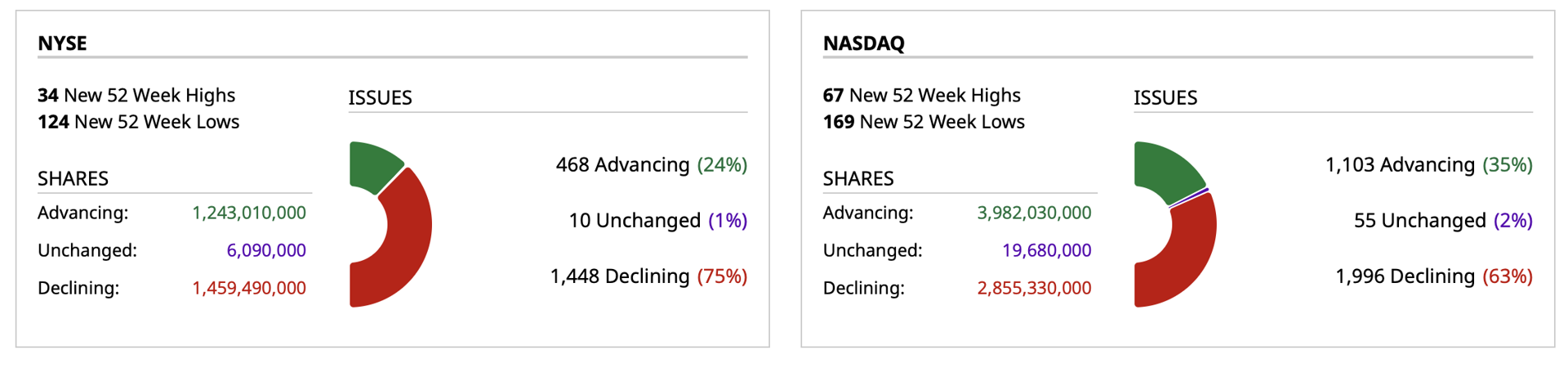

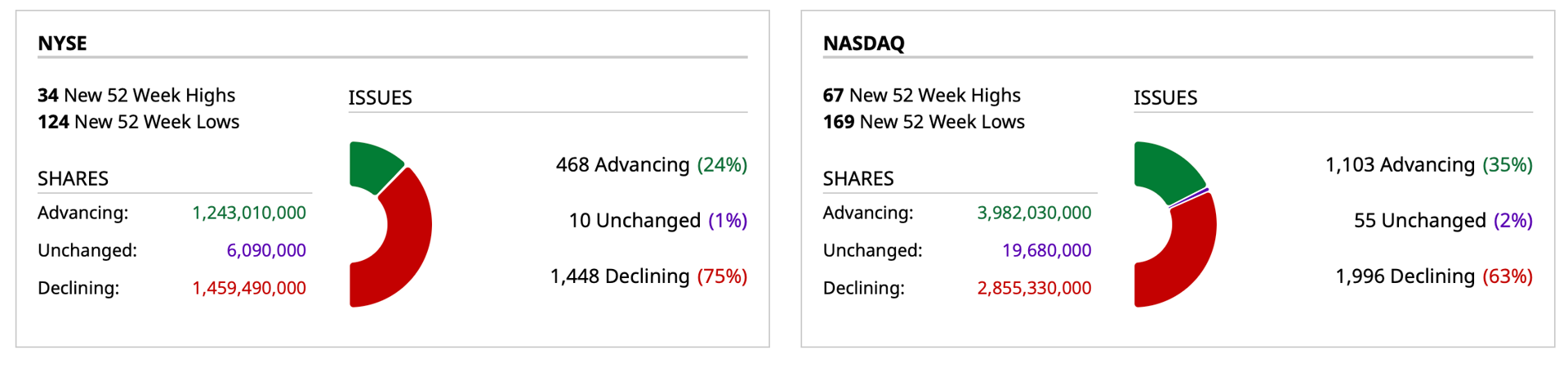

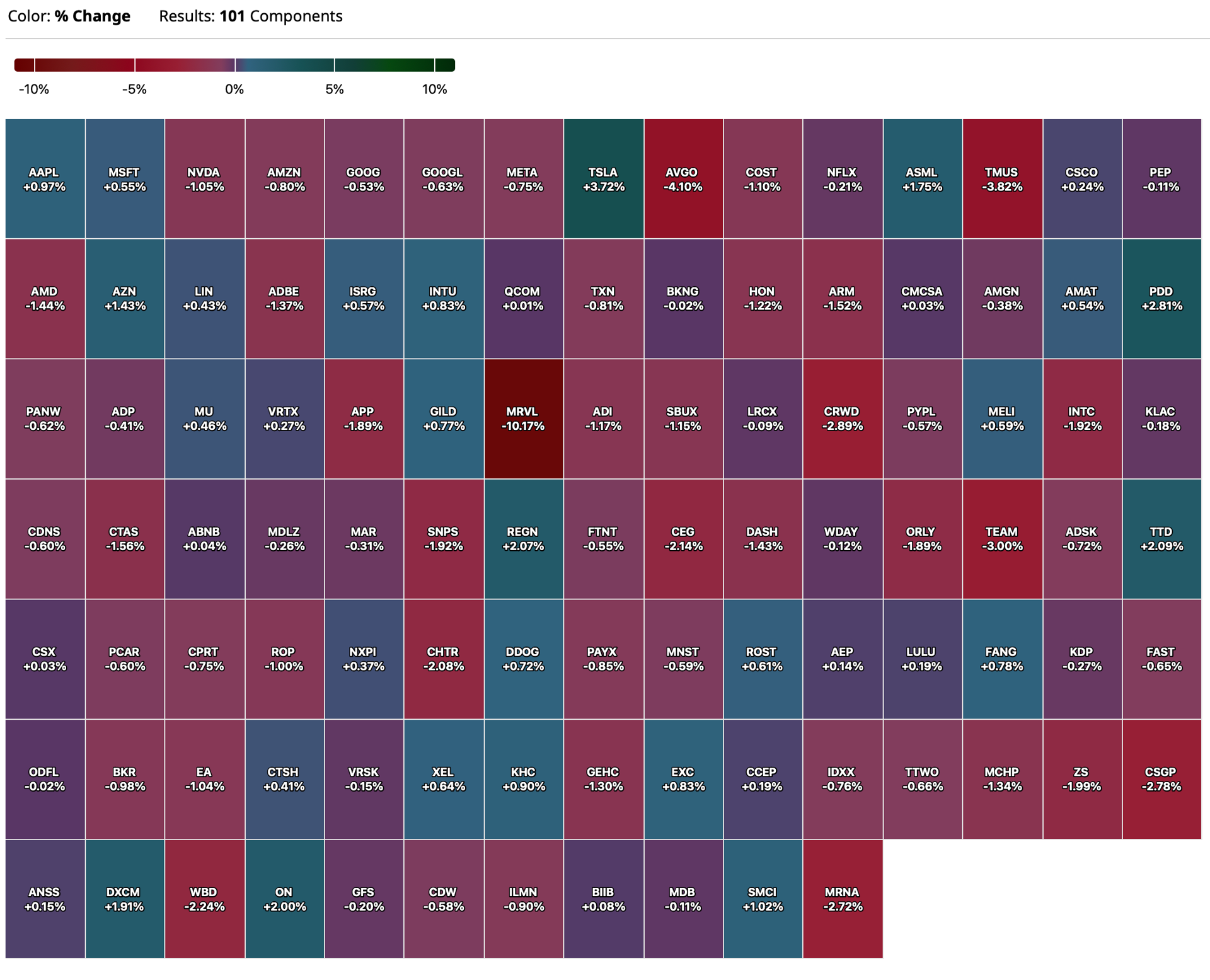

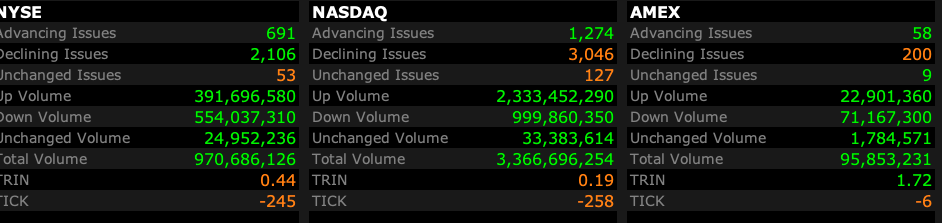

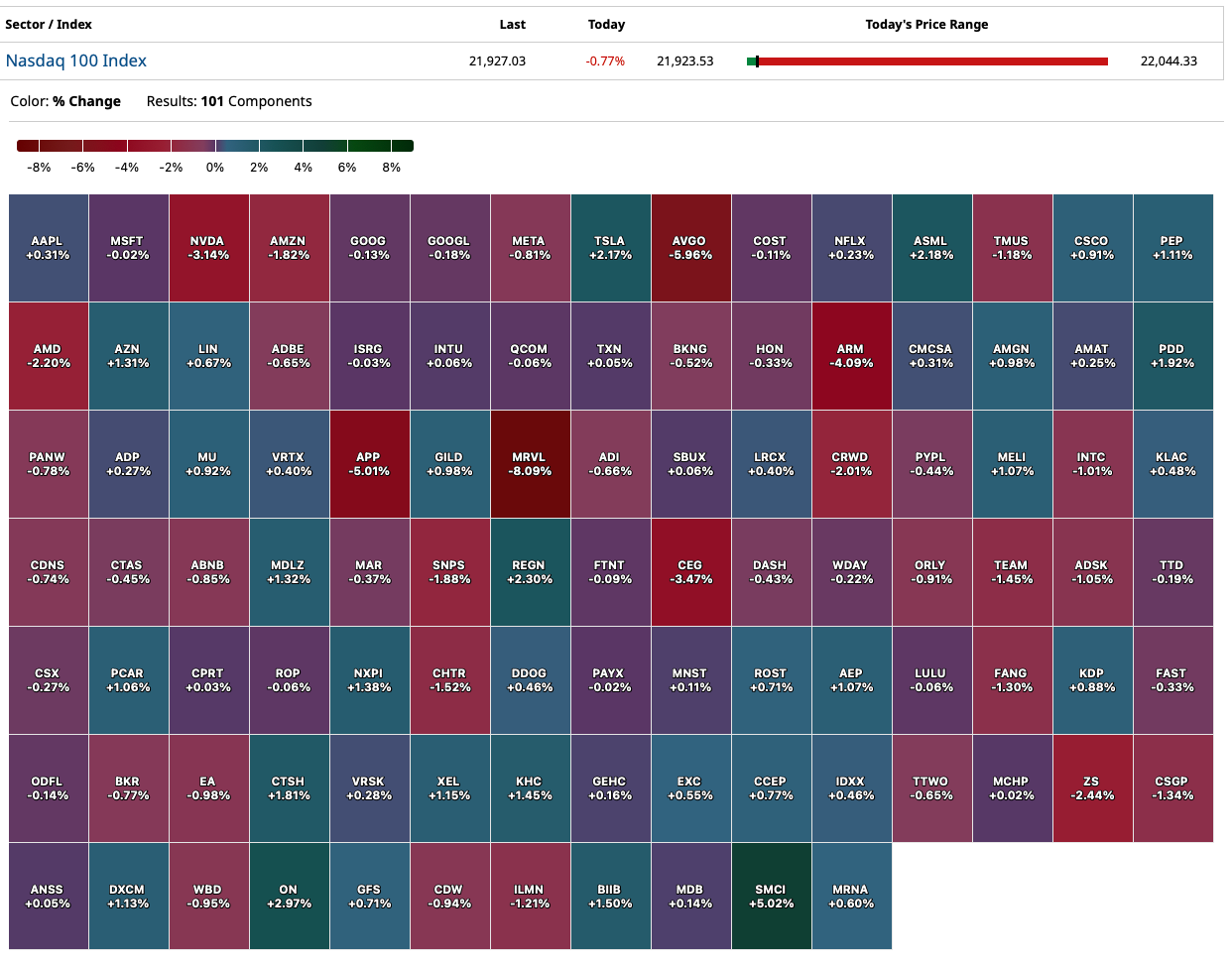

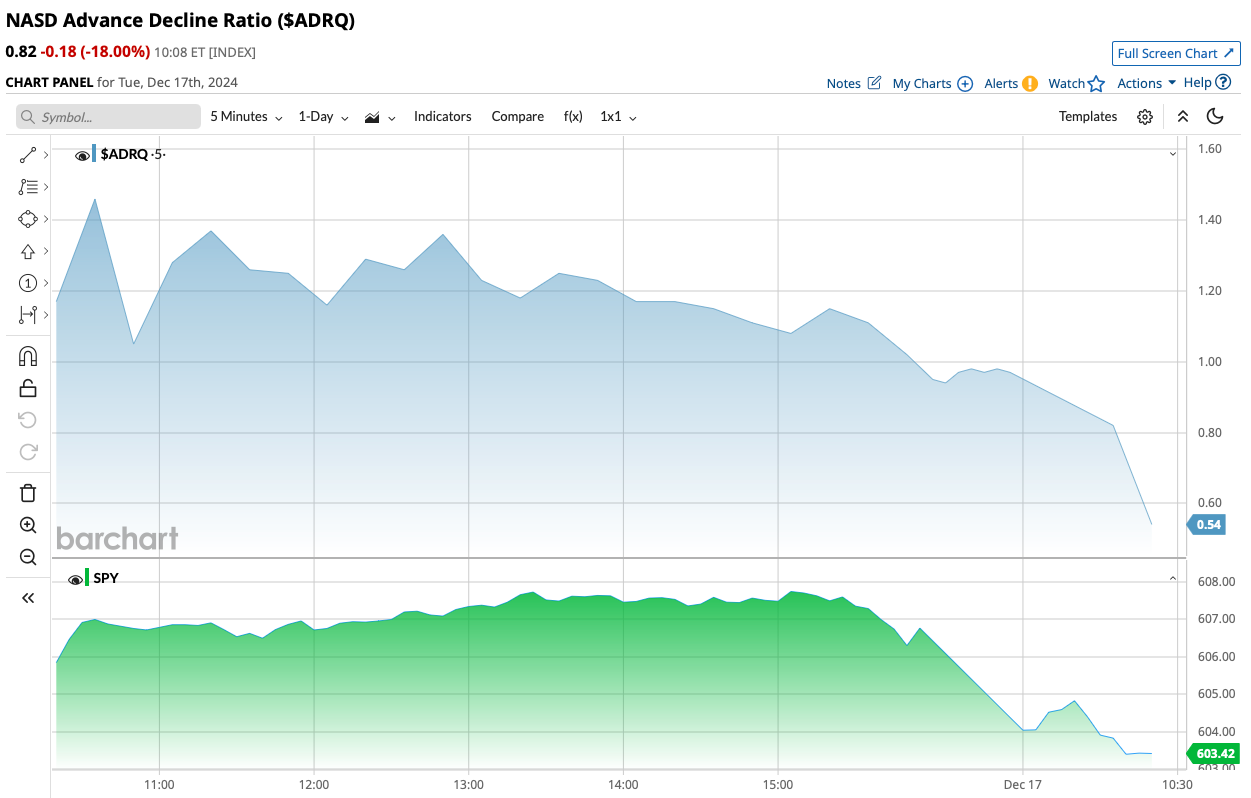

As I have been observing for the last week (or more), market breadth is stinking up the joint — with 3-1 losers on the NYSE and 2-1 decliners on the Nasdaq:

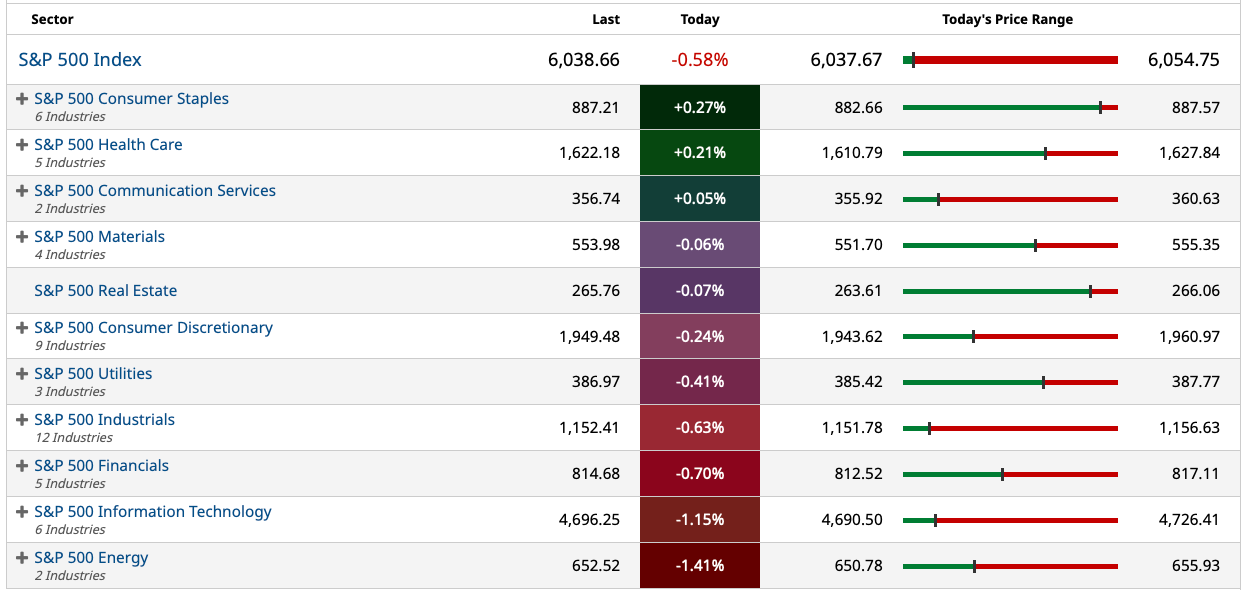

RSP (equal weighted S&P Index) dropped by -0.8% while the Russell wasn't crowing (IWM -1.16%).

VIX rose by +1.19 to 15.89.

Investors that appear in the business media are universally bullish.

Investors' cash positions are slimmer than at any point in years and the equity risk premium is paper thin.

There are few bears and no one I know that expects a serious market drawdown.

Nvidia NVDA, the former league leading hitter, is lower for the 7th or 8th day in a row and its chart looks worrisome (inverse head and shoulders?).

Financials, a favored "value proposition" appear to be rolling over.

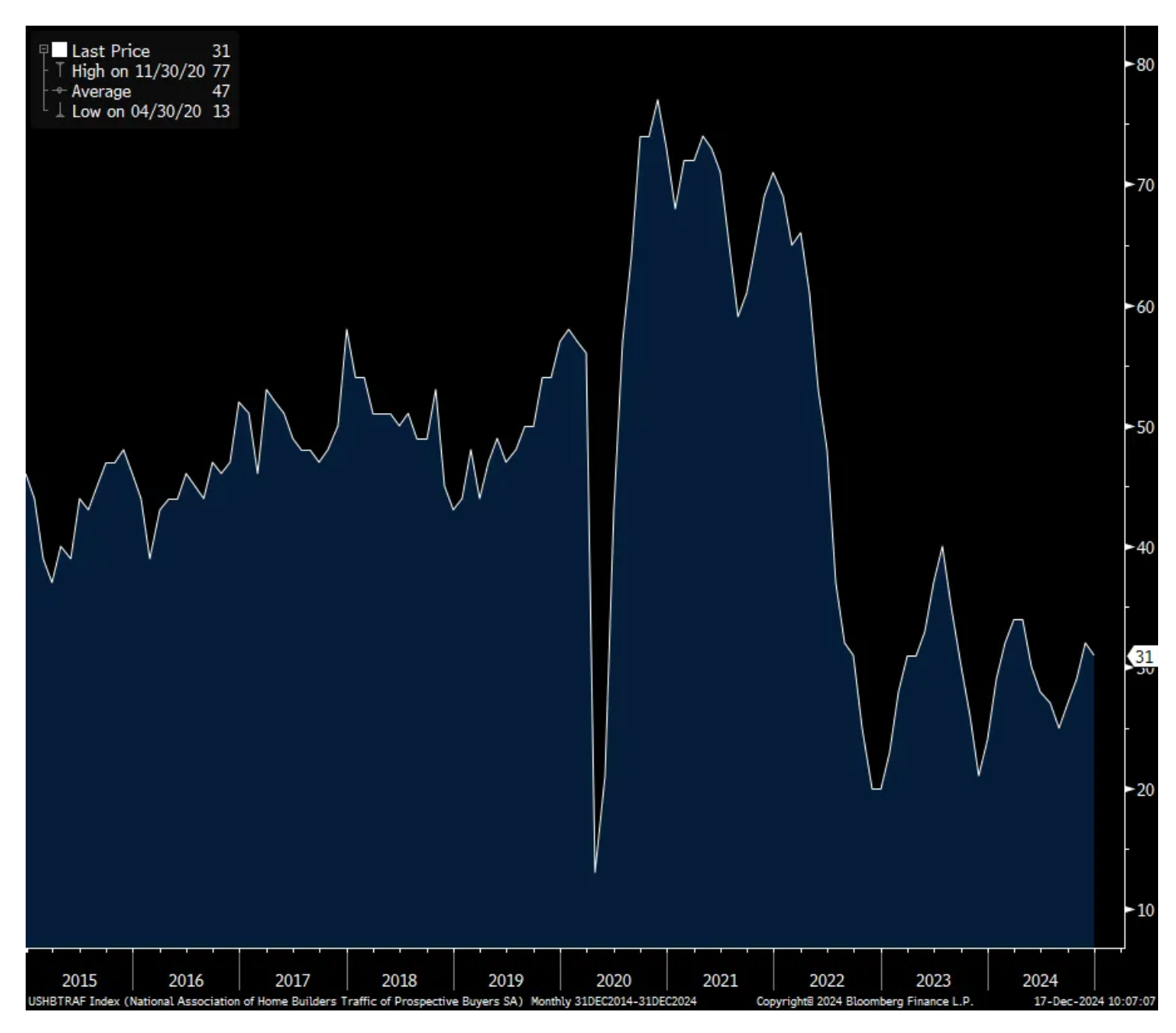

Homebuilders, which were also league leaders (and favored by the "talking heads" in the business media) are now down 25% from their highs.

There is plenty of speculation in certain quarters (including several of the annointed large-cap tech stocks) as well as, arguably, in a number of secondary and tertiary cryptocurrencies. Elon Musk's proximity to the President-elect is justifying a $600 billion + increase in Tesla's TSLA market cap).

Market structure, equity inflows and animal spirits have conspired to move the market robustly since the November election — but with it overall risks are raised.

Inflation remains sticky and the U.S. may not be an island of prosperity as the world's economies deteriorate .

"Slugflation" remains my baseline expectation.

A valuation reset and not an EPS reset has resulted in a forward P/E multiple of 22.6x, which, to many is now acceptable — even though most valuation metrics that have stood the test of time are in the 96%-tile.

A new investment paradigm is being heralded.

Excesses are never permanent and I remain cautious on the markets and of the view that risk dwarfs reward.

Riddle Me This, Batman: Bitcoin Up, MicroStrategy Down

* I don't buy what Michael Saylor is selling.

* As I have written, "bookmark this column."

Michael Saylor, Chairman of MicroStrategy MSTR, spent the last week all over business media — praising his own brilliance.

During the interviews, few commentators questioned his operating, financial and capital allocation strategy. Nor did they object to or comment on his creation of capital from the thin air within the context of his recent capital raises.

They didn't because they didn't spend the time analyzing it or they simply don't understand it.

But the markets seem to think differently (as I do)...

I Continue to Call B.S. to MicroStrategy and Michael Saylor

* And to the uncritical questioning (and implicit support) from the business media who missed the FTX fraud when it was right in front of their eyes.

* As MicroStrategy's shares fall, the company continues to sell $1 bills for $3.

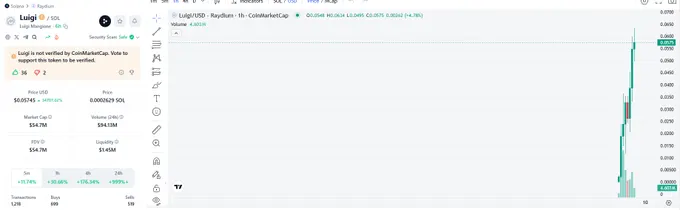

* Meanwhile, a cryptocurrency named Luigi (after UnitedHealthcare CEO murder suspect Luigi Mangione) has risen by 8,500% in the last 24 hours.

* Bookmark this column/analysis!

Coincident with a recent $2 billion equity offering, MicroStrategy's (MSTR) Michael Saylor recently went on the (predictable) business media tour.

Saylor was interviewed by commentators who (unfortunately and) consistently threw him softballs — reminiscent of when Sam "SBF" Bankman Fried (formerly known as "The White Knight of Crypto") was interviewed by Kate Rooney on CNBC only one month before he was indicted.

Here are two good example of Saylor's questionable investing logic and capital market jibberish which is at the core of MicroStrategy's financing (and very existence) — with little or no pushback from the interviewers:

Of course the difference between MicroStrategy and FTX is that MSTR is not a fraud — it is simply an Enron-like math scheme that will likely eventually eviscerate much of the money invested in the company (imho).

I remain short MicroStrategy.

In late November I shorted MSTR at $533.87. The shares closed yesterday at $365.

My MSTR Cost Basis Comment

My (MSTR) short basis is $533.87 - keeping it very small.

And, as I have written, MicroStrategy (with its "math" in expressing the case of buying $1 bills for $3 and MSTR's multiple derivative plays), is the standard bearer of the digital speculation today:

MicroStrategy Is Selling $1 Bills for $3

* To you!

* By issuing equity at a 300% premium to bitcoin.

* It is complicated, but delta trading provides random returns, though gamma trading provides steady returns.

MicroStrategy's (MSTR) Mike Saylor is sprouting a heavy dose of misinformation and Enron-style math in expressing the reason to own shares of MicroStrategy.

What Saylor is selling is volatility —with an operational asset (the MicroStrategy investor).

To summarize, when volatility is trending lower, problems arise. Moreover, the company prints shares for itself (share-based compensation) — another dilutive element to the MicroStrategy story.

Without getting too complicated, there is a useful life (and a depreciated asset associate with that) to produce a salvage value. (Maybe you should listen to the discussion.)

So, if you want to understand why I write this, listen to the complicated explanation:

* An extremely leveraged cryptocurrency market represents potential systemic risks. It is my view that cryptocurrency is "the mother of all bubbles" perpetuated by a number of factors (including the rejection of fiat money) and developing digital narratives — many of which have a weak foundation of logic. The absurd notion that the limiting of supply of bitcoin is as stupid as it is damning — as there is no limit to the supply of other cryptocurrencies. To this observer, the sheet market size of bitcoin and other cryptocurrencies is a manifestation of the risks.

Finally, the cryptocurrency craziness continues daily — with Luigi Coin, a meme cryptocurrency named after United Healthcare CEO murder suspect Luigi Magione, surging by over 8,500% in the last few hours, reaching a market capitalization in excess of $25 million:

JPMorgan Chase JPM, a short, is leading the rollover in financials.

That sector decline is now expanding with Goldman Sachs GS, Schwab SCHW, American Express AXP, private equity, money center banks (C, WFC and BAC), etc. joining the southerly move.

The financials remind me of homebuilders a month or two ago (they have subsequently fallen hard). Banks and selected financials are still near 52-week highs and loved by "value players."

US IP soft/Builder sentiment mixed and lacking traffic

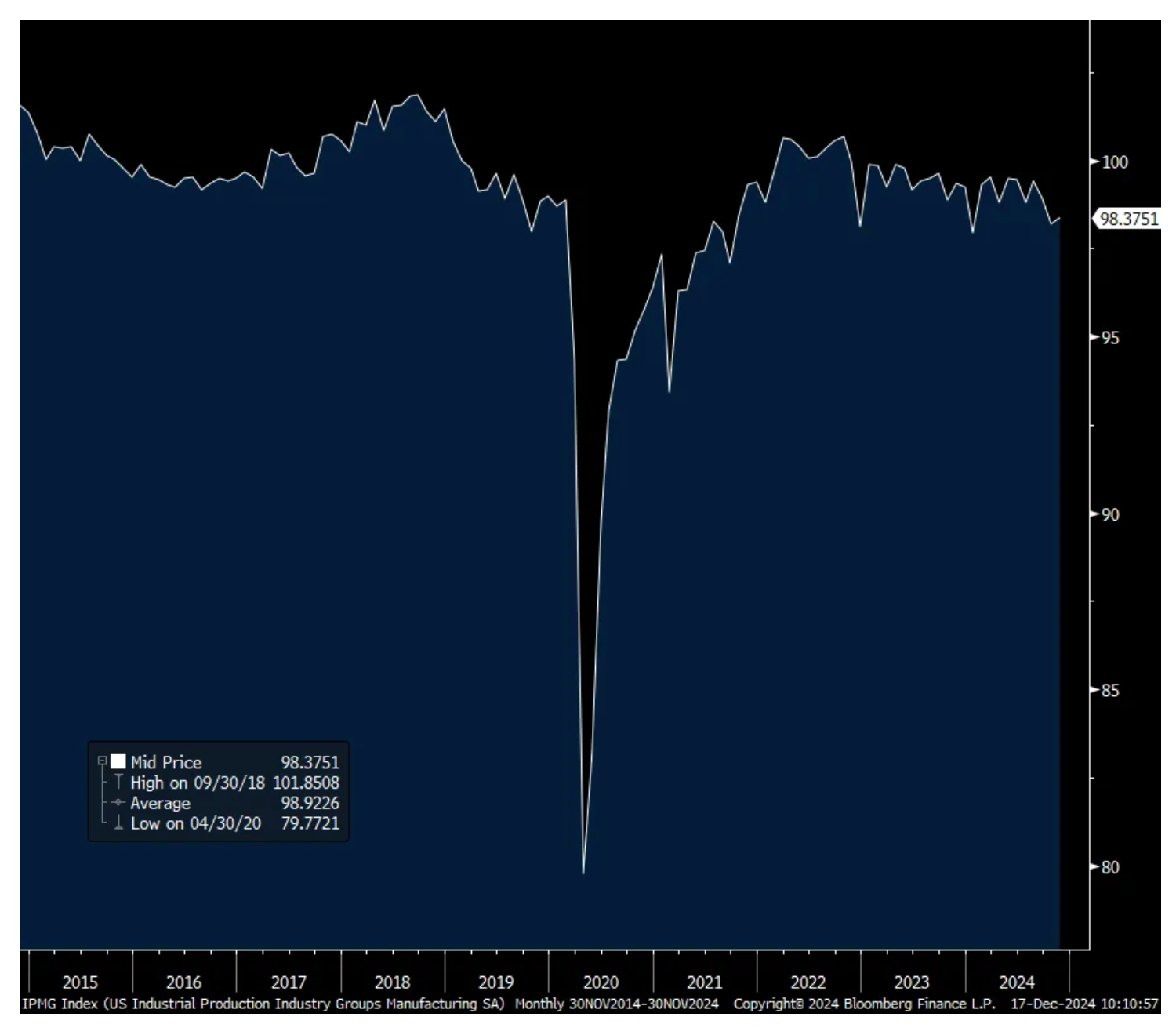

The 10 yr yield fell a touch back below 4.40% after the weak November industrial production figure, particularly in the manufacturing component. Manufacturing production rose .2% m/o/m vs the estimate of up .5% and October was revised down by 2 tenths to a drop of .7%. Auto production rebounded by 3.5% after a 5.4% drop in October but manufacturing production ex autos fell for a 3rd straight month and is down .7% y/o/y. Mining and utility output both fell.

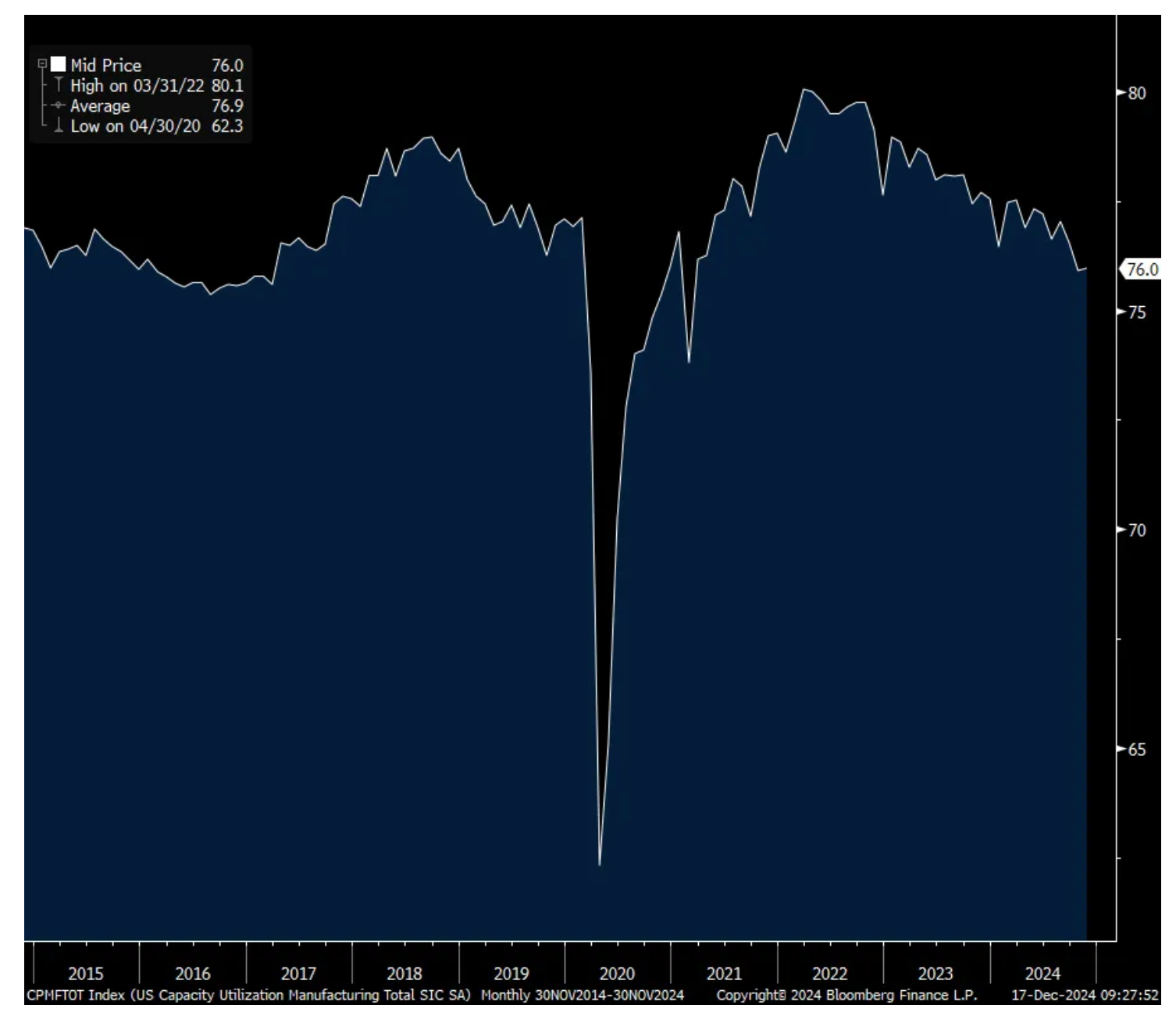

Capacity utilization for manufacturing stands at just 76% which is below the 10 yr average of 77% and is just off the lowest level since March 2017 ex Covid. Notice in the chart below that it peaked pre Covid just as the tariff battle was at its peak. Manufacturing production also peaked then and something no one seems to be talking about when debating the use of tariffs.

Mfr’g Component of US Industrial Production, still below the 2018 high

Mfr’g Capacity Utilization

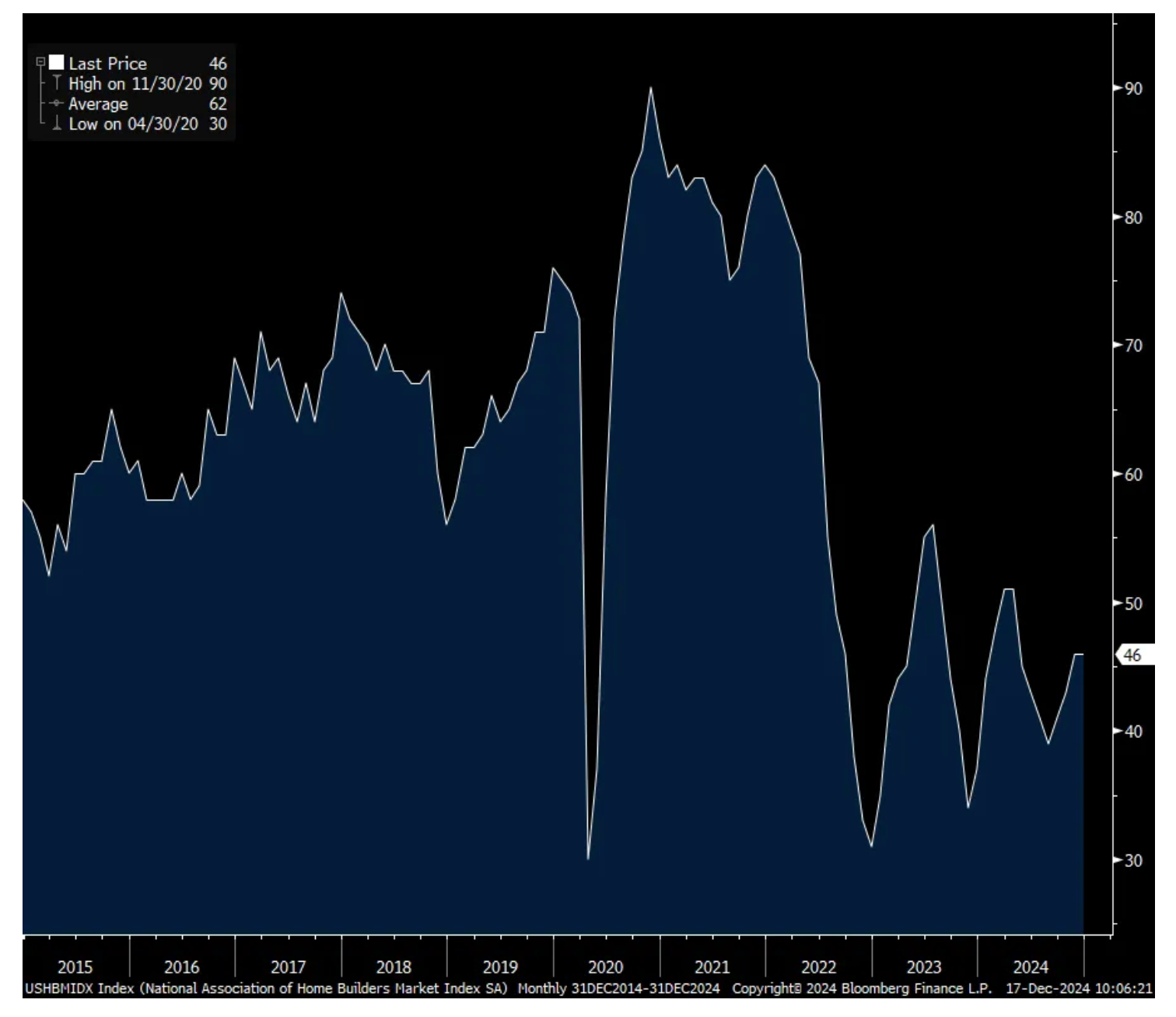

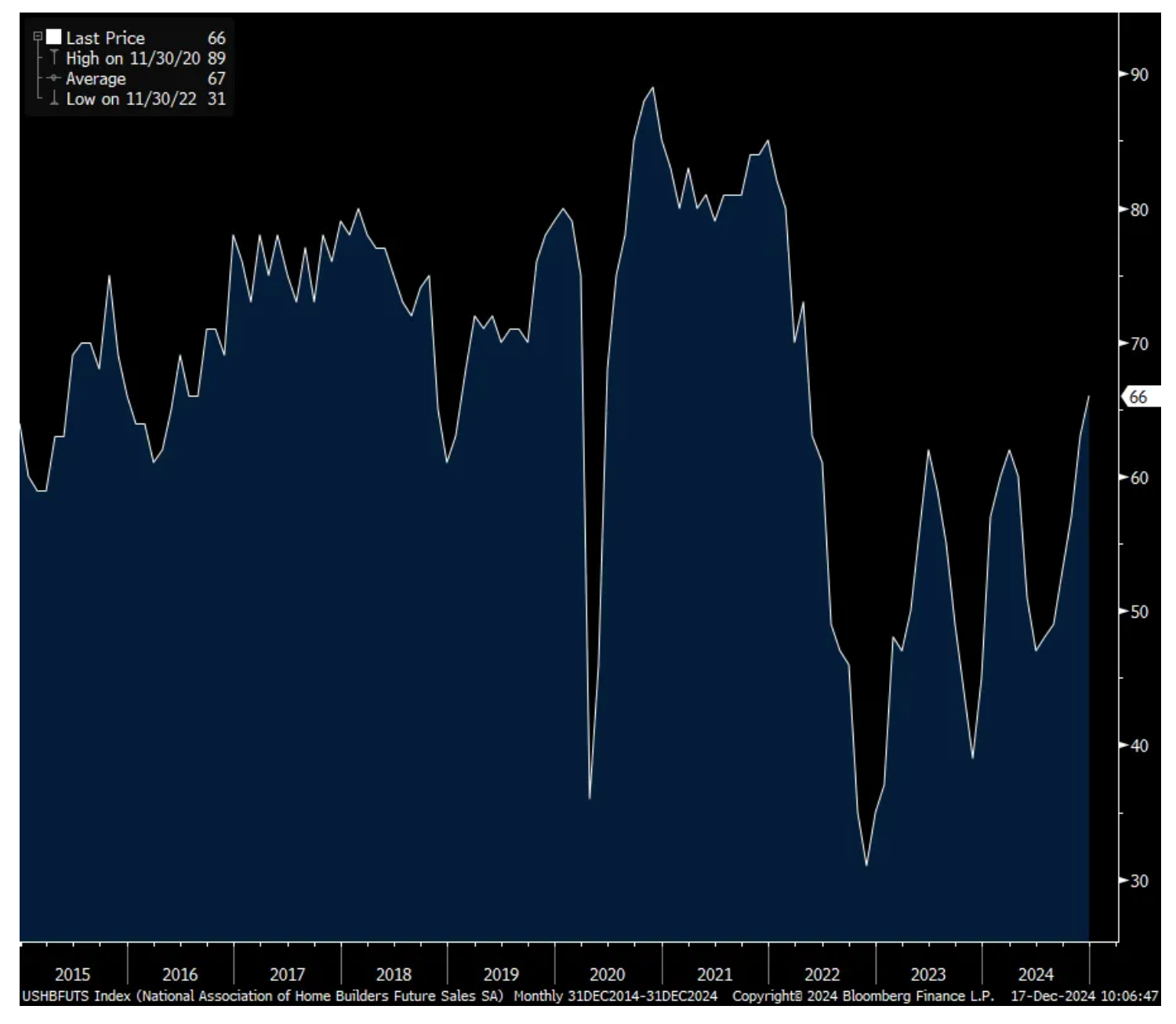

The December NAHB home builder sentiment index was unchanged m/o/m at 46. The estimate was 47 and thus also remaining below 50. Expectations though are for a notable improvement as this component rose again to 66 from 63 and vs 57 in October pre-election. The Present Situation held at 48. The drag remains really in the Prospective Buyers Traffic component which was 31 vs 32 in November and 19 pts below the breakeven.

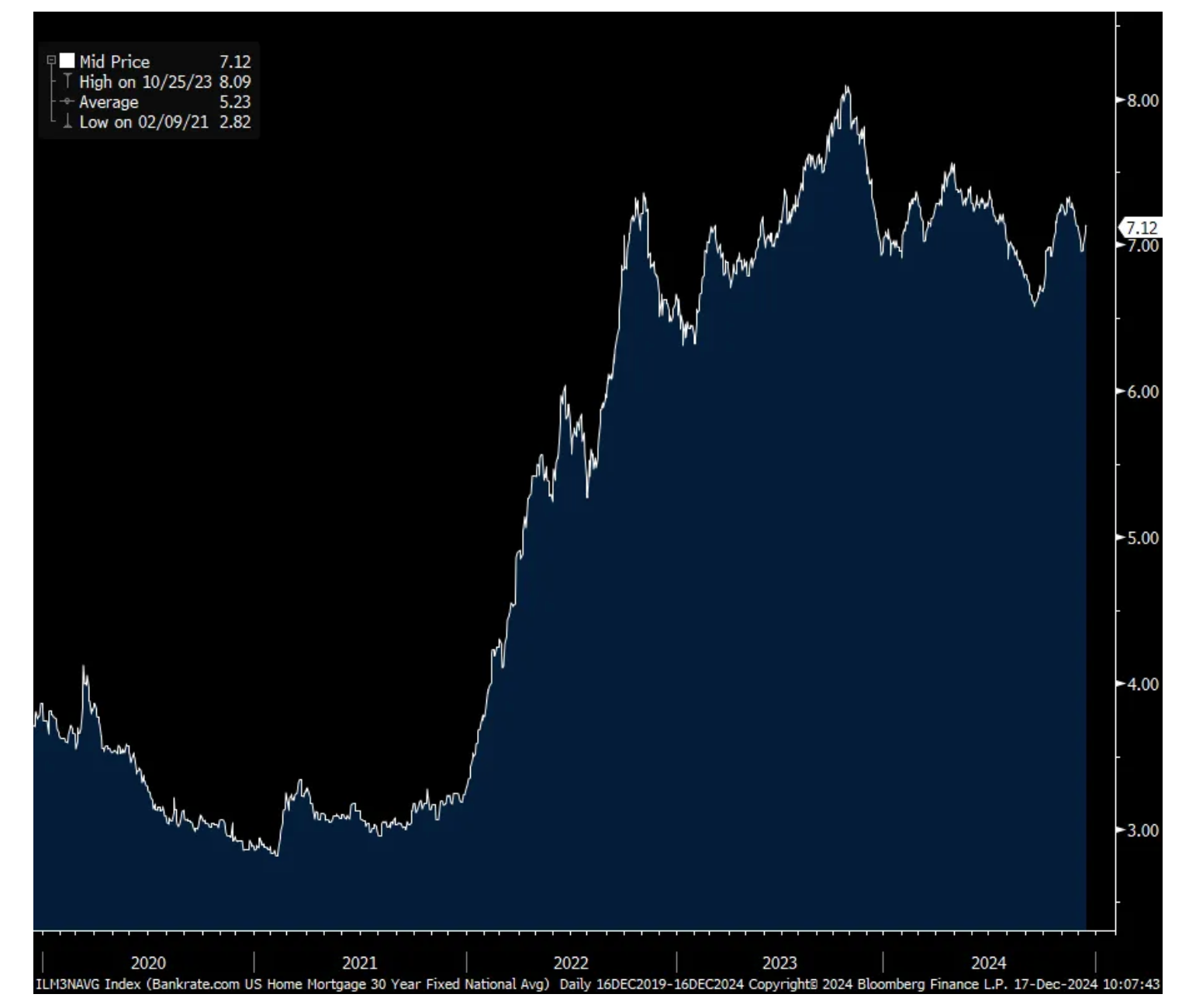

Before the September Fed rate cut, there was optimism everywhere that rates would fall across the yield curve, particularly from the housing industry but unfortunately long rates have stayed high and mortgage rates of course have inflected back up. Builders now acknowledge this reality but hope that an easing regulatory burden will help them with a new incoming administration. However, zoning and permitting for residential real estate is mostly conducted at the state and local level.

The NAHB said, “While builders are expressing concerns that high interest rates, elevated construction costs and a lack of buildable lots continue to act as headwinds, they are also anticipating future regulatory relief in the aftermath of the election,” said NAHB Chairman Carl Harris, a custom home builder from Wichita, Kan. “This is reflected in the fact that future sales expectations have increased to a nearly three-year high.”

I’ll add and to state the obvious, the main challenge for the housing market remains affordability for the first time buyer both from a home price perspective and this level of mortgage rates.

* But, as Bob Farrell reminds us, excesses are never permanent.

A market driven by momentum, the velocity of which is in part a product of concentration, invites a "tunnel vision," which ignores valuation and interest rates.

But, this condition never goes on forever, it just looks that way.

This time, a market structure, which invites greater levels of passive investment, has lengthened the cycle.

But it is my strong view that the inevitable unwinding of excess is also likely to be greater in either or both time, duration and magnitude.

From yesterday:

DEC 16, 2024 4:00 PM EST

Bob Farrell's Rule #3

* "There are no new eras; excess moves are never permanent"

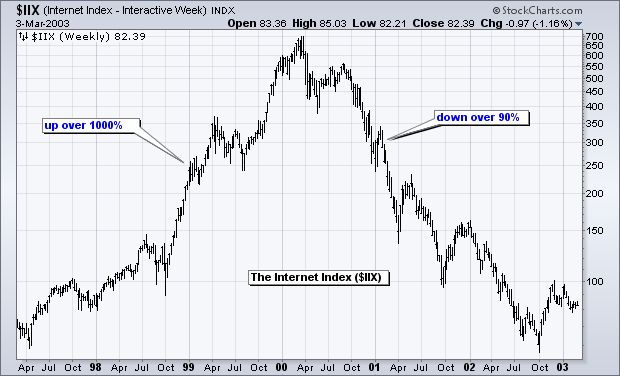

* I am starting to get a Wired Magazine feeling (circa late 1990s)....

"We're Facing 25 Years of Prosperity, Freedom and a Better Environment for the Whole World. You Got a Problem With That?"Unfortunately, during the next 25 years, we faced not only an 80% drawdown starting in 2000 (as the dot-com boom fizzled) but also "The Great Decession" of 2007-09 (in which the S&P Index fell to 666).

Which brings us to an interview with Merrill Lynch's Hyzy on CNBC (with Judge Wapner), in which Hyzy says he sees "a powerful new bull market and new paradigm lies ahead in 2025... as an asset light tech sector leads stocks higher."

I raise Merrill Lynch alum Hyzy one Bob Farrell (who also cut his teeth at Merrill Lynch): Farrell's Lesson #3. There are no new eras—excesses are never permanent

Translation: There will be a hot group of stocks every few years, but speculation fads do not last forever. In fact, over the last 100 years, we have seen speculative bubbles involving various stock groups. Autos, radio and electricity powered the roaring '20s. The nifty-fifty powered the bull market in the early 70s.

Biotechs bubble up every 10 years or so and there was the dot-com bubble in the late '90s.

“This time it is different” is perhaps the most dangerous phrase in investing. As Jesse Livermore puts it:A lesson I learned early is that there is nothing new in Wall Street. There can't be because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again.

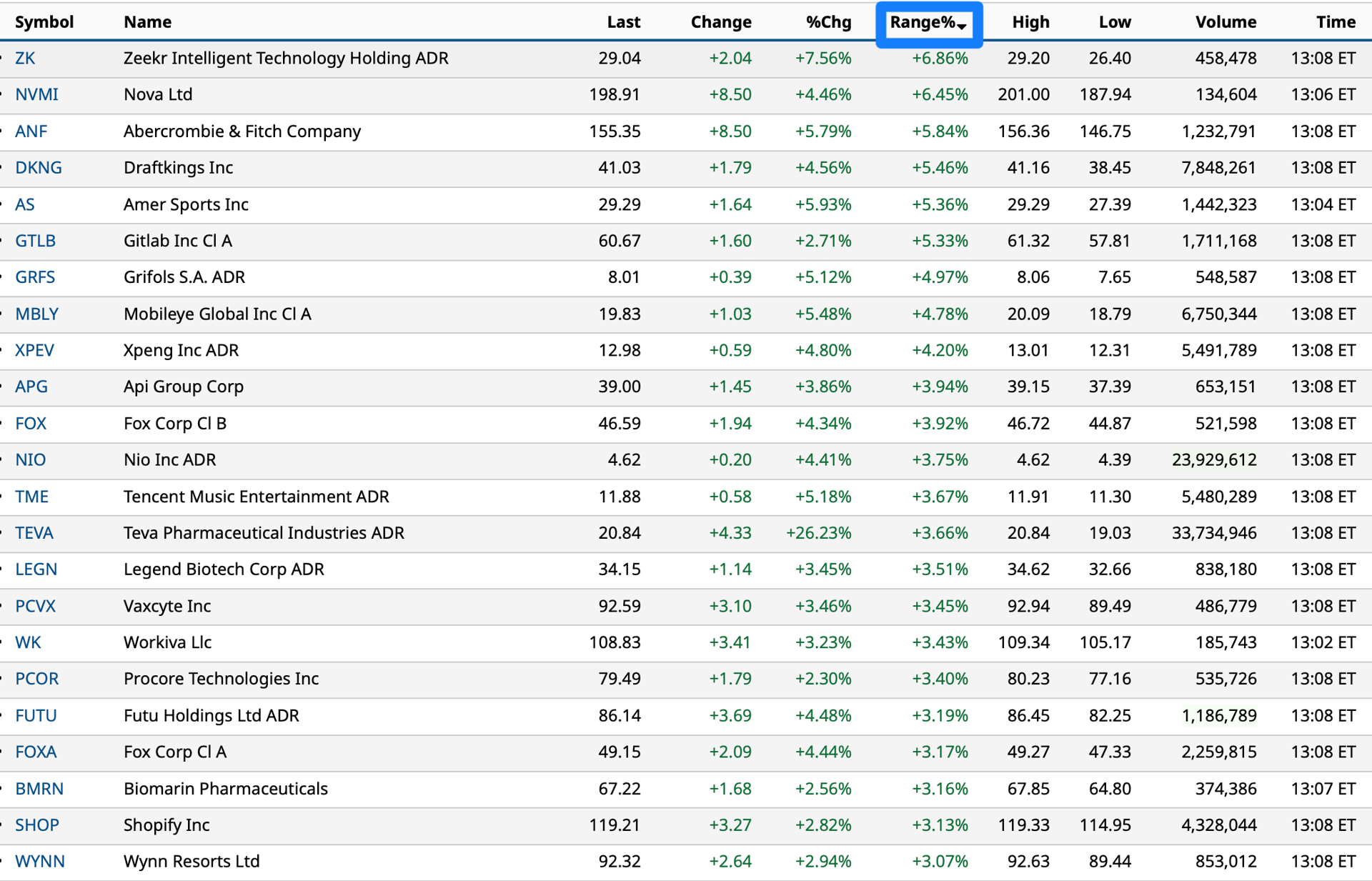

The following is premarket data that came in later than usual:

Upside:

-PRTG +183% (announces Letter of Intent with Immunova for an Option to Acquire iOx Therapeutics, Ltd.)

-EHTH +29% (raises guidance)

-KOS +21% (Tullow Oil plc confirms termination of preliminary discussions with Kosmos Energy Ltd)

-TEVA +18% (Teva and Sanofi Announce Duvakitug (Anti-TL1A) Positive Phase2b Results Demonstrating Best-in-Class Potential in Ulcerative Colitis and Crohn’s Disease; receives US FDA ANDA tentative approval for Binimetinib)

-MITK +17% (earnings, guidance)

-SEDG +15% (Goldman Sachs Raised SEDG to Buy from Sell, price target: $19)

-LAES +14% (partnering with Hedera in the Next Generation of Post-Quantum Semiconductors)

-RMNI +13% (Appeals Court vacates District Court's prior opinion which had largely ruled in favor of ORCL regarding infringing derivative works)

-QUBT +12% (awarded contract by NASA to support phase unwrapping using Dirac-3 photonic optimization solver)

-RMTI +10% (enters multi-year product purchase agreement with leading provider of dialysis products and services)

-STRM +9.1% (earnings)

-SHLS +9.0% (Morgan Stanley Raised SHLS to Overweight from Equal Weight, price target: $7)

-PLCE +7.7% (reports 6-week sales data)

-RICK +6.9% (earnings)

-KVYO +5.5% (momentum)

-USAU +5.3% (earnings)

-EUDA +4.9% (enters into preliminary discussions with Guangdong Cell Biotech regarding potential JV)

-TDW +3.7% (CEO Kneen sold 42K shares at $48.06/shr on 12/13)

-LPTH +3.2% (issues Shareholder Letter and Provides Corporate Update)

-LOVE +3.0% (guidance ahead of Investor Day)

-NET +2.4% (Stifel Nicolaus Raised NET to Buy from Hold, price target: $136)

-BYRN +2.3% (increases Launcher Production by 33% to 24K units/mo)

-PFE +2.3% (initial 2025 guidance, affirms FY24; receives US FDA NDA Supplemental 25 approval for Aromasin (Exemestane))

-HIMS +2.1% (Morgan Stanley Initiates HIMS with Overweight, price target: $42)

-TSLA +2.0% (Mizuho Securities Raised TSLA to Outperform from Neutral, price target: $515)

-ZBH +2.0% (JPMorgan Chase and Co Raised ZBH to Overweight from Neutral, price target: $128)

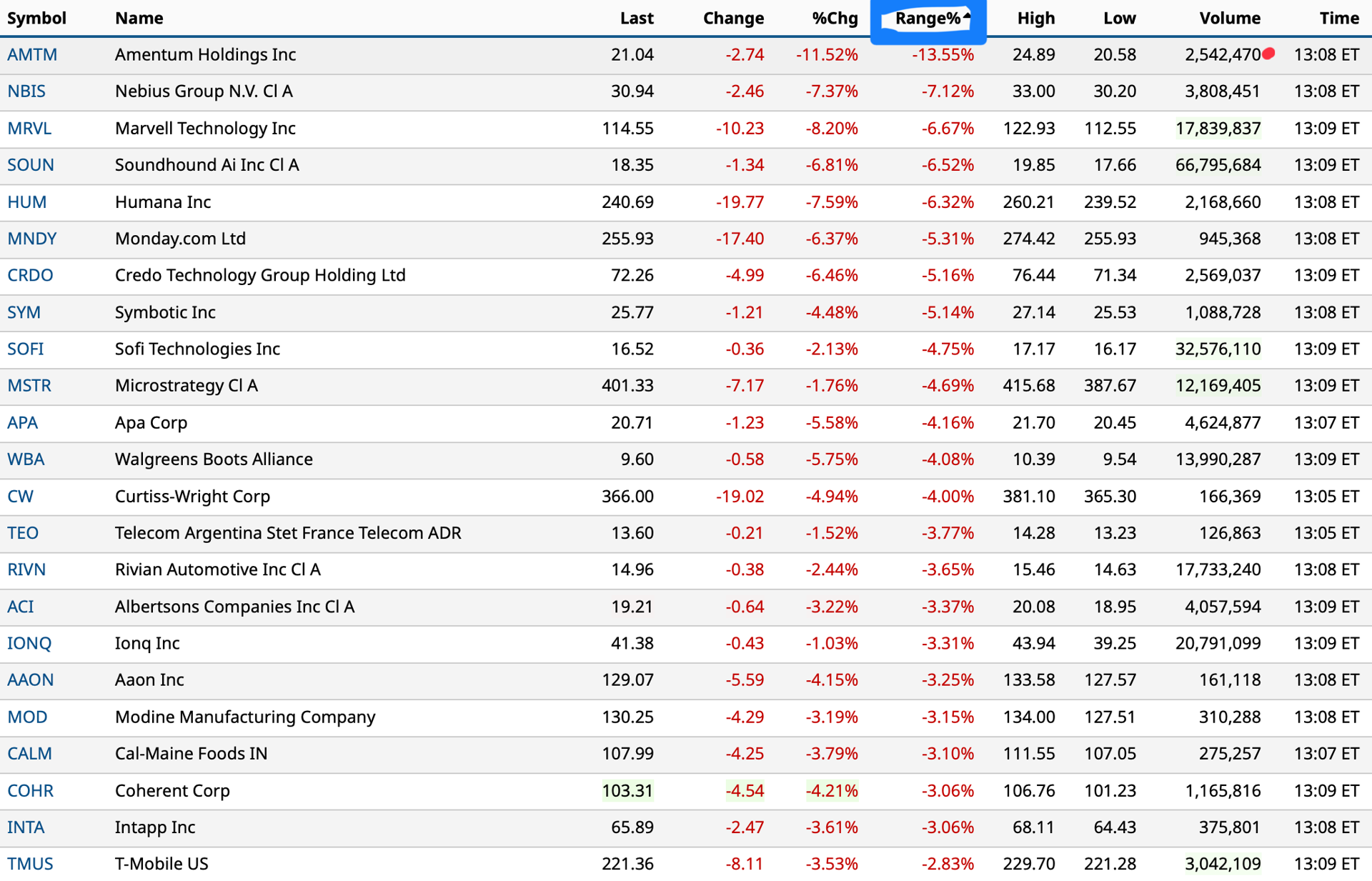

Downside:

-RVPH -40% (prices $18.0M equity offering at $1.50/sh)

-TNYA -26% (reports promising early data from MyPEAK-1 Phase 1b/2 Clinical Trial of TN-201 for Treatment of MYBPC3-Associated Hypertrophic Cardiomyopathy)

-EVGO -23% (prices 23M share secondary offering by holder at $5.00/shr)

-AFMD -22% (reports Positive Clinical Update on AFM24/Atezolizumab Combination Therapy in Non-Small Cell Lung Cancer (NSCLC))

-MAMA -16% (ROTH MKM Reiterates MAMA with Buy, price target: $11 from $10)

-RCAT -14% (earnings)

-BMEA -11% (announces positive topline results from ongoing Phase II COVALENT-111 Study in Patients with Type 2 Diabetes)

-COMM -5.9% (Morgan Stanley Cuts COMM to Underweight from Equal Weight, price target: $5)

-VIAV -5.8% (Morgan Stanley Cuts VIAV to Underweight from Equal Weight, price target: $9.50 from $8)

-UNCY -4.3% (announces publication of Oxylanthanum Carbonate (OLC) positive bioequivalence data in clinical therapeutics)

-MLCO -3.7% (Morgan Stanley Cuts MLCO to Equal Weight from Overweight, price target: $7.50)

-AFRM -3.1% (announces Proposed Private Offering of $750M of Convertible Senior Notes)

-TMDX -2.2% (JPMorgan Chase and Co Cuts TMDX to Neutral from Overweight, price target: $75 from $116)

-MQ -2.0% (Barclays Cuts MQ to Equal Weight from Overweight, price target: $4)

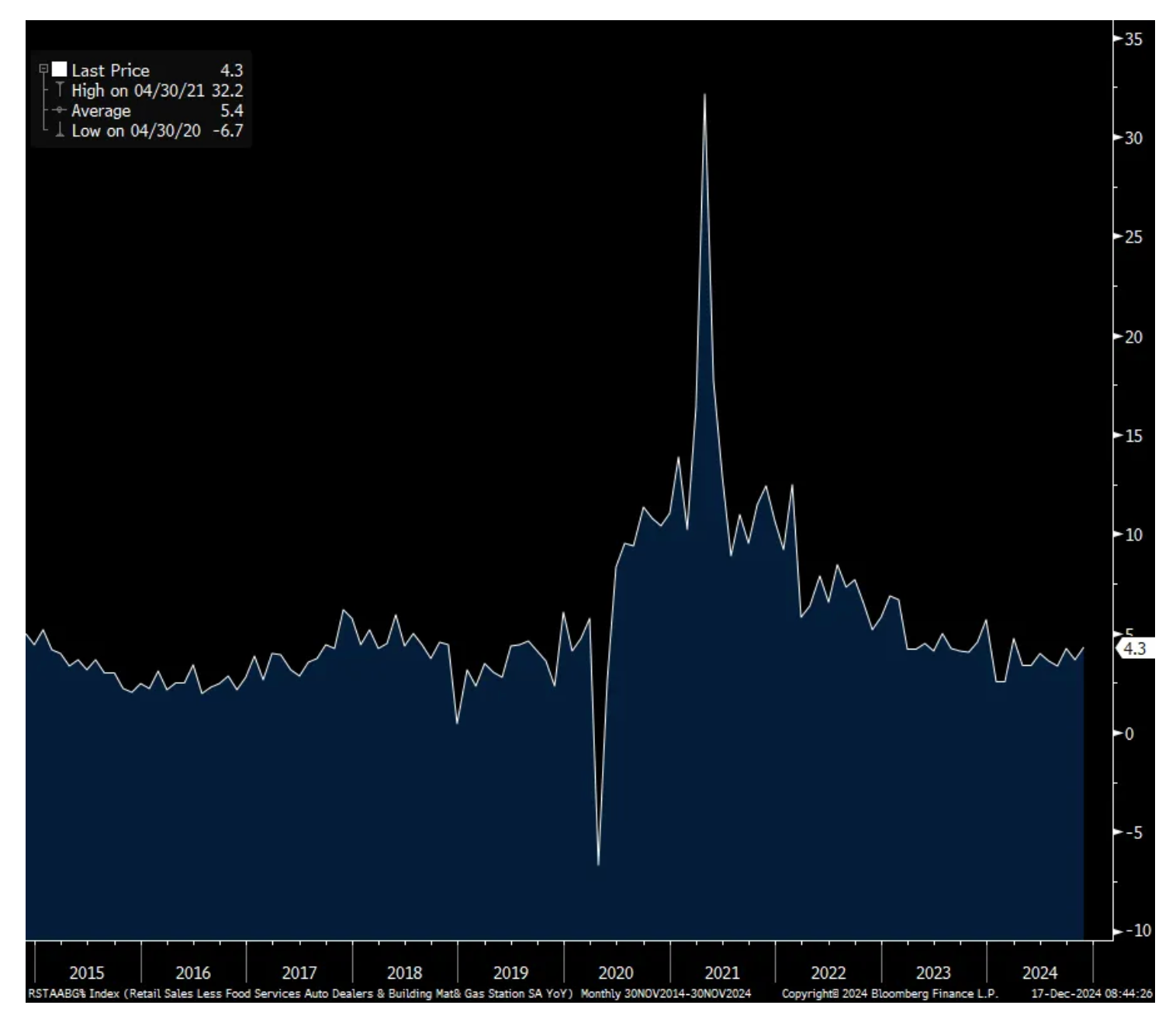

Core retail sales in November rose .4% m/o/m as expected after a one tenth decline in October. Not included in the core print was the 2.6% m/o/m jump in auto sales/parts after a 1.8% rise in October. Building materials, also outside the core read, was up .4% m/o/m and 2.5% y/o/y.

Elsewhere the spending was more mixed. They rose for furniture, electronics, sporting goods and for e-commerce but fell at restaurants/bars, department stores, apparel, food/beverage and miscellaneous for a 2nd month. Miscellaneous can include dollar stores, convenience stores, pet, flower, etc…

For perspective, over the past 10 years the y/o/y core retail sales growth was 5.4% and was 4.3% in November. Also for context, the top 20% income decile accounts for about 40% of all consumer spending and highlights the bifurcated consumer where we know the lower to middle income consumer has been much more circumspect with how they spend because of less savings while the upper end consumer is helping to support economic growth with a boost too from the wealth angle of higher stocks and home prices.

Treasury yields are about where they were right before the number release on the in-line data but staying at the highs of the morning. Also to keep in mind, with the later Thanksgiving compared to last year, holiday spending likely started much closer to November month end and thus making the December stats to be seen more relevant when compared to last year.

Boockvar on Those Pesky Shipping Costs, Bond Bear Market

From Peter Boockvar:

More on that line about 'shipping costs'/Other stuff, including the bond bear market that continues on

A line from yesterday's US PMI from S&P Global stood out and was this, "December saw raw material prices spike sharply higher amid supplier led price rises and higher shipping costs." On the latter, let's go through that. We've seen the lift in container shipping costs this year from where they started 2024. The Drewry World Container Index last week was at $3,529 per 40 ft container, up from about $1,700 at the beginning of the year. With air cargo, World ACD said on Friday that "Global air cargo average spot rates rose by a further 4% in the first full week of December to a 2024 high of US$3.30 per kilo, driven by a +8% surge from Asia Pacific origins, as the sector's strong but relatively stable fourth quarter peak season approaches its zenith." And, "Compared with last year, average worldwide spot rates in week 49 were up 21% y/o/y, led by a 62% increase from Middle East & South Asia (MESA) origins, and 19% y/o/y increases from Asia Pacific and Europe."

With respect to trucking rates, they continue higher too with the Dry Van per mile rate in the US (from Truckstop.com) rising to the highest level since February at $1.72, which is up 6.8% y/o/y.

So, while core goods prices have of course deflated this year, the cost of moving them around are up sharply this year and the catalyst for that PMI quote. Now this recent move up could very well be the pull forward of ordering ahead of likely tariffs but something we'll be watching closely of course.

Dry Van Per Mile price

Maybe another sign of pull forward but not necessarily to the US, Singapore said its November non-oil exports jumped by 14.7% m/o/m, well above the estimate of up 9.2% and was up 3.4% y/o/y vs the forecast of down 1%. The rise was led by a 23.2% y/o/y jump in electronics exports. The export strength was to India, Hong Kong, Taiwan, Korea and Malaysia. Exports to the US fell by 19% and to the EU by 1.2%. The Singapore Straits index fell by .6% with most of Asian markets red overnight but it is still up 17% ytd.

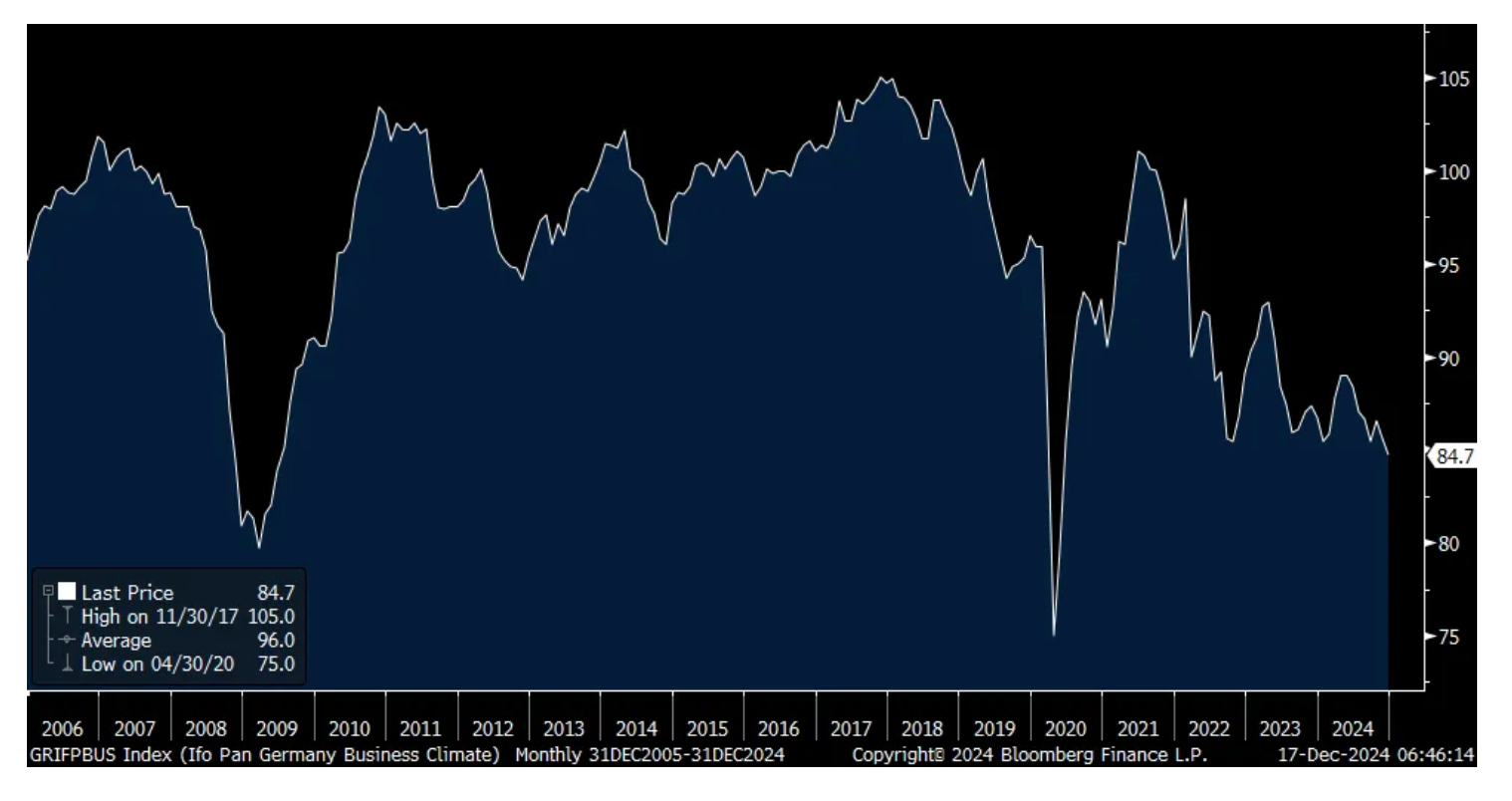

Of note in Europe was the German December IFO business confidence index which fell to 84.7 from 85.6. That is below the expectation of 85.5 and the weakest level since June 2009 not including Covid though the components were mixed. The Current Assessment ticked up to 85.1 from 84.3 but Expectations fell to just 84.4 from 87. The bottom line from IFO, "The weakness of the German economy has become chronic."

Within the report, manufacturing softened further. "The order situation deteriorated again. Production cutbacks have been announced." I'll add that one thing that doesn't get enough attention is that Germany went hard down the renewable, solar/wind road and rid themselves of nuclear. They now have some of the most expensive and least efficient energy costs in Europe as a result. Services and trade also weakened while construction was a bit less negative.

The euro is a touch lower in response, bund yields are little changed but the DAX is up slightly and higher by 21% ytd. That DAX performance is impressive relative to the underlying economic weakness but that is due in part to the weak euro and the multinational companies that make up the DAX.

German IFO

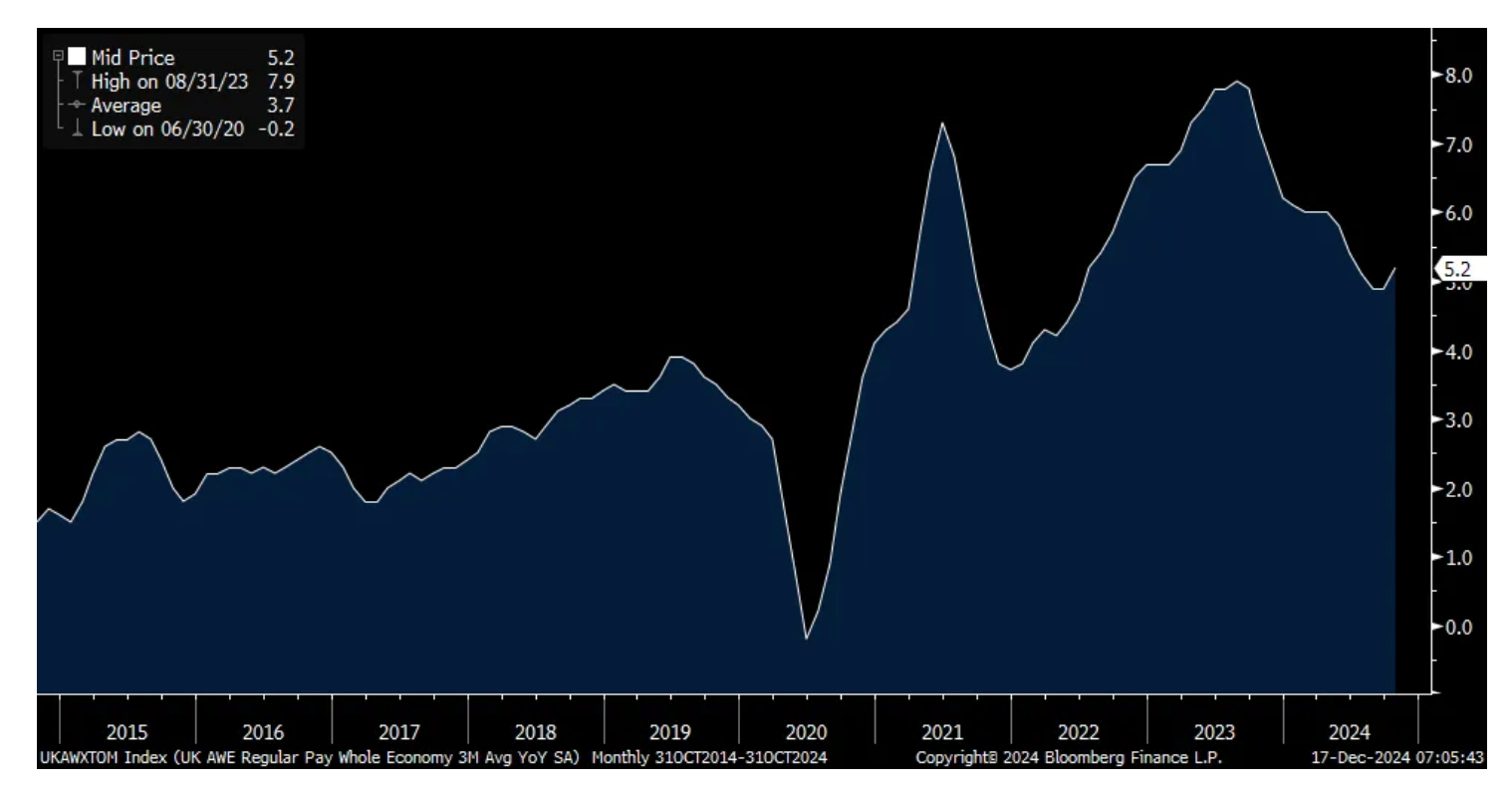

Gilt yields are jumping with the 2 yr and 10 yr yields up about 8 bps after stronger than expected wage growth was reported for the 3 months ended October. The pound is up too while the FTSE 100 is lower by .8%. Ex bonus, they rose by 5.2% y/o/y, above the estimate of 5% and a 4 month high. This was part of their full jobs report where 173k jobs were added vs the estimate of just 5k. Also, there was no change in November jobless claims.

By the way, at 4.52%, the 10 yr Gilt yield is just 4 bps from matching the highest level since October 2023. The global bond bear market is real.

* The 10-year Treasury note yield is approaching 4.5%.

* In the fullness of time, rising interest rates will adversely impact equities...

The rise in yields — domestically and "over there" — continues apace this morning:

* The yield on the 1-year Treasury bill is +3 basis points to 4.27%.

* The yield on the 10-year Treasury note is also +3 basis points to 4.43%.

* The yield on the 30-year Treasury bond is +2 basis points to 4.63%.

A subscriber in our Comments Section wrote that this is irrelevant to equities.

And, yes, thus far he is right.

"Thus far" being the operative words!

Remember, the risk-free rate of return is fundamental to the valuation of equities.

But, in the short term the market is a voting machine and in the long term it is a weighing machine.

It's just that, as, for now, we live in a world dominated by passive strategies and products who worship at the altar of price (and price momentum). Those strategies and products are materially influenced by the flow of funds and animal spirits.

This is, however, never a permanent condition — especially with valuations mostly in the 95%-tile (or higher).

The failure of Amendment 3 in Florida (which I feared and was the basis for my recent sales) means future state openings are unlikely.

I expect a rescheduling sometime in the second half of the year (which will help cash flows by eliminating unfair taxes).

Nonetheless, the industry is mostly comprised of companies that are debt laden (with large obligations of deferred taxes to the US government) with little hope of non adjusted cash flows to service that debt.

Many companies will go bankrupt - in fact most of them can not survive given those debt loads when combined with weak state sales (even in less mature states). Think Med Men, one of the better retail operations in California, which went bankrupt.

Most secondary and tertiary companies that are components of MSOS will go to zero, hurting the ETF.

Green Thumb will survive but even some of the largest cannabis companies will forced to do mergers of equals to eliminate redundant expenses.

Tax selling is likely hurting the stocks now, setting stage for a small bump into the New Year (but not, in my view, tradeable, except for the most facile).