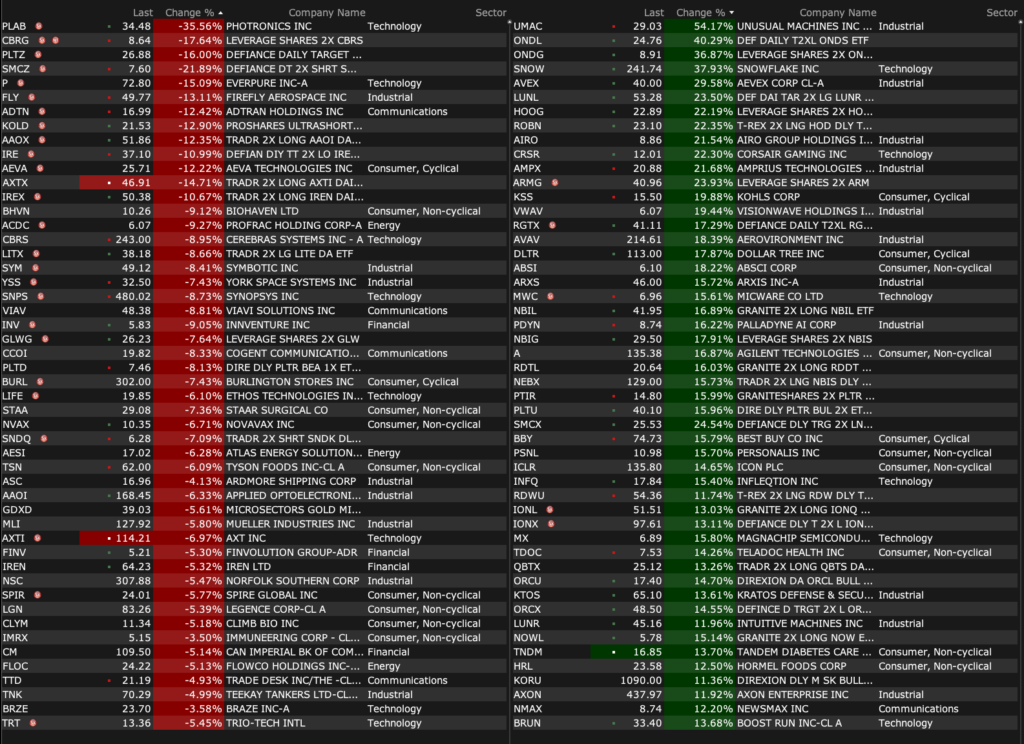

% Movers

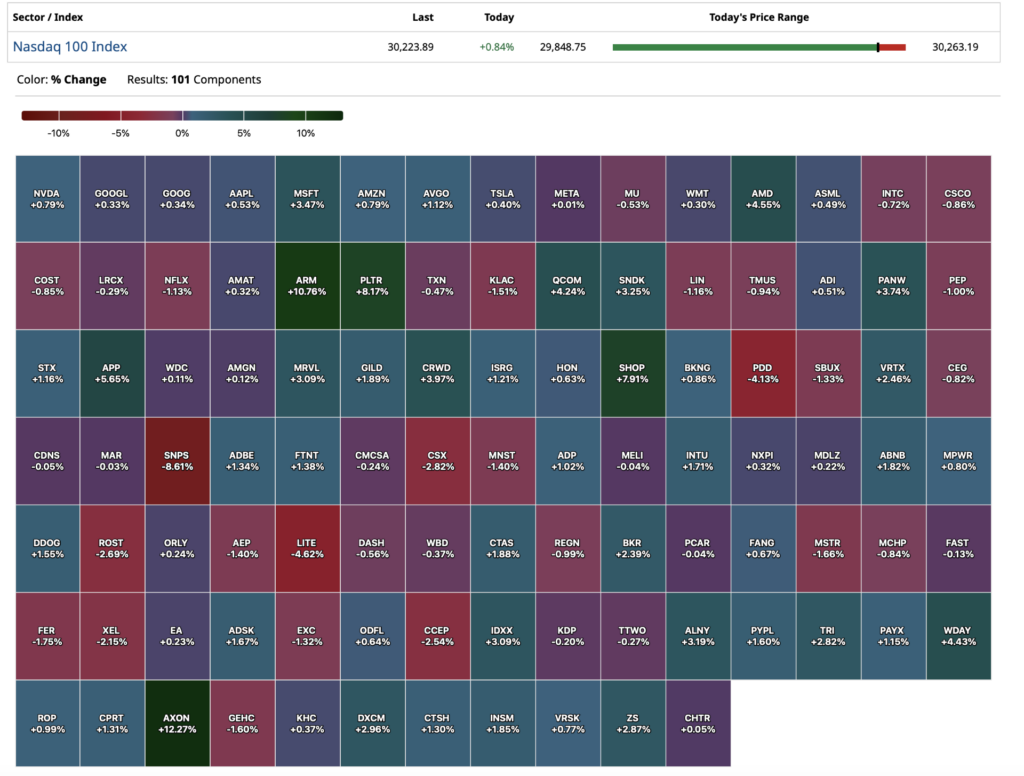

Nasdaq 100 Heat Map

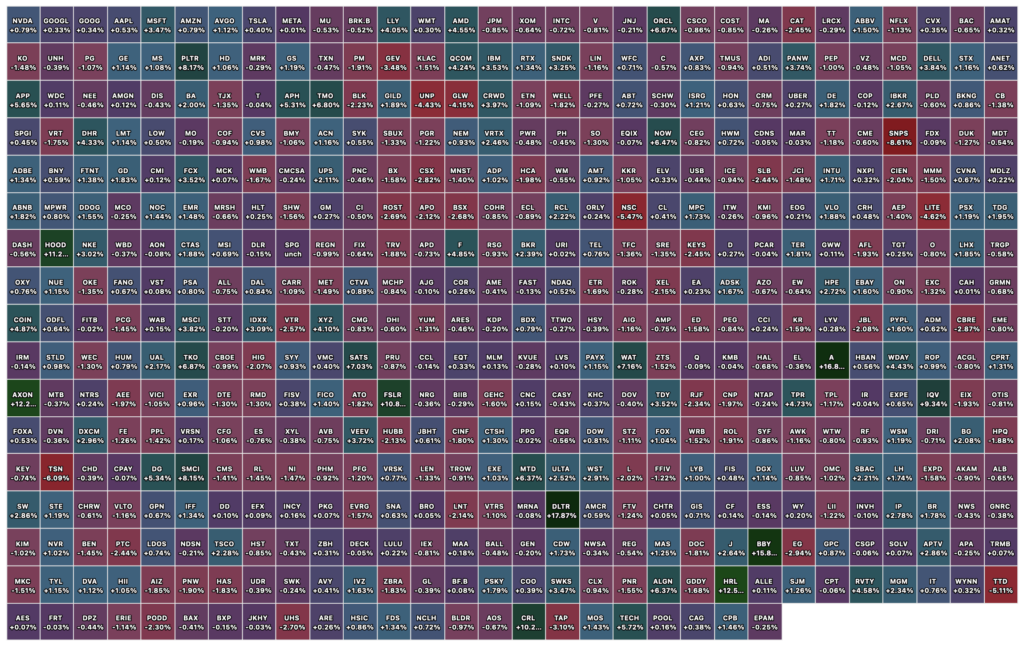

Closing S&P 500 Heat Map

Position: None

BY Doug Kass · May 28, 2026, 4:28 PM EDT

BY Doug Kass · May 28, 2026, 3:47 PM EDT

Break in.

Iran denies the Axios peace deal story from this morning.

Position: None

BY Doug Kass · May 28, 2026, 2:54 PM EDT

I am moving toward a large index short position:

* SPY $754.04

* QQQ $734.94

Position: Short SPY (M), QQQ (M)

BY Doug Kass · May 28, 2026, 11:49 AM EDT

– NYSE volume flat to its one-month average;

– Nasdaq volume 9% below its one-month average;

– VIX index: down 1.78% to 16

Positions: None.

BY Doug Kass · May 28, 2026, 10:51 AM EDT

BY Doug Kass · May 28, 2026, 10:42 AM EDT

Stocks rip higher on an Axios report that a peace agreement (again) has been reached.

I am adding to my index shorts with s and p cash +27 handles:

* (SPY) $753.10

* (QQQ) $732.16

Positions: Short SPY M QQQ M

BY Doug Kass · May 28, 2026, 10:22 AM EDT

From Peter Boockvar:

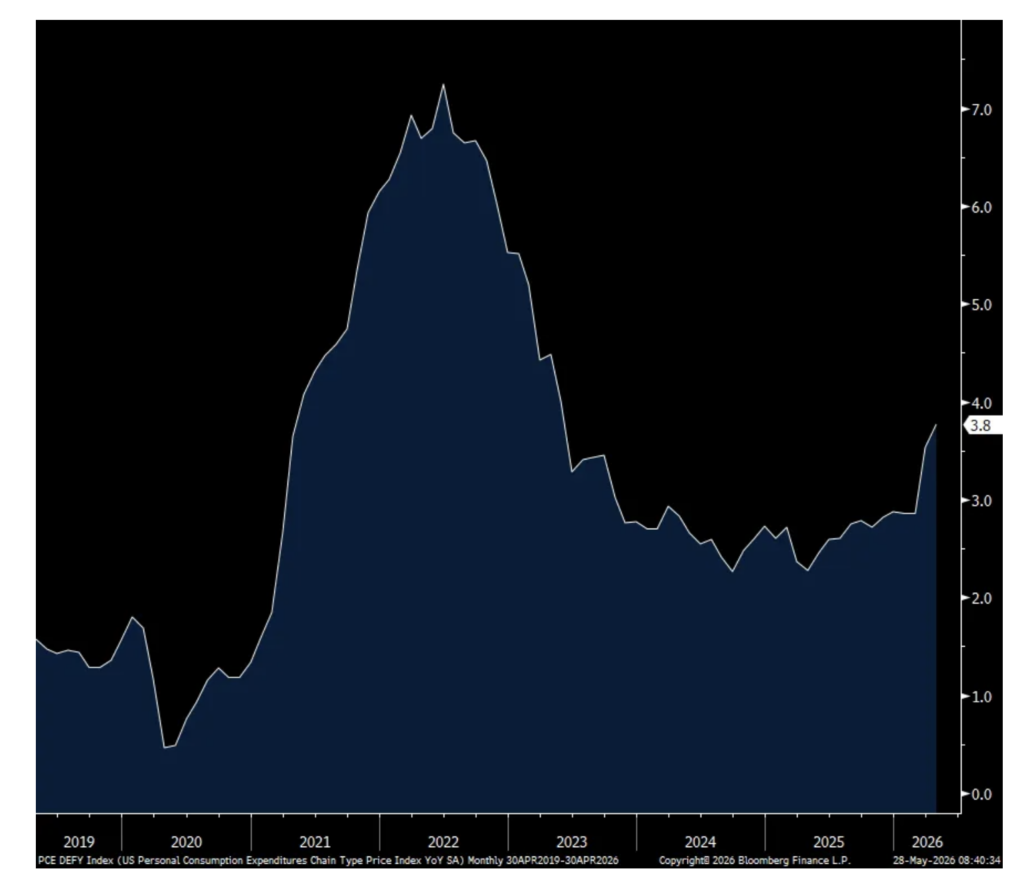

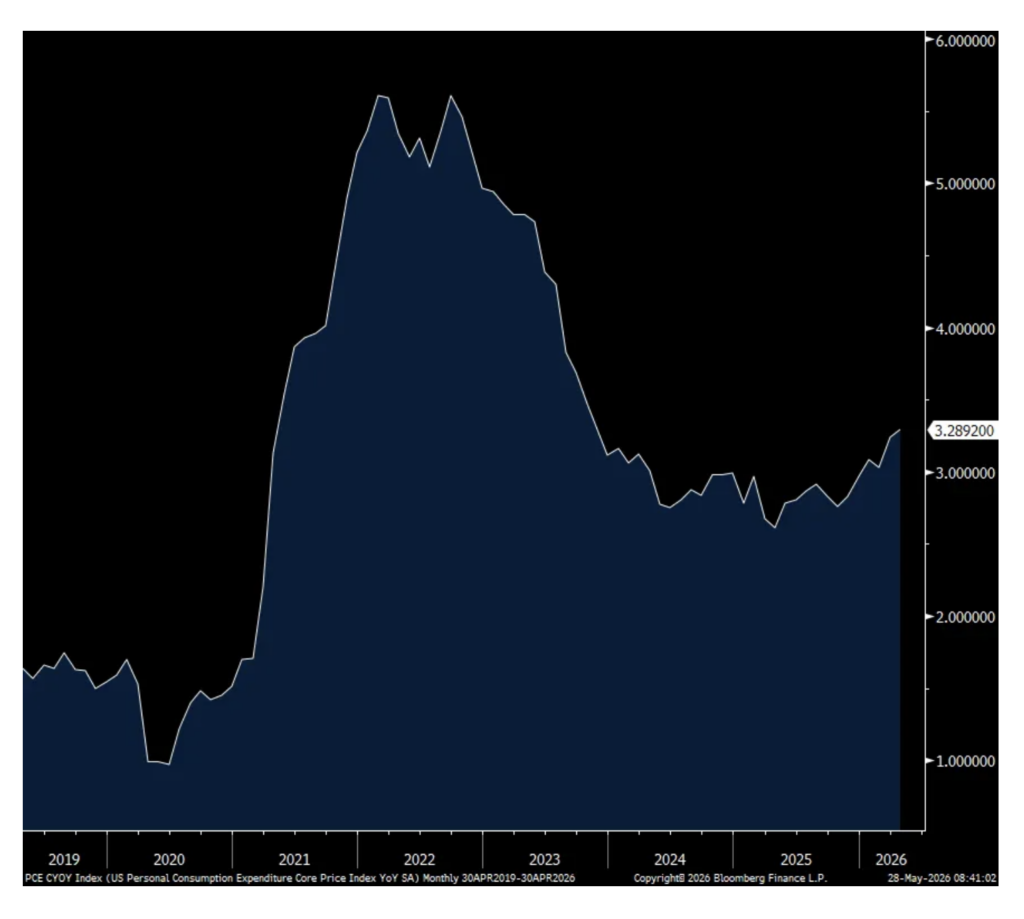

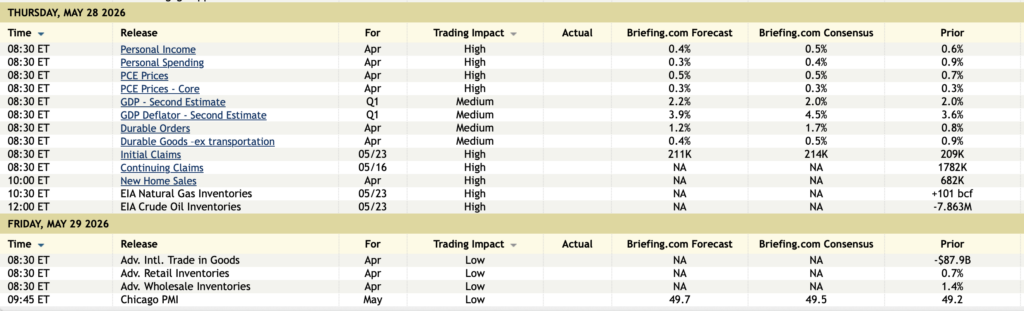

Headline PCE in April rose .4% headline and .2% core m/o/m, both one tenth below the estimate but due to rounding the 3.8% and 3.3% y/o/y gains were as forecasted. As expected, energy prices rose 18.3% y/o/y and food prices were up 2.5%.

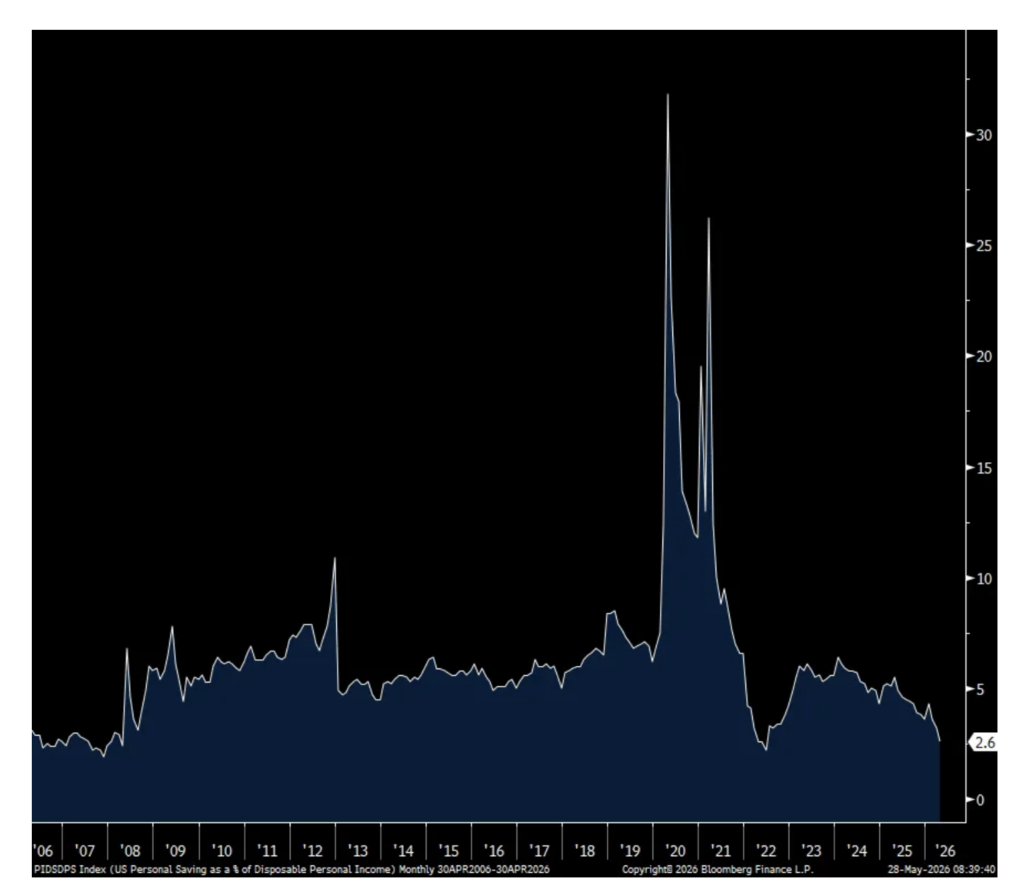

What really stands out in this April data was the big drop in the savings rate to just 2.6% from 3.2% in March, 3.6% in February and 4.3% in January. That matches the lowest level since June 2022 when it got down to 2.2% that month. Go back to 2007 the previous time it was under 2.6%.

Contributing to this was the no change in income growth m/o/m while spending rose .5% and .4% of that spending was inflation. The caveat though with the income drop was that it was mostly due to “The decrease in farm proprietors’ income” which “reflected a decrease in payments to farmers from the Farmer Bridge Assistance Program, which closed application submissions in mid-April.” Private sector wages and salaries, most importantly, rose .3% m/o/m.

Bottom line, inflation is again eating into REAL incomes and draining the savings rate. Also lowering the savings rate is higher stock prices for the upper income earner as that growing wealth is seen as a form of savings. And, the spending growth is mostly price, not volume.

After touching 4.50% again, the 10 yr yield backed off to 4.47%-.48% in response to the inflation, income and spending data.

PCE Headline y/o/y

PCE Core y/o/y

Savings Rate

Q1 GDP was revised lower to a gain of 1.6% from the first print of 2% and vs expectations of no change. Tweaks down in personal consumption and gross private investment were the main reasons. Final sales to private domestic purchases was revised just a hair lower to 2.4% growth from 2.5% initially.

For perspective, 150 bps of the GDP growth was from spending on ‘information processing’, ‘software’ and ‘R&D.’

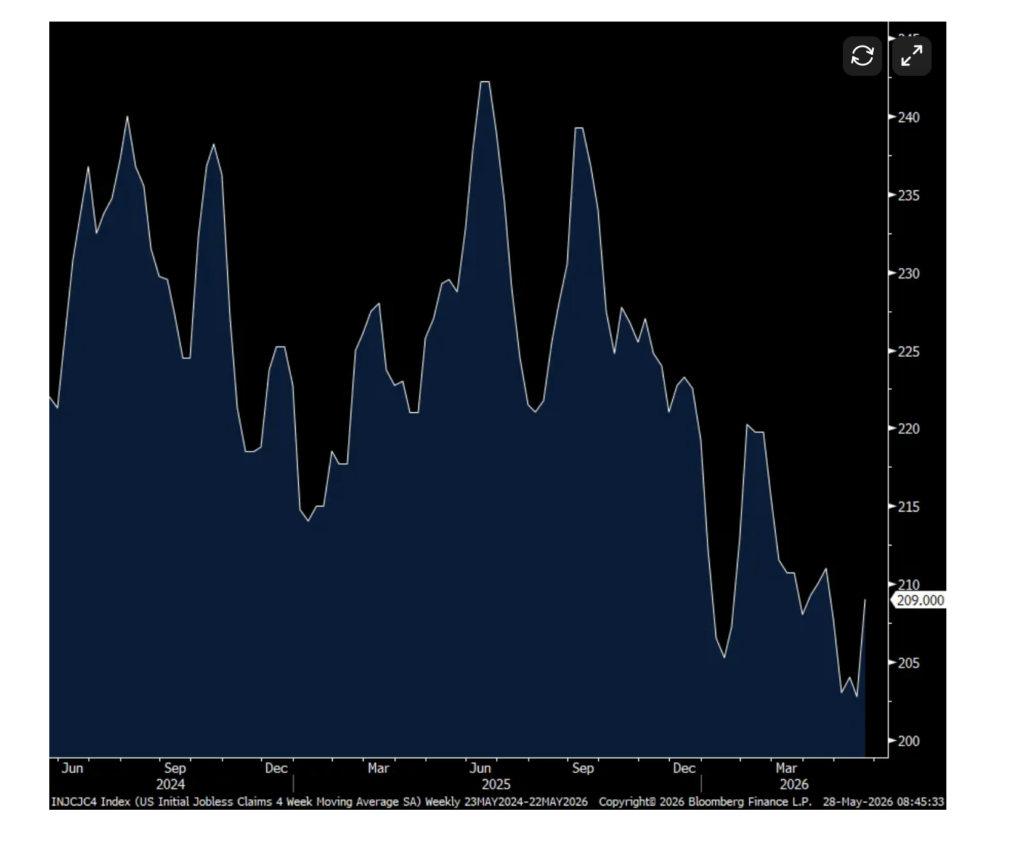

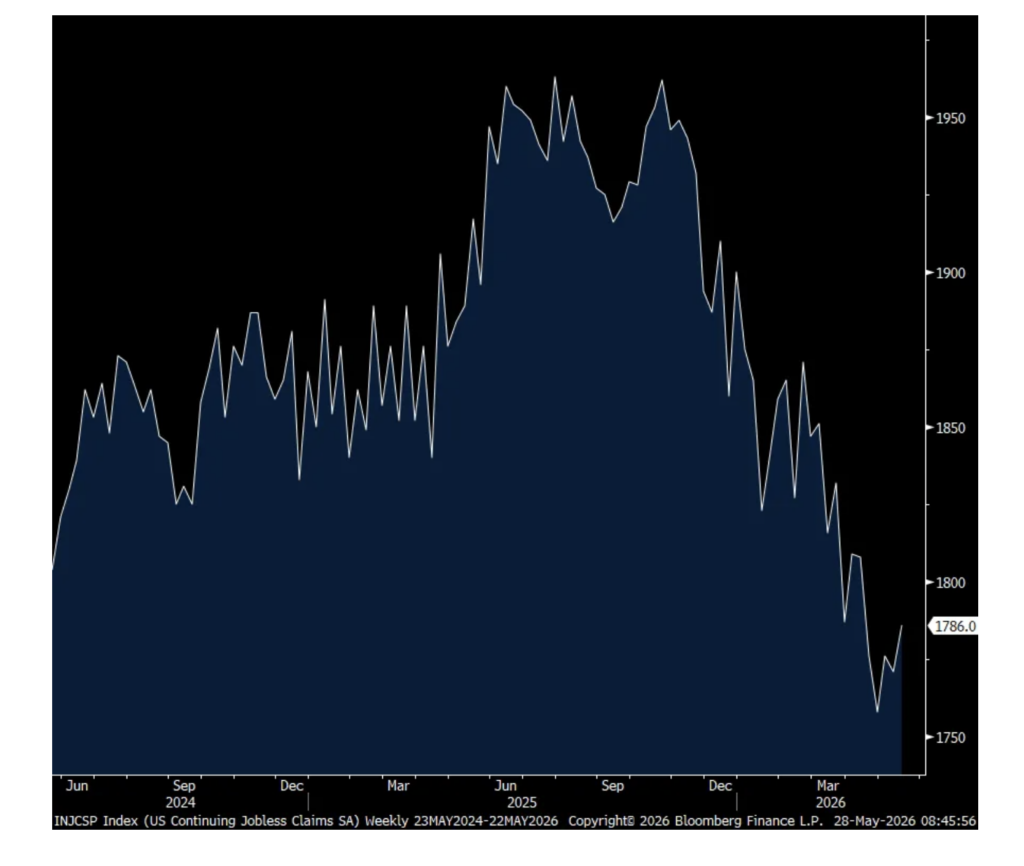

Initial jobless claims ticked up by 5k w/o/w to 215k and that was 4k above the estimate. The 4 week average moved up to 209k from 203k as a print of 190k drops out from 5 weeks ago. Continuing claims rose to 1.786mm as expected from 1.771mm but remaining below 1.9mm.

Overall, the bottom line continues to be the same with the slow pace of firing’s as measured here while continuing claims can be impacted by either the modest inflows of new filers, claims expiring, and/or people are finding new jobs.

4 week avg in Initial Claims

Continuing Claims

Core durable goods orders in April fell 1.1% m/o/m vs the expected gain of .4%, partly offset by a 5 tenths upward revision to the blockbuster month seen in March when they rose 3.9%.

Notwithstanding the orders pullback after the strong March, strength in anything touching the data center construction continues to be robust with an 18.8% y/o/y rise in computers/electronics, 5.8% increase in electrical equipment, 11.6% gain in machinery and you can’t build anything without metals as primary metals orders rose 13.6% y/o/y and fabricated metals were higher by 10%.

Core shipments, which get plugged into GDP, were about as expected.

Positions: None.

BY Doug Kass · May 28, 2026, 9:49 AM EDT

From Peter Boockvar:

I know we’re hearing the monetary policy and growth and inflation thoughts from a variety of Fed members, such as Kashkari, Goolsbee, Cook and Jefferson today (all basically in wait and see mode for now with a bias to hike if energy cost pressures spread) but I’m really only interested at this point in what Kevin Warsh has to say and we’ll hear him on June 17th at his first press conference. Where is his head at currently? What’s the plan with the balance sheet? To what extent does he want to look past the rise in energy prices on the belief that the Strait will eventually reopen?

Ahead of the April PCE data today at 8:30am est, this quote from a company in the food/drink business I saw going thru the Dallas Fed’s services index out yesterday that printed -7.7:

“Over the past 30 days, we have seen a surprising number of price increases from many of our suppliers, including green coffee, cups and bags. We are seeing fuel surcharges of 50 percent for coffee imported to New Jersey and 26 percent for Port of Houston. This is a material increase. We’ve also seen cost increases of over 10 percent for some required supplies, such as cups and bags and the like. So our concern is that input prices are far outpacing official inflation, and outpacing our pricing elasticity as well. Profitability has suffered in April and thus far in May. We’ve also seen some same-store decreases in traffic volume. Around 35 percent of our cafes have seen decreases of 2 percent to 6 percent, which is quite abnormal for our business. We tend to be very resilient, as our consumer is generally amongst the more affluent as our product is considered an affordable luxury. So in some instances we may be seeing a decrease in demand due to general consumer-spending declines. Time will provide a more complete picture.”

For others, dallasfed.org/research/surveys/tssos/2026/2605#tab-comments

Also with respect to inflation, Apartment List released its May rental data and new rents (as opposed to renewals) rose .5% m/o/m, up for a 4th straight month “as the market enters the busy summer moving season” but still down 1.5% y/o/y. Also of note, the vacancy rate is now ticking back down for the first time in “over four years”, to 7.2% after peaking at 7.3% in February which was the highest since at least 2017.

Austin remains the weakest market because of oversupply, down 5.1% y/o/y while San Francisco is seeing the fastest rent gains, of 6.3% y/o/y. As said here many times, most of the rent declines have been in the overbuilt sunbelt states while “many markets in the Northeast, Midwest, and parts of the West Coast continue to see prices trend up.”

With respect to renewal rates, not measured in this monthly survey, from what I heard from a bunch of multi family REITS, they are up anywhere between 2-4%. I continue to expect that by the end of 2026 and more into 2027, that excess sunbelt inventory will be absorbed and new rental trends will inflect higher again, further complicating the inflation situation as home buying still remains expensive for first time interested buyers.

To what some companies said on their earnings calls.

From DICK’s Sporting Goods, down 6% yesterday because of muted guidance but the business of sports in all facets remains healthy:

DICK’s comps rose 6% “with growth in average ticket and transactions…We saw more athletes purchase from us with more frequent purchases, and they spent more each trip compared to the prior year. We continue to see a healthy consumer across income demographics, with no signs of trading down alongside particularly strong engagement from our younger athletes. Our consumer is really responding to newness and innovation, which is showing up throughout the DICK’s business with broad based growth across footwear, apparel, and hardlines.”

In terms of guidance, “we continue to expect higher comps in the first half driven in large part by the timing of the World Cup.”

US Foot Locker comps were up by 6.4% but up 1.4% for all of North America.

From Monro, a tire and auto service provider, and a stock we own:

“We experienced a 5% decline in tire units during the quarter, which we believe aligns with broader industry trends. Our tire category was pressured as consumers continued to defer spending in higher ticket categories and gravitated toward lower cost alternatives. Further, fiscal February presented additional challenges when severe winter weather across our geographic footprint forced temporary store closures and significantly reduced customer traffic.”

“And while our business rebounded in April, with comp stores sales that were up almost 1%, our May month-to-date comps are down approximately 3%. We believe the primary driver is that certain customers are feeling increased pocketbook pressure as a result of recent increases in gas prices, as well as other related costs.”

They have also seen a trade down to tier 4 tires (lower quality but cheaper) from the best in tier one “and the price differential across tiers is typically $20-$30 up and down the assortment.” But, they are also seeing strength in tier 1 tires and highlights the bifurcation seen with the consumer.

Bath & Body Works saw its stock jump by 10% even with a sales decline as they still exceeded expectations. They said of note:

“Underlying business trends remain pressured and largely consistent with the past several quarters.”

Abercrombie & Fitch saw its stock pop by 9% yesterday. From them:

“We’re seeing good progress against our company priorities so far in 2026, led by net sales growth across brands in the Americas and other key markets like the UK.”

“In EMEA, continued growth in the UK was more than offset by declines in the Middle East and other European markets as the regional conflict ramped up, driving EMEA sales down 10% for the quarter.” APAC was strong with a 15% comp gain. Comps in the Americas rose 1%.

Denim continues to do well, “we are not seeing any change in the demand for denim. We’re actually excited about what we’re seeing. There’s some exciting trend happening within denim.”

They applied for some tariff refunds and expect lower tariffs this year but “we expect that relief to be offset by elevated freight costs and continued investments in marketing and stores.”

PayPal spoke at a Bernstein conference yesterday and said this of note:

“From a vertical perspective, we have seen a slowdown in the travel space, especially in Europe. And also from a regional perspective, Europe is the region where we have seen a slowdown of overall activity. When we look at monthly evolution, May was stronger than April, but in line to the expectations that we were having.”

To some tech earnings.

From HP, down slightly pre market as they try to manage higher costs:

“In personal systems, revenue grew 13% y/o/y, with strong growth in both commercial and consumer. This includes continued momentum in AI PCs, which increased from more than 35% to 44% of our shipment mix in the quarter, as well as continued strength in advanced compute solutions and workforce solutions.”

“In print, revenue was flat y/o/y in a competitive market, as expected.”

“Turning to the external environment, we continued to navigate a challenging supply and cost environment, while remaining focused on disciplined execution. In Q2, as anticipated, memory and storage costs increased sequentially. We expect this trend to continue in the second half of 2026, with costs increasing in fiscal Q3 and Q4.”

“In addition, we also anticipate broader inflationary pressures beyond memory and storage, including oil prices and their downstream effects.” And they are doing their best to mitigate these headwinds.

From Salesforce, down modestly pre-market on muted guidance and a company certainly at the center of the AI software disruption debate:

Agentforce is their pushback against irrelevance in terms of their software business but it’s still modest in size. “I think we’re going to talk about how we processed 28.6 trillion tokens, up 152% q/o/q, no greater example of the tremendous adoption of these new agentic products by our customers and how we’ve converted those into 3.8 billion Agentic Work Units.”

“Agentic AI, well, it’s the biggest growth opportunity for our customers, for us at Salesforce.”

Snowflake on the other hand is skyrocketing by almost 40% as they seem to be winning in software.

Marvell Technologies stock has more than doubled this year but trading down after earnings as I think people were looking for more with their guidance with already high expectations. “We are seeing strong demand and exceptional bookings across our entire data center portfolio.”

The only data point of importance overseas was the May Eurozone Economic Confidence index which rose a touch to 93.5 from 93.2 which was the lowest since 2020. This was at 97.9 in February right before the Strait was closed. The internals were mixed m/o/m with a rise in services and consumer confidence, while manufacturing, retail and construction declined.

The Bank of Korea kept its 7 day repo rate unchanged at 2.5% as expected but signaled they are going to hike soon. The Governor said “I believe a convincing case could certainly have been made even for raising rates at this meeting.” Yields in Korea rose in response.

Eurozone Economic Sentiment

Finally with stock market sentiment, I see it in no man’s land. In the II data, Bulls fell to 45.3 from 48.1 while Bears rose 1.5 pts m/o/m to 22.6. While still a wide spread of 22.7, it’s far from the extreme of 40+. The AAII survey which jumps around like an EKG chart each week saw Bulls rise by 3.9 pts to 35.6 but they are still below Bears which sit at 41.9, down 1.7 pts w/o/w. The CNN Fear/Greed index is in the ‘Greed’ category but barely at 61. The only real extreme, and still worth noting, is the .83 read in the Citi Panic/Euphoria index and that is double the .41 Euphoria threshold.

Positions: None.

BY Doug Kass · May 28, 2026, 9:36 AM EDT

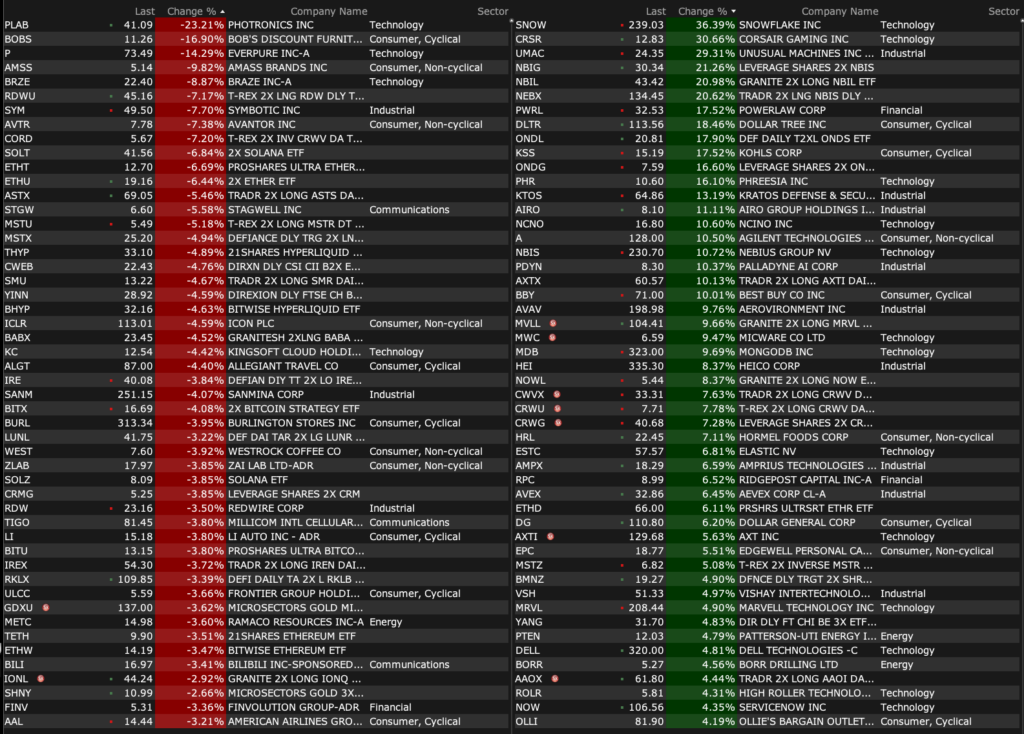

-SNOW +37% (earnings, guidance)

-CRSR +32% (Elgato brand is bringing MCP support to Stream Deck; Starting with NVIDIA G-Assist, AI tools and agentic workflows can now execute actions on a user’s system )

-UMAC +28% (said to be among companies linked to govt deals, amid ties to Donald Trump Jr)

-RCAT +18% (Trump Administration is in discussions to fund US drone companies)

-DLTR +16% (earnings, guidance)

-KSS +16% (earnings, guidance)

-NCNO +11% (earnings, guidance)

-A +10% (earnings, guidance)

-BBY +10% (earnings, guidance)

-NBIS +9.7% (Situational Awareness LP (Aschenbrenner) discloses 5.6% passive stake)

-ONDS +8.5% (Trump Administration is in discussions to fund US drone companies)

-DOO +7.9% (earnings, guidance)

-HRL +6.7% (earnings, guidance)

-DSX +5.4% (earnings)

-MRVL +3.9% (earnings, guidance)

-CZR +2.1% (confirms to be acquired by Fertitta Entertainment in all-cash $31.00 per-share deal)

-XPEV +2.0% (earnings, guidance)

-PLAB -21% (earnings, guidance)

-SIDU -18% (prices $100M registered direct offering at $5.08/shr)

-P -14% (earnings, guidance)

-TTD -3.1% (Rothschild & Co Redburn Initiates TTD with Sell, price target: $11)

-BBW -2.6% (earnings, guidance)

-SNPS -2.5% (earnings, guidance)

BY Doug Kass · May 28, 2026, 9:24 AM EDT

Positions: None.

BY Doug Kass · May 28, 2026, 9:12 AM EDT

With the reversal from the early morning lows I am adding to my index shorts:

* (SPY) $750.54

* (QQQ) $729.72

Positions: Short SPY M QQQ M

BY Doug Kass · May 28, 2026, 9:02 AM EDT

Positions: None.

BY Doug Kass · May 28, 2026, 8:58 AM EDT

8:55 a.m.: Fed Bank of New York President Williams (Voter) gives keynote before the Reykjavík Economic Conference organized by the Central Bank of Iceland and the Center for International Macroeconomics at Northwestern University, Reykjavik, Iceland (Text and moderated Q&A expected. Livestream available);

10:15 a.m.: Fed Bank of St. Louis President Musalem (Non-Voter) speaks on the U.S. economy and monetary policy before the Reykjavik Economic Conference 2026, Reykjavik, Iceland (Text anticipated. Moderated Q&A follows. Virtual option available);

3:00 p.m.: Fed Bank of Richmond President Barkin (Non-Voter) participates in moderated fireside chat before the “Leading with AI: Building Trust and Powering Growth” conference hosted by the Johns Hopkins Carey Business School, Washington, DC (No text. No livestream)

Economic Calendar

Positions: None.

BY Doug Kass · May 28, 2026, 8:33 AM EDT

Position: None.

BY Doug Kass · May 28, 2026, 8:22 AM EDT

“Welcome to “What Are We Doing” (WAWD), the Substack newsletter where Wall Street outsiders—Danny Moses, Vincent Daniel, and Porter Collins, famously portrayed in “The Big Short” pull back the curtain on markets and investing.”

– Danny, Vinnie and Porter

There are few smarter and contrarian investors than Danny Moses, Vincent Daniel and Porter Collins.

Read on:

They Look at Me Like It’s Christmas and I’m Santa Claus

Position: Long MSOS (L), GLASF (VS)

BY Doug Kass · May 28, 2026, 7:15 AM EDT

This is a non-event, IMHO:

Position: None

BY Doug Kass · May 28, 2026, 6:50 AM EDT

This important post was delivered late yesterday afternoon.

I wanted to be sure you all saw it:

I am growing much more optimistic on the cannabis complex.

I plan to super-size (VL) my MSOS holdings and I plan to expand individual equity positions (with emphasis on GTBIF and VRNO).

I am doing so because:

* I am extremely confident that rescheduling of both medical and adult use (recreational) will pass in the next few months.

* I am confident that uplistings will soon follow.

* More relaxed custodian rules allowing for institutional purchases of the group.

* The recent debt refinancings have eliminated the frightening debt maturity cliff that some feared.

* Industry fundamentals (volumes and pricing) have stabilized.

* Expectations are very low.

* Massive absolute and relative underperformance over the last five years has created a long runway for appreciation.

* Upside reward is probably more than 5x downside risk.

Position: Long MSOS common (L) and calls (S), VRNO (S), GTBIF (VS)

BY Doug Kass · May 27, 2026, 4:33 PM EDT

BY Doug Kass · May 28, 2026, 6:40 AM EDT

Position: None

BY Doug Kass · May 28, 2026, 6:27 AM EDT

Position: None

BY Doug Kass · May 28, 2026, 6:04 AM EDT

The S&P Short Range Oscillator has grown more overbought at 1.62% vs. 0.74%.

Position: Short SPY (M), QQQ (M)

BY Doug Kass · May 28, 2026, 5:53 AM EDT

The AI numbers are starting to look very ugly. Even under "best case" assumptions, FT's own data shows Microsoft AI ROI at -9%, Google at -15%, Meta at -28%, Oracle at -35%. Only Amazon barely comes out positive. This is exactly why I keep comparing this to the dot-com era. Show more

The AI numbers are starting to look very ugly. Even under "best case" assumptions, FT's own data shows Microsoft AI ROI at -9%, Google at -15%, Meta at -28%, Oracle at -35%. Only Amazon barely comes out positive. This is exactly why I keep comparing this to the dot-com era. Show more

What's happening with NVIDIA? While stock market is hitting new highs, $NVDA is down over 11% in just 2 weeks, erasing over $630,000,000,000 from its market value.

overheard from a fortune 20 company - ceo asked for $1 billion in AI generated opex savings at the beginning of this year. the team as a result has spent $200 million on tokens trying to achieve those savings year-to-date, with minimal results other than some modest Cx savings Show more

The world's best, most enduring and most valuable companies all have one thing in common: dominant moats that secure long-term pricing power. AI is the exact opposite And yet, trillions of dollars in equity value now rest on the assumption that trillions of dollars in capital Show more

Chinese AI models are 90% to 95% cheaper than the American AI bubble models. And people still don’t understand what is happening. Look at DeepSeek, Kimi, Qwen, MiniMax and the rest of China’s AI stack. They are cheap, fast and useful enough for most real-world use cases. The

This looks like the beginning of the end for OpenAI and Anthropic. The Chinese AI wave did not just cut prices. It destroyed the entire funding logic behind the American AI bubble. If developers can move from thousands of dollars per month to a few dollars per week with 80% of Show more

I Went From $3,000/Month on Claude to $5/Week on DeepSeek And honestly? 80% of my work is identical. For the past two months, I was burning $3-5K monthly on Claude Code. Every idea from design to development to testing - full end-to-end automation, even simulating users to test

No one knows when this ends, but anyone with even a cursory understanding of history should know exactly how this ends

$EWY Seniors in South Korea are taking out record amount of margin loans to buy stocks. koreatimes.co.kr/economy/202605…