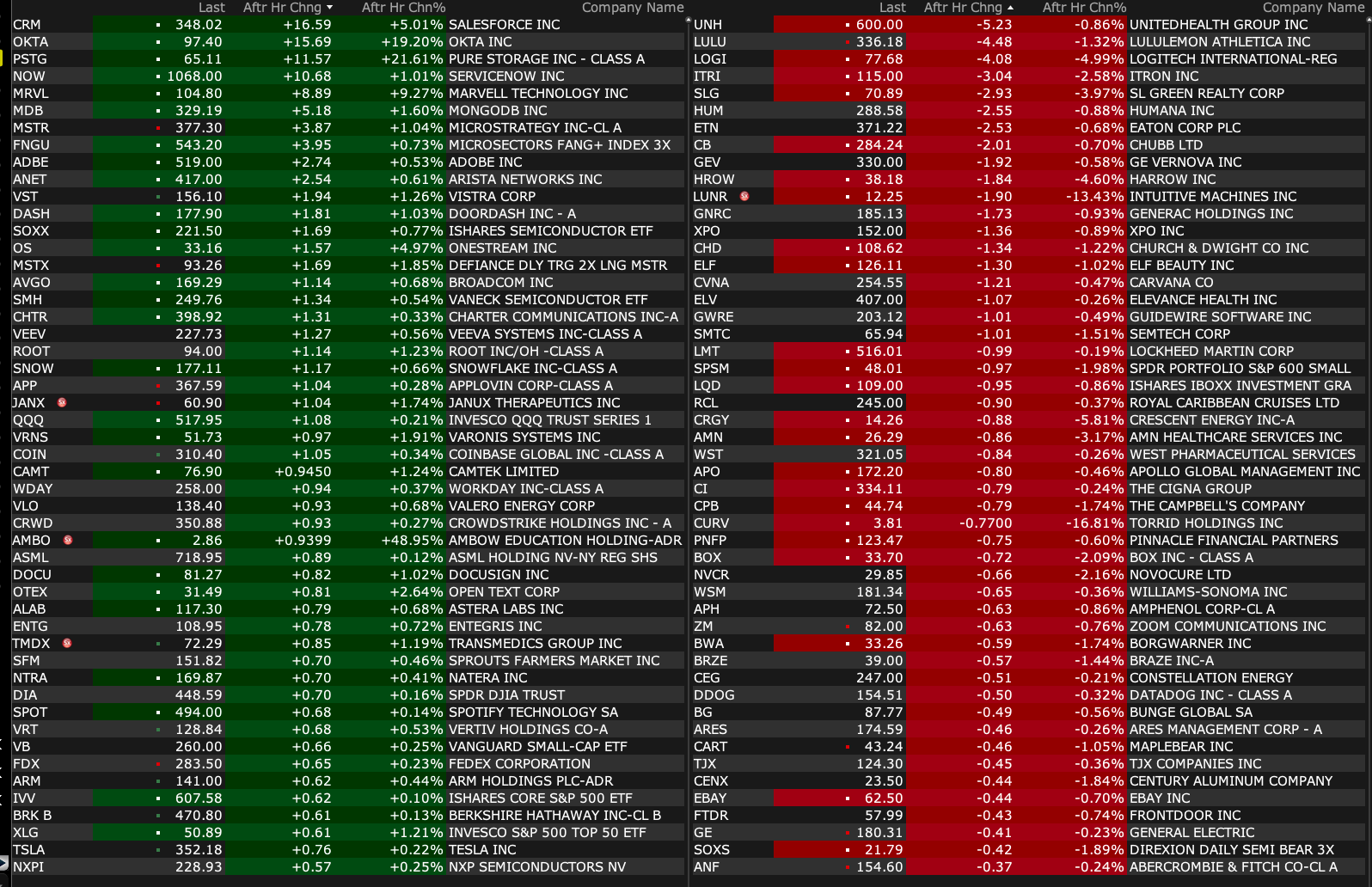

Tuesday's After-Hours Movers

As of 4:25 p.m.:

BY Doug Kass · Dec 3, 2024, 4:50 PM EST

As of 4:25 p.m.:

BY Doug Kass · Dec 3, 2024, 4:50 PM EST

BY Doug Kass · Dec 3, 2024, 4:36 PM EST

Regarding yesterday's Trade of the Week (shorting XLF).

I do think I am on to something here:

* JPMorgan JPM gapped several dollars higher in the early going and is now -$1.

* Same for Berkshire Hathaway BRK.A BRK.B, which is -$6.50 after being higher after the opening.

* Morgan Stanley MS is -$3/share from high this AM.

* Private equity stocks are clearly rolling over after a stupendous run.

* XLF is at the day's low.

BY Doug Kass · Dec 3, 2024, 3:57 PM EST

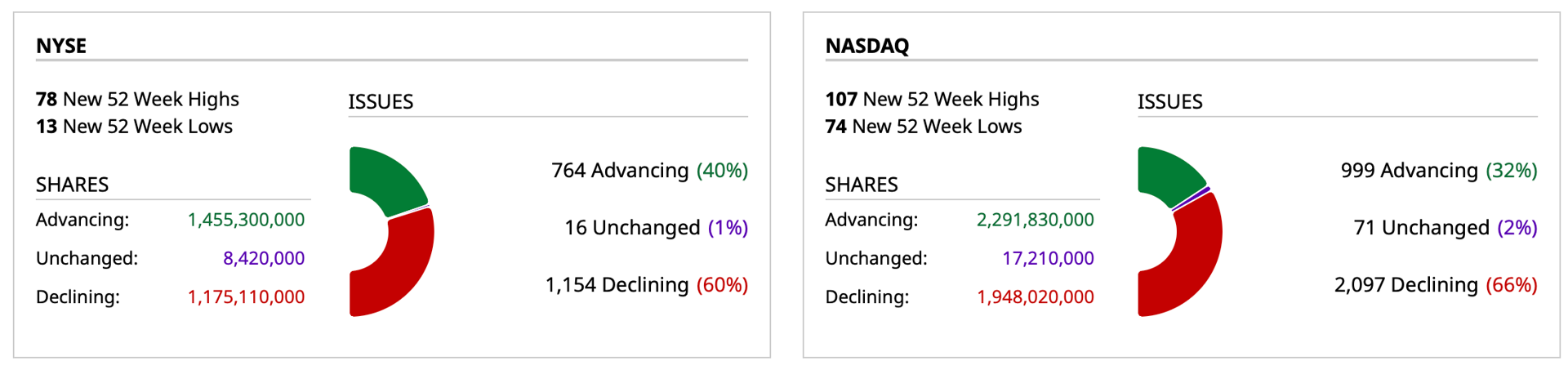

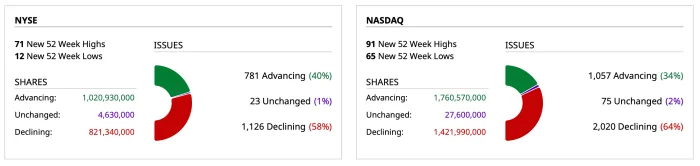

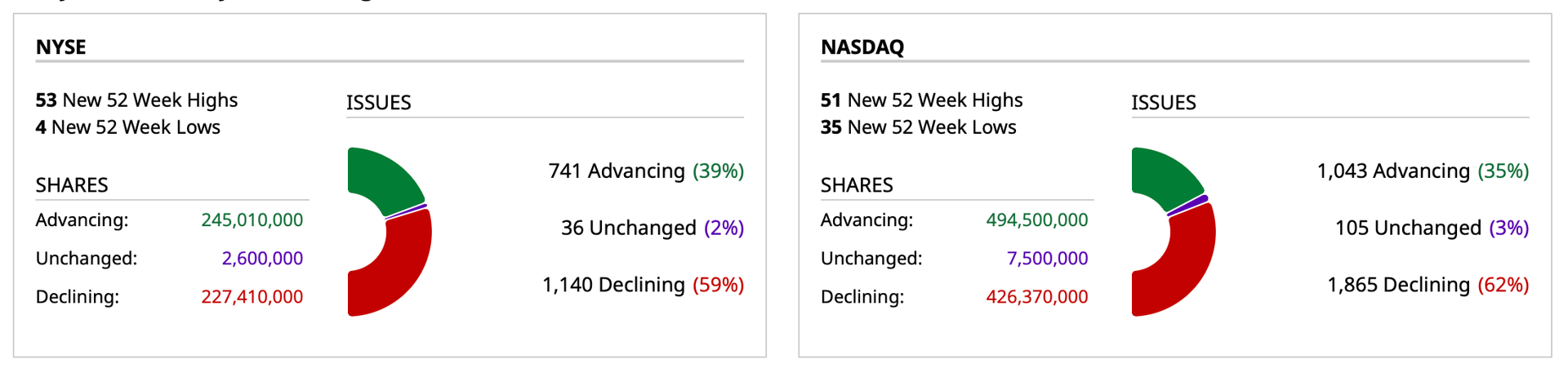

* A meandering market — with, still, an upside bias.

* But poor breadth for the second day in a row — a continuing divergence.

Breadth is weak on the NYSE (around 5-3 negative on the NYSE and 2-1 negative on the Nasdaq):

At 3:15 p.m. S&P cash was +3 handles.

Here are today's "Things" (Note: I was consistent!):

* Apple AAPL shorted at $241.58.

* American Express AXP shorted at $303.28.

* Shorted Citigroup C at $72.46.

* Shorted Goldman Sachs GS at $610.25.

* Shorted Walmart WMT at $93.51.

* With S&P cash -3 handles I shorted SPY/QQQ calls

BY Doug Kass · Dec 3, 2024, 3:16 PM EST

SPY advances since last screenshot...but without any breadth improvement.

BY Doug Kass · Dec 3, 2024, 2:31 PM EST

From Peter Boockvar:

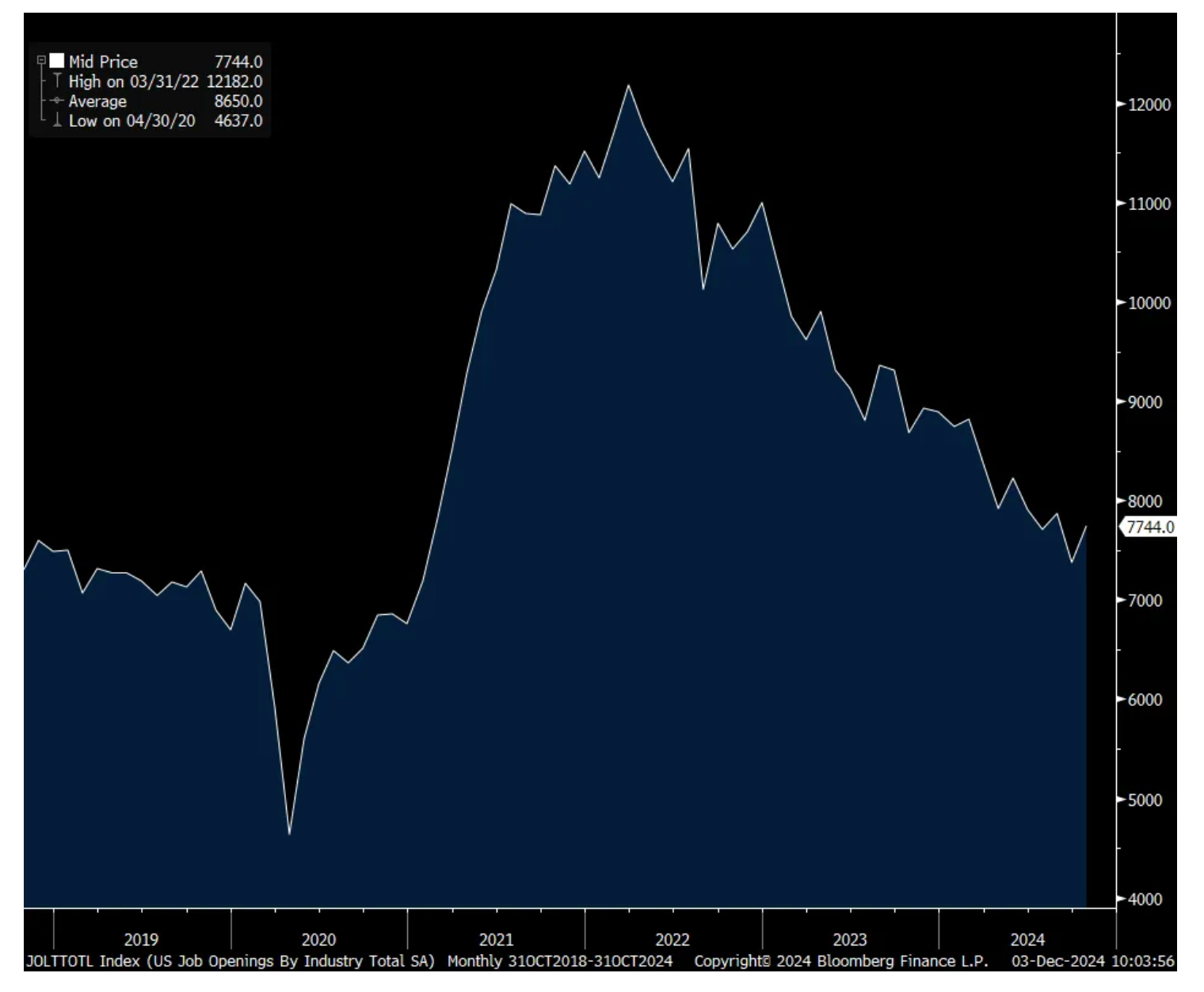

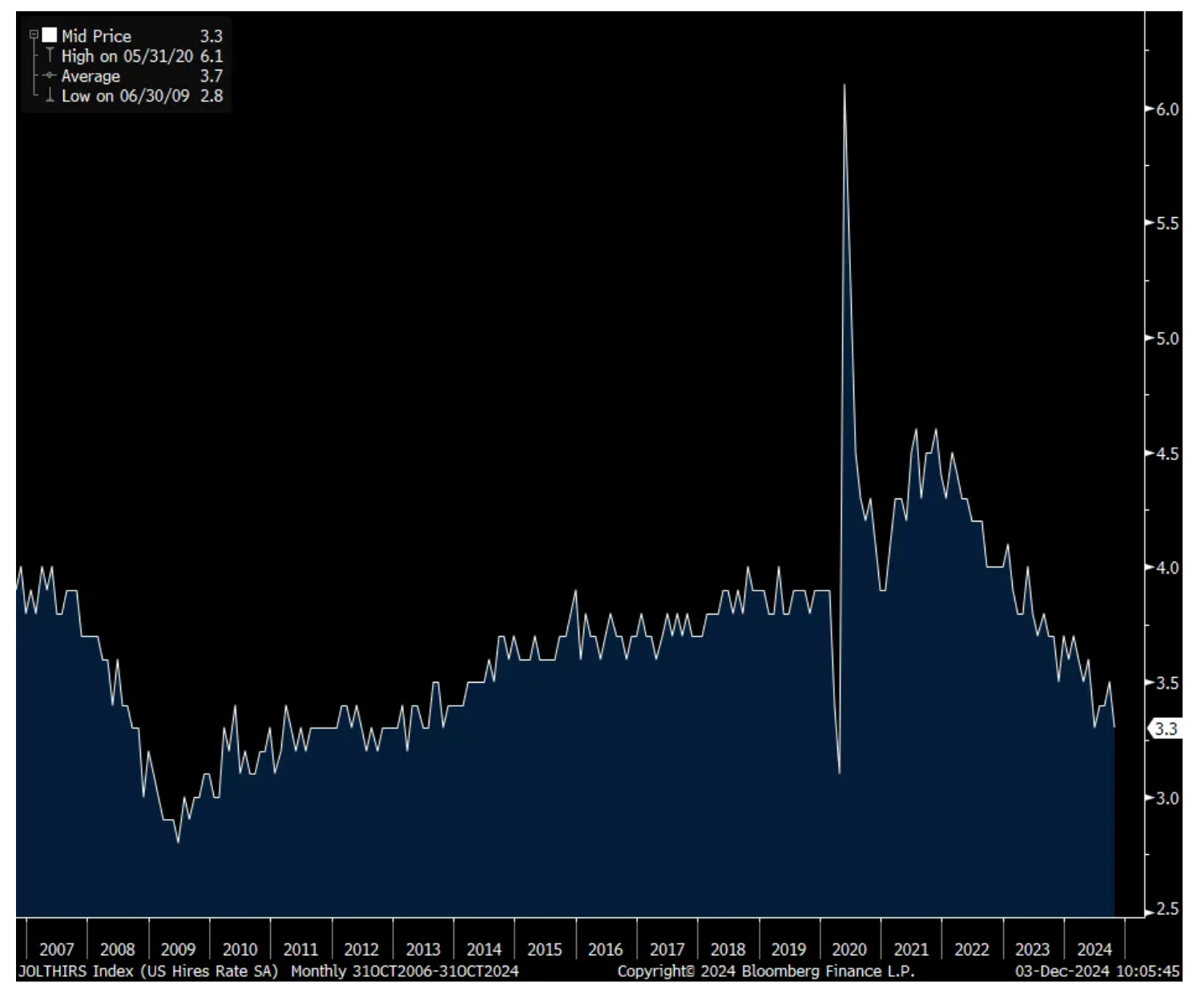

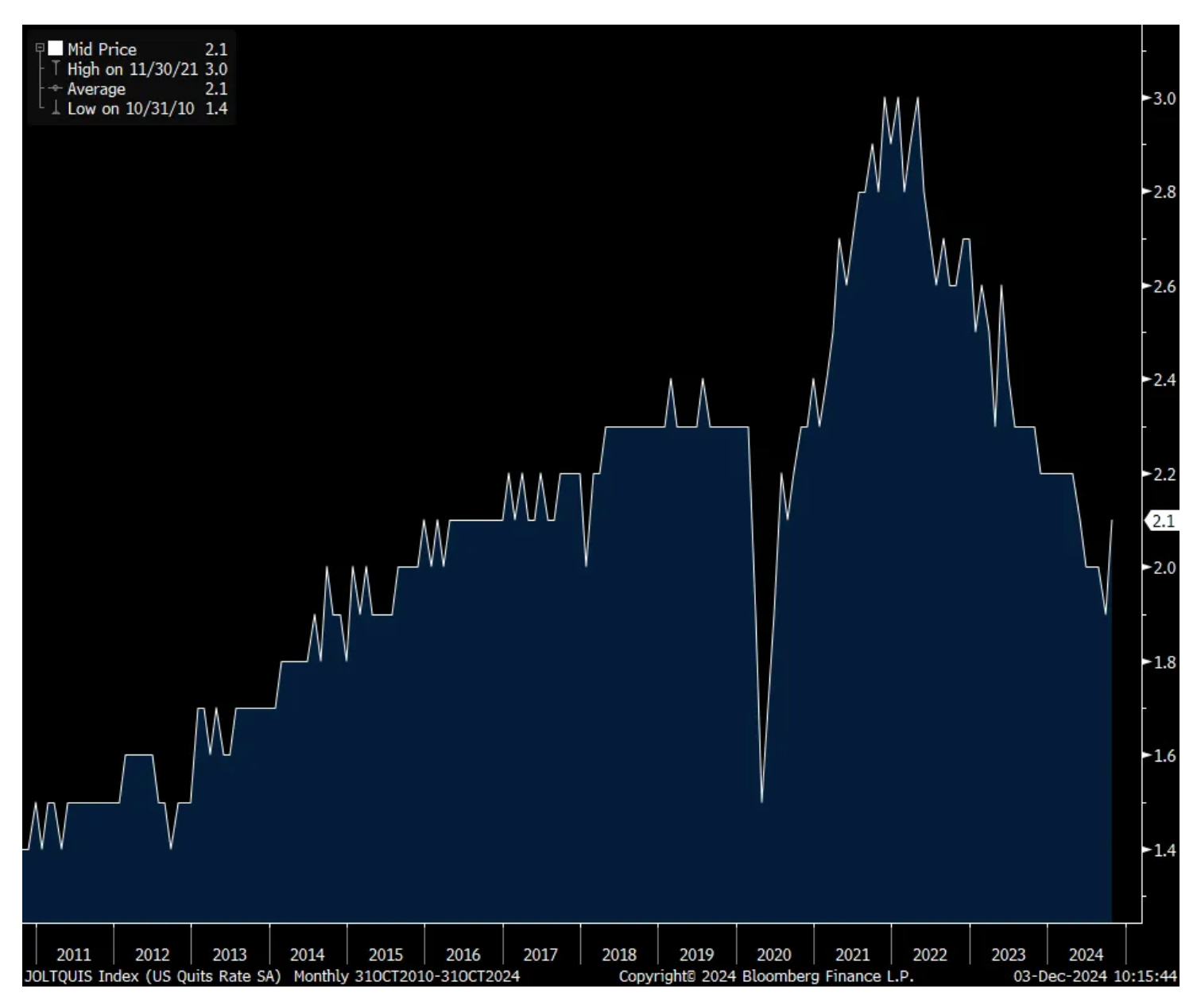

More job openings in October vs September but hiring rate slows again

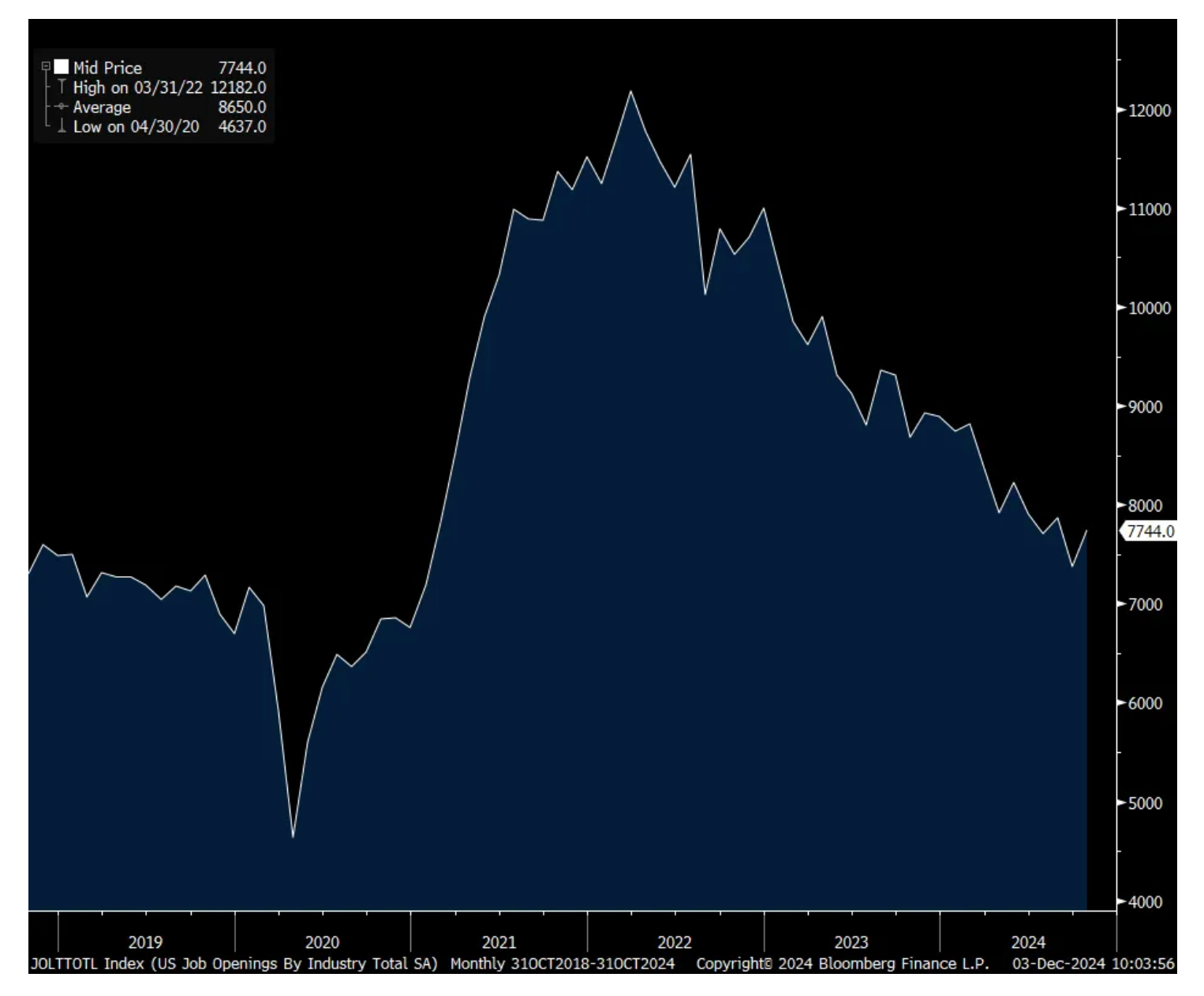

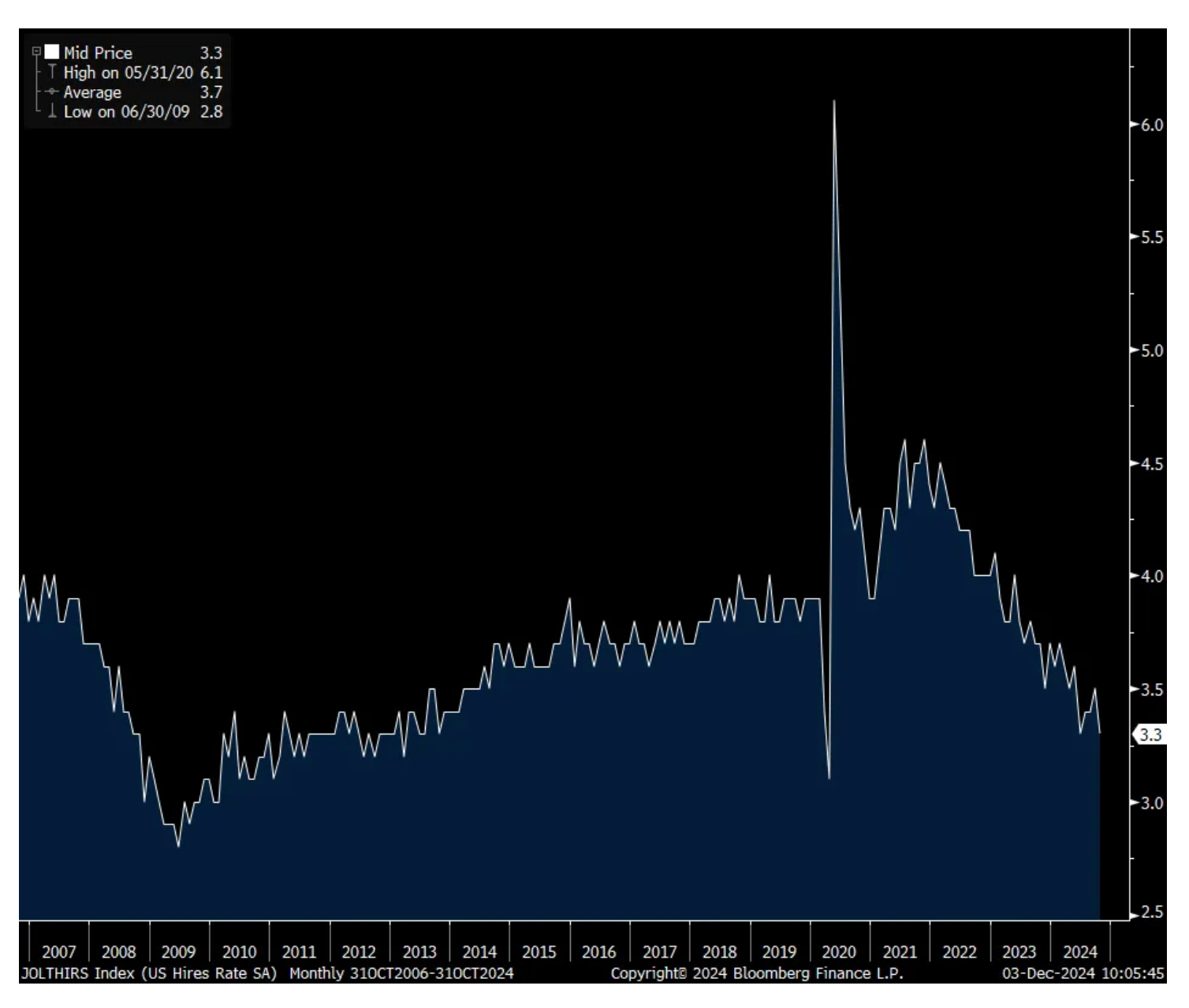

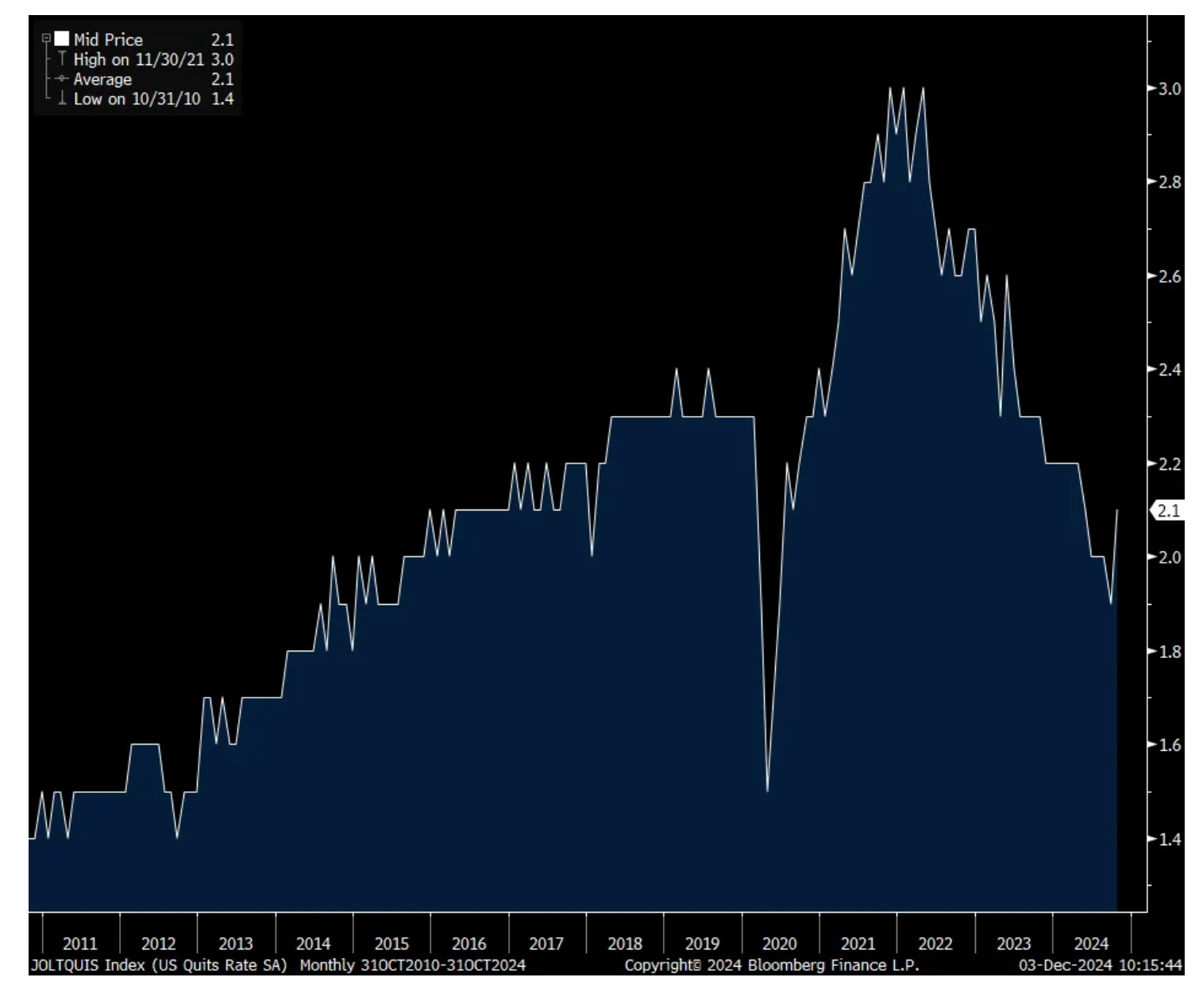

Job openings in October, ahead of the November jobs data we’ll get this week, totaled 7.744mm, 225k above expectations after dropping to 7.372mm in September which was the least since January 2021 and vs 7.861mm in August.

The problem though was the hiring rate which fell to just 3.3% which matches the lowest level since 2013 not including Covid. The number of quits did pick up though with the rate at 2.1% vs 1.9% in September and 2% in August.

In terms of industry, for the 2nd month there has been less job openings in healthcare as maybe finally after Covid, staff levels are back to mostly filled. On the flip side, we did see a lift of 87k in job openings in the ‘information’ sector after a notable slowdown in hiring in some areas of tech over the past few years.

Bottom line, notwithstanding the lift in openings when compared to September, as seen in the chart below and the hiring rate, there has been a clear slowing in the pace of hiring’s.

Job Openings

Hiring Rate

Quit Rate

BY Doug Kass · Dec 3, 2024, 2:17 PM EST

I have been on a research call over the last two hours — regarding my investment in Ligado bonds.

I have called this investment a potential home run.

Now trading near $34 (cost basis $15) I am increasingly confident of the probability that I will get par ($100) for this bond.

In addition, interest (currently in arrears), will likely be payable above par!

Here is a recent update from two weeks ago:

Back in April 2024 I mentioned a possible home run investment in Ligado Networks First Lien Bonds.

Trading at around $15 I thought they were worth par plus accrued interest — giving the investment a possible 8x upside.

I just learned that the company won their lawsuit against the government and I believe the bonds will ultimately be worth par!

Here was my brief outline from April:

* Ligado Networks First Lien 15.5% Bonds

My potential "home run investment" is complicated.

We have invested in Ligado Networks First Lien Bonds (15.5%) - and have paid about $15.

Not only is the story complex (and not without risk), but purchase/sale falls under Rule 144A rules.

As a result, most individual investors will not be able to invest directly in this paper. You can, however, get your money managers to look at this opportunity!

I will discuss this investment fully on my return back to the office next week.

Here is a sneak preview (from Lee Cooperman)... at the five minute mark.

Position: Long Ligado Networks First Lien Bonds

By Doug Kass Apr 26, 2024 11:30 AM EDT

Position: Long Ligado Bonds

DOUG KASS Nov 18, 2024 2:36 PM EST

BY Doug Kass · Dec 3, 2024, 1:52 PM EST

- NYSE volume was 7% below its one-month average;

- Nasdaq volume was 30% below its one-month average

- VIX: up 0.37% to 13.39

BY Doug Kass · Dec 3, 2024, 11:15 AM EST

From Peter Boockvar:

Job openings in October, ahead of the November jobs data we’ll get this week, totaled 7.744mm, 225k above expectations after dropping to 7.372mm in September which was the least since January 2021 and vs 7.861mm in August.

The problem though was the hiring rate which fell to just 3.3% which matches the lowest level since 2013 not including Covid. The number of quits did pick up though with the rate at 2.1% vs 1.9% in September and 2% in August.

In terms of industry, for the 2nd month there has been less job openings in healthcare as maybe finally after Covid, staff levels are back to mostly filled. On the flip side, we did see a lift of 87k in job openings in the ‘information’ sector after a notable slowdown in hiring in some areas of tech over the past few years.

Bottom line, notwithstanding the lift in openings when compared to September, as seen in the chart below and the hiring rate, there has been a clear slowing in the pace of hiring’s.

Job Openings

Hiring rate

Quit Rate

BY Doug Kass · Dec 3, 2024, 10:47 AM EST

I am now close to my largest net short exposure in about nine months.

BY Doug Kass · Dec 3, 2024, 10:16 AM EST

* Shorted C $72.45, AXP $303.37 and AAPL $240.61.

BY Doug Kass · Dec 3, 2024, 10:05 AM EST

Yesterday I increased my short book.

Fundamentals ("slugflation") and valuations (extended and in the 96%-tile) aside, I did this based on several sentiment/technical considerations:

* The S&P Short Range Oscillator is now quite overbought at 5.9%.

* Market breadth yesterday (a day doesn't make a week/month) was decidedly negative in the face I a higher S&P Index (+17 handles) and a smartly stronger Nasdaq (up by over +200 handles).

* Investor sentiment - based on any measure of attitude - remains near universally optimistic. (CNBC Blather: I recently noted in a five-day period, 38 CNBC guests were bullish while none were bearish).

* Bitcoin, a measure of speculation (and often providing a vision of future market reward/risk/volatility), has begun to roll over (declining from nearly $100,000 to $94,000). More significantly, Micro Strategy MSTR (the standard bearer of speculation) has recently declined in price from $540 to $365. (I just watched MSTR's Michael Saylor voice a ton of B.S. on CNBC; he was unchallenged as he sells $1 bills for $3)

Doug Kass: It's Warren Buffett vs. Michael Saylor for the Market Heavyweight Title - TheStreet Pro

We are short bitcoin and Micro Strategy.

* Fear and doubt have left Wall Street as we appear to be in a Bull Market of Complacency.

BY Doug Kass · Dec 3, 2024, 9:33 AM EST

BY Doug Kass · Dec 3, 2024, 9:15 AM EST

-ZJK +372% (NVIDIA expands collaboration for liquid cooling systems)

-PSQH +124% (reportedly Donald Trump Jr. is joining the board of PSQ Holdings Inc., the owner of online marketplace PublicSquare)

-JANX +71% (doses selected for Phase 1b Expansion Trials supported by encouraging efficacy and safety profile observed in Phase 1a Dose Escalation for JANX007 in mCRPC)

-CHRS +54% (announces agreement to divest UDENYCA Franchise for up to $558M to Intas Pharmaceuticals including $483M upfront payment)

-CRDO +31% (earnings, guidance)

-ENLV +27% (announces positive Interim Efficacy Data from Allocetra Trial in Patients with Moderate to Severe Knee Osteoarthritis)

-JFBR +14% (along with Deliverz.AI signs Letter of Intent regarding AI-powered fully autonomous robots)

-MP +14% (China bans export of key minerals to US)

-REX +11% (earnings)

-CNM +8.7% (earnings, guidance)

-SHO +7.1% (Trinity Investments said to be interested in acquiring Co for $13/shr)

-ADEA +6.2% (enters multi-year agreement with Amazon that covers Adeia's media intellectual property (IP) portfolio)

-THRY +5.3% (guidance ahead of Investor Day)

-TERN +3.3% (announces positive early data from Phase 1 CARDINAL Trial of TERN-701 for Chronic Myeloid Leukemia)

-T +2.7% (guidance ahead of Investor Day)

-COMP +2.2% (to acquire Christie's International Real Estate and @properties for ~$465M in stock and class A shares)

-OPTT -46% (reports prelim Q2 revenue)

-INDI -18% (announces proposed Convertible Senior Notes Offering of $175M)

-PPBT -18% (files to sell 473K ADSs at $6.00/unit in $2.8M registered direct offering)

-PLCE -15% (earnings)

-TMDX -8.2% (cuts guidance, appoints new CFO)

-ZS -6.5% (earnings, guidance)

-CLSK -6.3% (earnings, guidance)

-X -6.2% (US Pres-elect Trump says remains "totally against" Co being bought by Nippon Steel or any foreign company)

-AS -5.3% (files to sell up to 34M shares)

-RDVT -5.3% (insider selling; Board declares $0.30/shr special dividend)

-BILL -2.8% (to offer $1.0B of Convertible Senior Notes due 2030)

-ROIV -2.4% (Phase 2 RESOLVE-Lung Study of Namilumab in Chronic Active Pulmonary Sarcoidosis failed to show treatment benefit)

-LYV -2.0% (files to sell $1.0B in convertible senior notes due 2030)

-ONCY -2.0% (completes Initial Safety Phase Enrollment for GOBLET Trial's New Pancreatic Cancer Cohort)

BY Doug Kass · Dec 3, 2024, 9:12 AM EST

Chart from 8:30 a.m. ET:

BY Doug Kass · Dec 3, 2024, 9:05 AM EST

From Peter Boockvar:

My heart breaks with the loss of Art Cashin, both a good friend and an irreplaceable market participant and source for so many of us. His daily writings were always a must read and his personal friendship was something I always treasured as it was not every day when a legend was your friend. The one story I’ll give was his sole use of cash whenever we had dinner together, the countless memorable times. It was typically in a group setting, whether small or large, and he would first request an early start but would usually leave early, leaving me with either one or two crisp $100 bills to cover his cost of dinner. As it was always too much, I would keep the balance in my wallet and thus be his temporary bank, unfortunately without interest, with whatever was left over. The next time we would have dinner, I would make sure to give him his ‘withdrawal’ which he would then apply to that dinner’s bill. Art, as I know you’re reading my comments today from wherever you are now, as you always did and I thank you, I will miss you very much, both personally and professionally.

On to the Fed and I must say the focus of their analysis on whether to cut rates again in December and thereafter is becoming very myopic by their dismissive attitude towards markets and their holy grail view of restrictiveness and narrow focus of it. What is the stock market measuring anyway? Is it a reflection of the market’s view of the present value of future cash flows with a discount rate used? An earnings forecast with a P/E multiple slapped on? Is it just a casino? Is it just some random reflection of emotions with no regards to underlying fundamentals? I want to believe it is mainly the first choice but why would Fed Governor Waller say yesterday in a prepared speech, “I believe the evidence is strong that policy continues to be significantly restrictive and that cutting again will only mean that we aren’t pressing on the brake pedal quite as hard.” Evidence strong? Significantly restrictive? Governor Waller, please be specific, what exactly is being restricted and significantly? Are credit spreads at near record tights and stock market multiples near record highs sending any message that might be worth listening to about the economic and earnings outlook? Yes, the cost of capital is high for many, whether for business or households or anyone in commercial real estate but how do you square this with financial conditions?

As yes, the stock market is not the economy and vice versa, there still is a relationship between earnings growth and stock prices with the unknown multiple applied to it. If the case, why is the Fed ignoring what the market is telling us? What if the stock market is right that the economic and earnings prospects are looking bright with it trading at a record high and near record multiple? Because if it is not and if the Fed is right and its policy is restrictive, implying it is restricting economic activity, then we have an epic equity bubble on our hands. If the stock market is right, then the Fed’s indifference towards it is going to lead to further easing just as the economy is improving which then risks this whole inflation fight.

So Dear Fed, don’t ignore markets. Maybe the economy does need some more rate cuts but wouldn’t it be prudent to wait for some more information on the message that it is currently sending? I believe so and please be more specific of what your definition of ‘restrictive’ is in the current context.

In response to the newly announced export controls on more semi products, particularly high bandwidth memory and certain equipment, to China by the outgoing Biden administration, we're getting a taste of what is to come with tariffs too as China has now banned the shipments of gallium, germanium and antimony to the US. These are key raw materials that we need. According to Reuters, "Gallium and germanium are used in semiconductors, while germanium is also used in infrared technology, fiber optic cables and solar cells." Antimony seems to be used in a lot of different end markets.

Speaking of chips, Microchip lowered its revenue guidance last night and said "We indicated in our November 2, 2024 earnings call that significant turns orders were required to achieve the midpoint of our December 2024 quarter revenue guidance. Those turns orders have been slower than anticipated and we now expect our December 2024 revenue to be close to the low end of our original guidance which is $1.025 billion."

Also, "With inventory levels high and having ample capacity in place, we have decided to shut down our Tempe wafer fabrication facility that we refer to as Fab 2."

We are being reminded again that outside of the AI spend ecosystem, the semiconductor industry is still challenged by lackluster demand for PCs, smartphones and industrial uses.

French politics is headed for a no confidence vote tomorrow as the Barnier government is about to be the shortest tenured rule since 1958 but markets are relatively unperturbed. The euro is holding the $1.05 level and French oats are tame. That said, the CAC is down on the year, also hurt by the luxury brands and slower China spend on its products.

BY Doug Kass · Dec 3, 2024, 8:45 AM EST

Sarge

Morning, Sunshine.

Dougie Kass

To and in memory of Sir Arthur Cashin:

Ain't no time to hate

Barely time to wait

Whoa oh, what I want to know:

Where does the time go?

Grateful Dead, Uncle John's Band Grateful Dead - Uncle John's Band (Alpine Valley 7/17/89)

On this somber day.

To all, play this song before you start your day... and think about our mortality and our wonderful lives...

Dougie

BY Doug Kass · Dec 3, 2024, 8:32 AM EST

On Sunday morning, at 83 years young, my buddy Arthur Cashin passed away. Art Cashin, New York Stock Exchange fixture for decades, dies at age 83

For thousands of market participants Arthur was our boat's captain — steering the market's sometimes rough seas with agility and poetic grace:

O Captain! my Captain! our fearful trip is done,

The ship has weather’d every rack, the prize we sought is won,

The port is near, the bells I hear, the people all exulting,

While follow eyes the steady keel, the vessel grim and daring;

But O heart! heart! heart!

O the bleeding drops of red,

Where on the deck my Captain lies,

Fallen cold and dead.

- Walt Whitman, Oh Captain! My Captain!

With Arthur Cashin's permission I reposted his daily market thoughts in my Diary for almost 20 years.

Arthur seemed to like me and I revered him — perhaps it was our mutual sense of history of the markets that brought us so closely together.

We both spoke our mind — dull to the consequences of transparency and honesty.

We both enjoyed writing our thoughts down on paper. (He literally used "paper," preferring to write out his notes by hand and delivering them to his assistant and my pal, Judi).

We both "didn't suffer fools" as he and I lacked patience and had little tolerance for the incompetent and foolish.

Arthur was religious and his religious market views were steeped in history and historical perspective. His thoughts and opinions were austere, humble and contemplative as if filled with almost monastic clarity.

Over the past three decades I spent many early evenings marinating the ice cubes with Arthur.

All of us were better off having Arthur in our lives — his pearls of wisdom will reverberate for years to come.

Art appeared frequently on CNBC — I especially remembered this interview as he reminisced about 9/11 20 years after that tragedy... UBS's Art Cashin remembers working on Wall Street on 9/11

And here was what I believe to have been his last (or one of his last) interviews that Art had on CNBC about 11 months ago with his dear friend CNBC's Bob Pisani UBS' Art Cashin: Election year tends to be 'good' for the market

To honor my friend, here is the last "Sir Arthur Holds Court" in my Diary in early 2024 — right before his health began to fail:

From Arthur Cashin:

The main influence on Wall Street during the second trading session of the year was not Spartacus or Hitler or any other notable celebrities. Rather, it was a somewhat rotund red cheeked fellow named Santa Claus and what was happening to the supposed Santa Claus rally, which seemed to be disappearing rapidly before the eyes of Wall Street traders. After a setback on the first trading day of the year, things began to look a little difficult for the Wall Street bulls as we were headed for a negative session in the second trading day of the year.

As you probably recall from the writings of Yale Hirsch, who developed the now proverbial Santa Claus rally, it is the last five trading days of the outgoing year and the first two of this year. The first trading day was a lousy session to begin with and traders became more concerned as they moved into the second session, and it did not seem to hold many promises. In fact, as they struggled through the morning, that became the topic among traders, and we touched on a good deal of that in this late morning update: The Wall Street bulls are beginning to worry that a rebellious elf has pushed Santa out of the sleigh.

This is the final day of the so-called Santa Claus rally and the last couple of days it has swung into negative territory. This is not a very good sign for the seasonal success marker. My friend, Jeff Hirsch, editor of the invaluable Stock Trader's Almanac reminds that when the Santa Claus rally fails, it puts in jeopardy or at least puts on the alert signal from a variety of other early seasonal indicators, making it a bit of an uphill fight for the bulls.

The process so far has not been at all helpful to the bulls and the lingering weakness in Apple continues to provide a slight negative tone to the market overall.

Unless the bulls can get the Cavalry out and promote a rescue rally for the afternoon, the old rule of thumb will be getting talked about and that is - if Santa comes to Broad and Wall, the bears may return to make the call. The yields are not providing much influence either way and does seem to look like the markets moving pretty much on its own internals.

Let's see if the newsticker can provide some help because the algorithms are not finding much hope in the internals. If nothing else, a negative close today may, at the very least, slowdown the insertion of funds for the New Year as money managers start to look for sectors that are showing any real promise. Remain alert. Certainly, remain wary, but please stay safe.

Shortly after the update went out, it was convenient that my pal, Josh Brown, partnered with another of my Wall Street trading friends, Barry Ritholz, was on the screen and in Josh's own plain-speaking way nailed down what may be the causation of the Santa Claus rally disappearing and it had little to do with chart angles and moving averages and the like. It had more to do with capital gains and taxes as Josh aptly pointed out. A lot of people with that super late rally in 2023 were thinking about taking some profits and shifting sectors and not making a major decision, but basically repositioning themselves and their portfolios.

As Josh succinctly pointed out, one of things they normally would have to think about was their financial officers looking over their shoulder and saying - if you trim your position or shift your position here in the closing days of 2023, you are going to have to declare it on the taxes of this year that is now ending or if you wait and change those positions and make those decisions in the opening days of the new year 2024, you had the luxurious latitude of waiting days, weeks or even months before you had to declare for taxation purposes the day of that trade and make payments on the capital gains you might or might not owe.

What prompted this selling in the first two trading of this month - shooting Santa Claus in the foot - in all likelihood was something that had technically nothing to do with the stock market but more to do with tax positions of the entity who is doing the trading. Simply succinct and right on the mark as usual and once again, Josh laid it out to all of us that the answer was something you did not need a slide rule, calculator or a computer to determine.

Just tax timing. Pretty simple. Well, simple it may have been, but it did cause them to shoot the Santa Claus rally in its foot, perhaps even in both feet as it raised questions about the indications of the first few trading days toward the overall trading for the year 2024 and that will cause us and many others over the next several days to try and compute - are we seeing a true indication of what the balance of the years trading may look like or are we just stubbing our toe on an axiom of tax declarations. Nonetheless, the guidelines of an indicator are certainly the guidelines of the indicator. We were going to review those rather rare occurrences when the Santa Claus rally does not kick in, but overnight, our friend Jeff has magnanimously dipped into his prodigious files, and this is what he wrote:

On the heels of last year's momentous rally, the market is showing some signs of weakness causing the Santa Claus Rally to fail to materialize. Profit taking in January has become more commonplace in the last 25 years or so and January is notably softer in election years like 2024. Some profit taking is understandable following the massive rally from the end of October ranging from just over 16% for DJIA and S&P 500 to 19.9% for NASDAQ and 26.2% for Russell 2000 at their respective recent highs just before yearend. But the selling over the past few days is notable and a warning sign. Defined in the Stock Trader's Almanac, the Santa Claus Rally (SCR) is the propensity for the S&P 500 to rally the last five trading days of December and the first two of January with an average gain of 1.3% since 1950.

This indicator was discovered and first published by Yale Hirsch in the 1973 edition of the Almanac. The lack of a rally can be a preliminary indicator of tough times to come. This was certainly the case in 2008 and 2000. A 4.0% decline in 2000 foreshadowed the bursting of the tech bubble and a 2.5% loss in 2008 preceded the second worst bear market in history. Down SCRs were followed by flat years in 1994, 2005 and 2015, and a mild bear that ended in February 2016. Of the 15 down SCRs since 1950, 10 years have been up and 5 down, but the average gain is a measly 5.0%. As Yale Hirsch's now famous line states, "If Santa Claus should fail to call, bears may come to Broad and Wall."

With the Santa Claus Rally a no show we will be watching for a positive First Five Days (FFD) and January Barometer (JB), the second and third legs of our January Indicator Trifecta. Since 1950 there have been only three occurrences when SCR was down and both the FFD and JB were positive. Two out of three of those years were up over 20% and 1994 was a flat -1.5% with a 14.8% average gain on all three. Since there are only three down SCR years with up FFDs and JBs we present to you the other years with one of the Trifecta components down and the other two up. Of these 18 years 14 years were up and 4 were down with an average gain of 7.9%. So, as we said 2 out of 3 ain't bad when it comes to our January Indicator Trifecta.

Remember: if these seasonal indicators are negative and the market does not rally as it normally does during this time, we will likely shift to a less bullish posture - if not outright bearish. Thank you, Jeffrey, for that thorough review of some past occurrences.

Okay, now back to this morning. Overnight, global equity markets are once again showing signs of individuality. Japan closed down the equivalent of 180 Dow points. Hong Kong was flat. Mainland China was off about 130 Dow points and India was a bit of an odd man out, closing up the equivalent of about 250 Dow points. As we go to press, Europe is marginally optimistic. London is fractionally higher, but Paris and Frankfurt are up about the equivalent of 100 Dow points.

The calendar is not overly busy, but we begin with some job type information. Early on, we get the Challenger Layoff Report and at 8:15, we get the ADP Payroll Estimate and then at 8:30, of course, the Initial Jobless Claims and right after the opening, we get the PMI Composite. In midmorning, we get Natural Gas Inventories and, a little bit later, we get the Oil Inventories because of the New Year holiday earlier in the week.

After the close, traders will go to the newsticker to see what the Fed Balance Sheet looks like and if quantitative tightening continues and to what degree. A lot of finger pointing in the Middle East and some speculation that a further crackdown with the Houthi rebels may be in order, but no official confirmation one way or another.

Given the fact that geopolitics is bubbling up again, best stick to the current drill and that is stay very close to the newsticker. Keep your seatbelt fastened.

Stay nimble and alert and given these fractious times, please stay safe.

By Doug Kass Jan 4, 2024 9:35 AM EST

BY Doug Kass · Dec 3, 2024, 7:32 AM EST

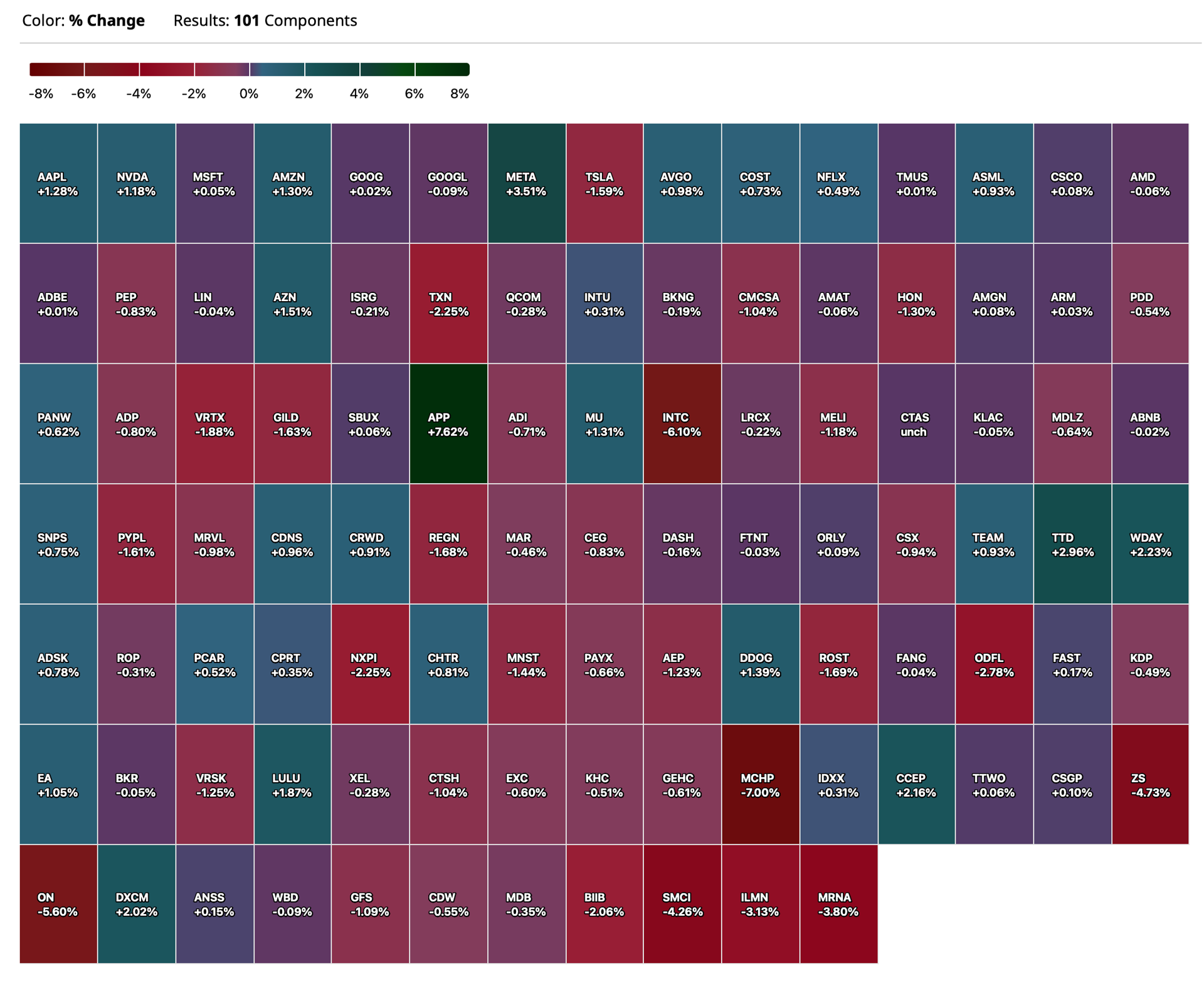

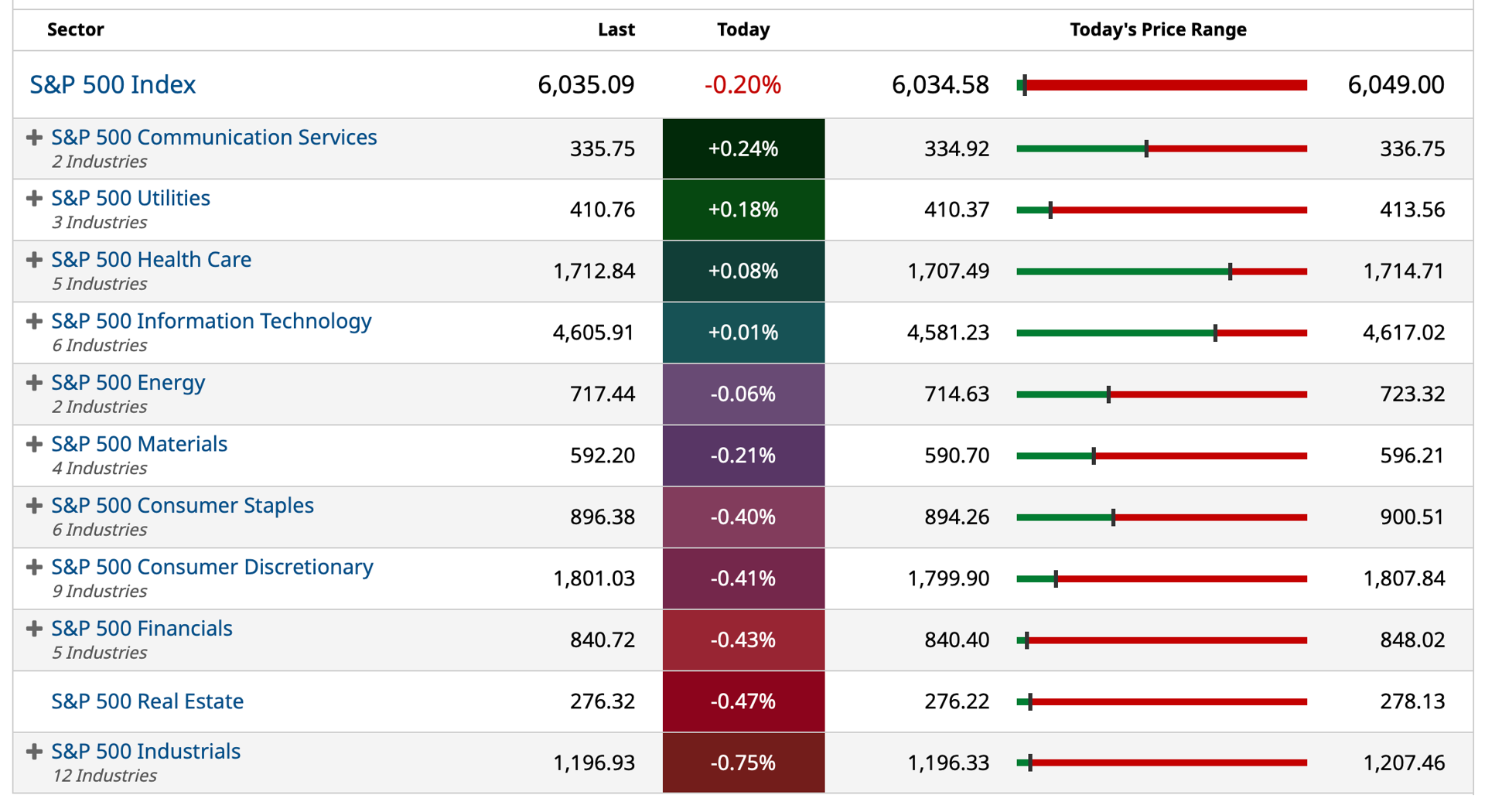

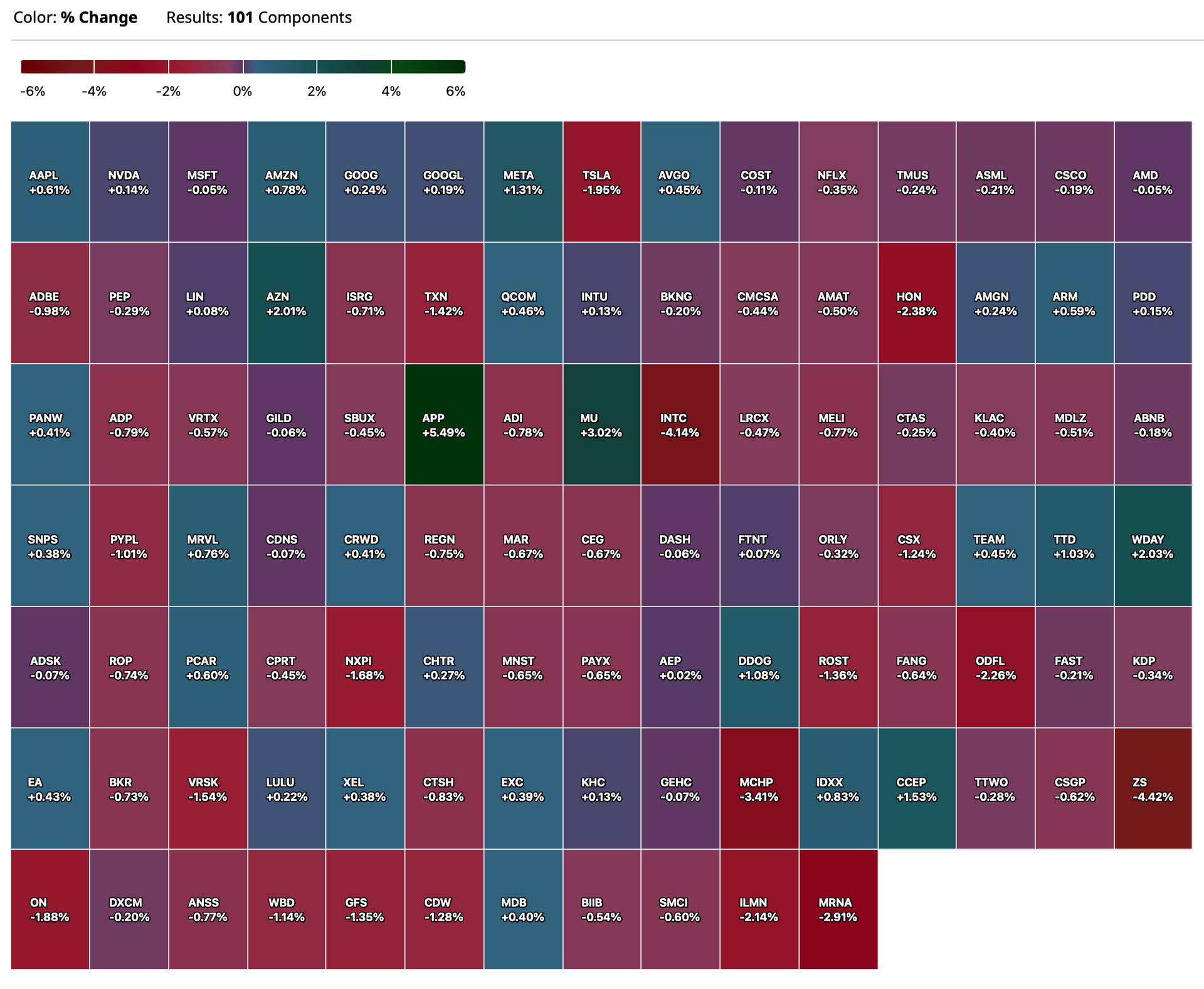

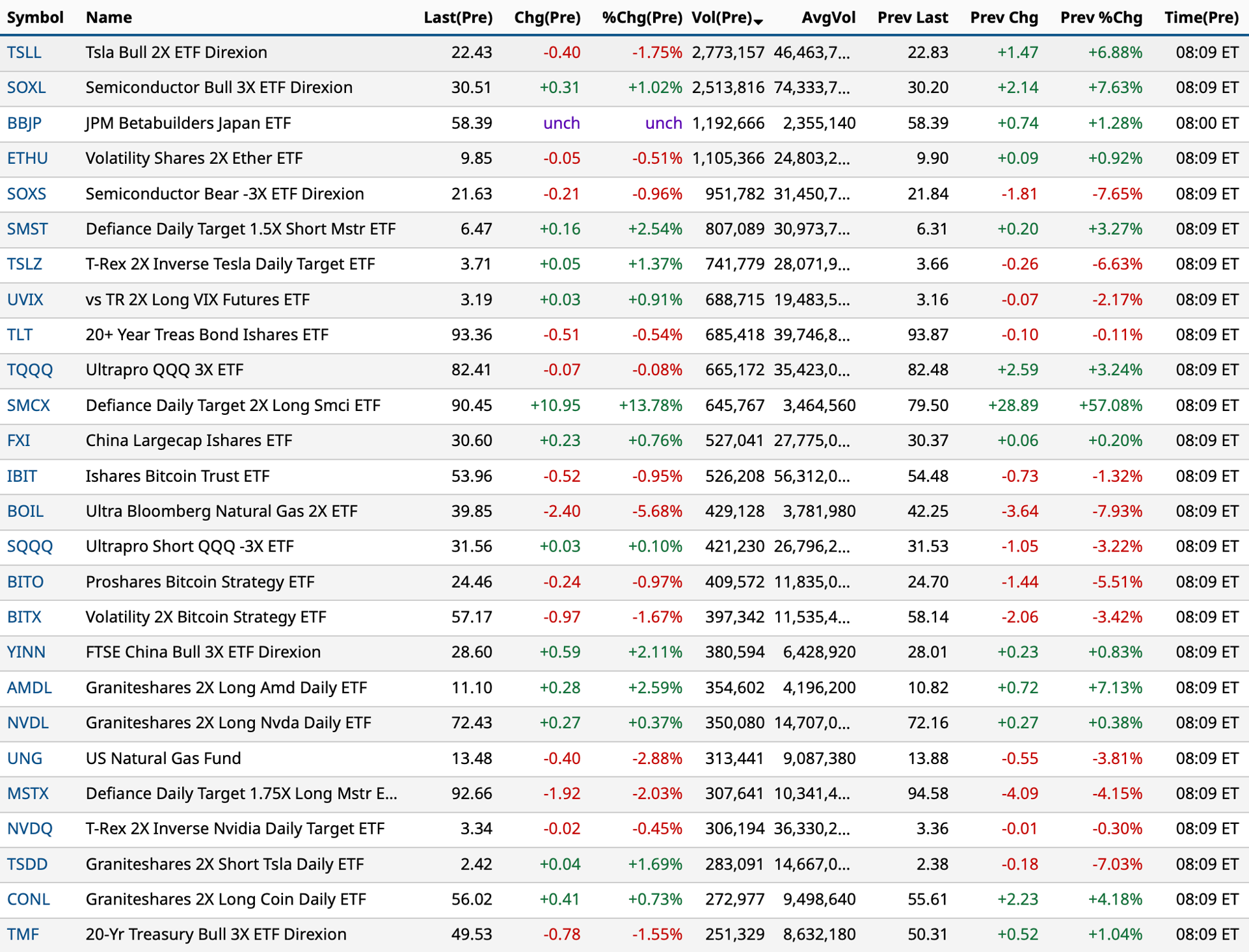

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Dec 3, 2024, 7:12 AM EST

I lean, tactically, on this Indicator for my short-term trading rental positioning.

And the S&P Short Range Oscillator is flashing an even more overbought — at 5.9% (last night) vs. 5.5% at the close of last week.

Yesterday I added to my short book on the continued market strength.

BY Doug Kass · Dec 3, 2024, 7:02 AM EST

From JPMorgan:

US: Futs are flat as the yield curve sees slight steepening; the US is not benefitting from the risk-on rally seen in EU/APAC. Pre-mkt, Mag7 names are mostly higher as Semis are bid. USD is lower as the cmdty complex catches a bid; WTI, silver, and sugar the outperformers. BBG reports China moved to restrict exports of metals to the US used in high-tech/military applications (gallium, germanium, antimony, and other superhard materials). Today’s macro focus will be on JOLTS and Vehicle Sales.

and...

EQUITY AND MACRO NARRATIVE: yesterday was a quiet session that saw stock grind higher with TMT leading as Mag7 and Semis added 1.7% and 2.4% (SMH), respectively. Bond yields moved lower during the session given (i) ISM-Mfg Prices Paid component printed materially below expectations, 50.3 vs. 55.2 survey; 54.8 prior and (ii) Waller comments on a December rate cut being the base case unless something “bad” happens.

Here were my thoughts immediately after the print: ISM-Mfg ticks higher, as expected, but not yet a game changer for markets since the print is below 50. Though, XLI is ticking higher post print as USD catches a bid. This does little to change the current market narrative of a No Landing/Soft Landing/Goldilocks. That said, if (or when) we see ISM-Mfg move back above 50 I think that will give investors more comfort that we are mid-cycle rather than late-cycle. Our view is that growth accelerates higher in 25H1, taking GDP back above 3%, unemployment below 4%, which means yields will remain higher, too.

JOLTS – Feroli tells us, “We look for the October job openings in the JOLTS to be basically unchanged at 7.45mn, and the job openings rate should stay at 4.5%. Our projection for no change does not reflect stability in other measures of job openings such as those from Indeed or LinkUp, which fell between the end of September and October. Rather, it reflects that the job opening rate has now returned to where one would expect it to be based on its pre-pandemic relationship with the unemployment rate. In addition, the job opening rate has fallen more steadily in the JOLTS than in those other reports, which is another reason why it could pause its decline in October.

Besides the job opening rate, we will be looking at the behavior of quits and layoffs: the quit rate has steadily declined to the lowest level since 2015 (ex-COVID), suggesting a softening labor market. This has come through in weaker hiring rates but generally not higher layoffs. The layoff rate did rise in September to 1.2%, the first time it has broken out of the 1.0%-1.1% range since early 2023, though that remains a low rate. The rise was concentrated in durable goods manufacturing. While our initial thought was that this could be related either to Boeing suppliers or to the layoffs that have caused a pop in jobless claims in the Midwest, the rise was in fact entirely concentrated in the Northeast region.”

BY Doug Kass · Dec 3, 2024, 6:52 AM EST

BY Doug Kass · Dec 3, 2024, 6:37 AM EST

BY Doug Kass · Dec 3, 2024, 6:27 AM EST

BY Doug Kass · Dec 3, 2024, 6:17 AM EST

"Never bet on the end of the world, because it only happens once, and even if it does, who are you going to settle the trade with?"

- Art Cashin

BY Doug Kass · Dec 3, 2024, 6:07 AM EST

BY Doug Kass · Dec 3, 2024, 5:57 AM EST

From Doomberg... Power Down Blunder - Doomberg

BY Doug Kass · Dec 3, 2024, 5:47 AM EST