My Tweet of the Day (Part Deux)

Tim Cook $AAPL to become Executive Chairman of the Board of $AAPL

— Dougie Kass (@DougKass)

John Ternus (hardware division) to become CEO of the company.

BY Doug Kass · Apr 20, 2026, 4:50 PM EDT

Tim Cook $AAPL to become Executive Chairman of the Board of $AAPL

— Dougie Kass (@DougKass)

John Ternus (hardware division) to become CEO of the company.

BY Doug Kass · Apr 20, 2026, 4:50 PM EDT

Neither overboughts/oversolds nor sentiment/surveys are good clocks... but they are (especially in the extreme) a good weather forecast ..

— Dougie Kass (@DougKass)

S&P Short Range Oscillator at close stands at 7.61% - very overbought. @SquawkCNBC @andrewrsorkin @BeckyQuick @CNBCFastMoney @HalftimeReport…

BY Doug Kass · Apr 20, 2026, 4:45 PM EDT

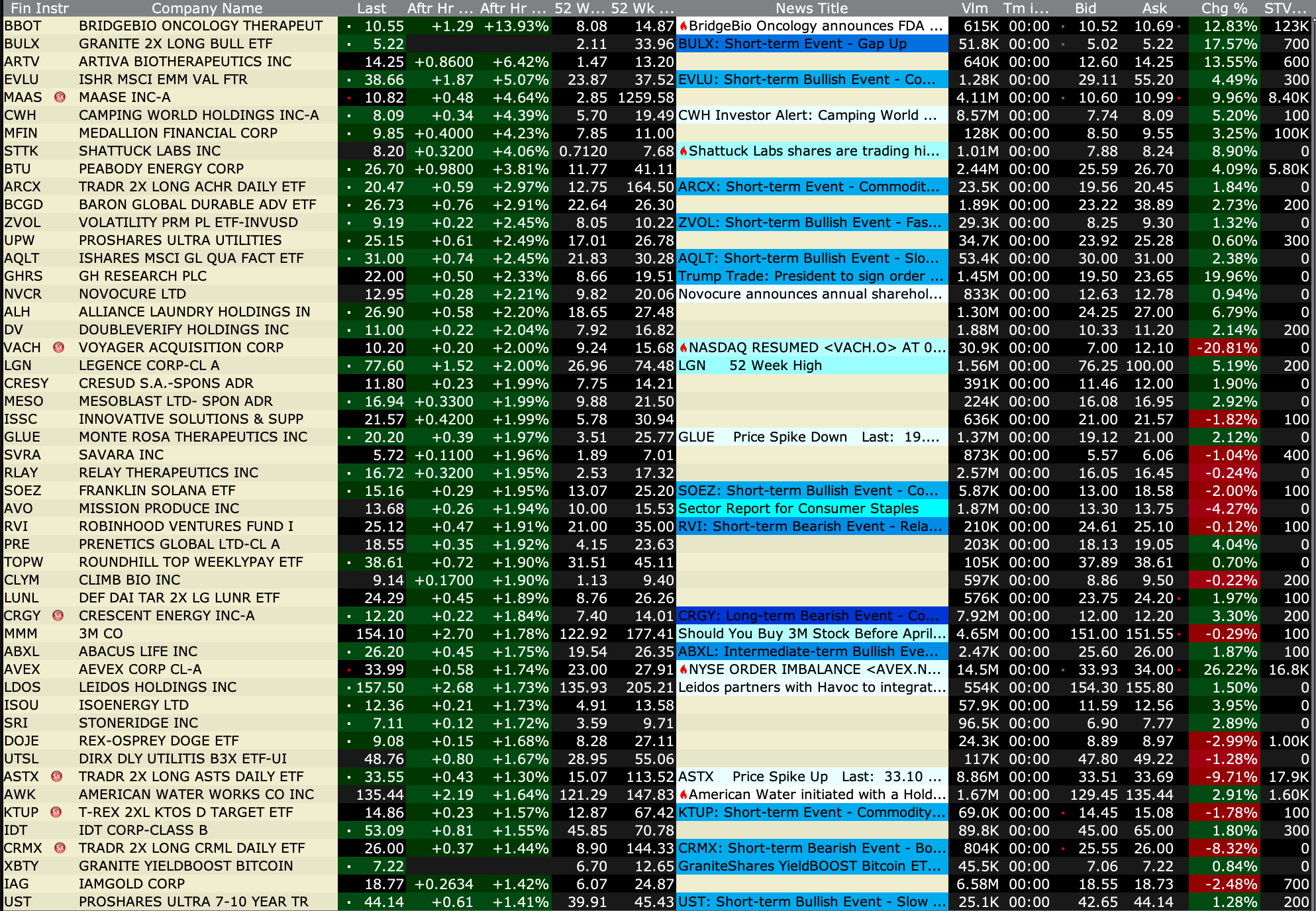

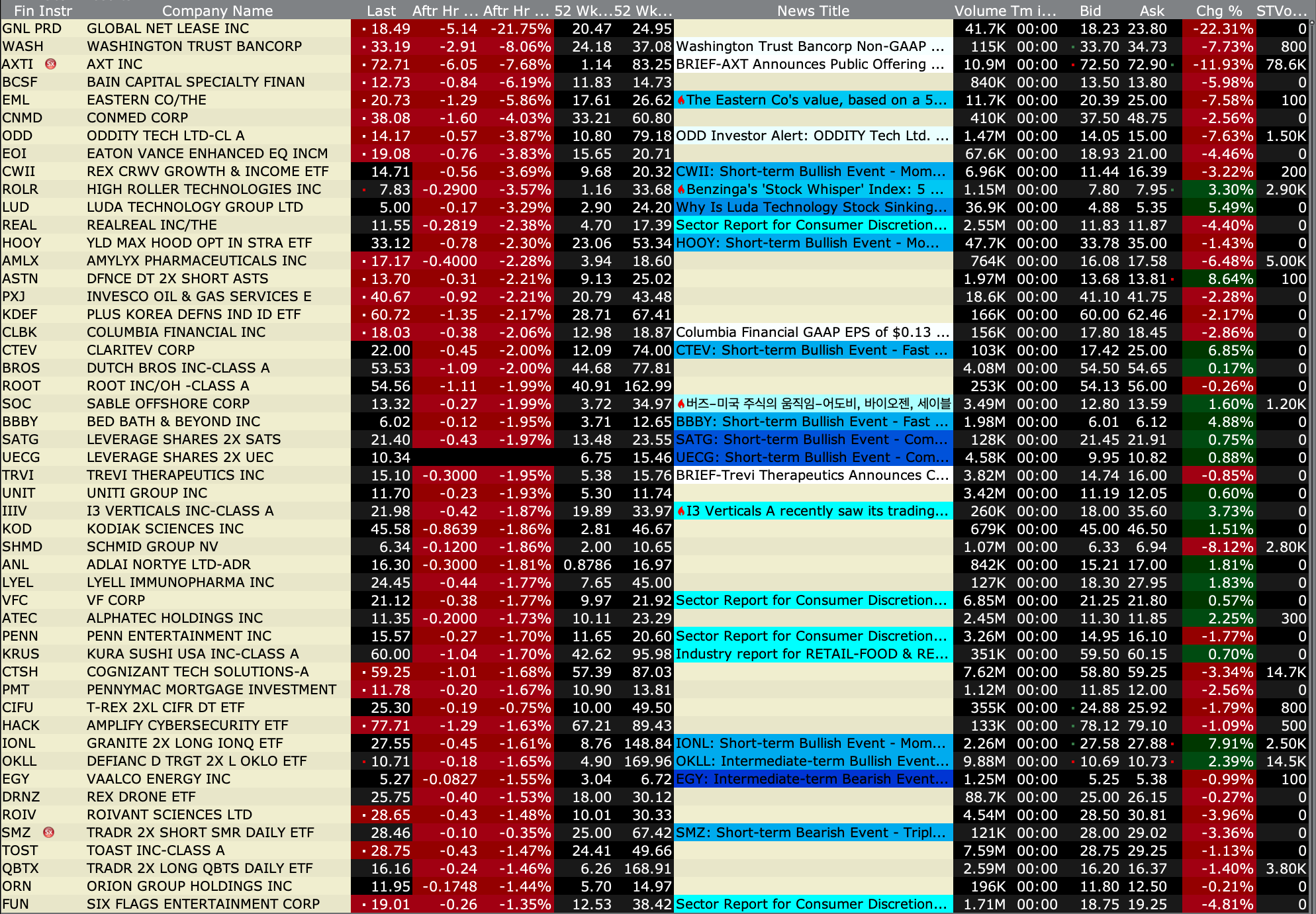

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Apr 20, 2026, 4:40 PM EDT

Closing Volume

- NYSE volume 17% below its one-month average;

- NASDAQ volume 7% below its one-month average;

- VIX index:up 8.07% to 18.89

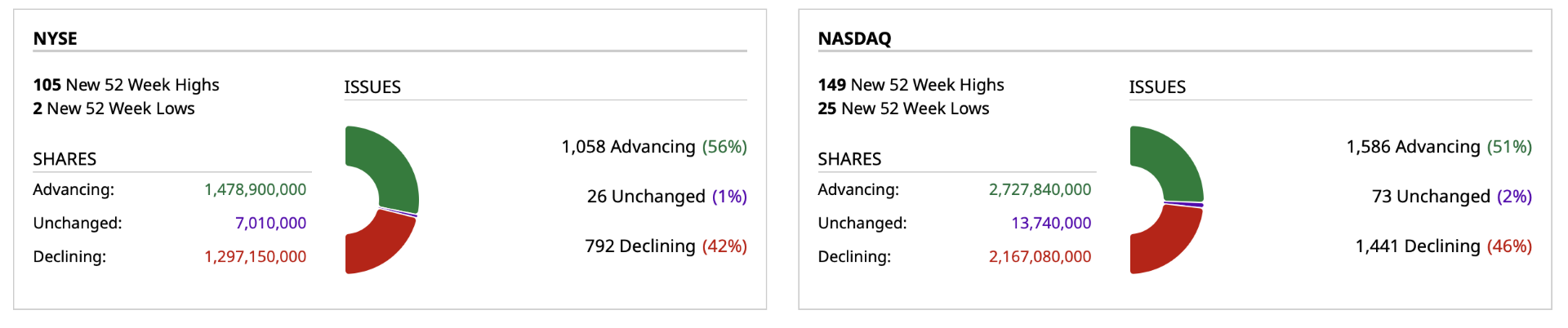

Breadth

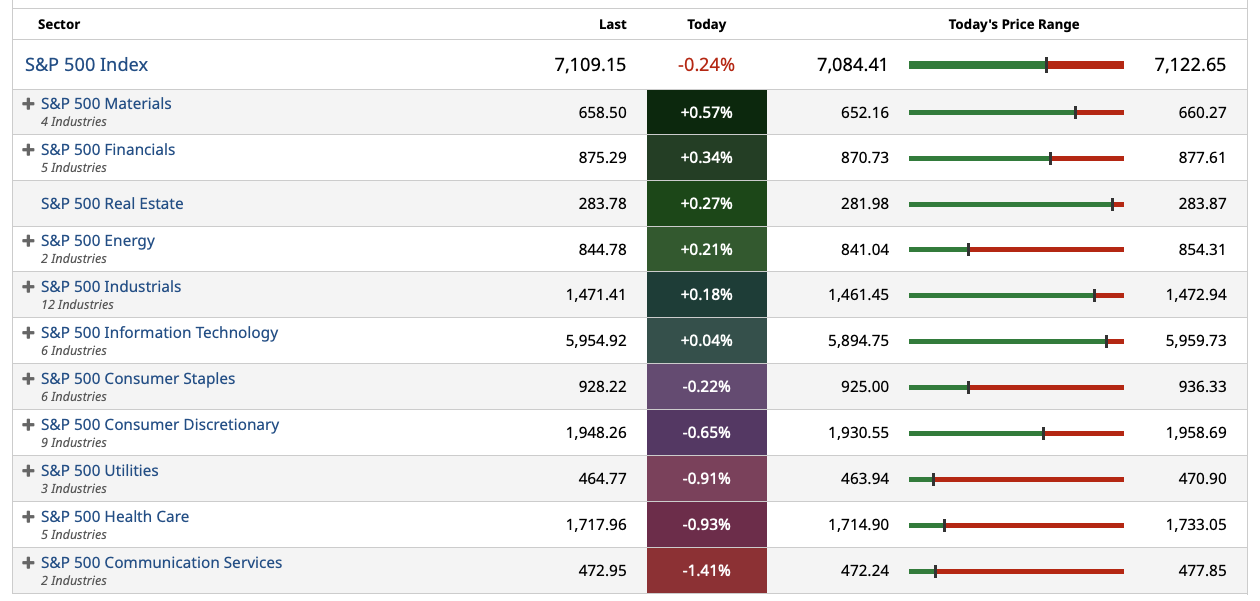

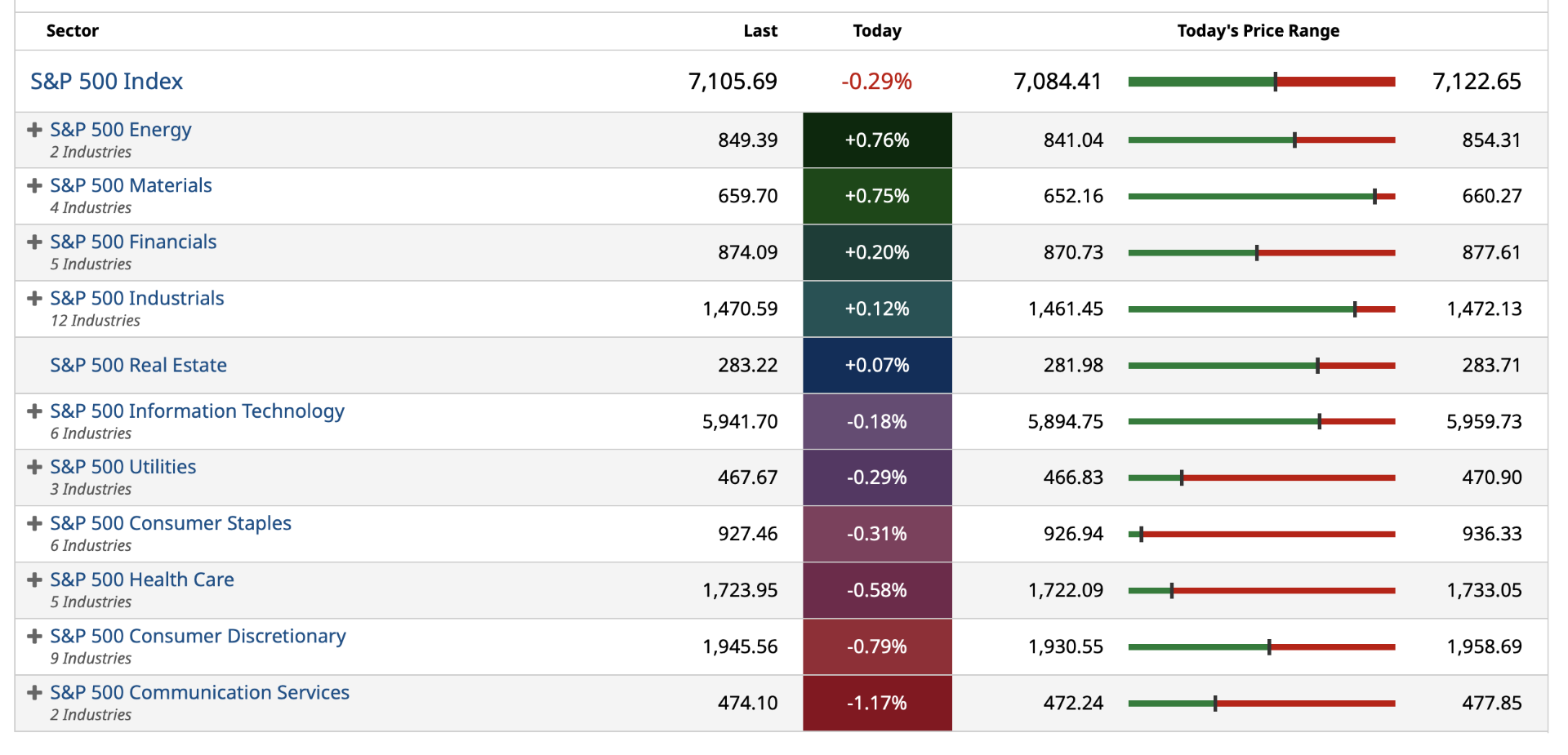

S&P 500 Sectors

% Movers

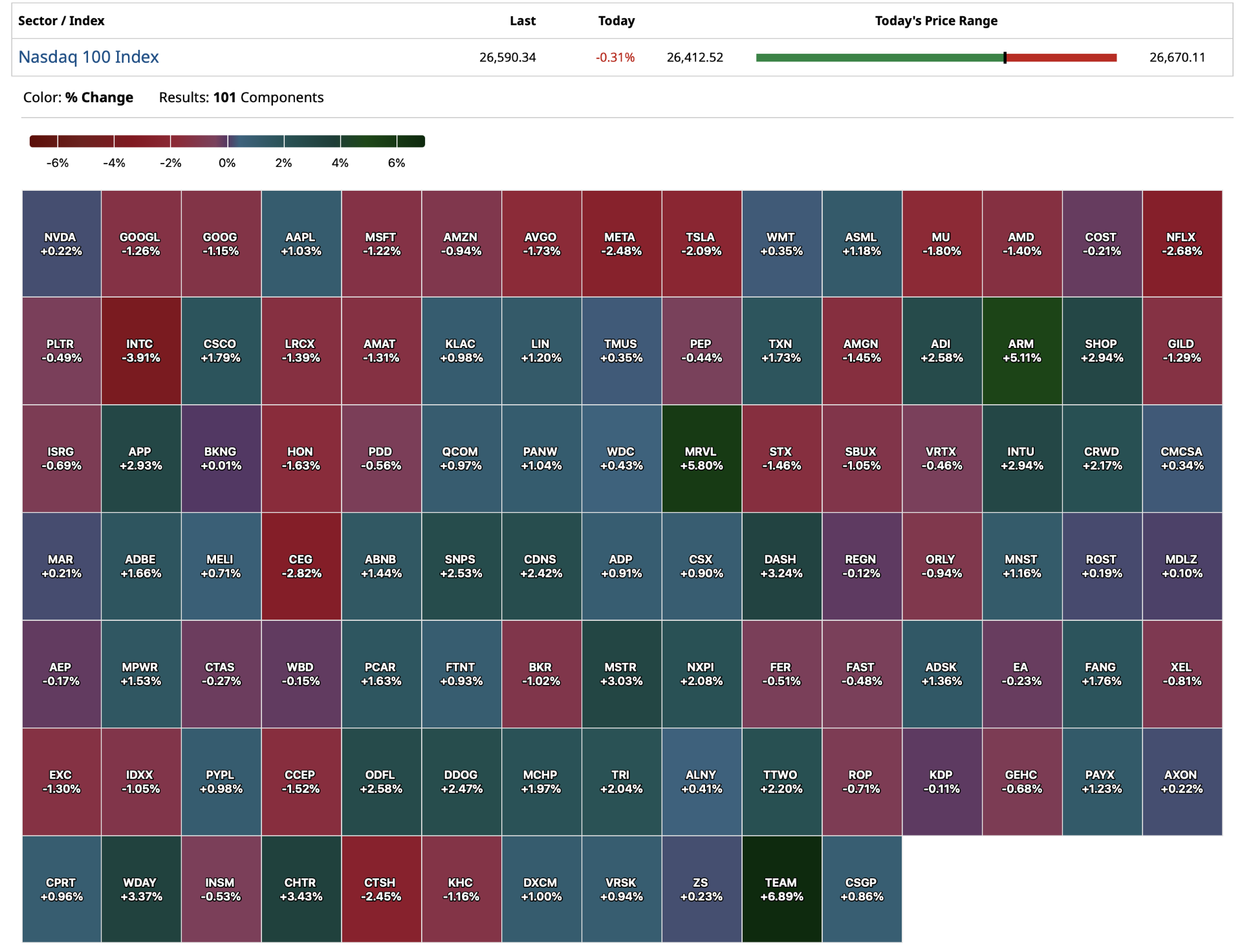

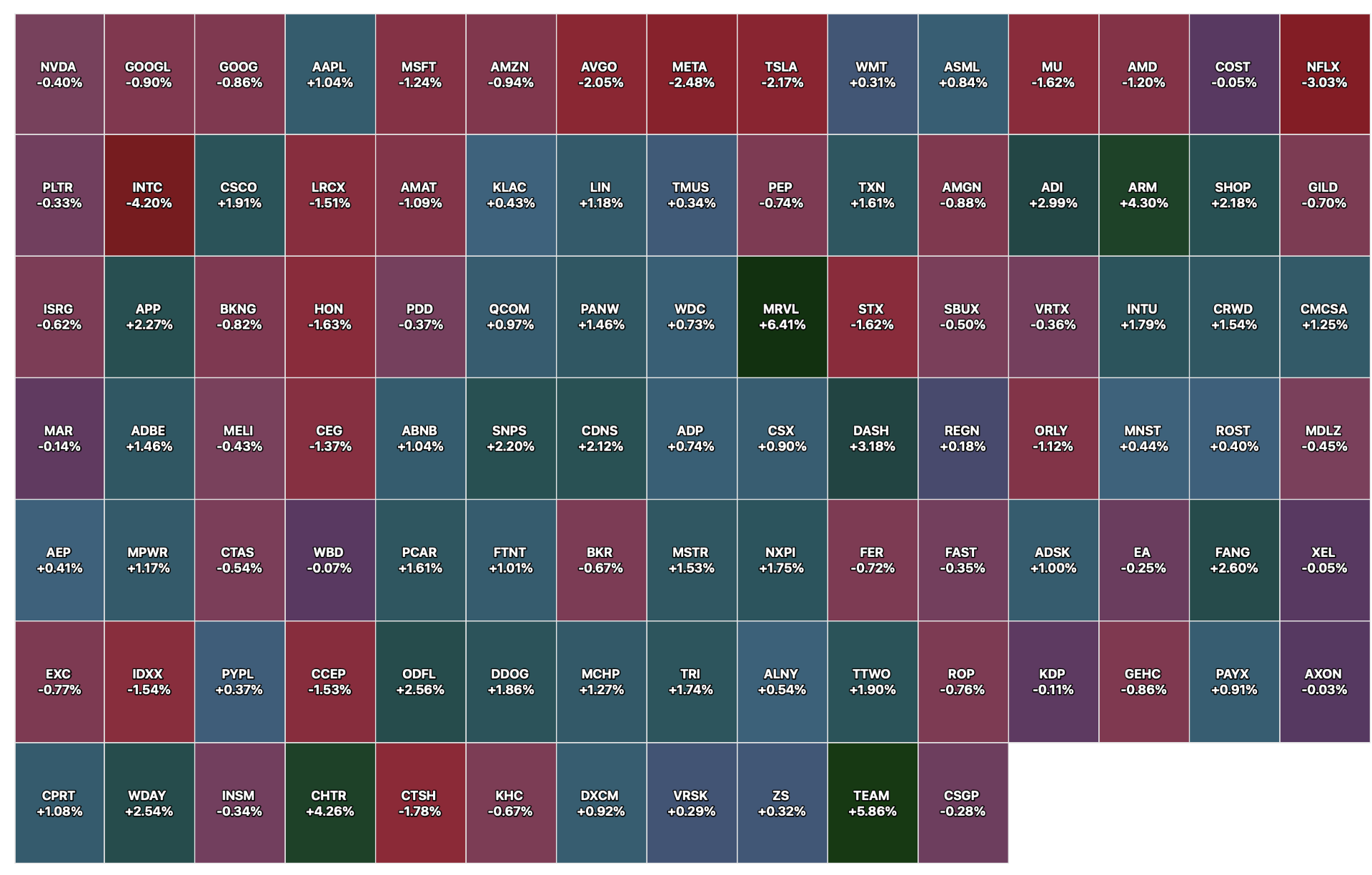

Nasdaq 100 Heat Map

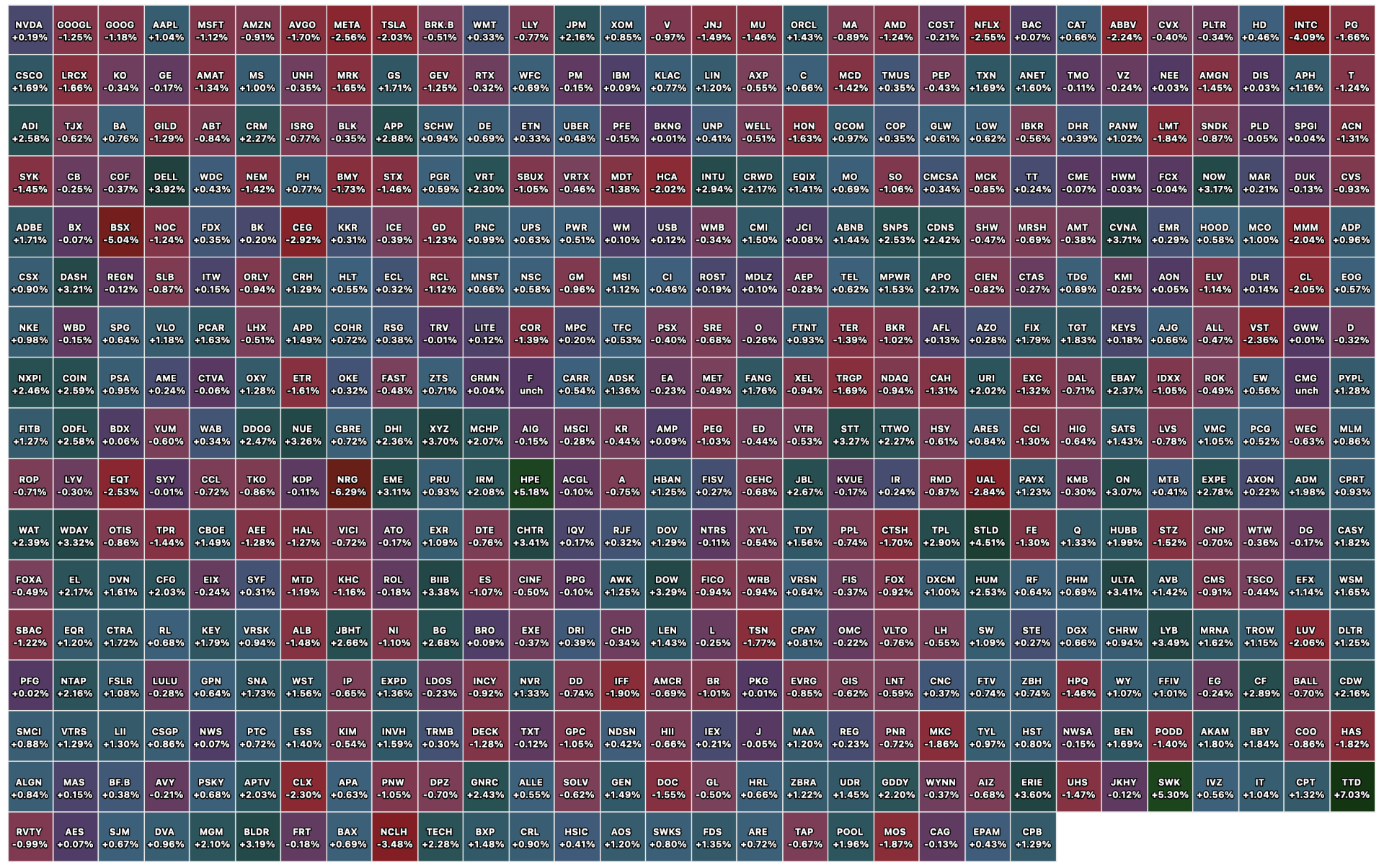

Closing S&P 500 Heat Map

BY Doug Kass · Apr 20, 2026, 4:30 PM EDT

While not near recessionary territory yet, real personal consumption expenditures continue to weaken. Such will likely feed into earnings and economics in the quarters ahead if it gets weaker.

— Lance Roberts (@LanceRoberts)

The trailing 3-month growth rate through February is annualizing at just 0.8%. pic.twitter.com/bAAnAi74tT

BY Doug Kass · Apr 20, 2026, 3:35 PM EDT

"As long as the roots are not severed, all is well and will be well in the garden..."

- Chauncey Gardiner, Being There

US small businesses are pulling back on investment as if we are in a crisis:

— The Kobeissi Letter (@KobeissiLetter)

In March, only 16% of small businesses said that they plan on investing in CapEx over the next 6 months, the lowest reading since November 2009.

This percentage has declined -12 points since November… pic.twitter.com/0r8SgwK1Ia

BY Doug Kass · Apr 20, 2026, 3:25 PM EDT

I added to index shorts:

* (SPY) $708.49

* (QQQ) $646.48

Position: Short SPY common (S), QQQ common (S)

BY Doug Kass · Apr 20, 2026, 3:15 PM EDT

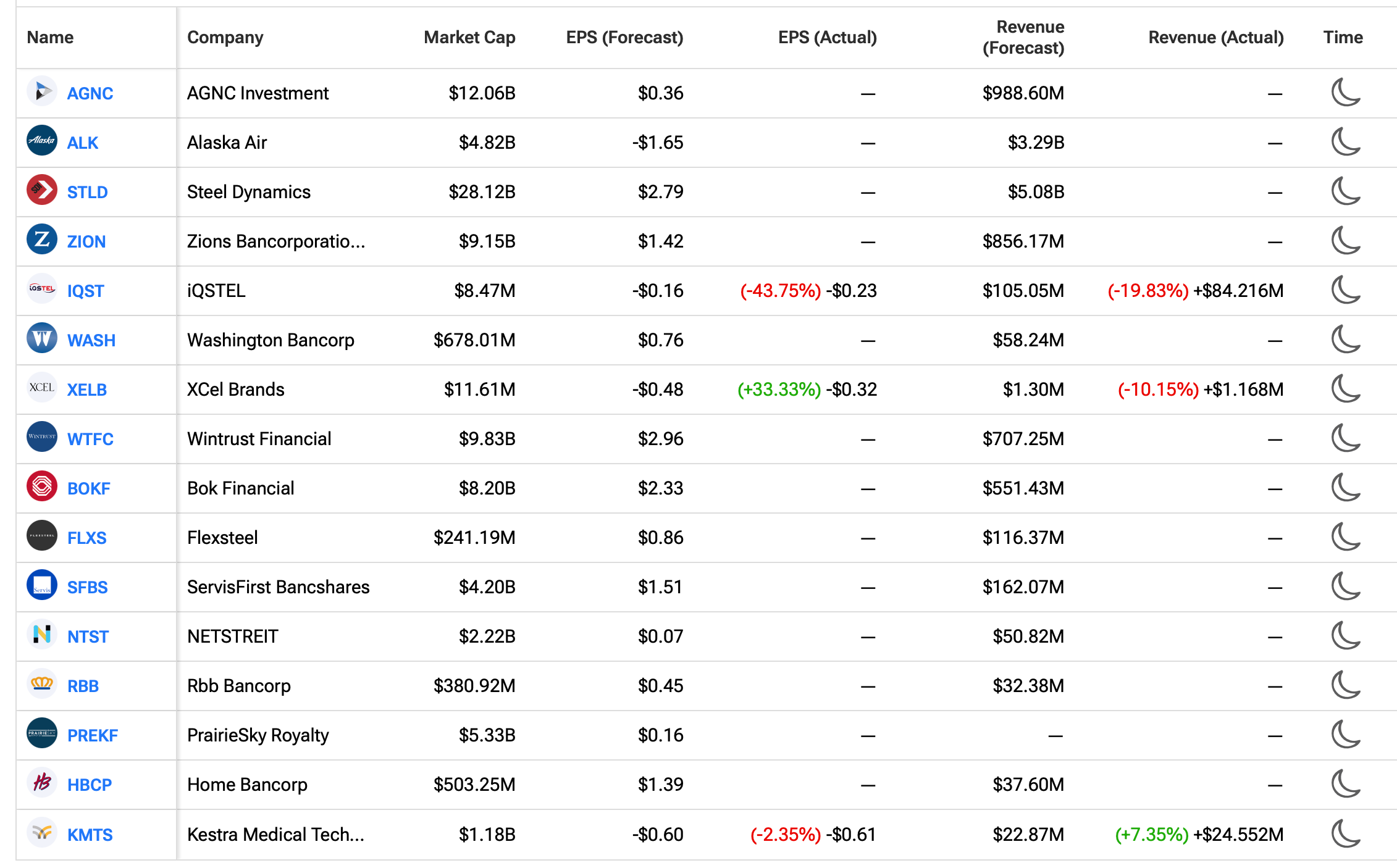

Earnings After the Close Monday April 20

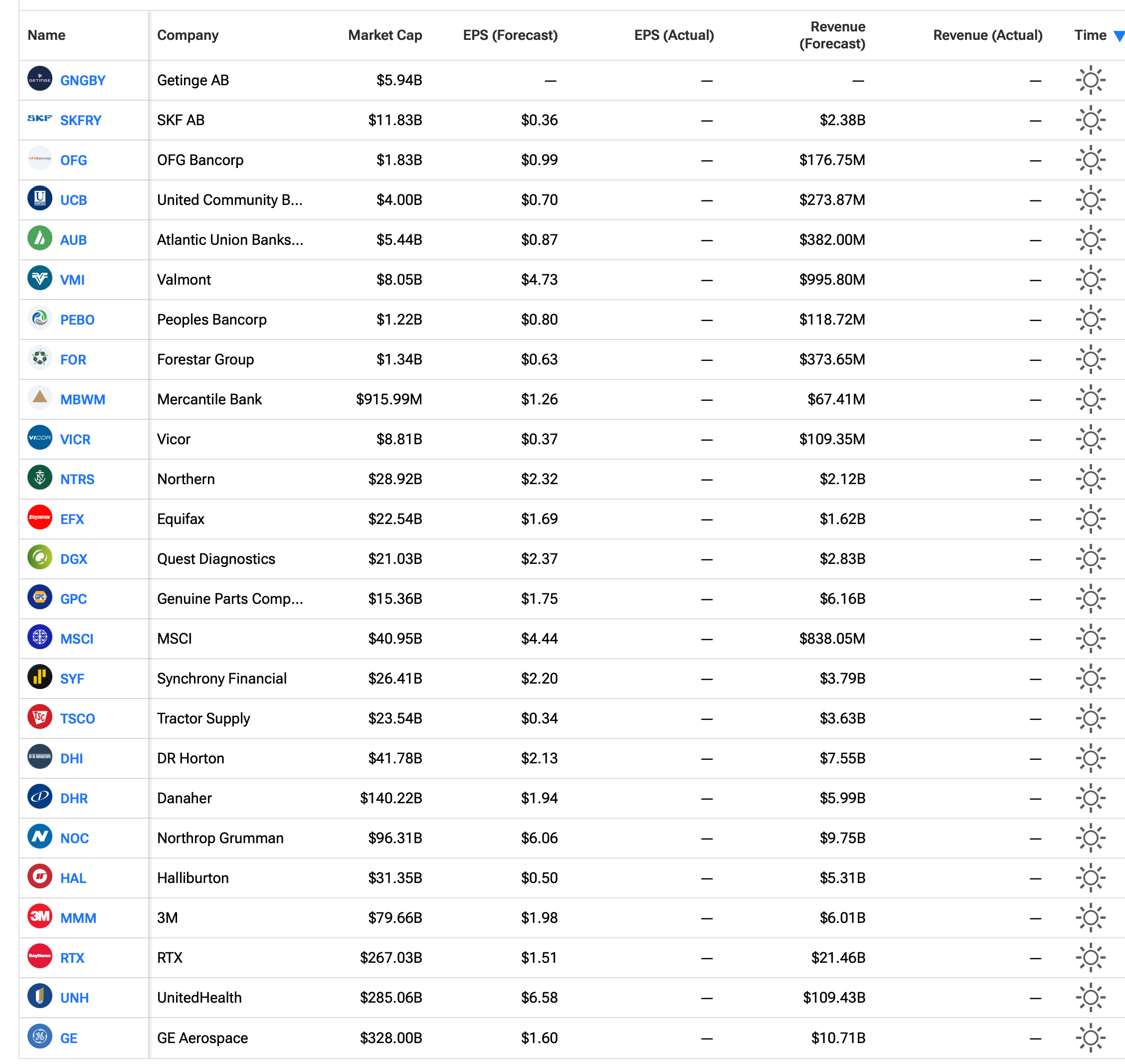

Earnings Before the Open Tuesday, April 21

BY Doug Kass · Apr 20, 2026, 3:10 PM EDT

At 2:45 PM

Breadth

Sectors

Nasdaq 100 Heat Map

BY Doug Kass · Apr 20, 2026, 3:04 PM EDT

Goldman Sachs on stocks/economy:

— Brian Sozzi (@BrianSozzi)

"Relative to the pre-war period, we expect lower growth, higher inflation, higher long-term oil prices, and somewhat higher policy rates, at least in the near-term. Rising earnings expectations have also lowered US equity valuations. This makes…

BY Doug Kass · Apr 20, 2026, 2:00 PM EDT

Professional investors are rushing back into equities:

— The Kobeissi Letter (@KobeissiLetter)

US equity positioning jumped +0.55 points last week, the largest weekly increase in 8 years.

This metric covers institutional investors like fund managers, hedge funds, and algorithm-based trading strategies.

Since 2010,… pic.twitter.com/umCmdl3UaT

BY Doug Kass · Apr 20, 2026, 1:43 PM EDT

Green Thumb's (GTBIF) Ben Kovler appears on Bloomberg discussing rescheduling.

Cannabis CEO Calls for Reform

— Todd Harrison (@todd_harrison)

🇺🇸 #Cannabis 🌿 /positions $MSOS $GTBIF pic.twitter.com/ZRz97hA8fl

Position: Long GTBIF (VS)

BY Doug Kass · Apr 20, 2026, 1:22 PM EDT

Run, don't walk to watch MRKT CALL at 11 AM with Guy and Dan for a practical trip down the markets, objective analysis, real-time trading ideas all delivered with a sense of humility.

And they take ownership of their mistakes!

Let's go to the recorded tape of this morning's show. (This morning they briefly discuss my opening missive).

BY Doug Kass · Apr 20, 2026, 12:05 PM EDT

Charts from 9:46 a.m. ET

Positions: None.

BY Doug Kass · Apr 20, 2026, 11:17 AM EDT

From Peter Boockvar:

Another few days of lost shipments thru the Strait but markets certainly hopeful for an imminent deal anyway with the modest pullback in the S&P futures and a full reopen without threat.

A lot of focus on tanker and shipping rates but air cargo rates have really spiked. According to the weekly figures from WorldACD Market Data, prices rose by another 3% in the week between April 6-12 and are now up 37% y/o/y and higher by 40% from the end of February. WorldACD said this, “The two-week ceasefire agreement this month between Washington and Teheran raised hopes of a lasting settlement of the conflict, although the truce remains fragile and the outlook for peace is uncertain. Most observers have warned that inflation and elevated fuel costs are likely to persist for some time, even if the current ceasefire holds, and there are increasing concerns that jet fuel shortages and rising costs of jet fuel will lead to flight cancellations and further air cargo rate rises in the coming weeks unless there is a swift resolution to the current crisis. Meanwhile, bellyhold capacity through the Middle East will take time to fully recover, and container lines do not expect a return to pre-conflict flows any time soon, meaning air cargo pricing is likely to remain elevated for some time.”

Still no increase in the crude oil rig count in the US in response to higher prices and the oil price drop seen on Friday helps to explain why as drillers don’t want to commit right now to more drilling. The Baker Hughes crude oil rig count fell by 1 rig to 410. Not much of a change from the 407 rigs drilling at the end of February.

Something I’ve been arguing is that even upon the cessation of the conflict and full reopening of the Strait is that there will be an underlying bid for a variety of commodities as countries stockpile inventories for future rainy days, among other reasons, so as not to repeat this current experience. On Friday, the FT reported “DR Congo to stockpile critical minerals.” In the piece, “The Democratic Republic of Congo will establish a strategic reserve of three minerals, including cobalt and coltan, in a move designed to give the Central African country more leverage over the market for some of the world’s most important metals.”

“The plan is the latest in a series of moves by African countries to gain greater control over their raw materials...The reserve, which will also include germanium and could be expanded to other minerals, builds on previous measures to bolster cobalt prices, including a temporary ban on exports last year followed by a quota system.”

Now, this will be used by African mineral producers to balance the market and “stabilize” prices as they say, sort of their own cartel but imagine the strategic reserves that the rest of the world is going to want to create so no one gets caught short of inventory of key things, like oil too.

https://www.ft.com/content/d0f19c7c-2f5c-4865-a326-e4765bbcec58?syn-25a6b1a6=1

We’re also going to see in the years to come, as mentioned here, an attempt to build infrastructure and logistics that will bypass the Strait. Over the weekend I read a Bloomberg News article saying “IEA head pitches Iraq-Turkey pipeline to bypass Hormuz.” It said “IEA Executive Director Fatih Birol proposed building a new oil pipeline linking Iraq’s Basra oil fields and Turkey’s Mediterranean oil terminal in Ceyhan to shift the balance away from the Strait of Hormuz, according to Turkish newspaper Hurriyet.”

This is just one proposal but we’re going to see a lot of this, with projects to follow in the coming years and Iran will lose more and more leverage over the Strait.

Source: https://www.bloomberg.com

To some financial company earnings calls of relevance.

Ally Financial rallied 8% Friday after earnings and said this of note:

“Adjusted provision expense of $474 million was down $23 million y/o/y, largely driven by continued improvement in retail auto net charge-offs and the exit from credit card.”

“1Q marked the fifth consecutive quarter of y/o/y improvement in NCOs as we benefited from particularly strong used vehicle prices and record low flow to loss ratios...30 plus all-in delinquencies of 4.6% were down 17 bps from the prior year, marking the 4th consecutive quarter of y/o/y improvement on an all-in basis.”

“Notwithstanding the increase in tax refunds and a dynamic macro, delinquency followed what we consider to be a typical seasonal pattern during the quarter. We’ve continued to see a resilient consumer, but given the evolving backdrop, we feel it’s appropriate to remain measured.”

How they define ‘measured,’ “If you look at the data from the quarter, auto applications are up 16% y/o/y but origination volumes are at a slightly more moderate pace. And so we’re prioritizing, I call it, discipline over volume.”

More, “there’s a bit of a disconnect between consumer sentiment data and what we’re seeing in our portfolio...we continue to see opportunities to generate loans with attractive risk-adjusted returns.”

Lastly, “And so you put all this stuff together, you got headwinds and tailwinds, but we feel good about what we’re seeing in our portfolio. And so overall, I’m aware the environment is unusual, but I’m really pleased with our fundamentals and our recent performance.”

From Fifth Third Bank:

“In commercial, legacy Fifth Third C&I loan balances grew 6% y/o/y. Production remained healthy, with the strongest activity in manufacturing and construction supported by restoring and infrastructure investment.”

“Clients are cautious but active.”

“The consumer portfolio remains healthy, with non-accrual and over 90 delinquency rates relatively stable across all loan categories.”

“We have been deliberate about where we choose to grow. Our exposure to non-depository financial institutions represents only 7% of our total loan portfolio, well below the industry average. Our three largest categories are subscription lines supporting capital call facilities, corporate credit facilities to traditional institutions such as payment processors, insurance companies and brokerage firms, and secured lending to residential mortgage related entities. These are long standing portfolios.”

“On private credit, we have chosen not to participate meaningfully in lending to private credit vehicles and business development companies, which combined represent less than 1% of total loans. That was a deliberate decision, not a missed opportunity. The structural complexity embedded in these exposures introduces risks that are harder to assess through a cycle.”

“On software and data center lending, we have maintained that same disciplined posture. We believe in the long demand for AI infrastructure, but we have also seen how quickly these build cycles can overshoot. We have remained selective, and our exposure is intentionally limited. Software related exposures is less than 1% of total loans, with the portfolio performing in line with expectations, with no material migration in the quarter.”

To the one data point of note overseas, Germany’s March PPI, thus capturing the commodity price spikes, jumped 2.5% m/o/m, well more than the estimate of up 1.4%. Notwithstanding this, wholesale prices were flattish y/o/y. The German 10 yr inflation breakeven is unchanged in response but the 2 yr yield is up by 3 bps to 2.99%, 10 bps from a 15 yr high.

Positions: None.

BY Doug Kass · Apr 20, 2026, 11:03 AM EDT

📢 "You’re going to get the rescheduling done, right, please? Will you get the rescheduling done, please? You know they’re -- Joe [Rogan], they're slow-walking me on [cannabis] rescheduling. You’re going to get it done, right?" - @POTUS

— The Dales Report (@TheDalesReport)

"Absolutely." - presumably DOJ off camera pic.twitter.com/1u6PUzscs7

Position: None.

BY Doug Kass · Apr 20, 2026, 10:38 AM EDT

"Only the small secrets need to be protected. The large ones are kept secret by public incredulity."

- Marshall McLuhan

The strength and rapidity of the market's rally (especially since March) has likely been momentum-driven (due in part to market structure changes over the last decade in which passive products and strategies have dominated the investment landscape). This backdrop of momentum based machine-driven dominance — in which buyers buy strength and sellers sell weakness — has, in turn, led to a great deal of fear of missing out. These factors and others have contributed to a record pace of recovery ("V"-type) from the March, 2026 lows.

While I pivoted long in the second half of March, I quickly took profits and eliminated many of my longs late last week.

The magnitude and strength in the major indexes over the last week have been anathema to me, and especially to those with a value (and non-momentum based) orientation.

At times like this I am reminded that incredulity robs us of many pleasures and gives us very little in return! Or as Samuel Johnson wrote:

"To revenge reasonable incredulity by refusing evidence, is a degree of insolence with which the world is not yet acquainted; and stubborn audacity is the last refuge of guilt."

In my view, the markets have ignored the same conditions that set off the January-February selloff. None of the non-war issues that drove stocks lower have been resolved:

* Oil prices are off their highs but are likely to remain elevated because of the magnitude of the supply shock and continued uncertainty.

* Inflation is higher than before the conflict in Iran.

* Interest rates will be higher for longer.

* The 2026 annual deficit will approach $2 trillion, neither political party show any signs of being fiscally responsible.

* The U.S. debt will hit $40 trillion — the cost of servicing the debt is over $1 trillion/year.

* With a burgeoning deficit, stiff debt load and persistent inflation, the Fed's hands are tied.

* While private equity's problems are not systemic, the leverage they brought us remains in place.

* The enormous amount of money spent on AI will probably never see an adequate return on investment. As noted by Stan Druckenmiller, AI's societal and transformative impact could rival the internet's life changing influence — and so may the stock market consequences (rhyme) be similar:

"If we were all sitting here in 1999 talking about the Internet, I don’t think anybody would have estimated it would be as big as it got in 20 years. And yet, if you bought the Nasdaq in ’99, it went down 80% before that all came to fruition. That’s not going to happen with AI. But it could rhyme – AI could rhyme with the Internet as we go through all this capital spending we need to do. The big payoff might be four to five years from now. So AI might be a little overhyped now but under-hyped long term."

- Stanley Druckenmiller

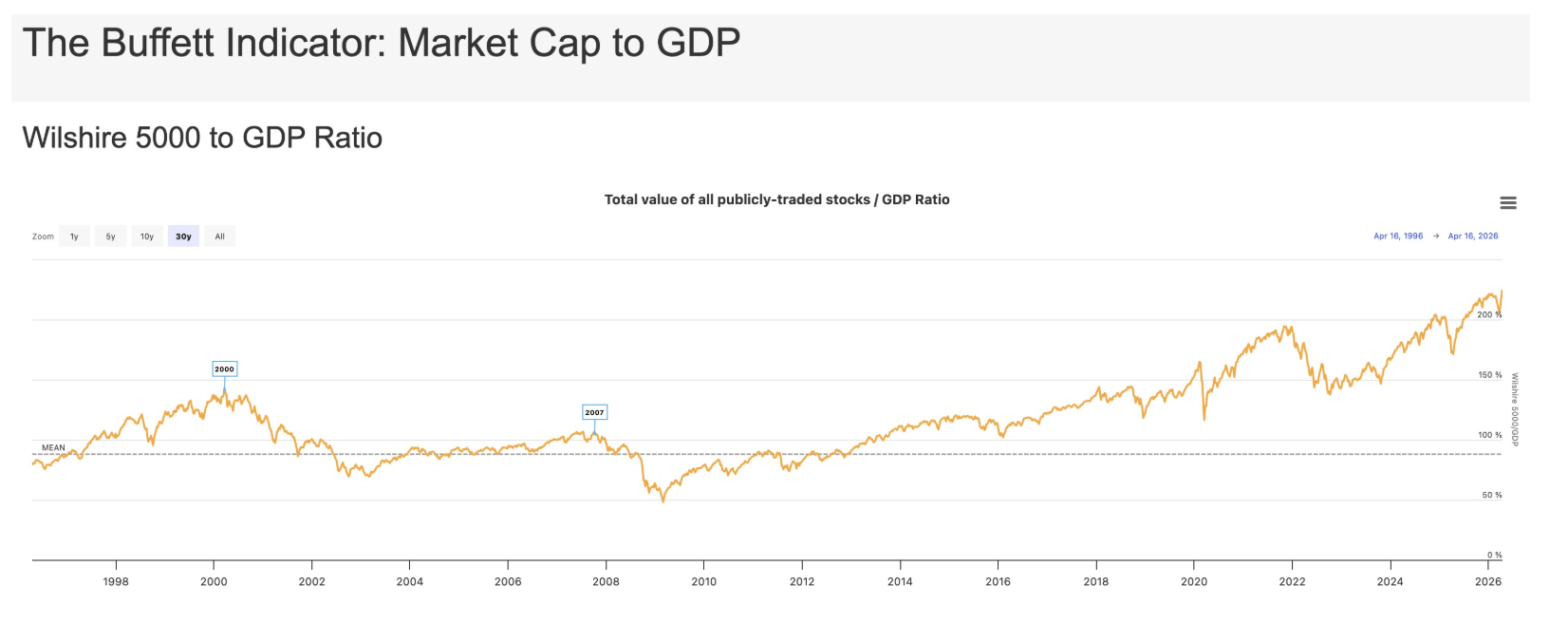

* Valuations are stretched (e.g., the Buffett ratio (the total market capitalization divided by GDP) hit an all-time high this week). Other methodologies and traditional historic metrics signal overvaluation.

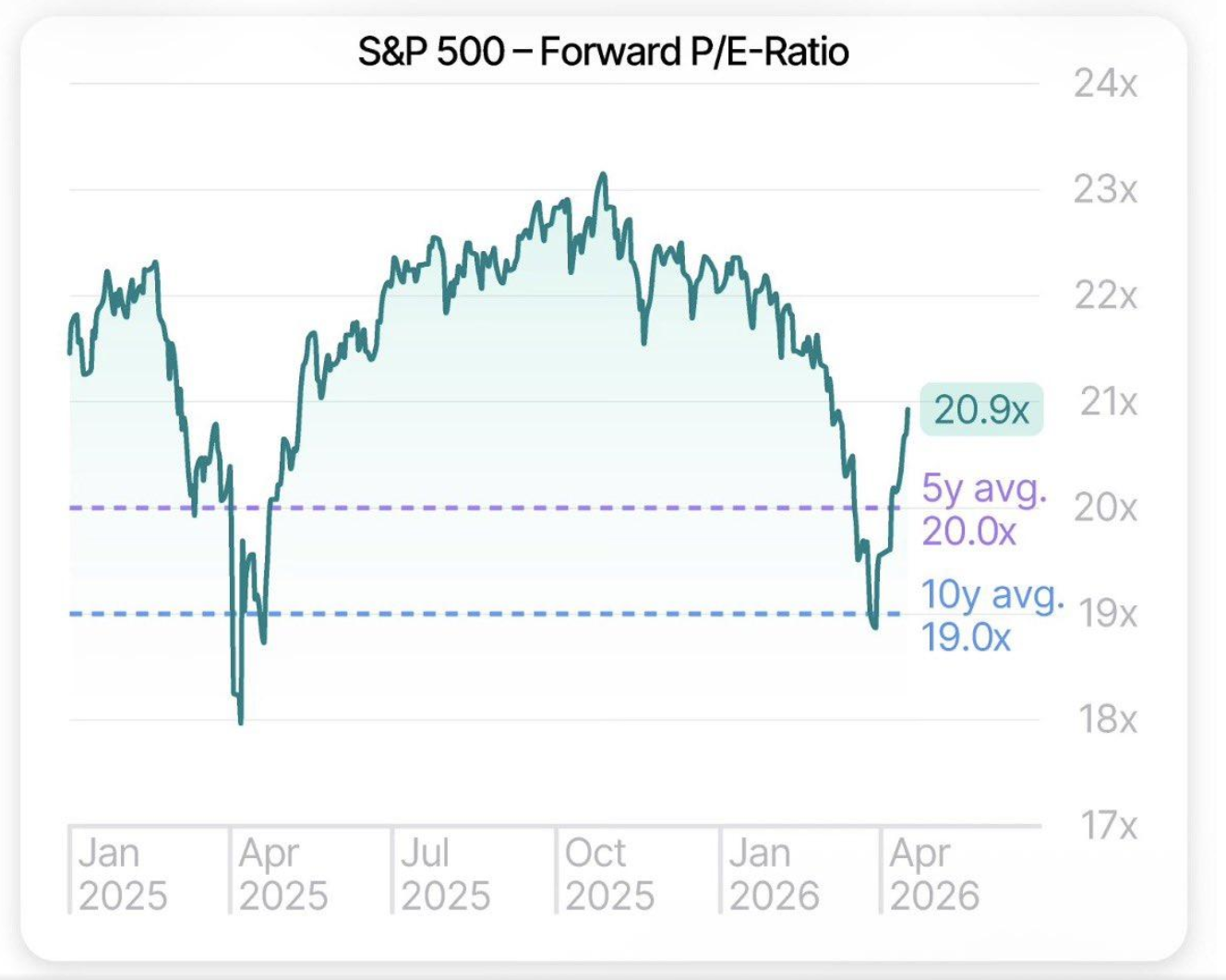

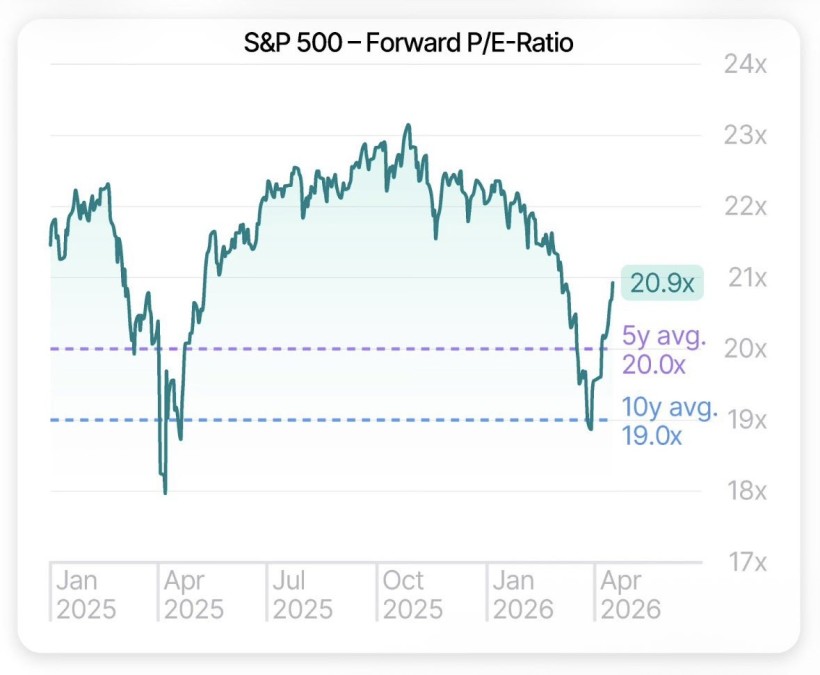

Valuations are a terrible clock but a good weather forecast:

and...

and ...

One last important bullet point (that I highlight from the above 10 issues) is that bulls argue that 2026 S&P earnings per share growth will be robust (at about +17%) — so profits justify current valuations. However, if one takes out Nvidia (NVDA) and Micron (MU) from the calculus, 2026 S&P EPS growth will be under +10%:

Most investors are now convinced we are in a continued Bull Market led by AI-related equities.

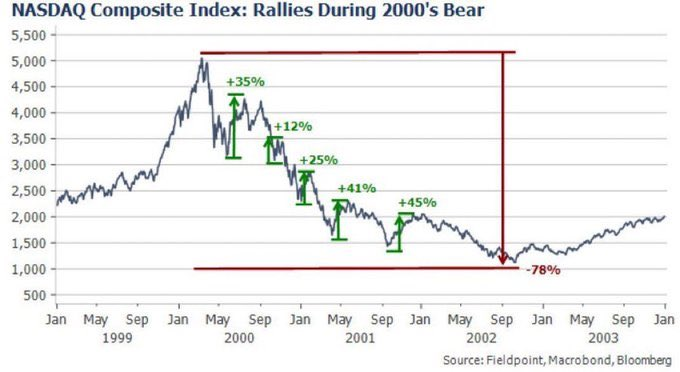

However, the anatomy of a Bear Market (we will not know until after the fact!) is that there are violent rallies.

As noted above, a classic and extreme example was when the Nasdaq declined by -78% (2000-2002) following the dot.com boom in which the revolutionary impact of the internet was heralded and applauded in the indexes.

Along the way to the nearly 80% drop, there were five robust rallies of between +12% and +45%. The average gain in the rallies was +33%.

Every rally felt like a bottom but every rally was a trap:

"It is always well to accept your own shortcomings with candor but to regard those of your friends with polite incredulity."

-Russell Lynes

In my Diary I share my views and try to attach empirical evidence and observations that support that outlook.

In the case of today's markets I am reminded of Warren Buffett's quote:

"What the wise do in the beginning, fools do in the end."

With the same intended message, Barton Biggs was more colorful when he said:

“A bull market is like sex. It feels best just before it ends.”

Citigroup's CEO Charles Prince — in July, 2007, only months before The Great Financial Crisis (and historic market decline) — had a different view (as reported in an interview he had with The Financial Times): “When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing."

That said, with the S&P Index making an all-time record in April — and despite my protestations — it is abundantly clear that neither the markets nor most market participants (human and machine) share my outlier and ursine outlook.

Market participants are still dancing and having sex.

Positions: Short SPY common (S)

BY Doug Kass · Apr 20, 2026, 9:35 AM EDT

Stanley Druckenmiller on AI in late 2024: "If we were all sitting here in 1999 talking about the Internet, I don’t think anybody would have estimated it would be as big as it got in 20 years. And yet, if you bought the Nasdaq in ’99, it went down 80% before that all came to… pic.twitter.com/lVOvSvxiWu

— Steve Burns (@SJosephBurns)

Position: None.

BY Doug Kass · Apr 20, 2026, 9:06 AM EDT

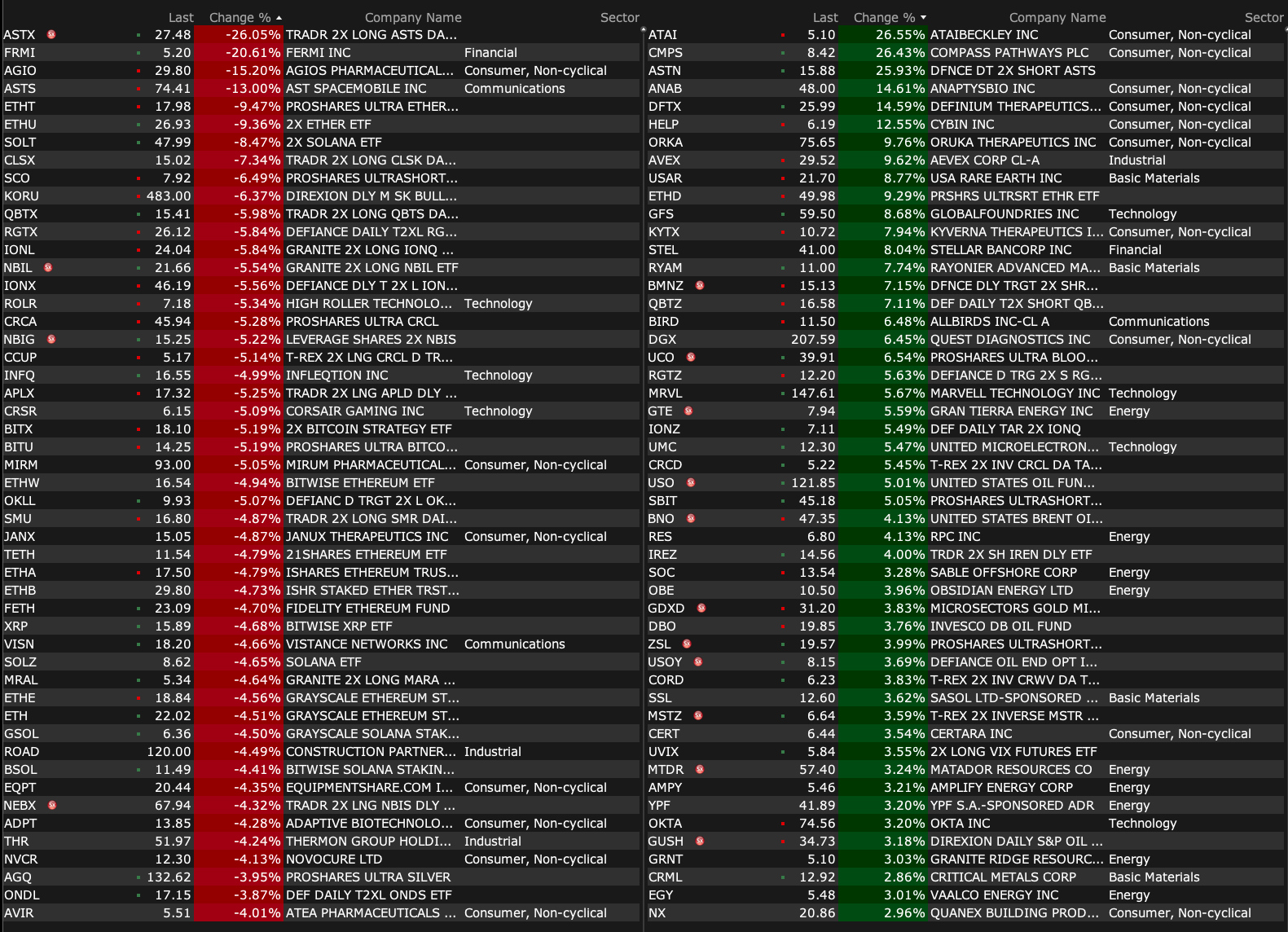

-PBM +104% (President Trump signs order to fast-track psychedelic drugs)

-ENVB +90% (President Trump signs order to fast-track psychedelic drugs)

-ATAI +27% (President Trump signs order to fast-track psychedelic drugs)

-CMPS +26% (President Trump signs order to fast-track psychedelic drugs)

-BLD +19% (QXO to acquire TopBuild in ~$17.0B transaction for $505/share in a cash and stock transaction)

-GHRS +19% (President Trump signs order to fast-track psychedelic drugs)

-NKTR +17% (52-Week Topline Results from 16-Week Blinded Treatment Extension of REZOLVE-AA Demonstrate Deepening of Responses in Severe-to-Very-Severe Alopecia Areata with Rezpegaldesleukin)

-DFTX +15% (President Trump signs order to fast-track psychedelic drugs)

-PRLD +15% (presents Preclinical Data from Development Candidate, PRT13722, a First-in-Class, Orally Bioavailable, Potent and Highly Selective KAT6A Degrader at American Association for Cancer Research (AACR) Annual Meeting 2026)

-BATL +11% (tracking crude rally over Middle East peace deal concerns)

-FLYX +11% (path cleared to close merger with Jet.AI in Q2)

-USAR +9.3% (acquires 100% of Serra Verde for $300M cash plus 126.8M shares implying $2.8B equity value; investor meeting guidance)

-MRVL +5.6% (Google said in talks with Marvell to develop two new chips for running AI models more efficiently as Google seeks to diversify away from Broadcom)

-SOC +3.8% (issues update on operations and debt refinancing)

-OKTA +3.2% (Barclays Raised OKTA to Overweight from Equal Weight, price target: $90)

-MDA +2.2% (Airbus selects company to design, build >880 Ka-band steerable antennas and 440 Ku-band user replacement antennas for the OneWeb LEO constellation owned by Eutelsat)

-FRMI -20% (CEO departs; Board forms interim CEO office and expands board)

-AGIO -15% (rival Novo Nordisk reports late-stage data for sickle cell disease drug)

-ASTS -13% (addresses orbital launch of BlueBird 7 on the New Glenn launch vehicle; notes altitude is too low to sustain operations with its on-board thruster technology and will de-orbited)

-SRFM -11% (guidance; files to sell $15M registered direct offering of common stock a new asset-backed loan)

-DOCS -3.4% (Truist Cuts DOCS to Hold from Buy, price target: $29 from $37)

-CALM -3.2% (reportedly DOJ preparing an antitrust case against some large egg producers over alleged price coordination, including Cal-Maine and Versova)

-QBTS -3.1% (quantum name broad weakness)

-UAL -2.9% (AAL denies merger discussions with UAL)

-QXO -2.2% (QXO to acquire TopBuild in ~$17.0B transaction for $505/share in a cash and stock transaction)

Positions: None.

BY Doug Kass · Apr 20, 2026, 8:58 AM EDT

Positions: None.

BY Doug Kass · Apr 20, 2026, 8:55 AM EDT

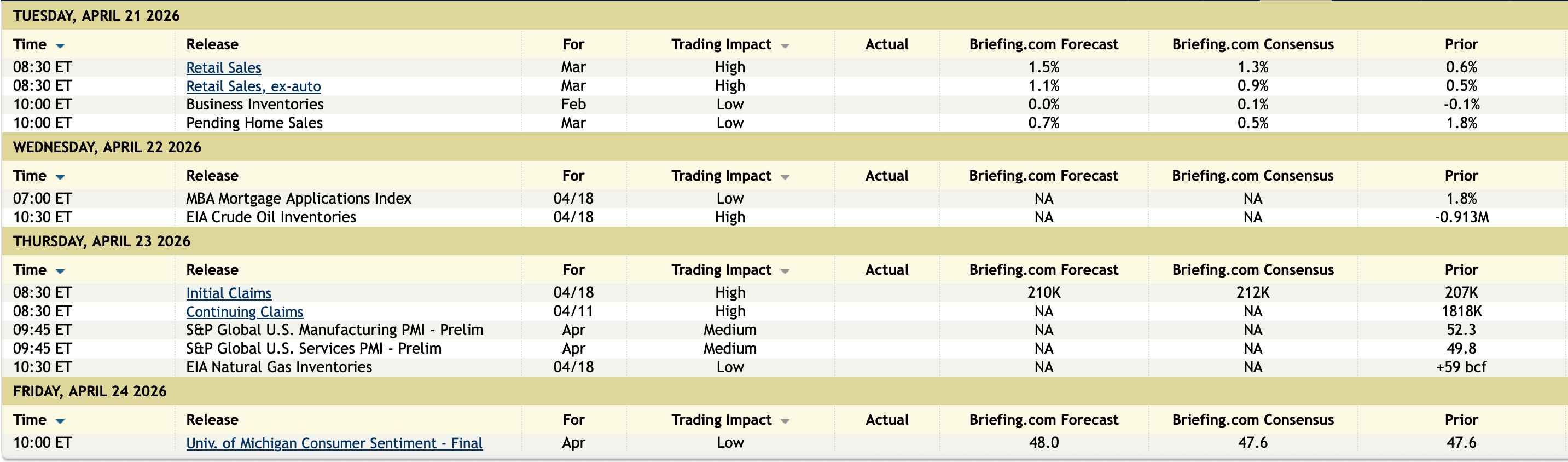

11:30 a.m.: Treasury hosts a $89B 3- and $77B 6-Month Bill Auction

11:30 a.m.: Federal Reserve Board of Governors holds a Board Meeting: Review and determination by the Board of Governors of the advance and discount rates to be charged by the Federal Reserve Banks.

None.

BY Doug Kass · Apr 20, 2026, 8:39 AM EDT

Positions: None.

BY Doug Kass · Apr 20, 2026, 8:28 AM EDT

Chart of the Day: XLK

The Technology Sector ETF (XLK) just logged its 13th consecutive up-day, matching the longest winning streak in its history.

Over that stretch, it’s surged more than +20%, a move typically seen at major bear market lows like the Dot-Com crash, the Great Financial Crisis, and the COVID crash.

What makes this instance unique is that it’s occurring at all-time highs rather than within a large drawdown, highlighting the overwhelming demand in the market's most important sector.

The Takeaway: The tech sector is exhibiting historically strong upside momentum, with a 13-day winning streak and gains exceeding 20%.

- Scott Brown, CMT (@scottcharts) / X

S&P 500 from brief Stage 4 breakdown attempt to Stage 2 breakout attempt in just 3 weeks. $SPY $SPX pic.twitter.com/SriaoNbdwl

— Stage Analysis (@stageanalysis)

$SPY $QQQ $IWM

— BACH (@CyclesWithBach)

"Three White Soldiers"

Extremely rare. Extremely powerful. Extremely bullish!

Melt-up still alive and well 🚀 pic.twitter.com/341l2nXlrC

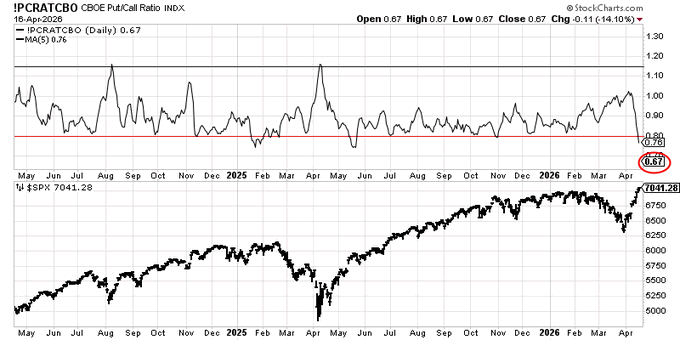

The 5-day put/call ratio has collapsed while the market rallied and is into the "complacency zone." The one-day reading of 0.67 is also deep into that zone. I sometimes have tried to ignore this in the past because I don't want it to get any harder, and it feels too good with… pic.twitter.com/a4pTky0Pwq

— Wesley Mattox, CFA, CMT (@WesleyJMattox)

$QQQ on the loose. pic.twitter.com/p7qwupVrIL

— Mark Ungewitter (@mark_ungewitter)

$IGV Software best week since 2001

— Mike Zaccardi, CFA, CMT 🍖 (@MikeZaccardi)

+16% pic.twitter.com/jtL8G8dkVx

What rose with oil is now falling with oil.$WTI $DXY https://t.co/4uLuC4Nyqh pic.twitter.com/ohPDjCYdF2

— Randy Dunham (@itmrandy)

Stunning chart and comments from GS:

— Macro Charts (@MacroCharts)

- CTAs bought more than $86Bn in global equities over the past five sessions — one of the biggest buying sprees on record.

- *My notes*: remember GS’ trading desk *projected* this would happen, one week in advance. Hats off to them.

- Brian… pic.twitter.com/77AKJKqFZs

Bonus — Here are some great links:

BY Doug Kass · Apr 20, 2026, 6:50 AM EDT

On March 30, the S&P 500 was down 7% in 2026, the 12th worst start to a year in history. After one of the biggest 3-week rallies ever, it's now up +4.5% YTD and above the average year at this point in time (+3%). There is no impossible in markets. $SPX pic.twitter.com/90ODFJDMGw

— Charlie Bilello (@charliebilello)

BY Doug Kass · Apr 20, 2026, 6:40 AM EDT

Valuations are a terrible clock but a good weather forecast:

BY Doug Kass · Apr 20, 2026, 6:30 AM EDT

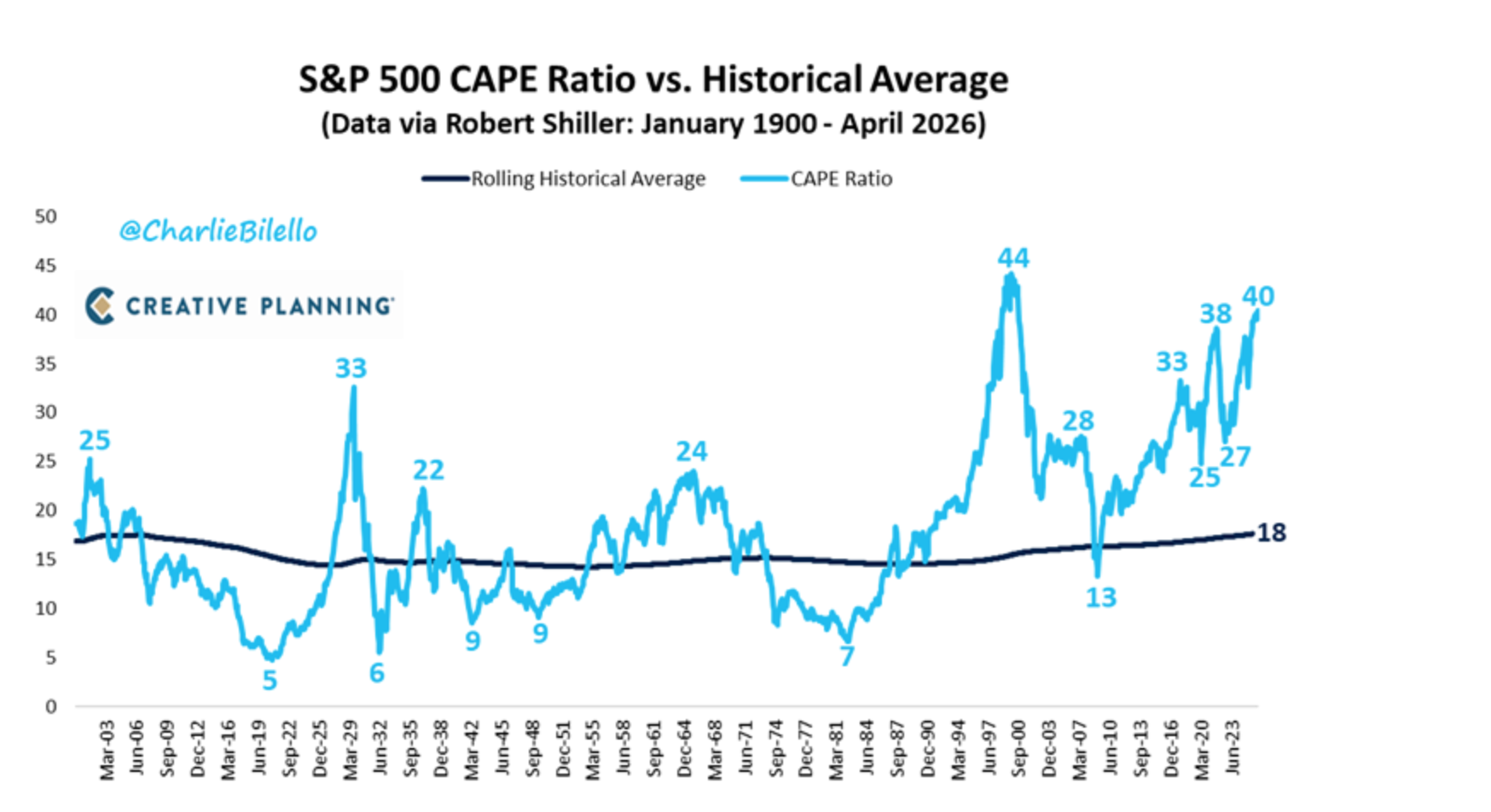

The S&P 500's CAPE Ratio has moved up to 40, its highest level since 2000 and now above 99% of historical valuations. $SPX pic.twitter.com/uhUt33SCp5

— Charlie Bilello (@charliebilello)

BY Doug Kass · Apr 20, 2026, 6:20 AM EDT

The S&P 500 is at an all-time high while Consumer Sentiment is at an all-time low.

— Charlie Bilello (@charliebilello)

We've never seen a gap this wide between Wall Street and Main Street. pic.twitter.com/BPu6ncbG9F

BY Doug Kass · Apr 20, 2026, 6:13 AM EDT

The S&P Short Range Oscillator remains in deep overbought territory at 7.89% vs. 6.68%

Position: Short SPY common (S), QQQ common (S)

BY Doug Kass · Apr 20, 2026, 5:58 AM EDT

While not near recessionary territory yet, real personal consumption expenditures continue to weaken. Such will likely feed into earnings and economics in the quarters ahead if it gets weaker. The trailing 3-month growth rate through February is annualizing at just 0.8%.

The 5-day put/call ratio has collapsed while the market rallied and is into the "complacency zone." The one-day reading of 0.67 is also deep into that zone. I sometimes have tried to ignore this in the past because I don't want it to get any harder, and it feels too good with Show more

Goldman Sachs on stocks/economy: "Relative to the pre-war period, we expect lower growth, higher inflation, higher long-term oil prices, and somewhat higher policy rates, at least in the near-term. Rising earnings expectations have also lowered US equity valuations. This makesShow more

US small businesses are pulling back on investment as if we are in a crisis: In March, only 16% of small businesses said that they plan on investing in CapEx over the next 6 months, the lowest reading since November 2009. This percentage has declined -12 points since November Show more

Professional investors are rushing back into equities: US equity positioning jumped +0.55 points last week, the largest weekly increase in 8 years. This metric covers institutional investors like fund managers, hedge funds, and algorithm-based trading strategies. Since 2010, Show more

On March 30, the S&P 500 was down 7% in 2026, the 12th worst start to a year in history. After one of the biggest 3-week rallies ever, it's now up +4.5% YTD and above the average year at this point in time (+3%). There is no impossible in markets. $SPX

📢 "You’re going to get the rescheduling done, right, please? Will you get the rescheduling done, please? You know they’re -- Joe [Rogan], they're slow-walking me on [cannabis] rescheduling. You’re going to get it done, right?" - @POTUS "Absolutely." - presumably DOJ off camera

The S&P 500's CAPE Ratio has moved up to 40, its highest level since 2000 and now above 99% of historical valuations. $SPX

$QQQ on the loose.

Stanley Druckenmiller on AI in late 2024: "If we were all sitting here in 1999 talking about the Internet, I don’t think anybody would have estimated it would be as big as it got in 20 years. And yet, if you bought the Nasdaq in ’99, it went down 80% before that all came to Show more

$IGV Software best week since 2001 +16%

Stunning chart and comments from GS: - CTAs bought more than $86Bn in global equities over the past five sessions — one of the biggest buying sprees on record. - *My notes*: remember GS’ trading desk *projected* this would happen, one week in advance. Hats off to them. - Brian Show more

Oil is the common thread behind the market's recent headwinds. h/t @DualityResearch for being one of the first to highlight this.

Neither overboughts/oversolds nor sentiment/surveys are good clocks... but they are (especially in the extreme) a good weather forecast .. S&P Short Range Oscillator at close stands at 7.61% - very overbought. @SquawkCNBC @andrewrsorkin @BeckyQuick @CNBCFastMoney @HalftimeReport Show more