Fed cuts as they raise economic forecasts and also catches up to market pricing/Yields are jumping

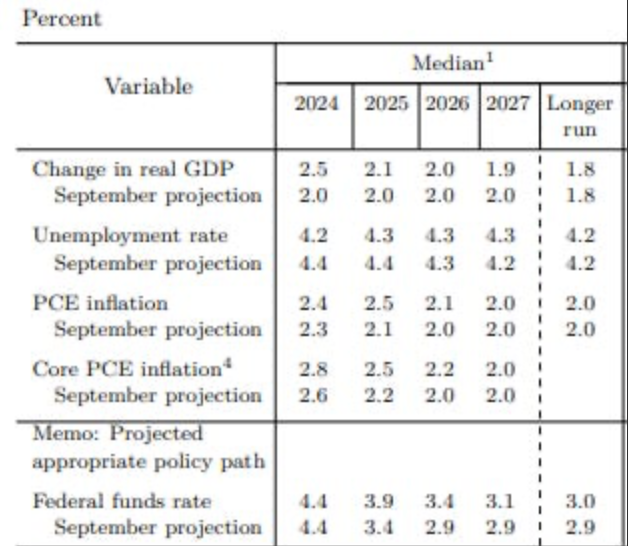

The FOMC statement was about identical to what they said in November as they cut rates again even though they raised their 2024 GDP forecast to 2.5% from 2%, lowered their unemployment rate estimate to 4.2% from 4.4%, increased their headline PCE forecast to 2.4% from 2.3% and the core rate from 2.6% to 2.8%.

So, all their estimate changes should have pointed to a pause but they cut anyway and, I guess, Jay Powell at 2:30 p.m. will help us better understand. Also of note for 2025, and we take with a grain of salt, they increased a touch their GDP forecast to 2.1% from 2%, lowered their unemployment rate estimate to 4.3% from 4.4% and raised their headline PCE guess to 2.5% from 2.1% and the core rate also to 2.5% from 2.2%. The 2025 median dot plot for the fed funds rate now stands at 3.9% from 3.4%. I’m not going to bother with the 2026 estimates as it’s too far out in time.

Finally of interest, Beth Hammack dissented and did not want a cut and I’m surprised that Bowman didn’t dissent either.

Bottom line, as stated, Powell needs to reconcile the change in their economic forecasts with his desire to cut rates again. That said, the Fed’s median dot plot has now squared up with where the fed funds futures are pricing, that being just two more cuts in 2025 to 3.83%. At its most dovish pricing a few months ago, the December 2025 fed funds contract had a fed funds rate of about 2.80%, so the market and corroborated by Fed estimates, has taken back about 100 bps of cuts.

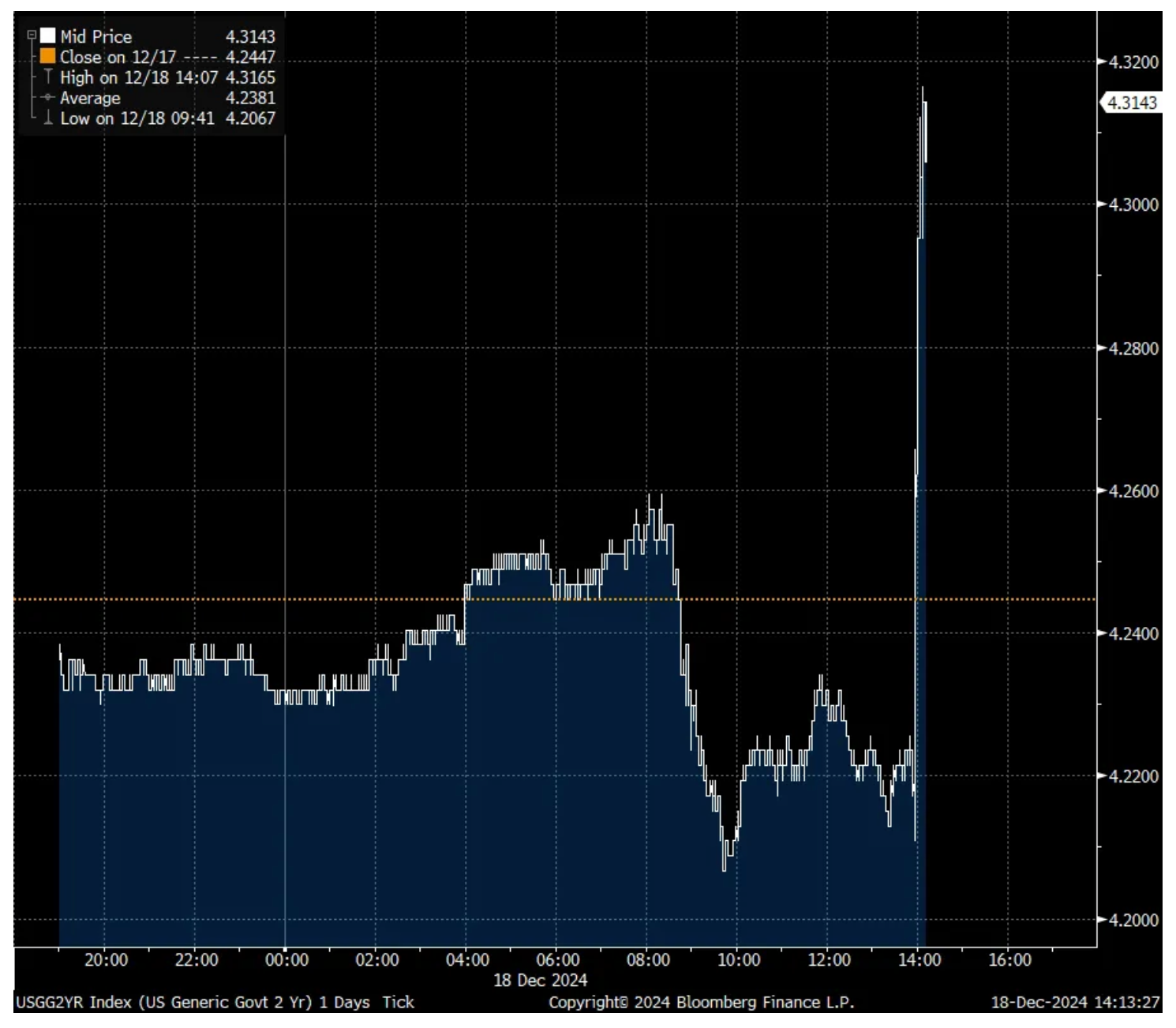

Rates are jumping in response, I’m guessing because of the upward economic forecasts and the Fed catching up to the markets by taking away some cuts. The 2 yr yield has jumped 10 bps in seconds to 4.32% and the 10 yr yield is at 4.45% from 4.40% right before.

Dougie, respectfully disagree with your negative view of 0DTE options. They are more than speculative tools. They are also hedging tools for very near term news expectations. The mkts are deep, and there are counter parties to all option contracts. Thinking 0DTE options are disruptive would lead one to assume that longer dated ones could be included in your argument. And of course, I disagree. (discl: I am a former member of CBOE)...But always respectful of your views. I am your greatest admirer...even if I occasionally (rarely) disagree with you.

TechNova

I think Dougie's point is that 0DTE's allow for market manipulation by forcing the market makers to hedge on the underlying asset.

TSLA has been a great beneficiary of this caveat.

Dougie Kass

Precisely.

Moreover, for the most part, these 0DTEs are hedged with 0DTEs. However, if someone big gets caught offsides one day, 0DTE could cause a nasty cascade of a sell. A 5+% downside day is likely at some point. For now though, the party rages on.

1)From the November Fed Beige Book, "Economic activity rose slightly in most Districts. Three regions exhibited modest or moderate growth that offset flat or slightly declining activity in two others."

2)On the labor market from the Beige Book, "Employment levels were flat or up only slightly across Districts. Hiring activity was subdued as worker turnover remained low and few firms reported increasing their headcount."

3)On inflation from the Beige Book, "Prices rose only at a modest pace across Federal Reserve Districts. Both consumer-oriented and business-oriented contacts reported greater difficulty passing costs on to customers."

4)The average interest rate being paid on a credit card is 23%, consumers need relief.

5)Small businesses are paying on average 9-10% for a loan, costly. Many commercial real estate owners/investors are in financial pain.

6)The average 30 yr mortgage rate is back above 7% according to Bankrate and existing home sales are around 30 yr lows.

7)The low to middle income consumer is financially stretched.

8)The US manufacturing recession is now past two years.

9)Capital spending outside of AI continues to flat line.

10)Global trade is punk with particular weakness in Germany, France and China.

11)Get in one more rate cut before a time out.

Don't cut,

1)Parts of the stock market are very frothy with speculation rampant. The forward multiple of the S&P 500 almost at 23x is approaching the March 2000 peak of 24.5x.

2)The high yield credit spread to US Treasuries is just 270 bps. It got down to 262 bps in July 2021.

3)We have Trump 2.0 back in town, wait to cut again after you see what fiscal policies and tariffs come our way. Why move before then?

4)Higher income consumers are spending like there is no tomorrow, particularly on leisure/hospitality but after the Fed cuts again today will have lost 100 bps of interest income in their money market funds over the past few months. On $6.77 trillion of money market assets, that is a lost $67.77 billion of interest income. Maybe one less cruise from that retired boomer couple.

5)The Atlanta Fed currently estimates that GDP is expected to rise by 3.1% in Q4 after a 2.8% performance in Q3.

6)Capital spending on anything AI is robust, especially from the hyperscalers.

7)Government spending continues to exceed tax receipts by almost $2 billion which is temporarily economic boosting and inflationary.

8)Core CPI is stuck at 3.3%. Yes, rental growth should continue to moderate but goods prices might be stabilizing and PPI continues to rise. Particularly on used car prices, Manheim said this yesterday, "We've continued to see tighter wholesale supply at Manheim over the last several weeks, and it has further declined in early December as sales conversion remains elevated...this is our second report in a row with the Manheim Used Vehicle Value Index exhibiting higher values y/o/y, so it appears we've seen the bottom in wholesale prices for now."

9)Historically, the REAL rate (aka, neutral rate) was around 200 bps. With a cut today and vs core CPI it will be around just 100 bps. The Fed is relying on PCE instead which is flawed because of the 20% healthcare component so they might cut 50-100 bps more than they should.

10)The pace of firing's remains muted as measured by jobless claims.

11)M2 money supply remains 16.5% above its long-term trend line.

Bottom line, with so many cross currents, the Fed should sit tight until they gain more confidence on how all this plays out.

Overseas, Bank Indonesia and the Bank of Thailand each kept rates unchanged as expected at 6% and 2.25% respectively.

Japan's exports in November lifted by 3.8% y/o/y, above the estimate of 2.5%, boosted by the weak yen as volumes actually fell by .1% y/o/y. Export volume to the US fell 9.5% and by 14.2% to the EU, led by lower auto shipments. Exports to China fell 6.4% but was offset by a lift to other Asian countries by 4.4%. Nothing market moving as we await the BoJ announcement tomorrow. Rate hike odds are down to just 12%.

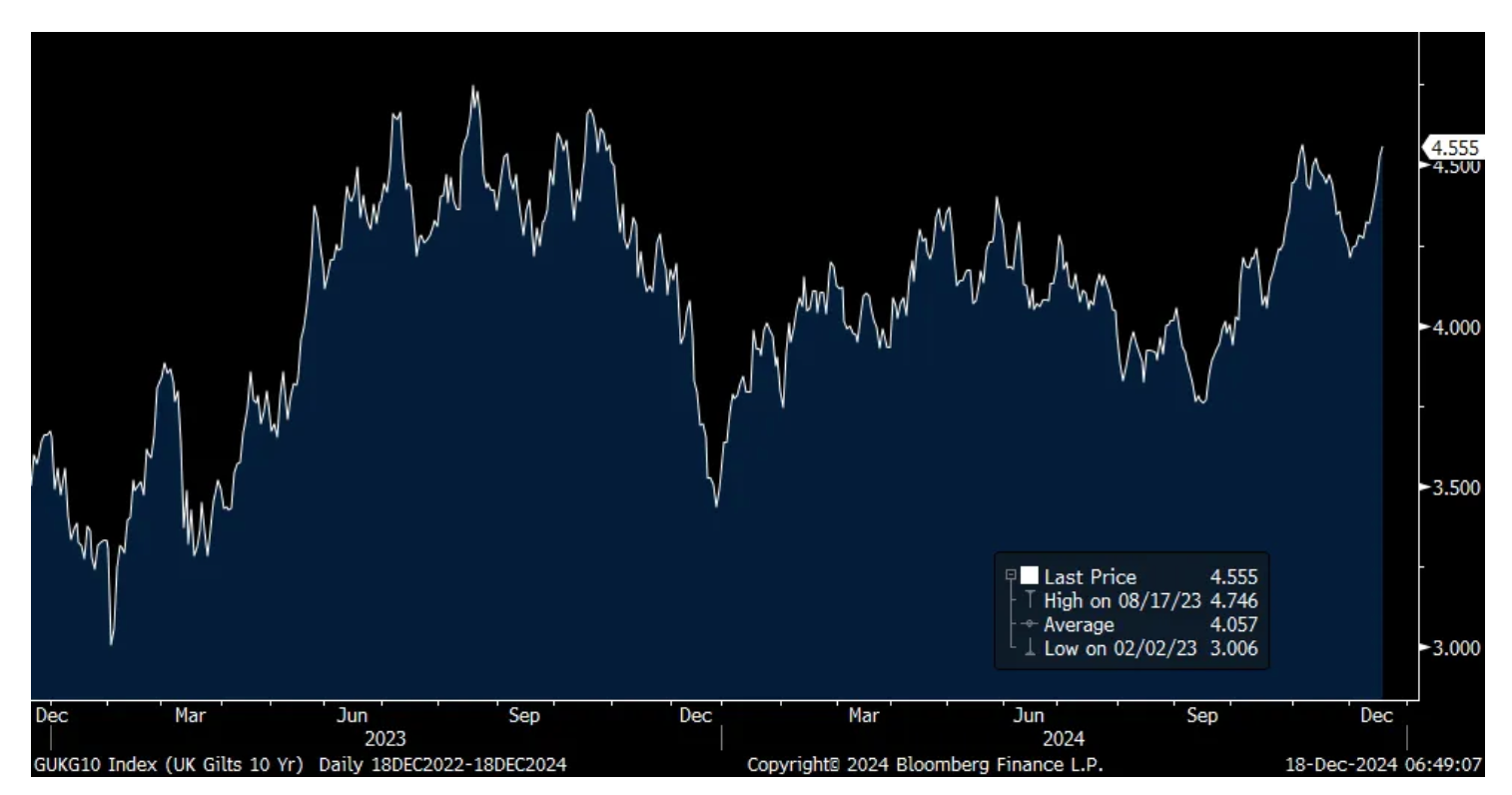

The market expects the Bank of England to sit tight tomorrow and after today's November CPI data, that is most likely going to be the case. Headline CPI rose 2.6% y/o/y as expected but up from 2.3% in October. Core CPI was higher by 3.5% vs 3.3% in the month before but one tenth less than anticipated. Services inflation in particular was up by 5%. Wholesale prices, both output and input charges, were as expected.

While the inflation data was about in line, the 10 yr gilt yield is rising by another 3 bps to 4.55%, just one bp from the highest level since October 2023. The pound is up a touch as are UK stocks.

* So attractive one day and not attractive the next.

* "Have you come across this? Yes I am familiar with this syndrome. She is a Two Face!"

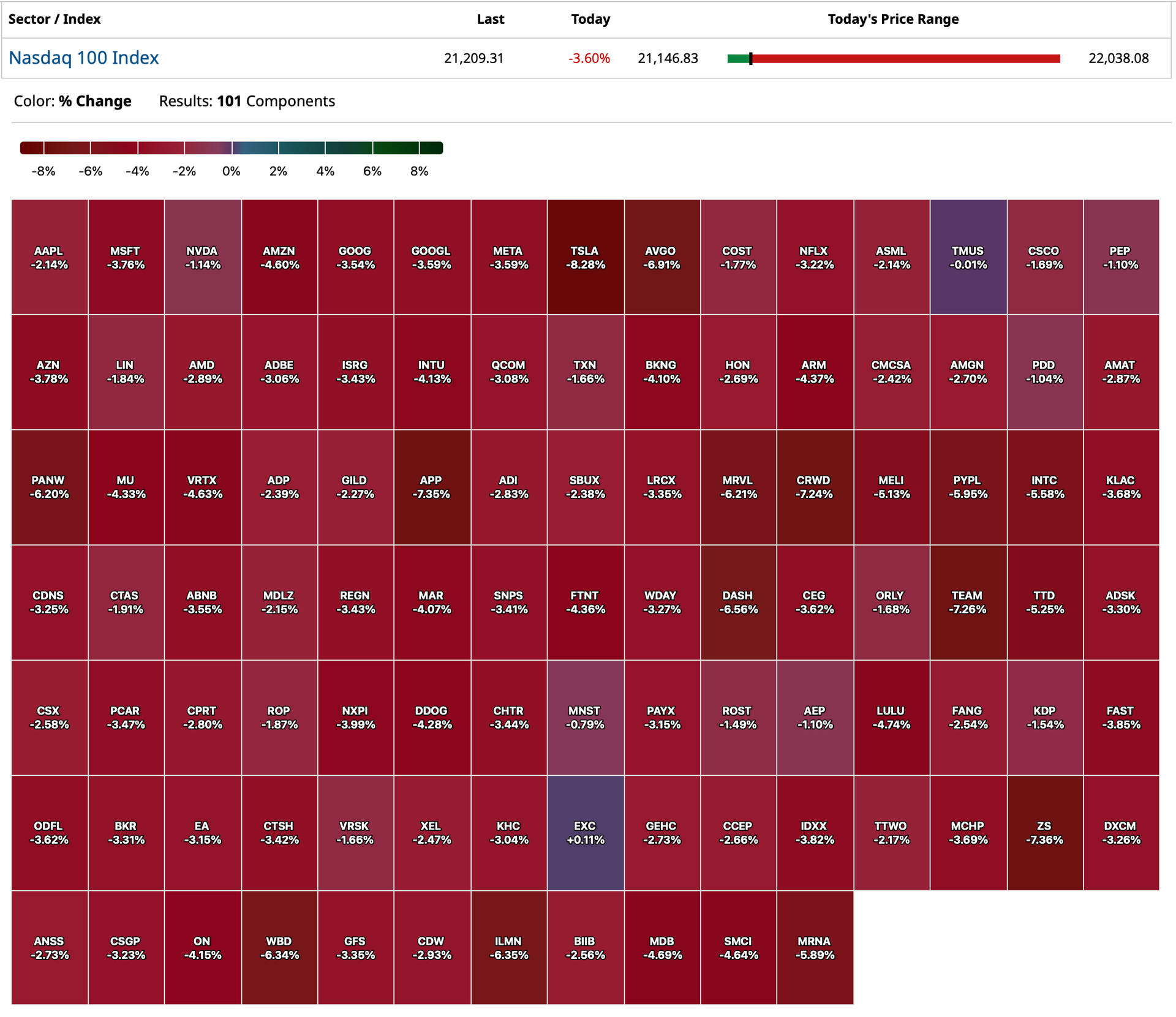

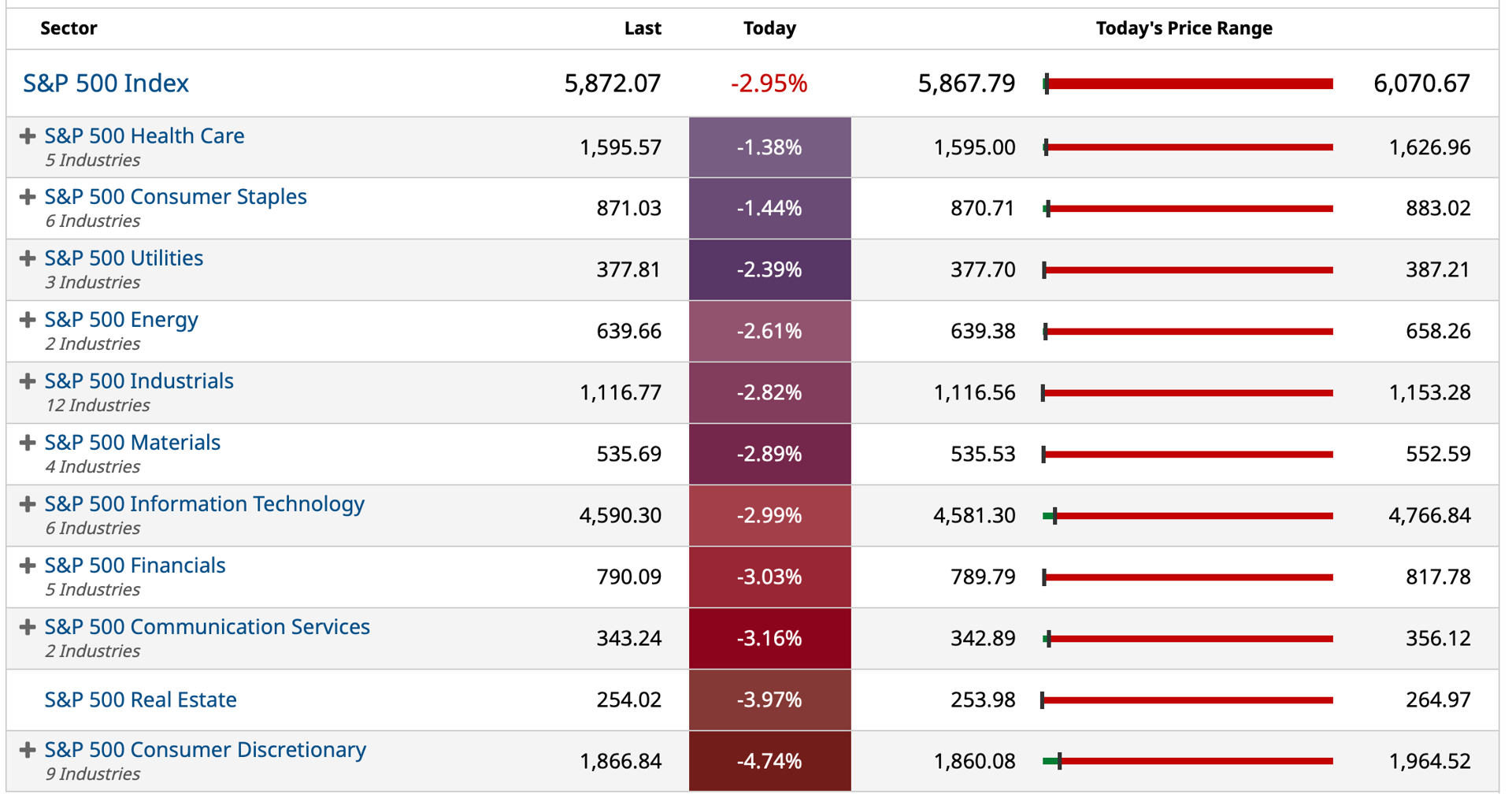

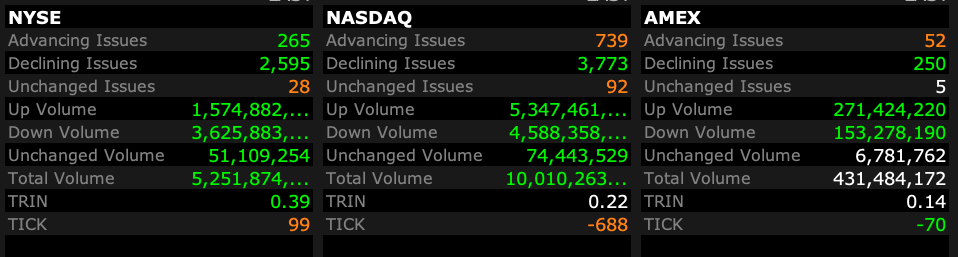

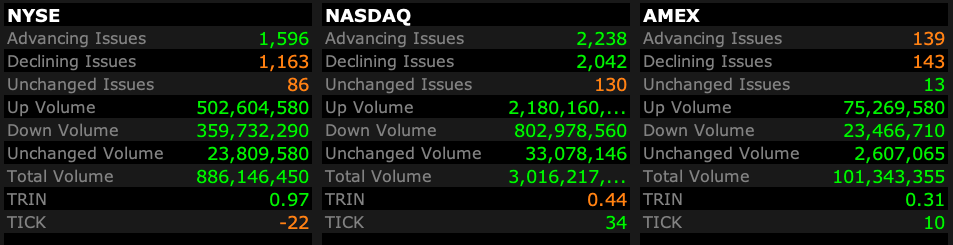

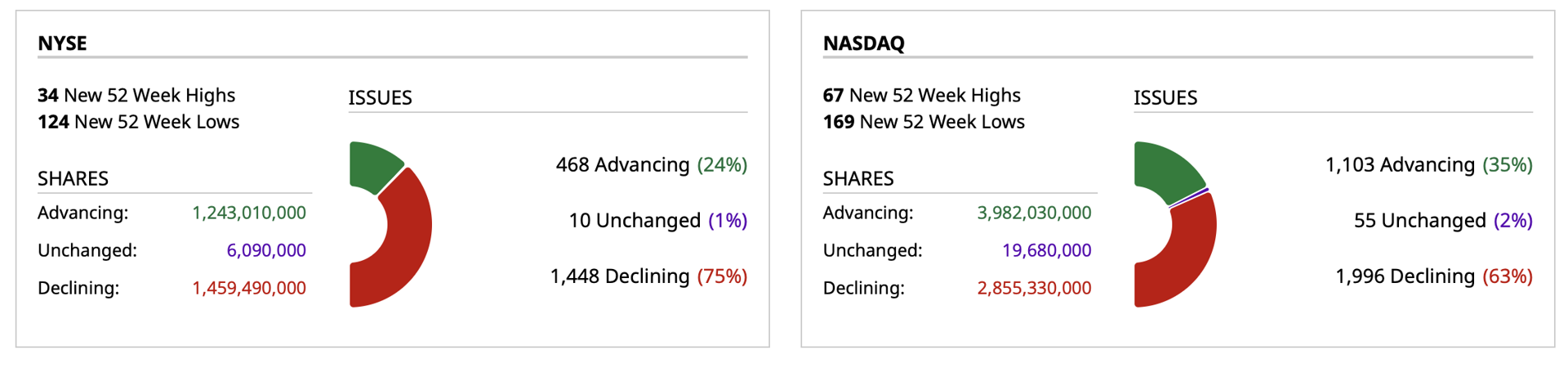

* Every day in December the overall market has had negative breadth though the S&P and Nasdaq have held up — my bet is that the senior averages "ketchup" to the downside in the time ahead...

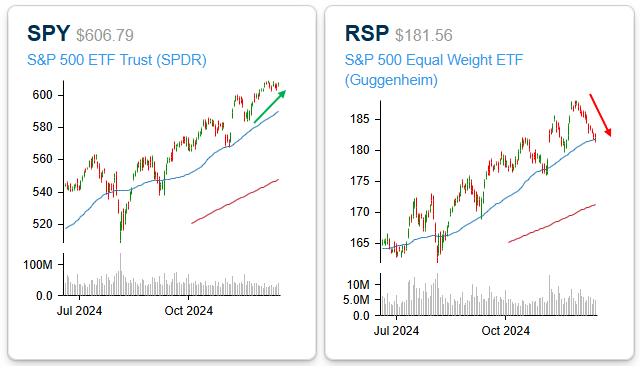

The S&P Value ETF IVE is now down by 12 days in a row — the longest daily decline in history:

So depending upon the "type" of exposure one has in today's market, investors may be seeing the attractive (S&P) or the unattractive girls (RSP/Value)..."Gwen, really?"

Or...

"Boy, am I glad to see you.. this is a good looking booth."

Bottom Line

That said, with overall market breadth lower in each trading session this month, my view is that the good-looking senior averages (S&P and Nasdaq) may soon play "ketchup" to the downside with the other ugly segments of the market that have been faltering.

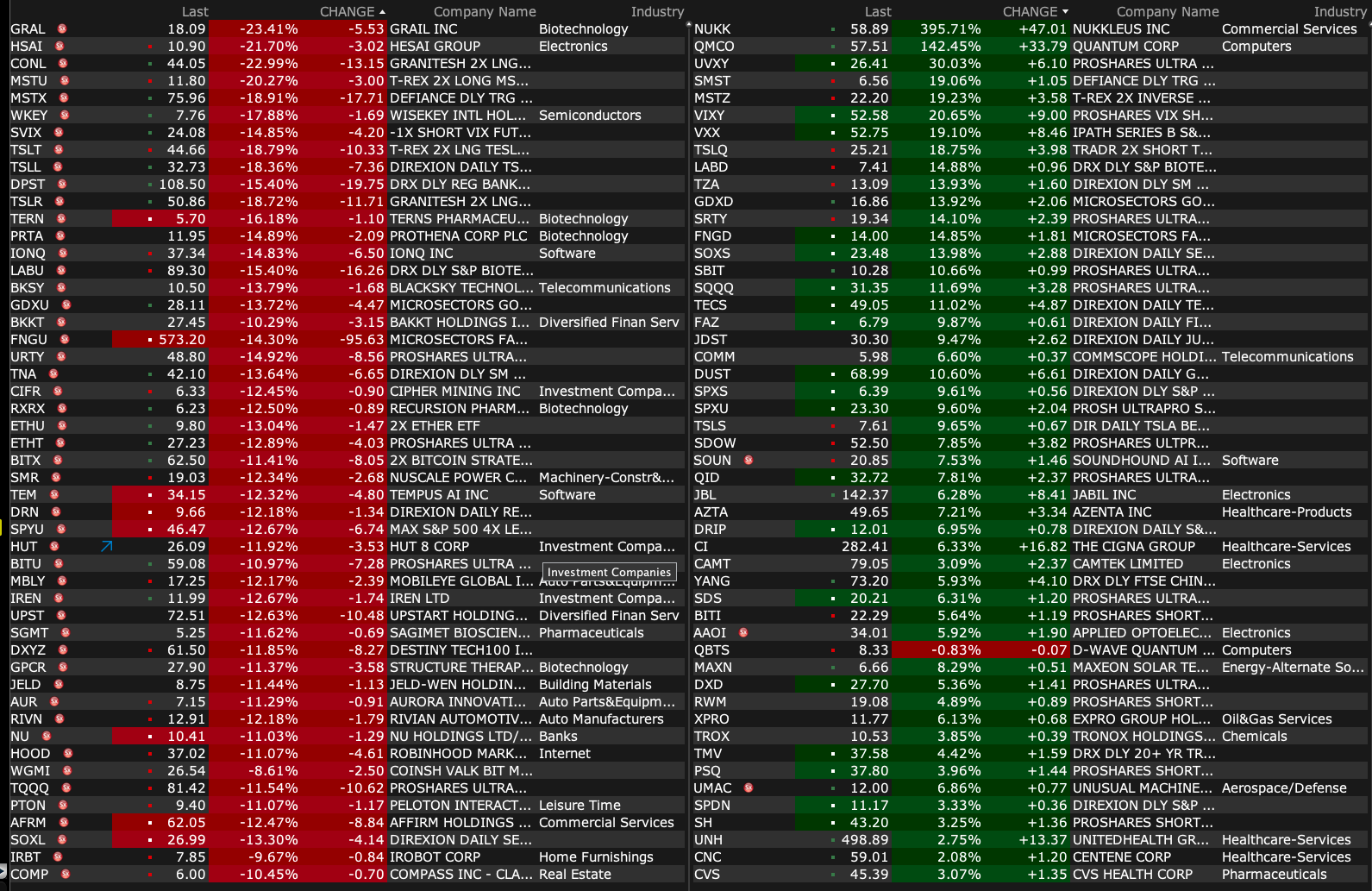

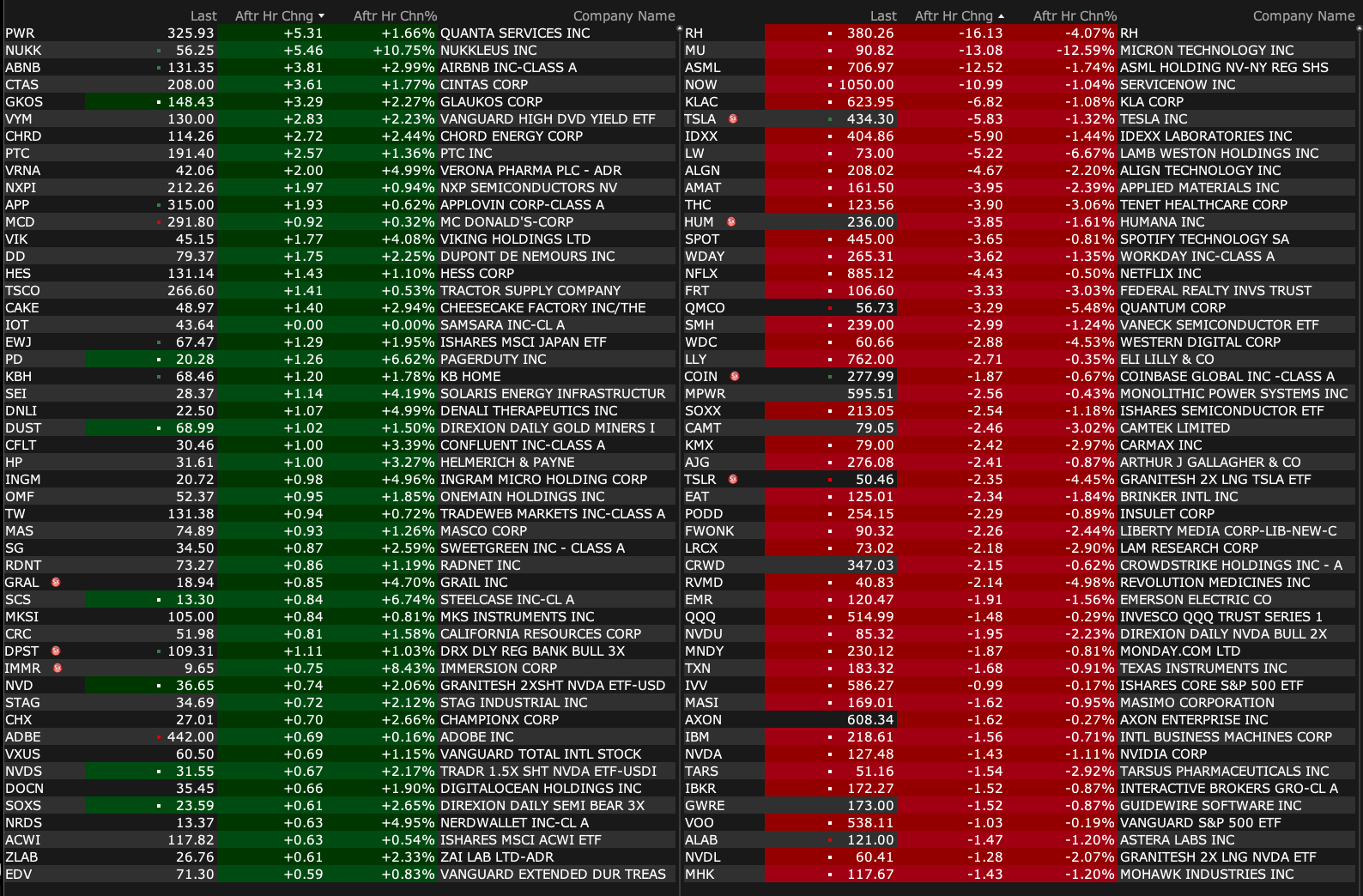

-PLRZ +175% (moving forward with expected 2025 clinical trial; entered manufacturing agreement for its PL-14 Allergy Blocker)

-CGTX +129% (announces topline results from the exploratory Phase 2 ‘SHIMMER’ study demonstrating CT1812 produced strong therapeutic responses across behavioral, functional, cognitive, and movement measures in patients with dementia with Lewy bodies (DLB))

-COMM +22% (closes comprehensive refinancing with first-lien secured lenders)

-NTGR +17% (US reportedly considering ban on Chinese made routers from TP-Link)

-OKLO +15% (forms strategic relationship with Switch to deploy 12 GW of Advanced Nuclear Power)

-WOR +14% (earnings)

-CHPT +11% (ChargePoint and General Motors collaborate to install hundreds of EV Fast Charging Ports)

-JBL +9.4% (earnings, guidance)

-OGI +9.3% (earnings)

-INBS +8.8% (announces 510(k) Submission to US FDA for Fingerprint Sweat-Based Drug Screening Technology)

-NURO +8.8% (to be acquired by electroCore)

-BIRK +7.9% (earnings, guidance)

-EOSE +7.7% (secures 400 MWh order with International Electric Power to Deliver Critical Resilience in California)

-NSANY +5.7% (reportedly Honda Motor and Nissan Motor entered into merger talks in order to rule out the risk of an acquisition by Taiwan's Hon Hai Precision Industry)

-EXPE +3.5% (Tier1 firm Raised EXPE to Buy from Neutral, price target: $221 from $187)

-OLLI +3.2% (CitiGroup Raised OLLI to Buy from Sell, price target: $133)

-NVDA +2.7% (introducing $249 version of Jetson computer for AI, down from $499)

-NKLA +2.5% (announces West Sacramento station, marking HYLA's first modular refueling station in Northern California)

-QTWO +2.3% (Keybanc/Pacific Crest Raised QTWO to Overweight from Sector Weight, price target: $126)

Downside:

-CRVS -27% (announces interim data from placebo-controlled phase 1 clinical trial of Soquelitinib for Atopic Dermatiti)

-NOTV -18% (priced 6M shares secondary at $4.25/shr)

-APDN -14% (earnings, guidance; announces strategic restructuring of business ops)

-TTC -8.0% (earnings, guidance)

-PESI -7.7% (prices 2.2M shares at $10.0/shr in $22M public offering)

-HEI -5.6% (earnings)

-CARA -5.2% (enters into into Merger Agreement with Tvardi Therapeutics)

-GIS -4.1% (earnings, guidance)

-QMCO -3.7% (announces support for NVIDIA GPUDirect Storage with myriad all-flash file system)

-HMC -3.1% (reportedly Honda Motor and Nissan Motor entered into merger talks in order to rule out the risk of an acquisition by Taiwan's Hon Hai Precision Industry)

-ABM -2.2% (earnings, guidance)

-BYON -2.0% (hearing Argus Cuts BYON to Sell from Hold)

-TSLA -1.9% (China factory head Song Gang expected to 'depart' this week)

As I have been observing for the last week (or more), market breadth is stinking up the joint — with 3-1 losers on the NYSE and 2-1 decliners on the Nasdaq:

(RSP) (equal weighted S&P Index) dropped by -0.8% while the Russell wasn't crowing ( (IWM) -1.16%).

VIX rose by +1.19 to 15.89.

Investors that appear in the business media are universally bullish.

Investors' cash positions are slimmer than at any point in years and the equity risk premium is paper thin.

There are few bears and no one I know that expects a serious market drawdown.

Nvidia (NVDA) , the former league leading hitter, is lower for the 7th or 8th day in a row and its chart looks worrisome (inverse head and shoulders?).

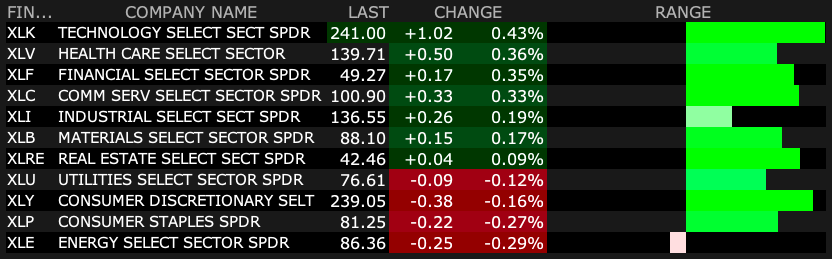

Financials, a favored "value proposition" appear to be rolling over.

Homebuilders, which were also league leaders (and favored by the "talking heads" in the business media) are now down 25% from their highs.

There is plenty of speculation in certain quarters (including several of the annointed large-cap tech stocks) as well as, arguably, in a number of secondary and tertiary cryptocurrencies. Elon Musk's proximity to the President-elect is justifying a $600 billion + increase in Tesla's (TSLA) market cap).

Market structure, equity inflows and animal spirits have conspired to move the market robustly since the November election — but with it overall risks are raised.

Inflation remains sticky and the U.S. may not be an island of prosperity as the world's economies deteriorate.

"Slugflation" remains my baseline expectation.

A valuation reset and not an EPS reset has resulted in a forward P/E multiple of 22.6x, which, to many is now acceptable — even though most valuation metrics that have stood the test of time are in the 96%-tile.

A new investment paradigm is being heralded.

Excesses are never permanent and I remain cautious on the markets and of the view that risk dwarfs reward.