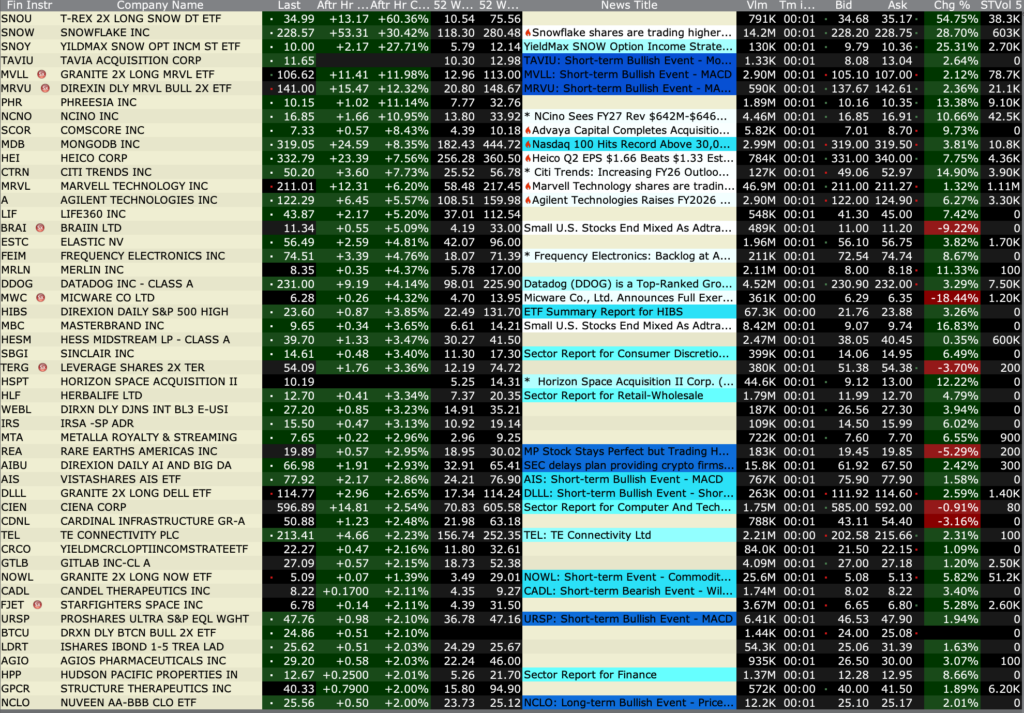

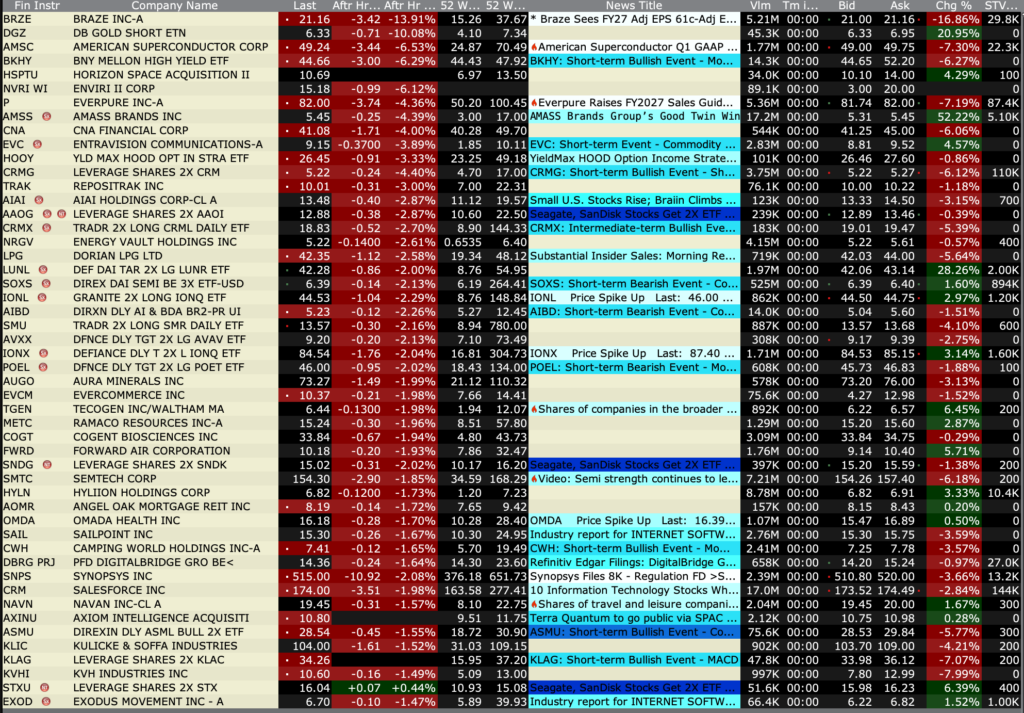

Wednesday’s After-Hours Advancers and Decliners

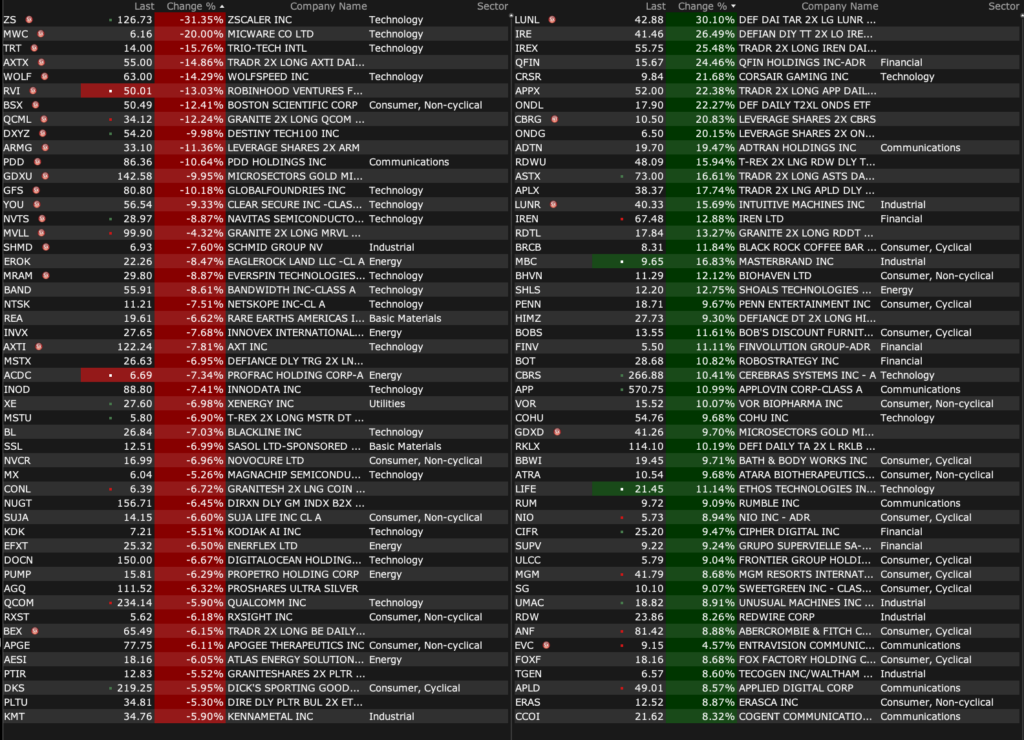

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · May 27, 2026, 4:40 PM EDT

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · May 27, 2026, 4:40 PM EDT

I am growing much more optimistic on the cannabis complex.

I plan to super-size (VL) my MSOS holdings and I plan to expand individual equity positions (with emphasis on GTBIF and VRNO).

I am doing so because:

* I am extremely confident that rescheduling of both medical and adult use (recreational) will pass in the next few months.

* I am confident that uplistings will soon follow.

* More relaxed custodian rules allowing for institutional purchases of the group.

* The recent debt refinancings have eliminated the frightening debt maturity cliff that some feared.

* Industry fundamentals (volumes and pricing) have stabilized.

* Expectations are very low.

* Massive absolute and relative underperformance over the last five years has created a long runway for appreciation.

* Upside reward is probably more than 5x downside risk.

Position: Long MSOS common (L) and calls (S), VRNO (S), GTBIF (VS)

BY Doug Kass · May 27, 2026, 4:33 PM EDT

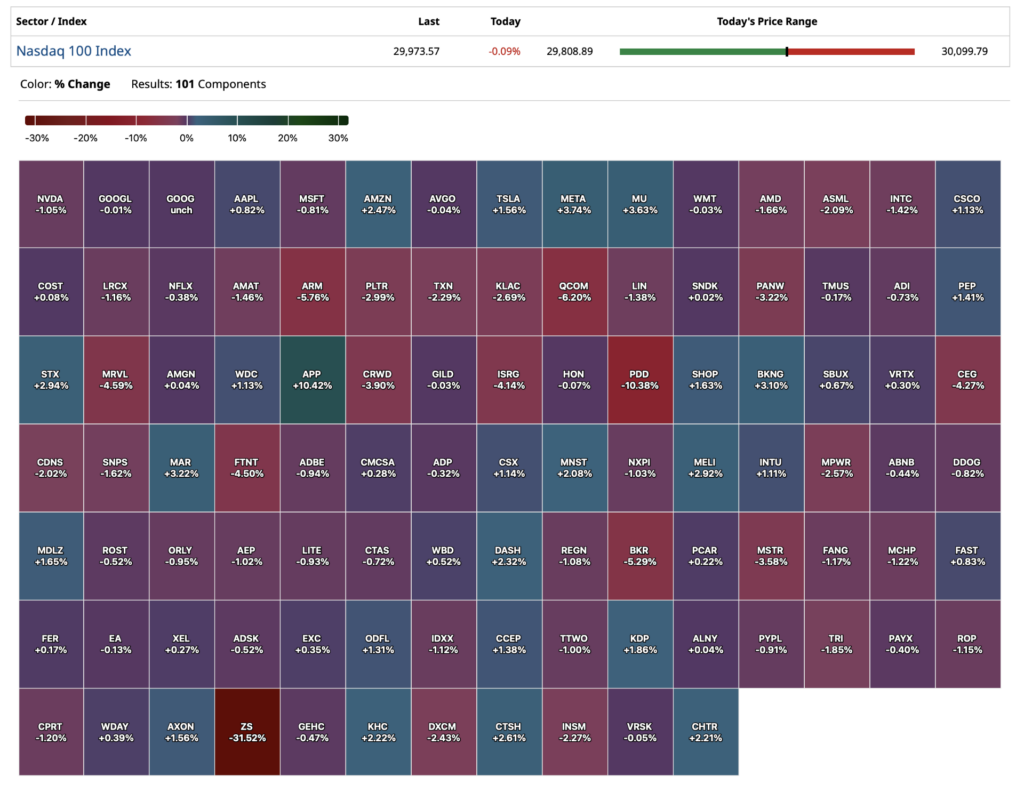

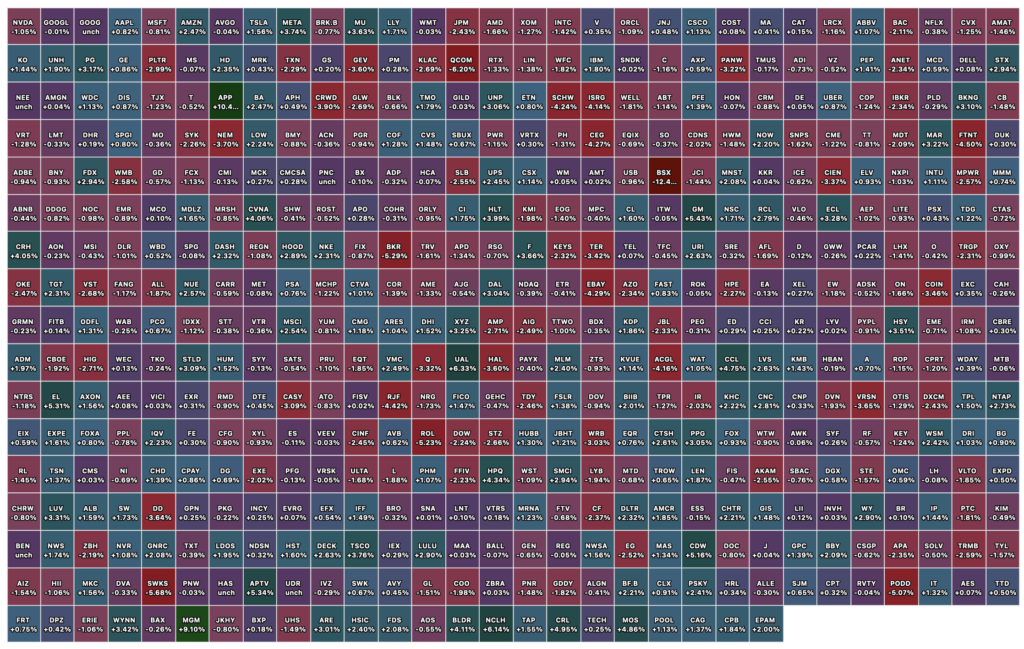

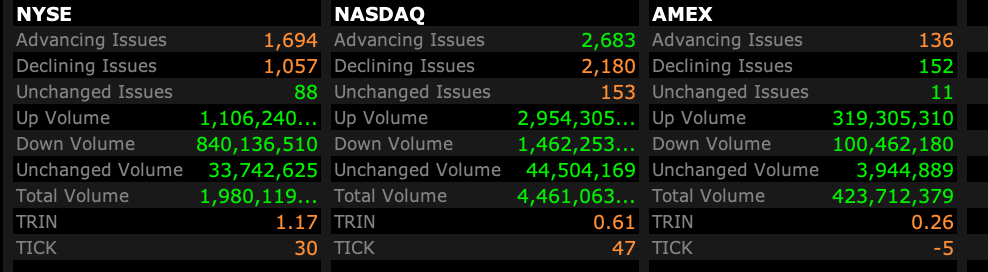

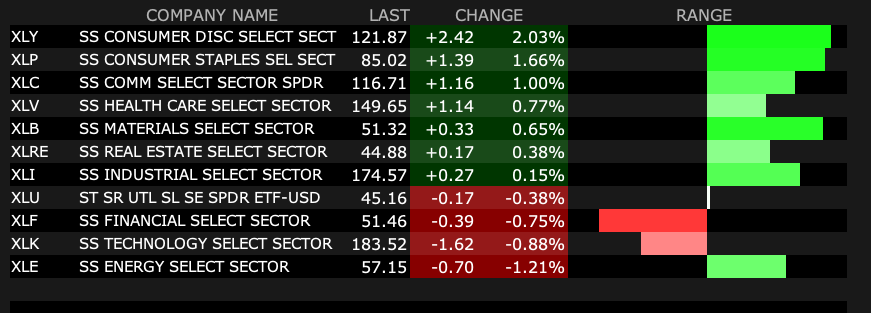

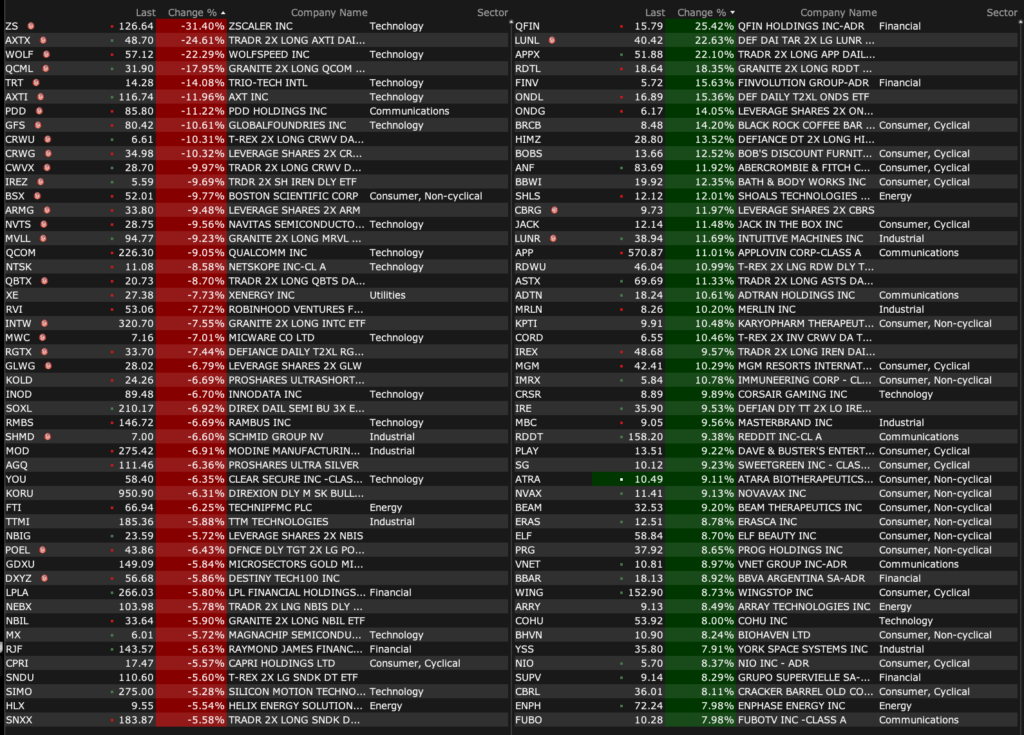

Closing Volume

– NYSE volume 4% above its one-month average

– NASDAQ volume 4% above its one-month average

– VIX index: down 4.06% to 16.32

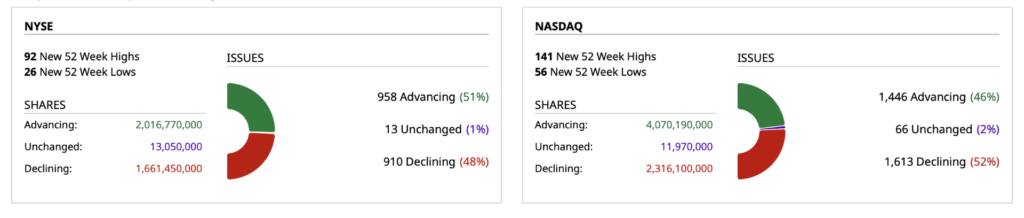

Breadth

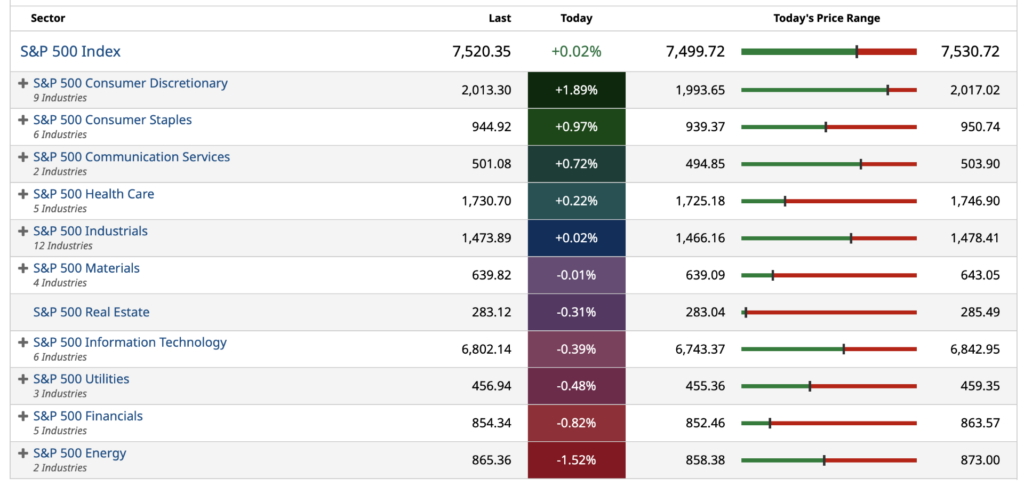

S&P 500 Sectors

% Movers

Nasdaq 100 Heat Map

Closing S&P 500 Heat Map

Position: None

BY Doug Kass · May 27, 2026, 4:24 PM EDT

Position: None

BY Doug Kass · May 27, 2026, 3:24 PM EDT

After the Close Wednesday 05-27-2026

Before the Open Thursday 05-28-2026

Position: None

BY Doug Kass · May 27, 2026, 3:10 PM EDT

With S&P cash +6 handles, I am expanding my index shorts:

* SPY $750.76

* QQQ $729.64

Position: Short SPY (M), QQQ (M)

BY Doug Kass · May 27, 2026, 2:35 PM EDT

Wolf Street howls about the “WTF AI Mania Chart of the Year.”

Position: None

BY Doug Kass · May 27, 2026, 2:00 PM EDT

I just finished a research call and I have another one at 1:15 PM.

I should be back in 45 minutes.

Position: None

BY Doug Kass · May 27, 2026, 1:35 PM EDT

Breadth

S&P 500 Sectors

% Movers

Position: None

BY Doug Kass · May 27, 2026, 11:59 AM EDT

I believe Nvidia’s share price is down every day since its earnings release.

The stock is down another five beaners this morning.

More Tales From Nvidia: A Lesson on Valuations of Cyclical Equities (Issue #197!)

Position: None

BY Doug Kass · May 27, 2026, 11:45 AM EDT

Covered some (MS) at $197.45 and I am putting those shares back short out at $200.55.

Positions: Short MS M

BY Doug Kass · May 27, 2026, 11:17 AM EDT

Adding to MSOS at $4.51.

Position: Long MSOS L

BY Doug Kass · May 27, 2026, 11:06 AM EDT

I have covered the balance of my speculative short package for a quick and good profit:

* (AMD) $487.27

* (MU) $893.58

* (SNDK) $1542.83

Positions: None

BY Doug Kass · May 27, 2026, 10:46 AM EDT

Dougie Kass

28m ago

Who is crazier:the long buyers of sndk, amd and mu the short sellers of the above

1ReplyShare

DDaveInKenya

27m ago

yes.

5ReplyShare

Positions: Short SNDK VS MU VS AMD VS

BY Doug Kass · May 27, 2026, 10:20 AM EDT

I am increasingly bearish.

I just sold out the balance of my three staples longs:

* (KMB) $101.92 (+$3.15)

* (PEP) $148.21 (+$2.51)

* (PG) $148.05 (+$5.01)

I plan to buy back these positions in a meaningful correction – if we ever get one!

Positions: None.

BY Doug Kass · May 27, 2026, 10:16 AM EDT

I covered this morning’s speculative package shorts (still there with what I started the day short, though!)

* (MU) $917.99

* (SNDK) $1576.55

* (AMD) $494.12

From earlier today:

I (unemotionally) added to my speculative short package in premarket:

* (MU) $972.02

* (SNDK) $1,632.11

* (AMD) $515.09

Given the volatility I will remain very small in these trading short rentals.

Again, this is not for homegamers – I am just being transparent.

Positions: Short MU VS SNDK VS AMD VS

BY Doug Kass · May 27, 2026, 8:54 AM EDT

BY Doug Kass · May 27, 2026, 10:02 AM EDT

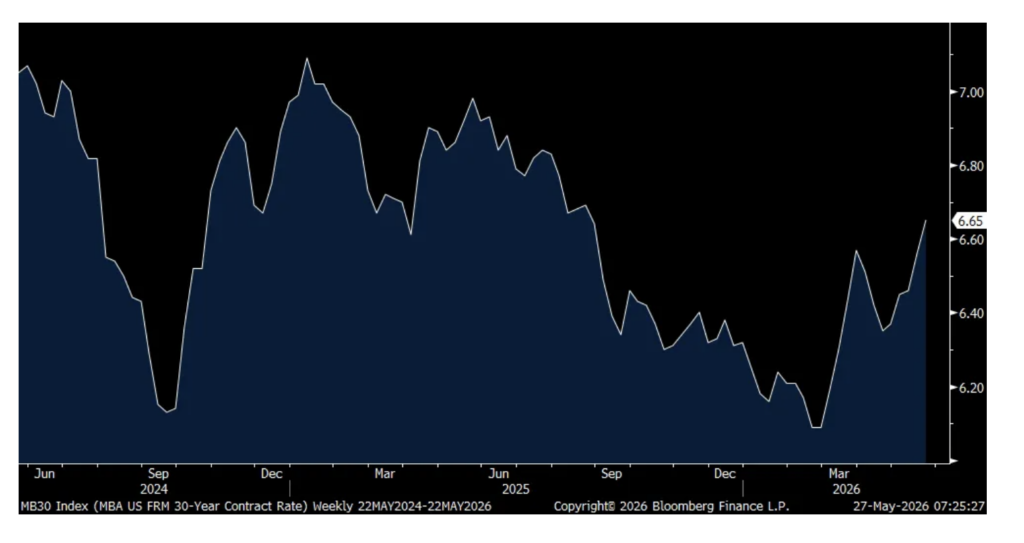

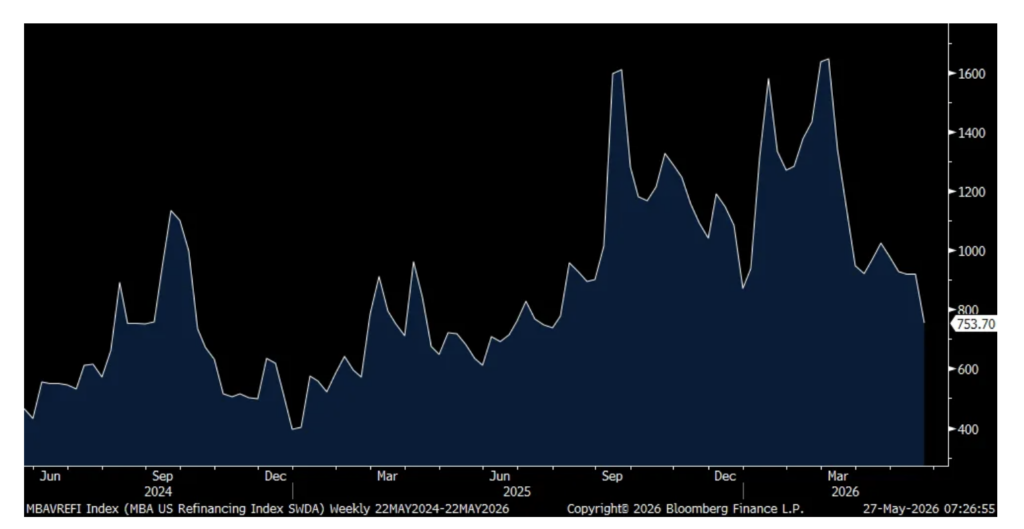

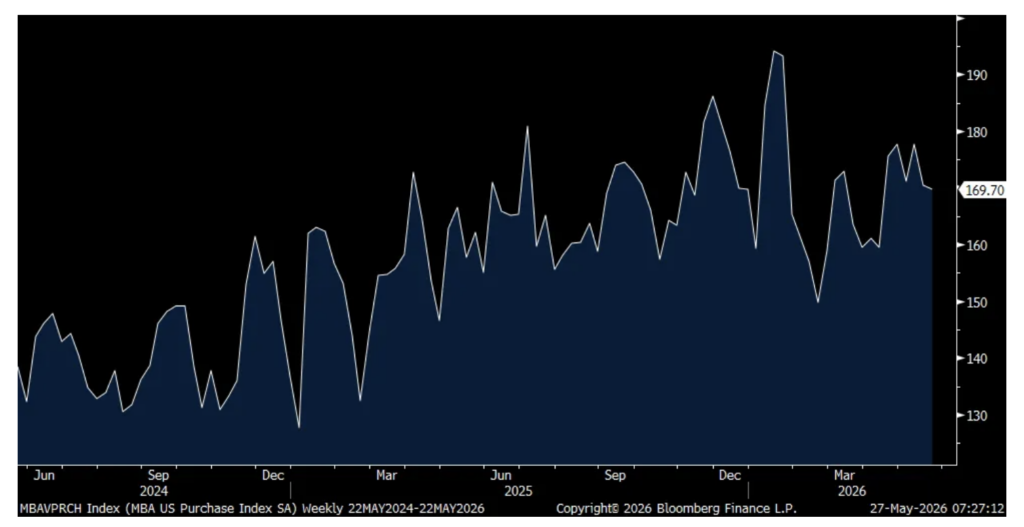

From Peter Boockvar:

The further rise in the average 30 yr mortgage rate to 6.65%, up 20 bps over the past two weeks and to the highest since last August, had an immediate impact on refi’s which fell 18% w/o/w to the lowest since last August. Purchase applications though were little changed but after falling by 4.1% in the week before.

In order to jump start housing transactions I believe we need lower prices and/or further increases in wage growth that exceed home price increases.

Average 30 yr Mortgage Rate

Refi Applications

Purchase Applications

Positions: None.

BY Doug Kass · May 27, 2026, 9:55 AM EDT

From Peter Boockvar:

There is not much new of substance this morning news wise but the drop in oil prices reflect continued optimism that we’re on the cusp of a deal and a full reopening of the Strait. The 10 yr US Treasury yield is down another 2 bps after dropping by 7 bps yesterday back below 4.50% and the 30 yr yield is back to 5%. While just round numbers, those seem to be the levels that many are currently focusing on.

Some relief was seen on the long end of the yield curve in Australia and Japan. Australia’s April trimmed mean CPI rose .3% m/o/m and 3.4% y/o/y as expected but no upside surprise. The 10 yr Aussie yield fell 5.5 bps overnight. Also in that region, the Reserve Bank of New Zealand kept its cash rate unchanged as forecasted at 2.25% but it was a 4-3 vote to do so with 3 wanting a rate increase. In Japan, they sold 40 yr government paper and the auction was pretty good with a bid to cover that was above the 12 month average. The 40 yr JGB yield fell for a 6th day, down another 3 bps and lower by 30 bps since last Tuesday.

In Europe, consumer confidence in France fell to the weakest since March 2023 so the sour consumer mood is not just seen in the US as inflation bites everywhere.

French Consumer Confidence

While all of the focus continues to be on memory chip producers such as Micron and the big ones in South Korea, and maybe this time is different with the structural changes in that business, maybe, another retailer expressed the consumer challenges in their business. AutoZone was down 9% yesterday and said this of note:

US comps grew 4.1% y/o/y with DIY up 2.2% “while our domestic commercial sales grew plus 10.4%” y/o/y. But, a lot of the growth was price and not traffic.

“With regards to inflation’s impact on DIY sales, we saw like-for-like same SKU inflation just north of plus 7% for the quarter, which contributed to our DIY average ticket being up plus 5.6%. The difference between the like-for-like inflation and ticket growth was attributable to product mix.” Traffic count for DIY was down 3.6%.” Commercial SKU inflation was up 7% too.

For the quarter they are in now, they expect SKU inflation around 4%. Tariffs are still apart of this.

“Coming into the quarter we were optimistic that our domestic store execution would drive sales growth for both retail and commercial. Regarding our plus 4.1% quarterly domestic same store sales, the cadence was plus 5% in our first four weeks, plus 4.5% in our second four weeks, and plus 2.9% over the last four week period of the quarter.”

“Now, let me address the last two weeks a little more specifically. Those two weeks were softer than the rest of the quarter with comps of plus 1.3%. This slowdown in sales was caused by unseasonably cool weather impacting our heat related categories which normally begin to ramp this time of year as summer heat begins to take hold. This affected both DIY and commercial.” Heat related would be AC for example.

“For the quarter, we felt we benefited marginally from higher than usual income tax refund season along with share gains and solid execution.”

They also have an international business and said “we remain cautious for this upcoming fourth quarter as the consumers in our international markets remain under pressure.”

The May Dallas manufacturing index was around the flat line, seen yesterday, at .4 vs -2.3 in April. These were some of the respondent comments that stood out:

Chemical manufacturing

Conflict in the Middle East, the closure of the Strait [of Hormuz] and elevated oil prices have reduced supply of polyolefins and raised the cost of oil-based feedstocks for polyolefins in Europe and Asia, causing sharp increases in export prices, which are being matched domestically. Shipments of polyolefins have increased from the U.S., but exports from China of coal-based feedstock for PVC (polyvinyl chloride), which doesn’t use oil-based feedstocks, has flooded the global market, so PVC prices rose in March and April but are now declining.

Computer and electronic product manufacturing

I keep waiting for the other shoe to drop as increased fuel prices filter through the economy, but we haven’t seen a major impact yet.

The change in government spending has hurt our chances of keeping the doors open.

Fabricated metal product manufacturing

Peak demand cycle [is] midyear. [Demand will] still be strong later in the year but will ease back to more normal levels.

[We] have received new orders that have improved our immediate outlook. More importantly, [there is] indication of an improved business environment.

Machinery manufacturing

[With] possible signs of a slowdown, [our] main concern is inflation.

Uncertainty continues to play a big role in capital expenditure decisions. We are not investing in fixed assets but are focusing all resources on reserves and ongoing operations, outsourcing more and establishing new alliances. The climate for oil and gas, despite higher prices at the pump, is by no means favorable for the industry. There is constant pressure to lower prices for the U.S. market as external factors increase to capture a very competitive, but not surprisingly shrinking, market.

What a blessed time we are in presently! Orders are up, output is steady and growth is full throttle. These periods are infrequent, when everything is forward-facing, rowing in tandem and prosperous. We’re very grateful and pray that the good times keep on rolling for an extended period.

Tariffs were a disaster! Everyone paid them, but only a few received refunds.

Business remains strong; however, we are experiencing many price increases for raw materials that we are having to pass on to customers.

Miscellaneous manufacturing

Business volume continues to grow, driven by increased market share and strong internal sales efforts. However, we are navigating several margin pressures. Slow pay is being observed across customer segments, and while price increases have met some customer resistance, we have been successful in implementing them through continued engagement efforts. On the cost side, supplier price increases and fuel surcharges are mounting, compounded by uncertainty around tariff changes and a sharp uptick in fuel prices. Keeping pace with these escalating input costs and passing them through to customers in a timely manner remains a key concern.

Positions: none.

BY Doug Kass · May 27, 2026, 9:35 AM EDT

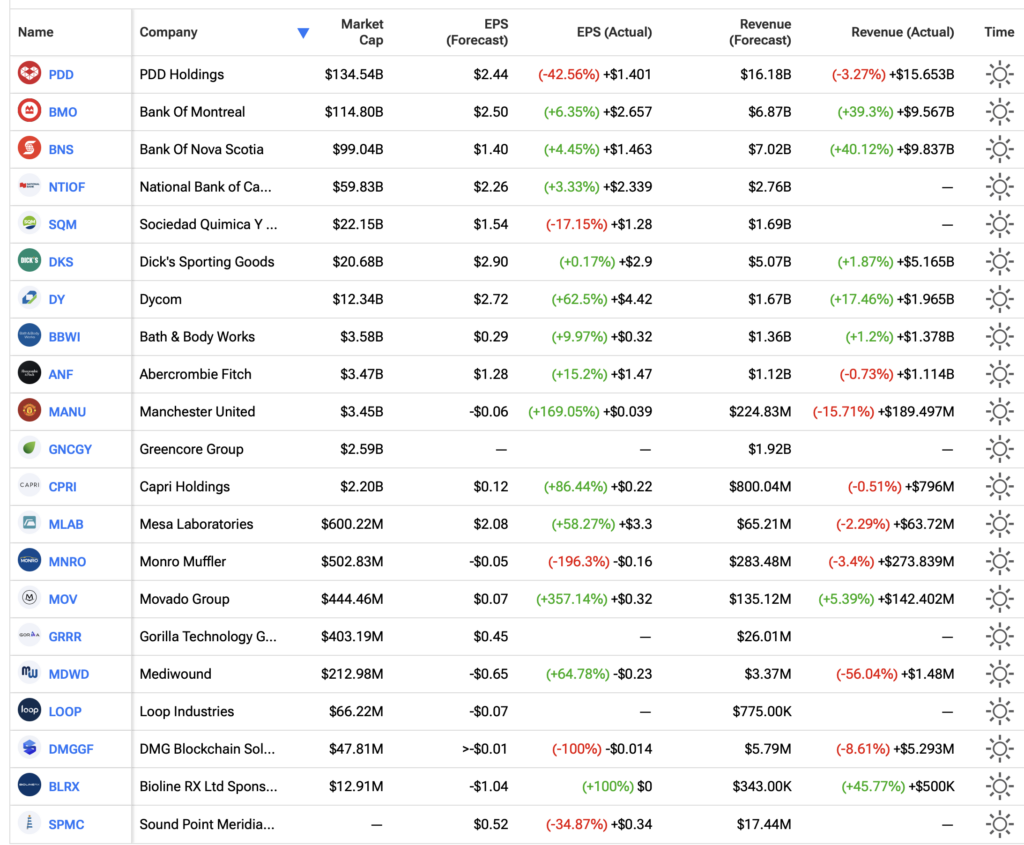

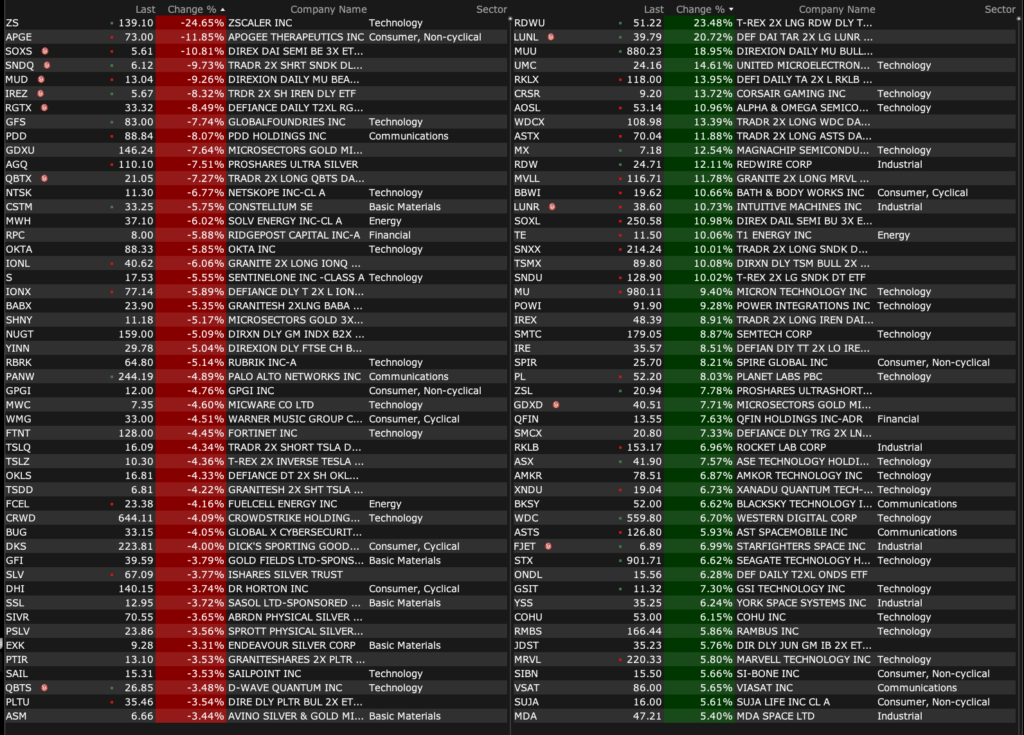

-DY +27% (earnings, guidance; acquires low-voltage engineering and construction firm National Technology Integrators for $275M)

-DTIL +13% (Clinical Data Show PBGENE-HBV Eliminates and Inactivates cccDNA in Liver Biopsies)

-SMTC +13% (earnings, guidance)

-BBWI +11% (earnings, guidance; CFO to resign)

-SPIR +7.1% (signs MoU with Schaeffler to develop space hardware subsystems and satellite platforms)

-CORT +6.0% (plans to resubmit relacorilant NDA for Cushing’s syndrome)

-MANU +4.9% (earnings, guidance)

-ANF +4.5% (earnings, guidance)

-TSM +4.2% (said to increase 3nm chip prices by 15% in H2, 2026)

-MGM +3.7% (JPMorgan Chase and Co Raised MGM to Overweight from Neutral, price target: $46)

-AXTA +3.3% (Akzo Nobel confirms on May 1st rejected conditional cash offer at €73.00/shr from Nippon Paint and Sherwin-Williams)

-APP +3.1% (constructive comments from Morgan Stanley)

-LULU +3.0% (confirms Chip Wilson (Founder) cooperation agreement for ~18 months)

-FLY +2.6% (confirms wins $75M NASA JPL MoonFall Subcontract to Deliver Drones to the Moon’s South Pole; files to sell total of 12M shares of common stock – Firefly offers 4M shares with 8M shares offered by Selling Stockholders)

-BNTX +2.5% (UBS Raised BNTX to Buy from Neutral, price target: $135 from $117)

-HIMS +2.0% (Board member purchases $1.2M of stock)

-VRRM -55% (receives Termination of Agreement Notice From Avis Budget Group; Cuts FY guidance)

-ZS -25% (earnings, guidance)

-APGE -11% (discloses data from APEX Phase 2 Part B trial; enters up to $1.3B financing collaboration with Blackstone Life Sciences for zumilokibart)

-GRRR -5.2% (earnings, guidance)

-KMT -5.1% (Barclays Cuts KMT to Underweight from Equal Weight, price target: $33 from $40)

-CPRI -3.8% (earnings, guidance)

-PODD -3.8% (issues voluntary recall for Omnipod Pods that could result in insulin under-delivery)

-DKS -2.6% (earnings, guidance)

Positions: None.

BY Doug Kass · May 27, 2026, 9:07 AM EDT

I (unemotionally) added to my speculative short package in premarket:

* (MU) $972.02

* (SNDK) $1,632.11

* (AMD) $515.09

Given the volatility I will remain very small in these trading short rentals.

Again, this is not for homegamers – I am just being transparent.

Positions: Short MU VS SNDK VS AMD VS

BY Doug Kass · May 27, 2026, 8:54 AM EDT

Over the last several trading days the market has behaved more like a casino than a church – with memory and semis serving as the house.

Caveat emptor.

I will be expanding my short exposure on the Iranian news.

Positions: None

BY Doug Kass · May 27, 2026, 8:50 AM EDT

11:30 a.m.: Treasury hosts a $69B 17-Week Bill Auction;

11:30 a.m.: Treasury hosts a $28B 2-Year FRN (r) Auction;

1:00 p.m.: Treasury hosts a $70B 5-Year Note Auction

4:00 a.m.: Fed Bank of Dallas President Logan (Voter) participates in “Policy Panel Discussion 1: Monetary Policy and Imbalances” before the 2026 Monetary Policy from New Perspectives Conference hosted by the Bank of Japan Institute for Monetary and Economic Studies, Tokyo (Embargoed text available);

3:55 p.m.: Fed Board Governor Cook (Voter) speaks on “AI, the Economy, and the Financial System” before the Stanford Institute for Economic Policy Research (SIEPR) Policy Forum, Stanford, CA (Text available. Q&A from moderator. Livestream at stanford.zoom.us);

8:00 p.m.: Fed Vice Chair Philip Jefferson (Voter) participates in “Fireside Chat: Monetary Policy and Supply Shocks” before the 2026 Monetary Policy from New Perspectives Conference hosted by the Bank of Japan Institute for Monetary and Economic Studies, Tokyo (Text available. Q&A from moderator. No webcast);

9:10 p.m.: Fed Bank of Chicago President Goolsbee (Non-Voter) Television Appearance – CNBC Squawk Box Asia (Interview to air across Asian markets. Interview excerpts will publish to CNBC Asia website after the interview);

10:25 p.m.: Fed Bank of Chicago President Goolsbee (Non-Voter) participates in a panel discussion titled “Monetary Policy in a Changing World Economy” at the Bank of Japan Institute for Monetary and Economics Studies Conference, Tokyo (No Live Stream, Embargoed Text)

Positions: None.

BY Doug Kass · May 27, 2026, 8:45 AM EDT

Positions: none.

BY Doug Kass · May 27, 2026, 8:39 AM EDT

Positions: None.

BY Doug Kass · May 27, 2026, 8:20 AM EDT

My pals Shadd Dales and Anthony Varrell had an informative Trade to Black interview after the close yesterday.

Run, don’t walk to watch the Chairman of (CURLF) discuss uplisting and reverse splits:

Positions: None.

BY Doug Kass · May 27, 2026, 8:11 AM EDT

From Knowledge@Wharton:

Cities Can’t Afford to Fight the Last War – Knowledge at Wharton

BY Doug Kass · May 27, 2026, 7:30 AM EDT

* The last chapter…

Twitter/X has an addictive quality.

The “discussions” on X mirror the anger that characterizes discourse in this country today.

As to my constant criticism of the financial media, Fin TV (in particular) prizes the consensus. It favors “first-level thinking” and generally ignores “second-level thinking.” This non-rigorous delivery is effective when the “tide is coming in.” Not so much in corrections when the “tide is going out.”

Many corners of the media have too often become an echo chamber of opinion. It is sometimes dishonest in the sense that it is not transparent (no timestamps and no ownership for investing/trading boners). But, at this point, I have made this point often enough.

In case you missed my Tweet of the Day:

Position: None

BY Doug Kass · May 27, 2026, 6:45 AM EDT

* Cyclical stocks tend to peak with what appear to be low price-earnings multiples

Position: Short MU (VS)

BY Doug Kass · May 27, 2026, 6:30 AM EDT

Position: Short MU (VS)

BY Doug Kass · May 27, 2026, 6:15 AM EDT

Dougie Kass

Last night shorts (off solely (massive) overboughts) and not for homegamers! Put on very small AMD $506.21 MU $949.56 SNDK $1636.

Position: Short AMD (VS), MU (VS), SNDK (VS)

BY Doug Kass · May 27, 2026, 6:05 AM EDT

The S&P Short Range Oscillator is back into overbought territory at 0.74 vs. -0.71.

Position: Short SPY (M), QQQ (M)

BY Doug Kass · May 27, 2026, 5:55 AM EDT

BY Doug Kass · May 27, 2026, 5:47 AM EDT

In a way Twitter mirrors drug addiction by hijacking your brain's dopamine system. Just as a drug triggers a massive chemical flood, Twitter creates a "compulsion loop" of intermittent, unpredictable rewards—likes, retweets, and outrage—that keeps you constantly craving your next Show more

Curaleaf Thickens The Plot While SAM Keeps Losing x.com/i/broadcasts/1…

Micron now trades with a ~10x multiple S&P 500 has a P/E ratio of ~21x

$mu up a casual $60B in market cap in the after hours session… or the entire value of the company 5 years ago Probably nothing

Just wait until MSOs uplist and start turning grows into datacenters