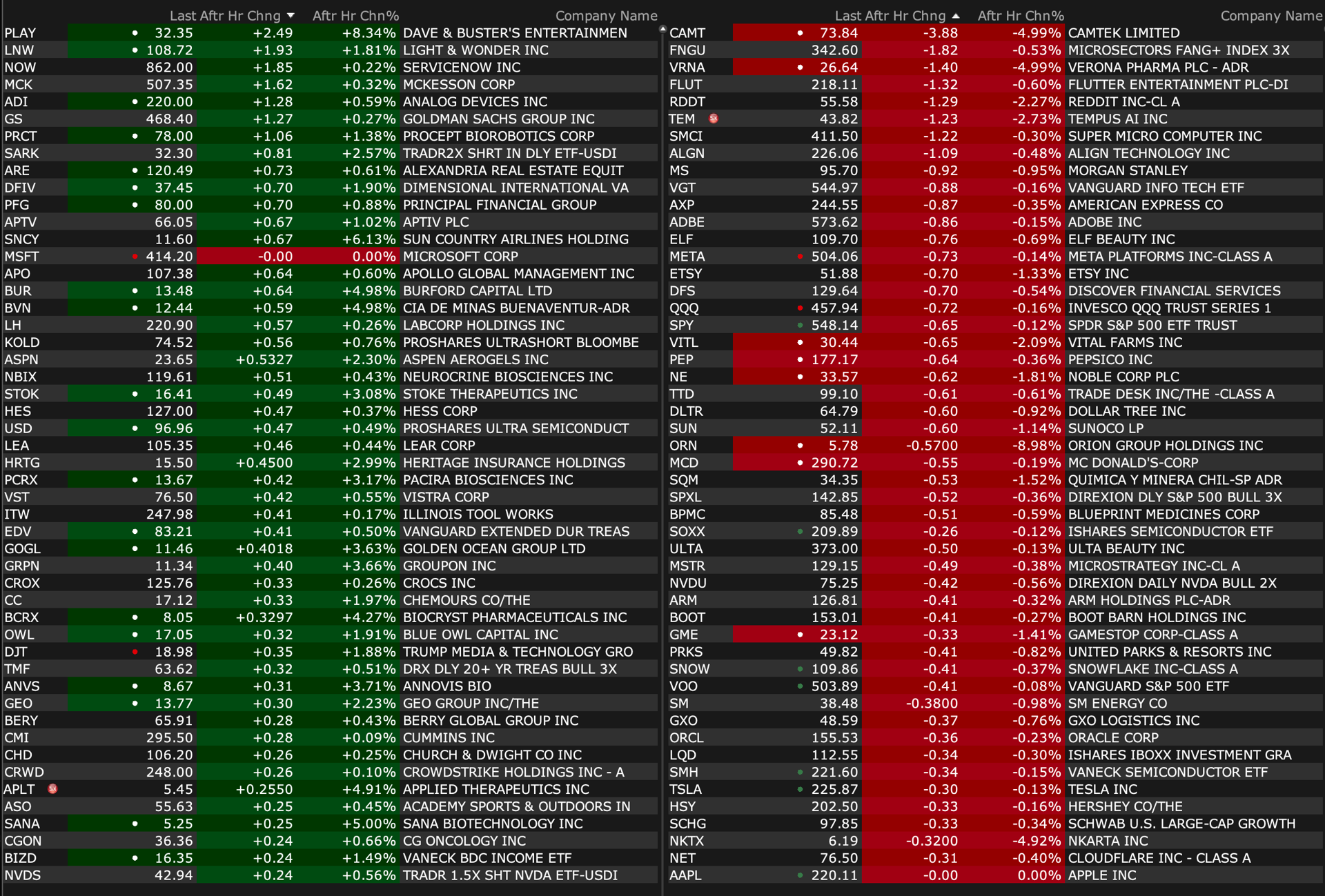

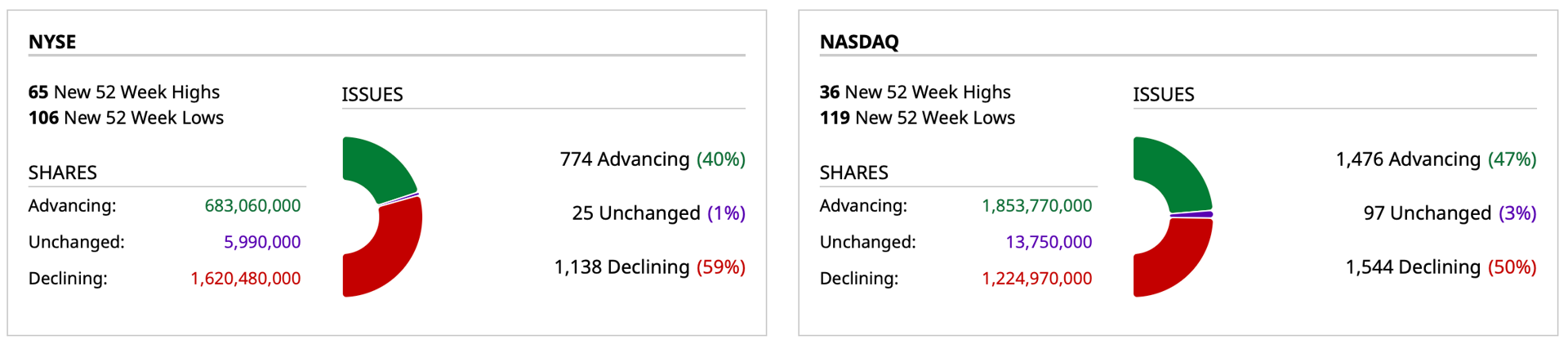

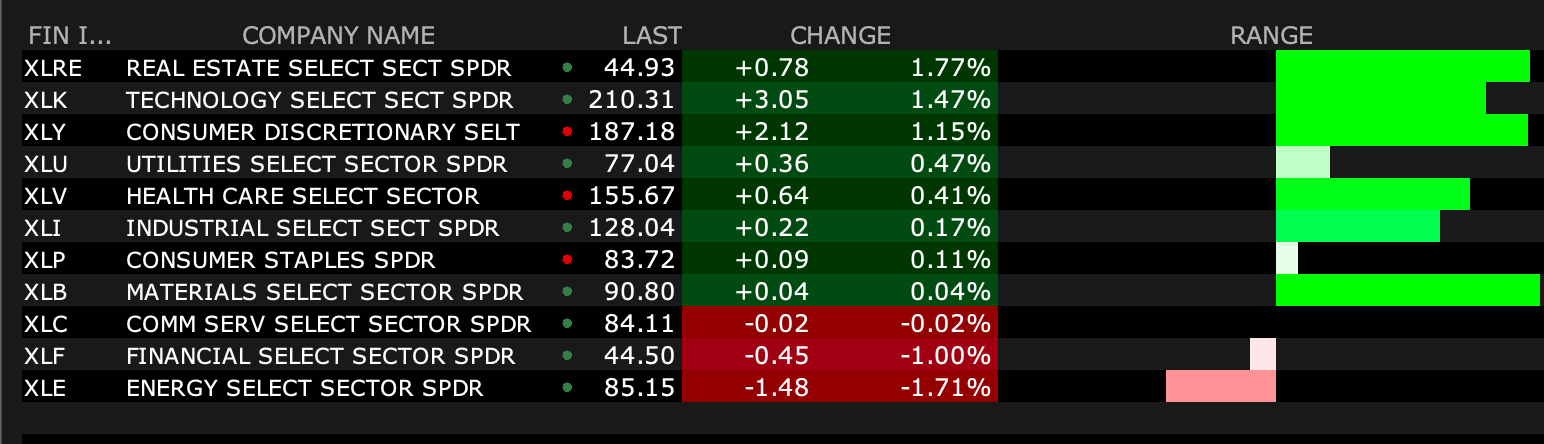

After-Hours Movers

As of 4:35 p.m.:

BY Doug Kass · Sep 10, 2024, 4:45 PM EDT

As of 4:35 p.m.:

BY Doug Kass · Sep 10, 2024, 4:45 PM EDT

BY Doug Kass · Sep 10, 2024, 4:20 PM EDT

* To stay abreast and as a reminder — I introduced this new column last week.

* In which I recap the meaningful trading/investing moves that I did during the trading session.

* Please give me feedback in the Comments Section if this is helpful or if you would like me to add anything to the column.

I came into the day modestly net long and slightly increased my net exposure in the face of a number of short covers (made during the morning's weakness):

* New long — SLB ($39.26).

* Added to a small OIH long (at around $269.60).

* Covered AXP ($242.50) and JPM ($206-ish) shorts on very meaningful gaps lower and very close to the day's lows. I will re-short on strength.

* I covered my XLF short ($44.30).

*Added to XLU short ($77.07).

* Covered BOOT short at $151.30 for a loss.

* There was no Index (SPY/QQQ) activity today.

Overall I did a medium amount of trades but my day was filled with four different research/company calls.

As I mentioned in this column yesterday:

"Given the market volatility I am trading around my positions more actively today and over the last few weeks."

Tomorrow I will update my market outlook!

BY Doug Kass · Sep 10, 2024, 4:10 PM EDT

I purchased a starter position in Schlumberger SLB at $39.26.

BY Doug Kass · Sep 10, 2024, 3:08 PM EDT

First sign of weakness in XLU....

Pressing the short.

BY Doug Kass · Sep 10, 2024, 2:34 PM EDT

* Not market related but I was such a fan

* I intensely followed Arnie's career (and he will always be in my thoughts)...

If alive, my second (you can guess my first! Hint: see my opener today, "Perfect") favorite athlete of all time (Arnold Palmer), would have been 97 years old today.

* The absolute best Arnold Palmer TV commercial:

* Arnie's last competitive start in a PGA tournament event:

BY Doug Kass · Sep 10, 2024, 1:50 PM EDT

Tune in to MRKT Call at 1 PM if you want to hear solid commentary, transparency of positions and honesty (they take ownership of winners and losers!) with my buds Guy, Carter and Dan.

Let's go to the video tapes! What The S&P 500 Chart Is Telling Us - YouTube]

And it's free!

BY Doug Kass · Sep 10, 2024, 1:06 PM EDT

* No broadening...

BY Doug Kass · Sep 10, 2024, 12:30 PM EDT

At 11:35 a.m.:

BY Doug Kass · Sep 10, 2024, 12:15 PM EDT

BY Doug Kass · Sep 10, 2024, 12:10 PM EDT

I covered the balance of my JPMorgan JPM at $203.88 and my XLF short at $44.28.

As well, I have covered my AXP short at $243.1 for a near +$10 gain in a day.

From yesterday:

Back short American Express (AXP) at $252.93.

Position: Short AXP (VS)

By Doug Kass Sep 9, 2024 1:26 PM EDT

BY Doug Kass · Sep 10, 2024, 11:15 AM EDT

I have covered most of my JPM short for a substantial 24-hour gain (as the shares have slipped from $220 to $206.15).

I have also covered a substantial amount of my XLF short at $47.30.

I plan to re-short both on any rally.

BY Doug Kass · Sep 10, 2024, 10:45 AM EDT

Boot Barn BOOT gapped higher on strengthening short-term sales — something I did not anticipate.

I covered my short at $151.30 for a loss.

BY Doug Kass · Sep 10, 2024, 10:38 AM EDT

From Peter Boockvar:

As we debate cadence of rate cuts, balance sheets continue to shrink/Small business still not optimistic

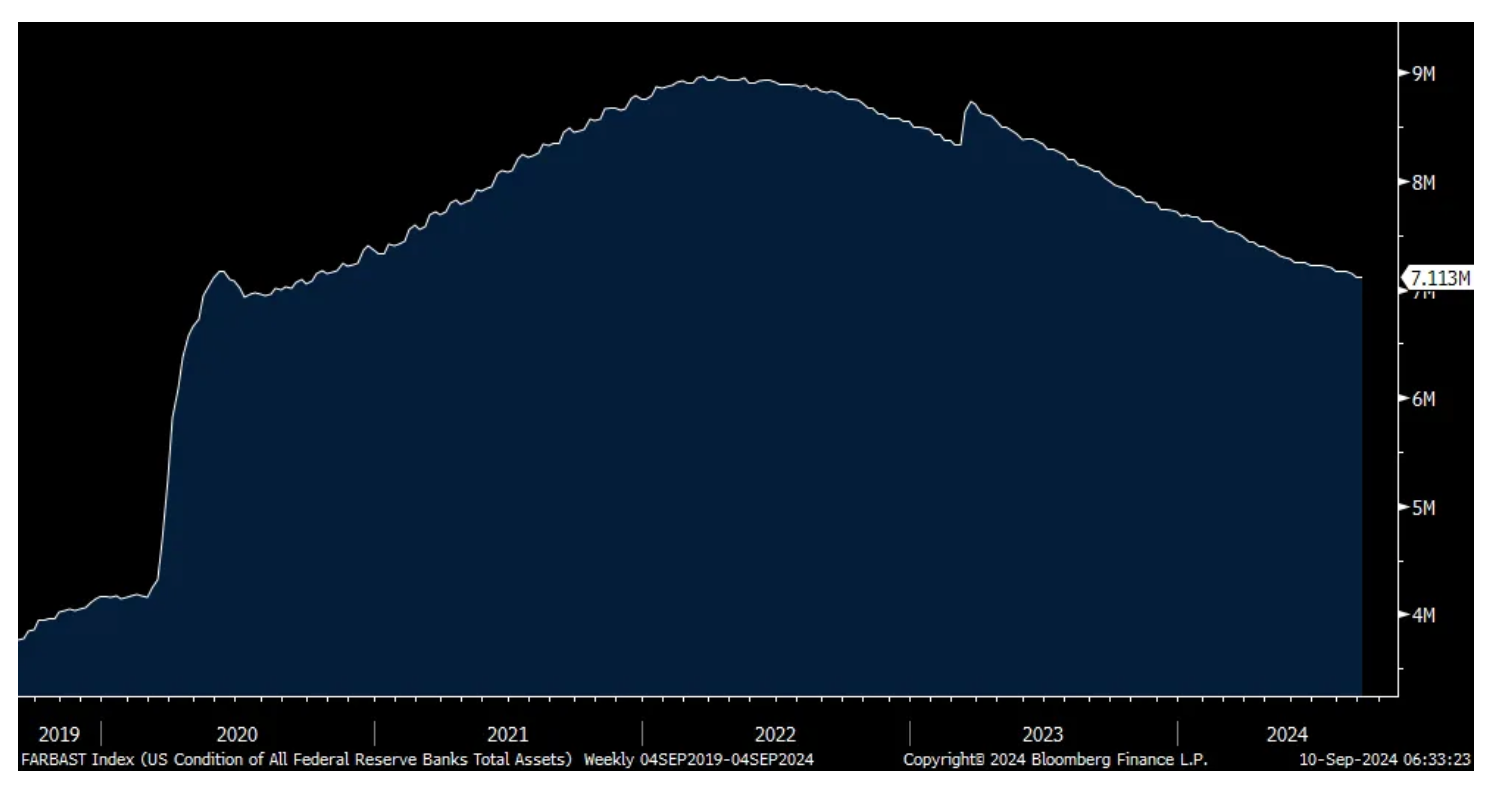

While many debate whether the Fed should cut 25 or 50 bps next week, with 100 bps priced in already into the fed funds futures market, that implies a 50 bps cut at one of the next three meetings. And the market is pricing in 233 bps thru next September. Thus, it's irrelevant whether it is 25 or 50 bps next week, it's well priced in already. What no one is talking about, and ahead of an ECB rate cut this Thursday too, is that central bank balance sheets continue to shrink and is a silent liquidity drain. That said, at least with the Fed, their balance sheet is still so enormous. At $7.1 trillion, it has reversed all the fluff QE that started in June 2020 when after the panic buying during the shutdowns ended, and it slowed to a still high $95b per month. But that compares with a still large $4.16 trillion level in February 2020. Ben Bernanke truly created a monster that has still yet been contained and likely never will.

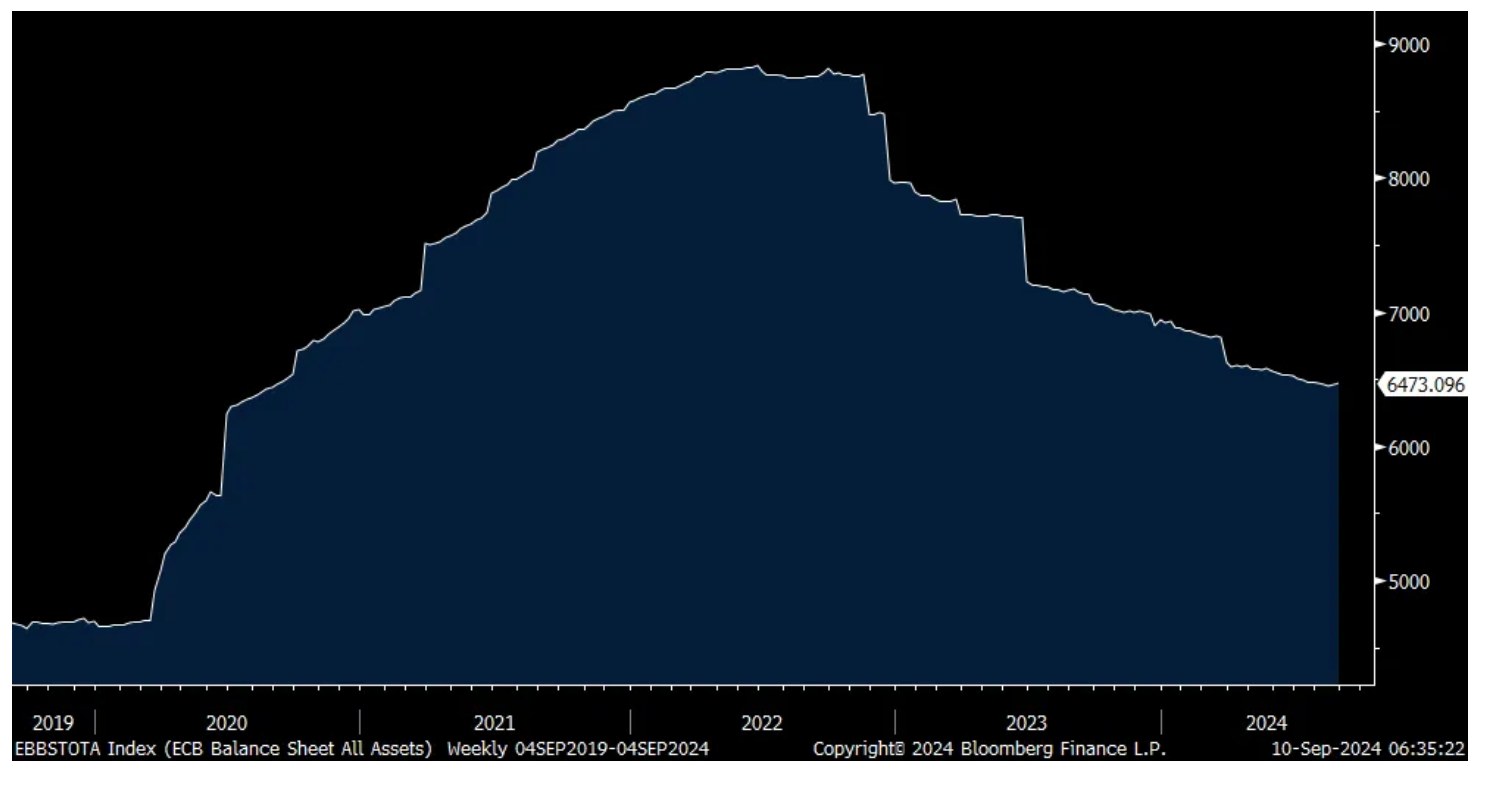

The ECB's balance sheet has shrunk by 2.35 trillion euros to the lowest since September 2020 but still 1.7 trillion euros above where it stood in February 2020.

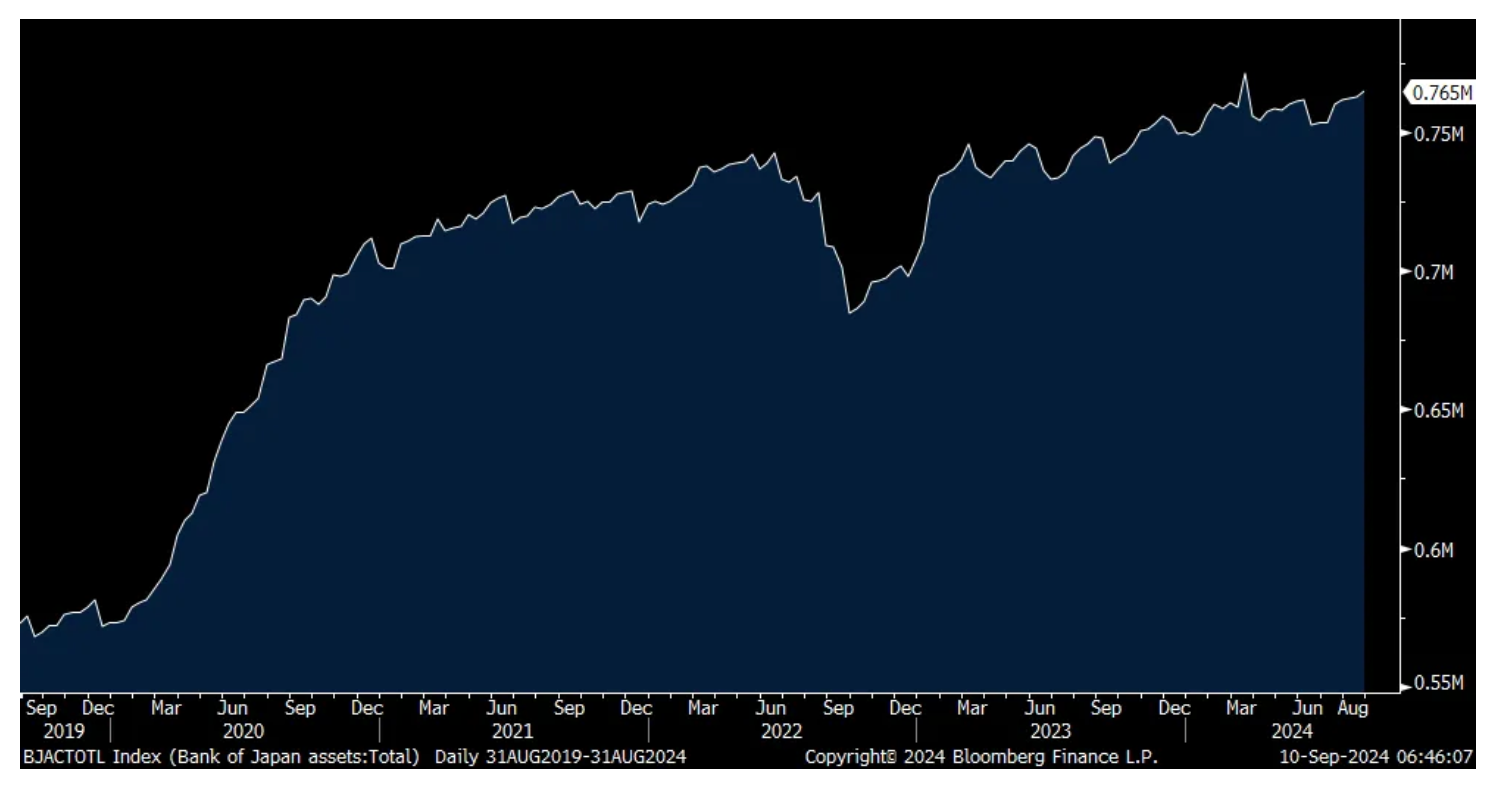

The Bank of Japan's balance sheet has barely grown over the past year and their pace of purchases will continue to slow thru March 2026 to maybe an eventual end.

Something to watch because the shrinkage will continue even as rates get cut in most places, but hiked in Japan.

Fed's Balance Sheet

ECB Balance Sheet in euros

Bank of Japan Balance Sheet in yen

With respect to the BoJ, they meet next week and they won't be hiking again just yet. From Bloomberg News, "Bank of Japan officials see little need to raise the benchmark rate when board members gather next week, as they're still monitoring lingering volatility in financial markets and the impact of the July hike, according to people familiar with the matter." Those 'people' who always seem to know everything.

The NY Federal Reserve released its August results of its Consumer Expectations survey and the inflation guesses both 1 yr and 5 yrs out were unchanged at 3% and 2.8% respectively. The 3 yr finger in the air guess was 2.5% vs 2.3% in the month before. Price expectations grew for homes, gas, rents and medical care and fell for food and college.

Employment expectations weakened as the mean probability of those expecting a rise in unemployment rose to 37.7% from 36.6% in July. On the other hand, there was a reduction in those thinking they personally would lose their job. Income expectations rose slightly as they did for spending.

On the credit side, "Perceptions of credit access compared to a year ago improved with a smaller share reporting tighter conditions compared to a year ago." However, and especially of note, "The average perceived probability of missing a minimum debt payment over the next three months increased by .3 percentage point to 13.6%, its 3rd consecutive increase. The current reading is the highest since April 2020." I bolded for emphasis.

Not that this is a surprise to any of us that have heard from a variety of consumer touching companies over the past few months, particularly retailers, but the CFO of Citi at the Barclays conference yesterday said "The nature of spend is evolving. It's going from discretionary to a more staple-type spend."

Highlighting the importance of Oracle's cloud business, they guided to overall revenue growth for Q2 of just 7% to 9% y/o/y in constant currency but their cloud revenue is expected to rise by 23% to 25% in constant currency. In terms of count, Larry Ellison said "Today, Oracle has 162 cloud data centers, live and under construction throughout the world." The biggest debate in tech right now seems to be, how much is enough? I have zero idea.

I didn't see any macro comments from them as about every single question was asking/talking about AI.

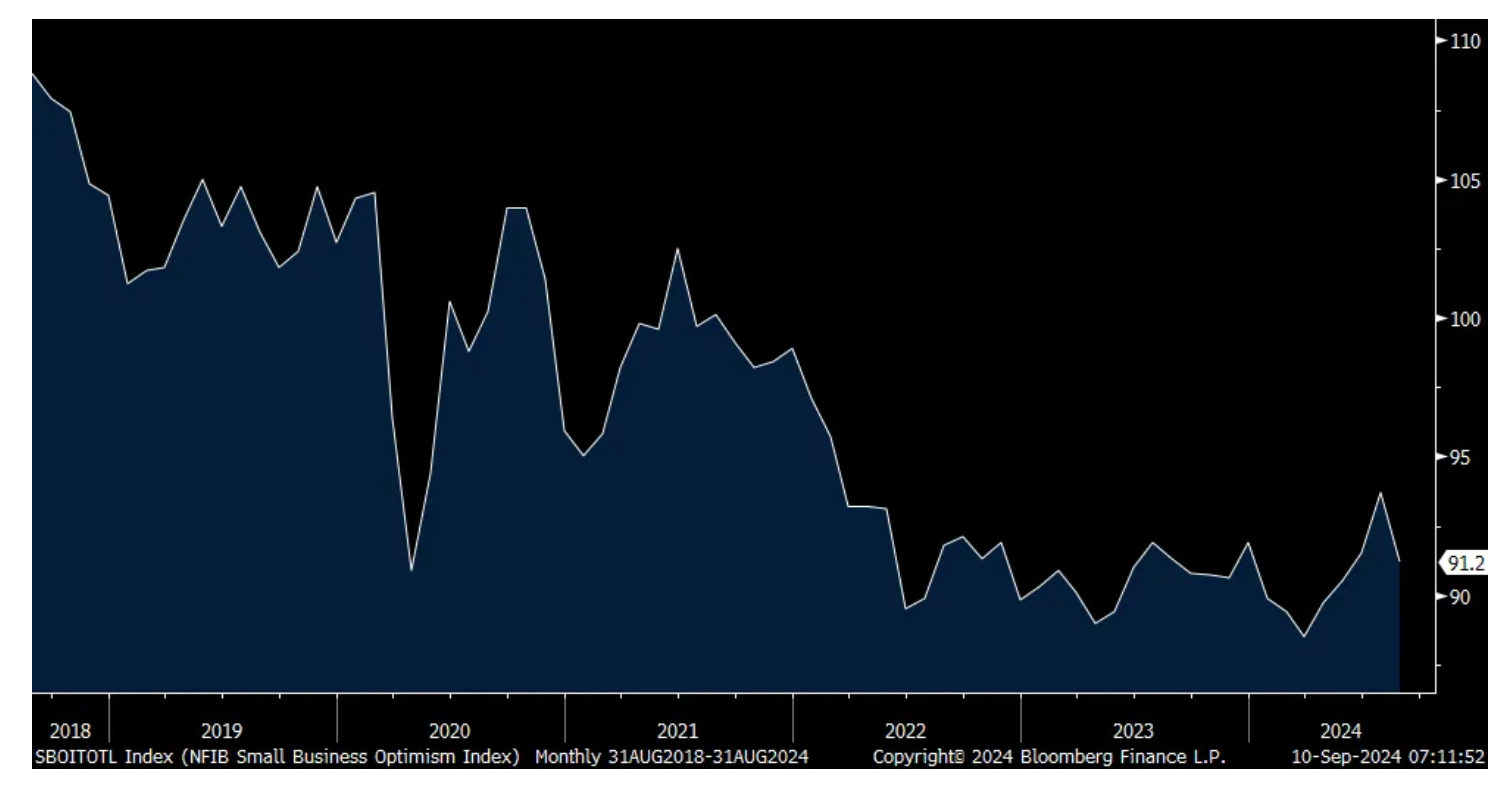

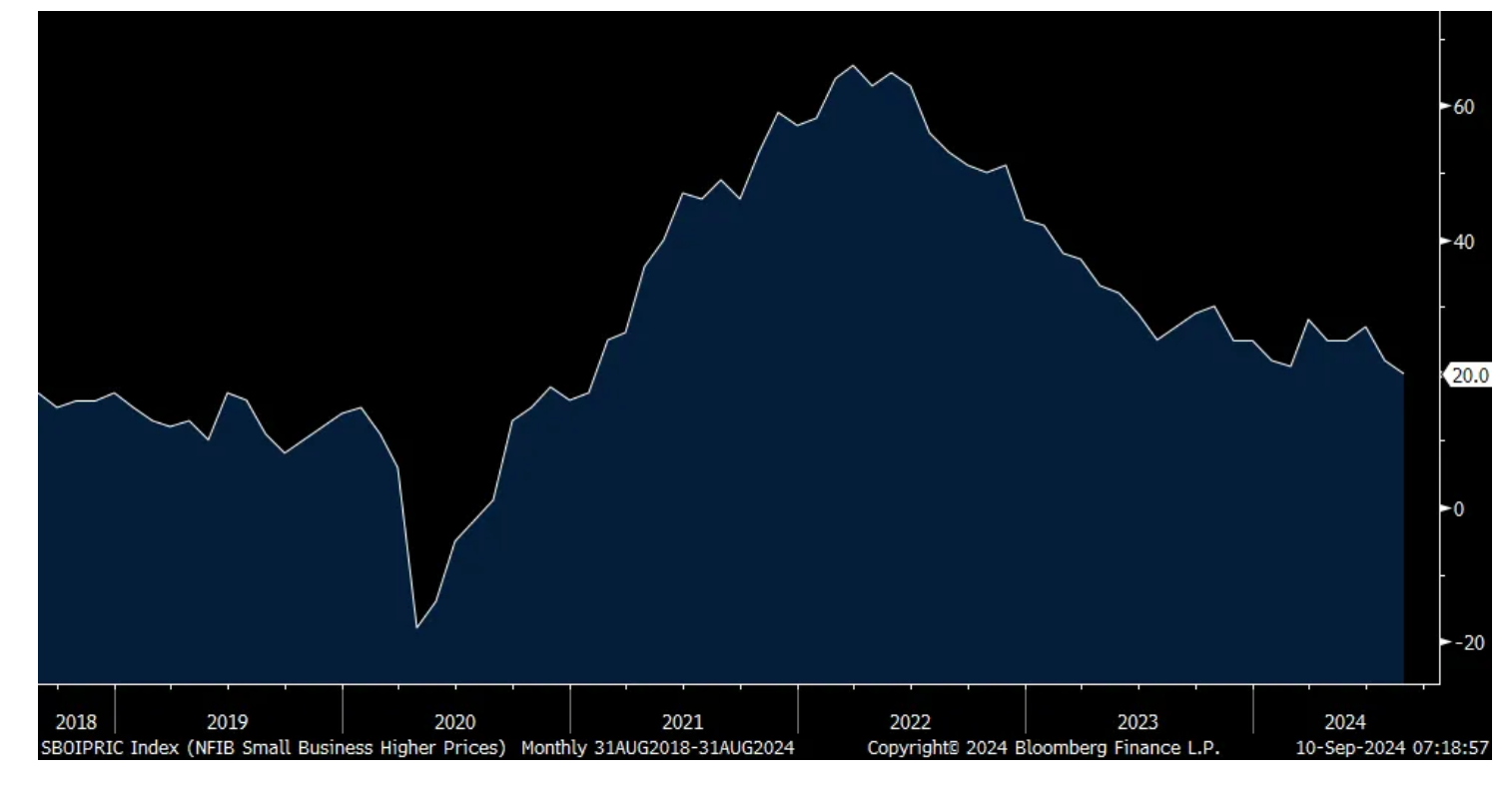

The August NFIB small business optimism index fell to 91.2 from 93.7. That is a three month low and still bouncing along the bottom of this cycle. Of particular note, and follows the small business job cut seen in the ADP report, Plan to Hire fell 2 pts to a 4 month low at 13%. Job Openings thought did tick up by 2 percentage points. Current comp was unchanged but rose 2 pts for future comp plans.

After improving by 18 pts in July, those that Expect a Better Economy weakened by 6 pts and those that Expect Higher Sales softened by 9 pts to -18%, matching the lowest since May 2023. Those that said it's a Good Time to Expand fell 1 pt.

Capital spending plans rose 1 pt to 24%, the highest this year but it was 28% in early 2020. And those that Plan to Increase Inventory fell 3 pts. Higher Selling Prices were down by 2 pts to the least since January 2021.

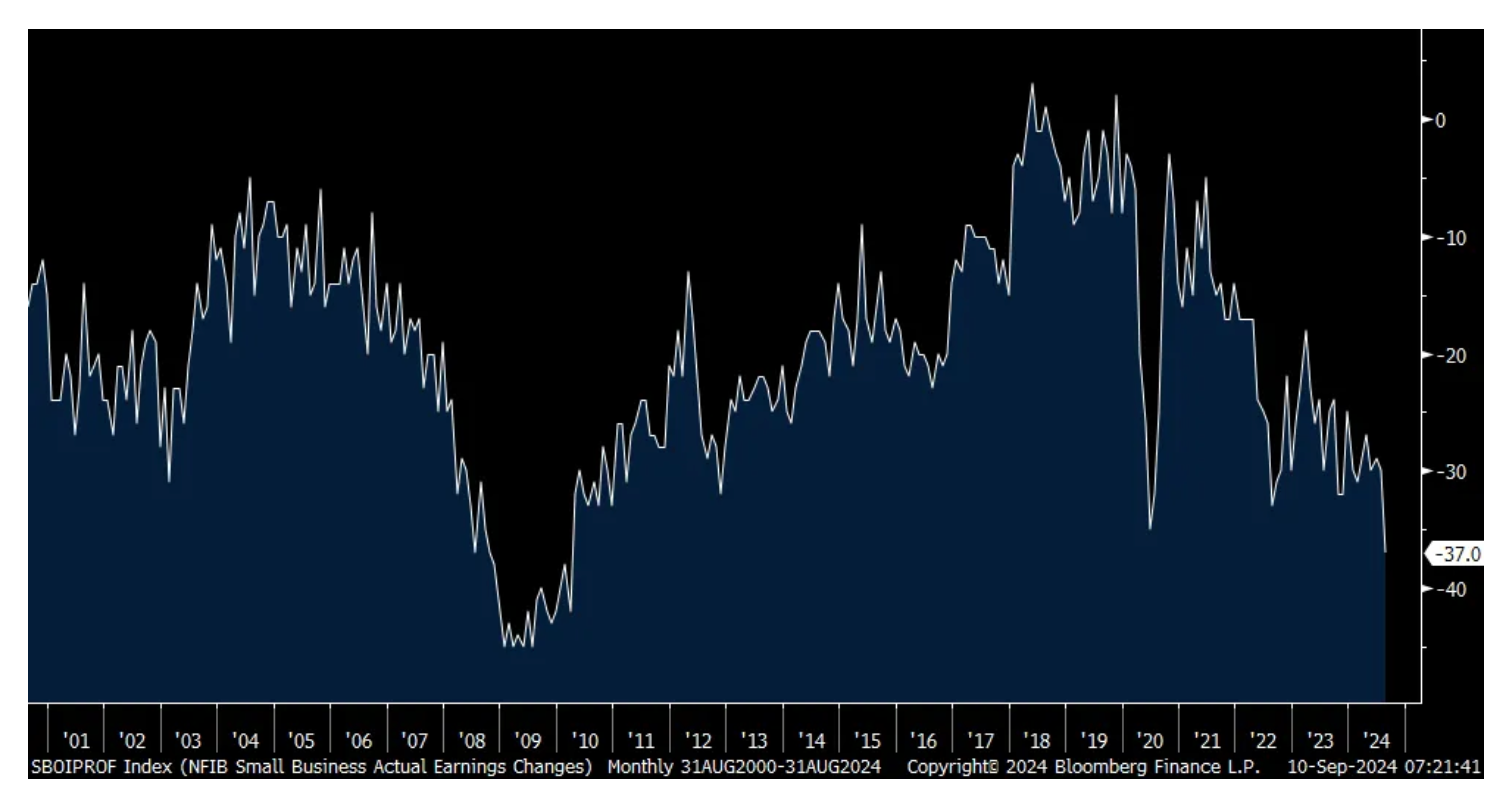

Lastly, 'Easing of Credit Conditions' weakened to the lowest in 4 months and the 'Positive Earnings Trends' fell 7 pts to -37%, the worst since March 2010. I bolded for emphasis. Specifically, 31% blamed weaker sales, 17% blamed the rise in the cost of materials, 13% cited labor costs and 10% blamed lower selling prices. The average rate paid on a loan rose to 9.5% from 9.4% and remains expensive.

The bottom line from the NFIB doesn't read well, "The mood on Main Street worsened in August, despite last month's gains. Historically high inflation remains the top issue for owners as sales expectations plummet and cost pressures increase. Uncertainty among small business owners continues to rise as expectations for future business conditions worsen."

NFIB

Higher Selling Prices

Positive Earnings Trend

China said its August exports rose by 8.7% y/o/y, above the estimate of 6.6%. It was led by autos and shipbuilding. While the US has essentially blocked Chinese EV's, they are selling them to the rest of the world, particularly Southeast Asia where they are affordable for those with much lower per capita incomes. Imports though were flattish, up .5% vs the estimate of up 2.5%. About 30% of China's imports eventually make their way into an export.

The UK reported a stronger than expected job gain for the 3 months ended July of 265k vs the estimate of 123k. The unemployment rate fell one tenth to 4.1%. But in August, payrolls fell by 59k vs the estimate of up 25k. Wage growth remained well above inflation at 5.1% y/o/y ex bonuses thru July, as expected, though down from 5.4% in June in part due to tough comps. After a spike in July which I can't explain of 102k, jobless claims in August grew by 23.7k. The mixed data has brought a modest response as gilt yields are up a touch, breakevens are down a touch and the pound is up a touch. The FTSE 100 is lower by .5%. I'm sure the BoE will follow the ECB with another rate cut soon.

BY Doug Kass · Sep 10, 2024, 10:30 AM EDT

I am pressing my JPM and XLF shorts.

BY Doug Kass · Sep 10, 2024, 10:15 AM EDT

I also made a mistake in covering my Goldman Sachs GS short last week.

BY Doug Kass · Sep 10, 2024, 10:06 AM EDT

BY Doug Kass · Sep 10, 2024, 9:45 AM EDT

Apple Intelligence capabilities demo 'somewhat underwhelming,' says Bernstein Bernstein analyst Toni Sacconaghi says Apple's new hardware product announcements were largely in line with expectations, and more evolutionary than revolutionary. Further, the firm sees the demo of and timeline for Apple Intelligence capabilities as "somewhat underwhelming." While Bernstein expects Apple to aggressively market AI functionality, it sees the possibility that consumer upgrades could be pushed out until later this year/ iPhone 17, given the slow AI rollout. Contrary to expectations, Apple essentially retained prices on all iPhones in the U.S. and internationally, though the dollar has weakened year over year vs. most currencies, providing a modest tailwind, all else equal, the firm adds. Bernstein has an Outperform rating on the shares with a price target of $240.

Apple iPhone 16 launch event as-expected, says Morgan Stanley Morgan Stanley says there were "no major surprises" at yesterday's "It's Glowtime" event, which included new details on the Apple Intelligence rollout, a new Visual Intelligence feature, and iPhone pricing being "the most important incremental announcements." Attention will now turn to iPhone preorder and lead time data this Friday, notes the analyst, who says Apple remains a Top Pick with an Overweight rating and $273 price target.

Apple updates for iPhone 16 in line with expectations, says Citi Citi says Apple yesterday introduced the new iPhone 16 family, Apple Watch Series 10 and AirPods 4, among other product updates. Overall, the hardware updates for the iPhone 16 family are in line with expectations, including new designs, upgraded processors, upgraded cameras, longer battery life, improved audio, and a new Camera Control, the analyst tells investors in a research note. The firm notes that Apple kept the pricing the same as prior models. Citi thinks Apple is "making a clearer and stronger case" around Apple Intelligence that is focused on personal intelligence. It remains positive on the iPhone refresh next year with a gradual rollout of the AI features across the globe. The firm keeps a Buy rating on Apple shares.

Unchanged pricing may help Apple sell more phones, get more upgrades, says BofA BofA notes that Apple's iPhone pricing remained unchanged for its newest models, which may help Apple sell more phones and also help in getting more users to upgrade in order to take advantage of Apple Intelligence. The firm, which models 224M iPhones for FY24, 241M units or up 8% year-over-year for FY25, and 257M units or up 7% year-over-year for FY26, maintains a Buy rating and $256 price target on Apple after the company unveiled its new iPhone line-up as well as Apple Watch Ultra 2, refreshed Airpods and other refreshed products at yesterday's launch event.

BY Doug Kass · Sep 10, 2024, 9:35 AM EDT

-AVO +18% (earnings, outlook)

-VRDN +17% (announces Positive Topline Results from Veligrotug (VRDN-001) Phase 3 THRIVE Clinical Trial in Patients with Active Thyroid Eye Disease)

-MTRX +12% (earnings, guidance)

-CNTA +11% (plans to rapidly advance ORX750 into Phase 2 studies in patients with narcolepsy type 1 (NT1), narcolepsy type 2 (NT2), and idiopathic hypersomnia (IH) beginning in 4Q24; announces Positive Interim Phase 1 Clinical Data with Novel Orexin Receptor 2 (OX2R) Agonist, ORX750, in Acutely Sleep-Deprived Healthy Volunteers)

-NNE +8.9% (selected for inclusion into the broad-market Russell 3000, effective Sept 23rd)

-ORCL +8.3% (earnings, guidance; acquires Accelalpha with no terms disclosed)

-CGNT +8.2% (earnings, guidance)

-BOOT +7.7% (reports prelim Q2 SSS)

-CVGW +7.3% (earnings)

-KGS +5.8% (prices ~6.1M shares at $25.00/shr by selling holder)

-CDMO +2.8% (earnings, guidance)

-WFC +2.8% (guidance from Barclay’s conference)

-AMSC +2.7% (adjusts Rev guidance to reflect the recently announced acquisition of NWL)

-BABA +2.7% (set to make its debut on Shenzhen/HK Stock Connect today)

-POET +2.7% (selected by Mentech to supply engines for 800G and 1.6T optical modules, terms not disclosed)

-BHIL +2.6% (signs Letter of Intent with Argonautic for acquisition of Company)

-IONS -7.5% (prices 11.5M shares at $43.50/shr)

-AU -6.2% (Centamin plc receives takeover offer from Anglogold Ashanti at equivalent of 163p, in $2.5B share and cash deal)

-RBRK -5.5% (earnings, guidance)

-HPE -5.2% (files to sell $1.35B Proposed Public Offering of Mandatory Convertible Preferred Stock)

-STEP -4.4% (prices shares ~4.0M shares at $50/share)

-NBTB -2.9% (NBT Bancorp announces merger with Evans Bancorp in an all stock deal)

-VIK -2.9% (Holders file to sell 30M shares in secondary offering)

-ASO -2.7% (earnings, guidance)

-SEG -2.7% (to distribute to holders right to purchase up to 7M of common shares at $25/shr)

-LMNR -2.3% (earnings, guidance)

BY Doug Kass · Sep 10, 2024, 9:15 AM EDT

As of of 8:14 a.m.:

BY Doug Kass · Sep 10, 2024, 9:10 AM EDT

As of 8:31 a.m.:

BY Doug Kass · Sep 10, 2024, 9:02 AM EDT

* Yesterday Sandy Koufax, known as "The Left Arm of God", celebrated the 59th anniversary of his perfect game (Thanks to Sarge for his baseball trivia quiz which reminded us all of Sandy's nickname)

Yesterday was the 59th anniversary of my cousin, Sandy Koufax's perfect game.

Here is the historic call by Dodgers announcer Vin Scully of the bottom of the ninth inning of that game: CHC@LAD: Koufax's perfect game called by Scully (youtube.com)

It is a gem.

Here is a several-year-old Diary article I wrote about my cousin which I wanted to repost on the anniversary of Sandy's accomplishment:

Happy Birthday, Cuz!

* May you stay forever young

* They don't make pitchers like Sandy anymore and they don't make markets the same way they did either

May God bless and keep you always

May your wishes all come true

May you always do for others

And let others do for you

May you build a ladder to the stars

And climb on every rung

May you stay forever young

May you stay forever young

- Bob Dylan, Forever Young

On this day in 1935, my cousin Sandy Koufax was born.

What a delivery he had!

If I could only pick stocks the way he threw strikes!

Sandy is 87 years old today, and that makes me feel old!

In honor of his birthday I wanted to post this five year old column I wrote about investing and baseball... and Sandy:

Nov 01, 2017 ' 12:57 PM EDT DOUG KASS

"Its a beautiful day.

Lets play two!"

-- Ernie Banks (Chicago Cubs)

Tonite Dodgers Stadium will host the seventh game of the World Series for the first time ever.

Being related to Hall of Famer, Sandy Koufax, I bleed Dodger Blue.

I can't wait for tonite's game.

Over the last two decades I have written more than 50 columns noting the parallels between baseball and investing.

* Playng Ball With Warren Buffett

* Rounding Third and Heading Home

* Forget Stocks Its Opening Day

* How Long Will The Joy In Mudville Last?

* Never Fear Getting Back in the Game

* Take Me Out to the Ball Game For a Sense of History

Here is one of my favorites from more than two years ago:

SEP 9, 2015 2:34 PM EDT

"We live in a dystopian investment world whose markets -- currencies, commodities, stocks and bonds -- have morphed into an Orwellian backdrop of omnipresent government intervention and manipulation that is increasingly dictated by the quant community. (Who worship at the altar of prices and price momentum and are agnostic on values.)... In recalling this past week's action, it should be clear to most that the market mechanism is broken.

-- Doug's Daily Diary, Is 2015 Really 1984? (Aug. 28)

As I wrote in this morning's opening missive, "A Picture of Imperfection," the market's mechanism is broken.

The collateral damage ... that has come out of a broken market dominated by quants makes both trading and fundamental investing difficult in a market that has morphed into one without memory from day to day. Moreover, "artificial" and deep gaps or advances in prices -- another outgrowth of quants' dominance in daily trading activity -- also render technical analysis less useful.

Over the past 16 years, I have made clear my passion for the game (and purity) of baseball and the investment lessons I have gleaned from the sport.

Two years ago, in "Defense Drill," I pointed out that it's not your batting average that matters in investing and trading, it's your defense that counts. Back in 2012, in "America's Pastime Applies to Markets," I recalled that I have learned over my career that (baseball) history is instructive for investors. And back in the summer of 2007 -- just before all hell was about to break loose -- I penned a column titled "Take Me Out to the Ball Game for a Sense of History":

But, tonight, September the 9th of Nineteen Hundred and Sixty Five, Sandy made the toughest walk of his life I am sure because through eight innings he has pitched a perfect game. He has struck out 11 and he has retired 24 consecutive hitters.

You can almost taste the pressure now... Krug must feel it too.

There are 29,000 people in the ballpark and a million butterflies.

I would think that the mound at Dodger Stadium is now the loneliest place in the world.

A lot of people in the ballpark now are starting to see the pitches with their hearts.

He is one out away from the promised land.

You can't blame a man for pushing so hard.

On the scoreboard in right field it is now 9:46 p.m. in the City of the Angels, Los Angeles, California.

A crowd of 29,139 just sitting in to see the only pitcher in baseball history to hurl four no-hit, no-run games. He has done it four straight years. And now he has capped it with a perfect game.

Sandy Koufax, his name will always remind you of strikeouts. He did it with a flourish. He struck out the last six hitters. And when we write his name in the record books, the "K" will stand out more than "O-U-F-A-X."

-- Vin Scully, calling the last inning of Sandy Koufax's perfect game 50 years ago

In marked contrast to the markets' imperfection, perfection was found on a baseball diamond in Los Angeles as 50 years ago today my cousin Sandy Koufax pitched a perfect game against the Chicago Cubs. The Cubs pitcher, Bob Hendley, threw a one-hitter -- making the game, arguably, the greatest pitching duel in history.

As a teenager, I listened to the game with a small transistor radio. I moved the radio around my bedroom in Long Island to get the best reception possible.

But, through the beauty of YouTube, you can listen with clarity to the last inning's broadcast by legendary Dodger announcer Vin Scully.

And here is the box score of the game.

They don't make pitchers like Sandy anymore and they don't make markets the same way they did either ("in the good old days").

Call me old-fashioned, but in Season of the Glitch, I outlined why more volatility will emerge from our broken markets and in the past I have been adamant in my view that we should KILL THE QUANTS BEFORE THEY KILL OUR MARKETS.

There have been a number of factors that have conspired over the last decade to produce the current environment, which resembles less of a stock market than a casino -- providing fertile ground for the disruptive influences of quants, risk parity and other strategies that pay little heed to balance sheets and income statements:

-- Regulation: Volcker Rule, Basel III, Dodd Frank prevented dealers from providing their classical role of ensuring market liquidity and stability -- in part because of lowered allowable leverage and, in part, because of a mandated reduction in proprietary trading activities.

-- The elimination of the uptick rule in 2008: This will go down as one of the dumbest regulatory moves ever.

-- The proliferation and popularity of ETFs: These weapons of financial destruction(which rebalance during the day) have taken a much larger share of trading activity as retail investors have moved away from individual stock picking and toward the use of "these baskets." (As evidence, a disproportionate amount of stock trading activity occurs in the first 30 minutes and last 30 minutes of daily trading, when ETFs "rebalance.")

-- The decline in retail investor involvement

-- The electronization of the NYSE: This has eliminated the stabilizing impact of market makers and specialists. In the past, human beings have used common sense, today emotionless machines rule the day and have recently proven disruptive to our market system.

-- The steady drop in commission rates, which gave brokerages less incentive to take the other side of a trade.

There are some easy near-term solutions to the adverse impact of our Brave New Market -- including the adoption of a tax on financial (stock) transactions and/or the reimposition of the uptick rule.

Unfortunately, the SEC is asleep at the switch and, for now, we have to play the hand we have been dealt.

So, get used to spending more time in a trading mode and less time in an investing mode -- and given the rise in volatility, keep an eye on your portfolio's value at risk (VAR).

My cousin Sandy Koufax controlled his destiny with his golden left arm.

However, to an important degree, we -- as market participants -- have lost control of our markets and our investment destinies.

It's a sad state of affairs that is not likely to be resolved any time soon.

Position: None

By Doug Kass Dec 30, 2022 12:12 PM EST

BY Doug Kass · Sep 10, 2024, 8:30 AM EDT

BY Doug Kass · Sep 10, 2024, 8:20 AM EDT

From my pal Danielle DiMartino Booth:

BY Doug Kass · Sep 10, 2024, 8:00 AM EDT

Despite the current trend towards lower mortgage rates I expect housing (activity and prices) to begin to contract:

BY Doug Kass · Sep 10, 2024, 7:50 AM EDT

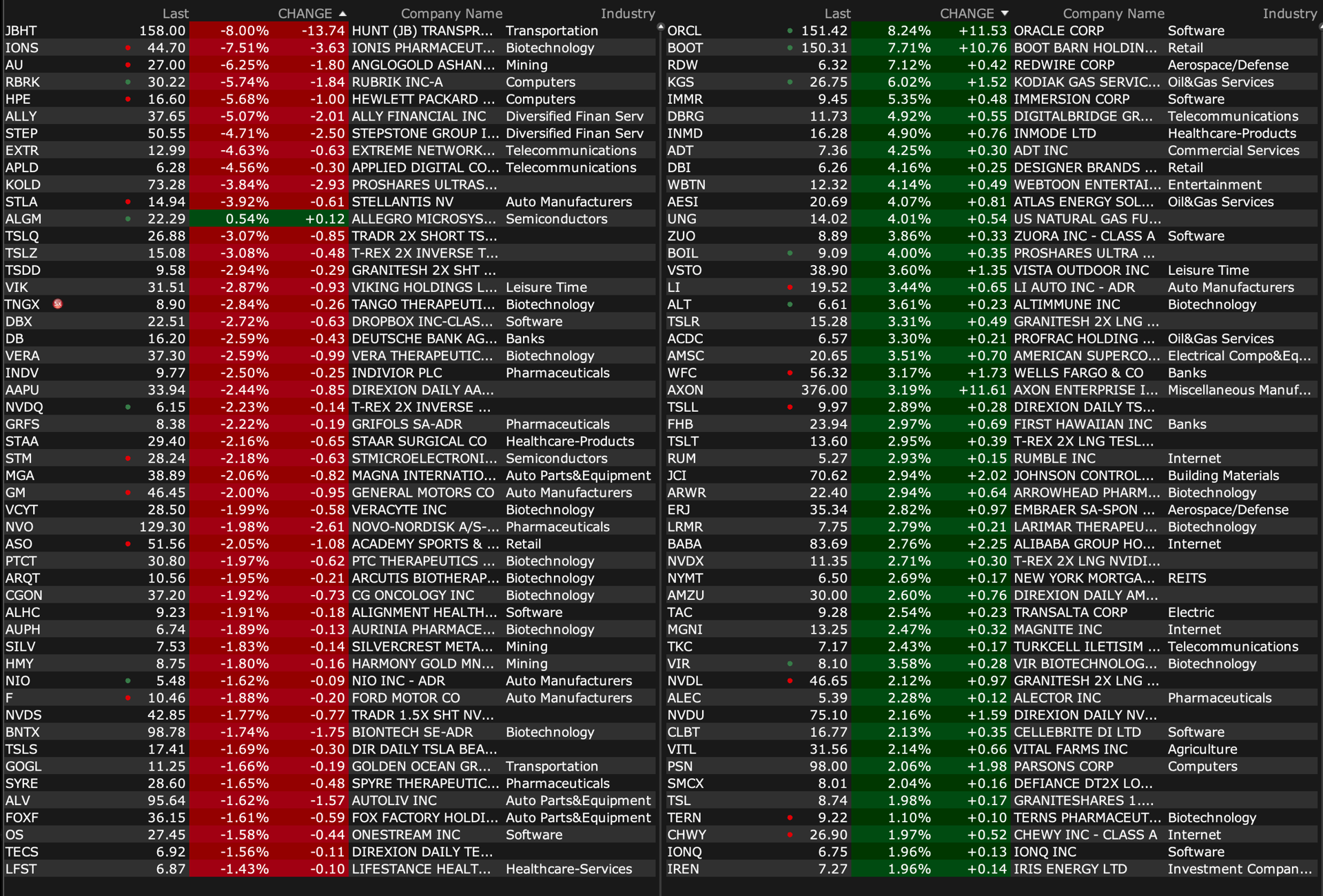

On bullish sentiment:

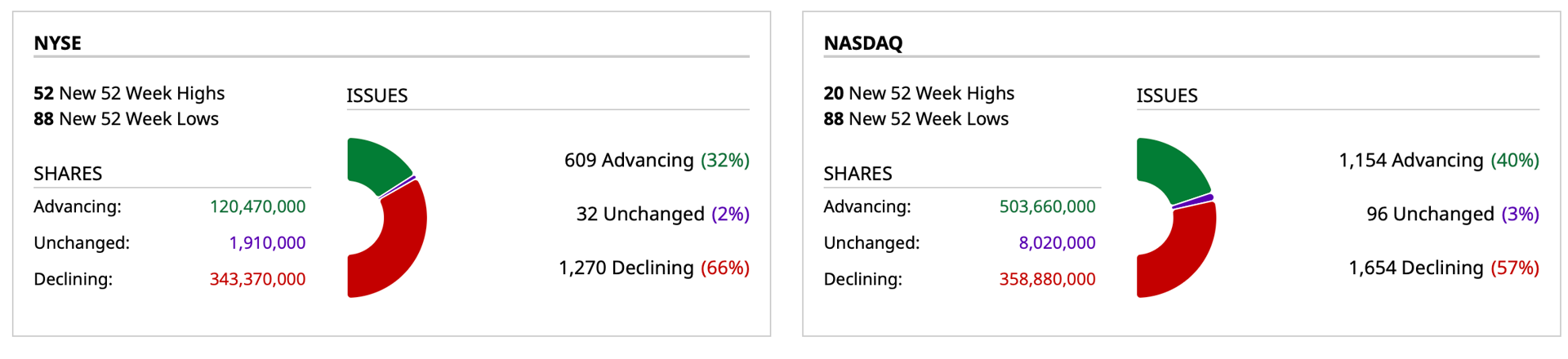

BY Doug Kass · Sep 10, 2024, 7:40 AM EDT

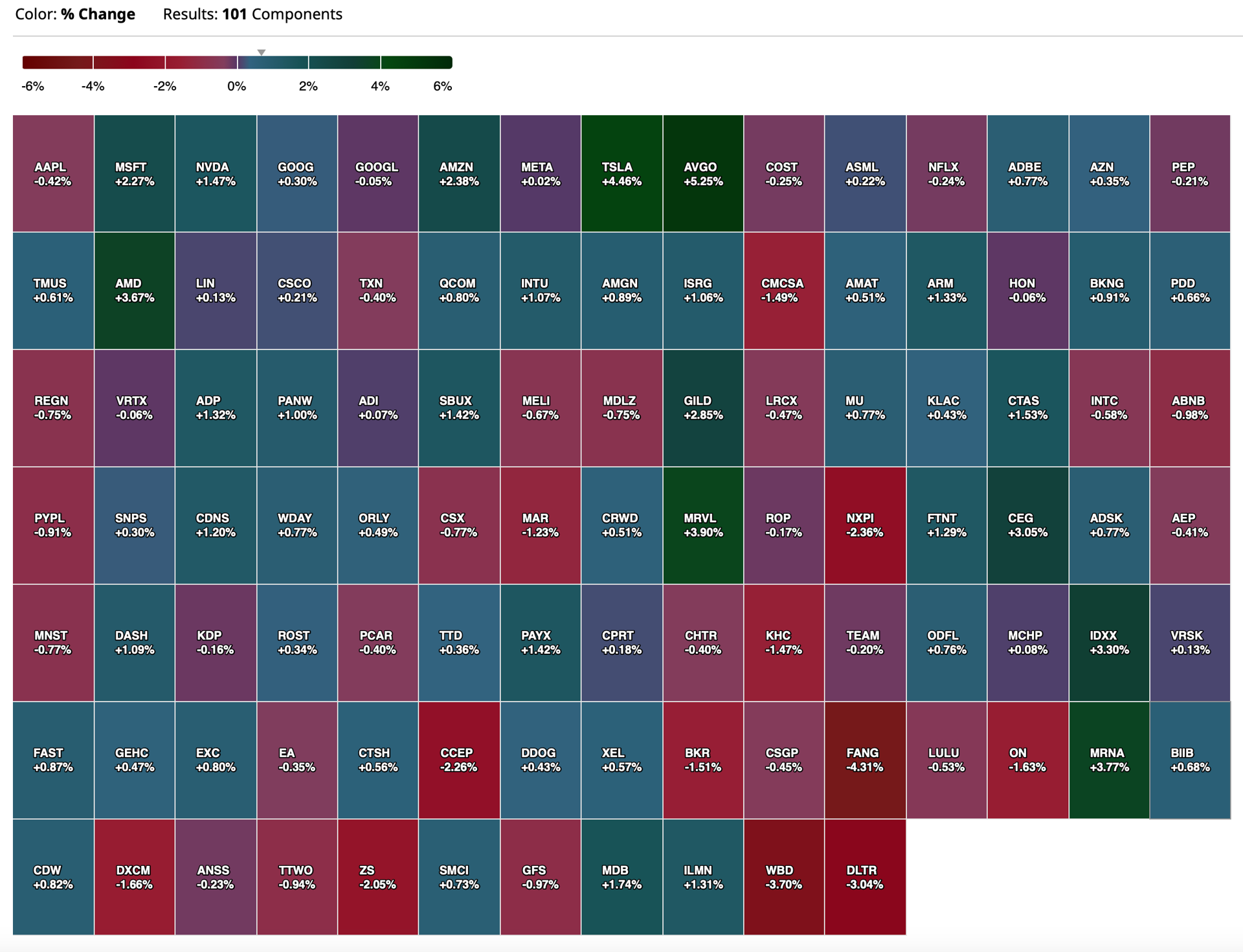

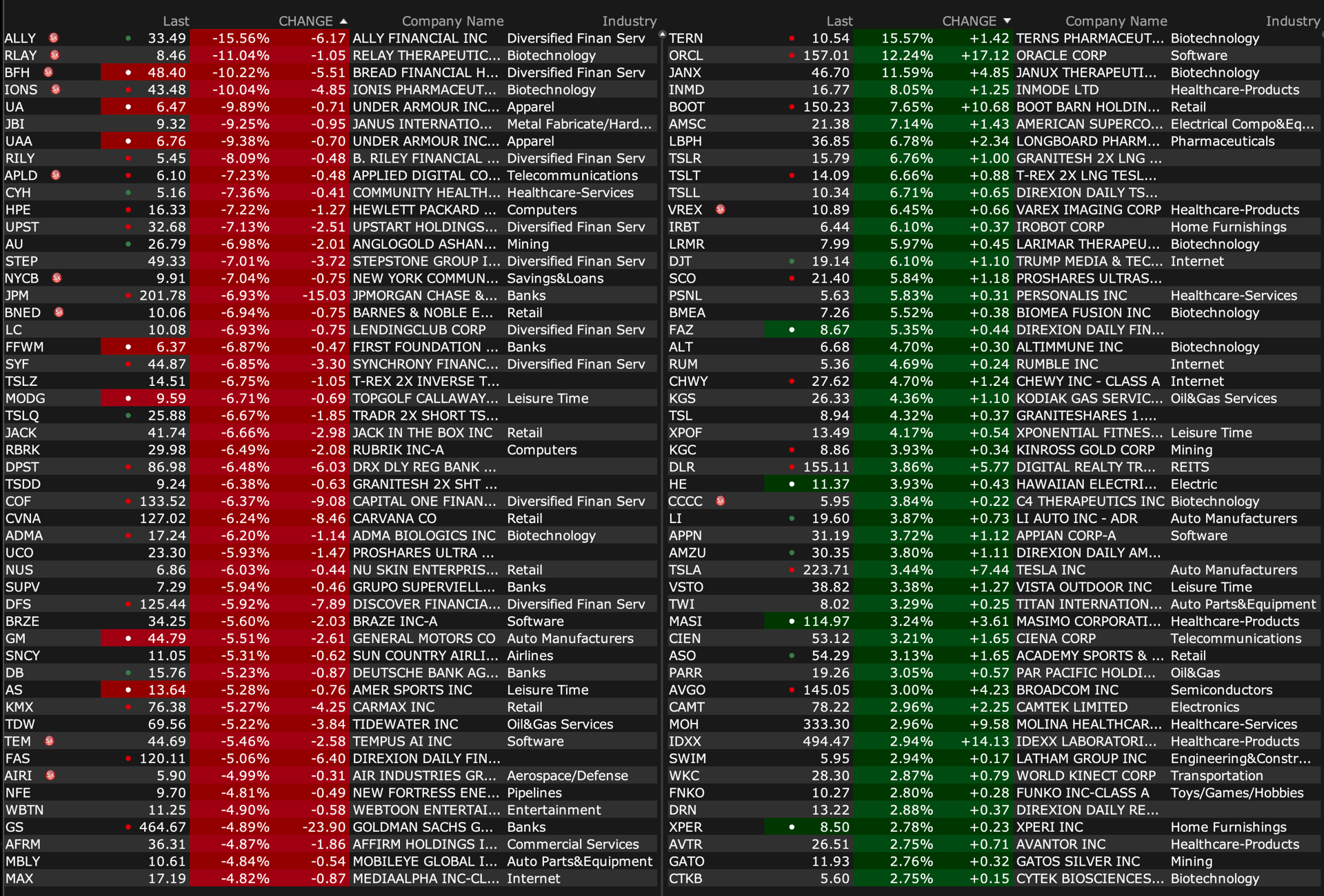

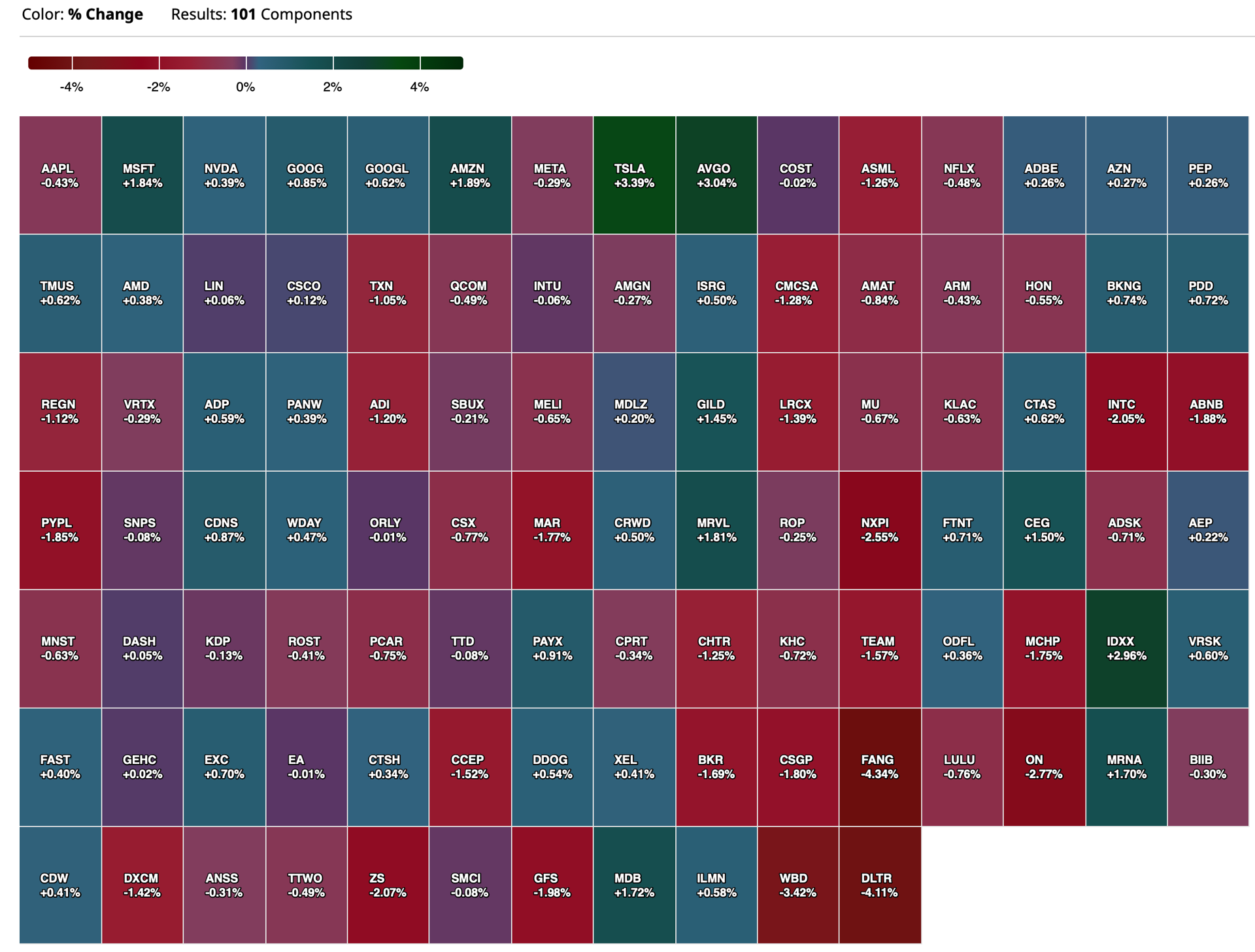

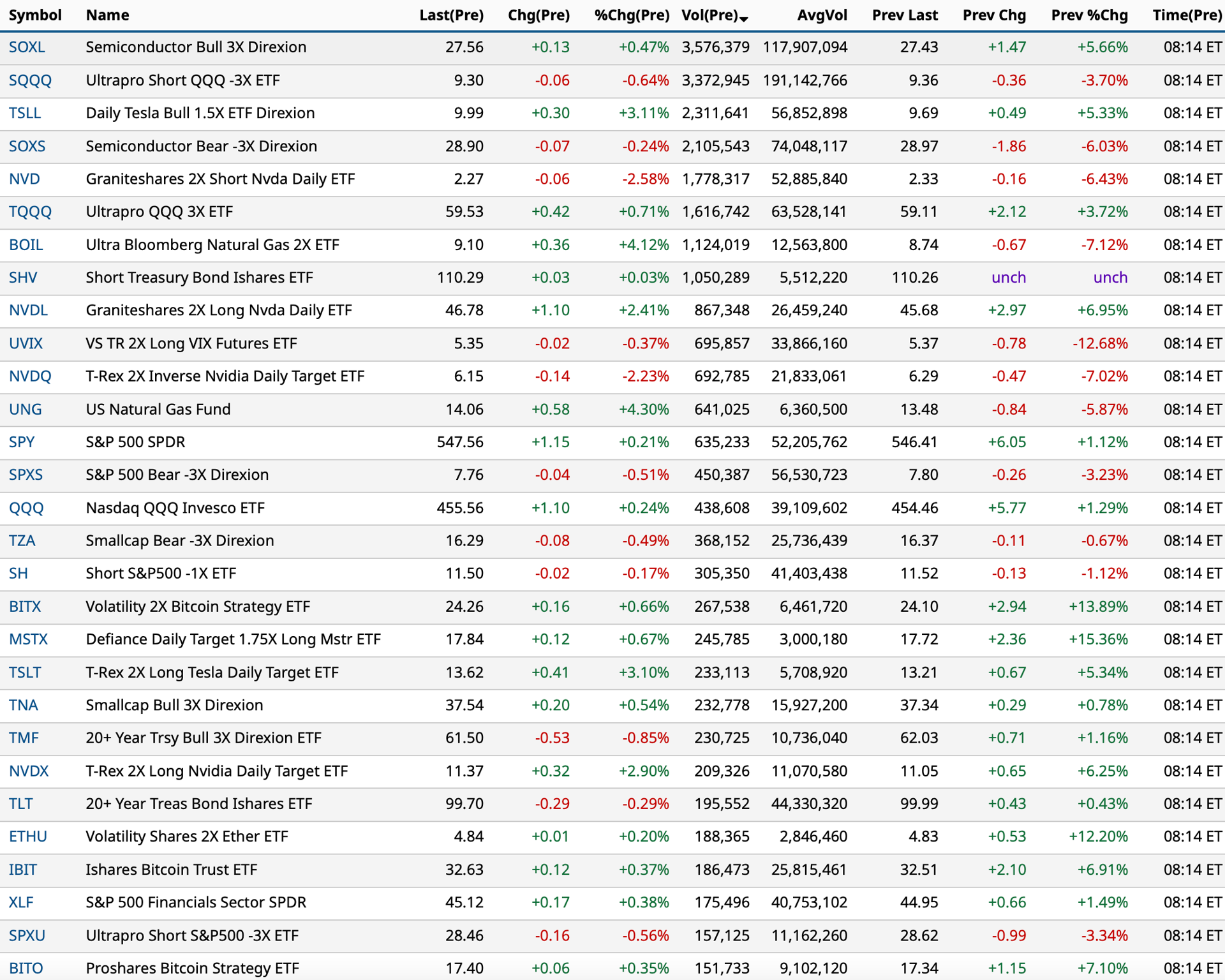

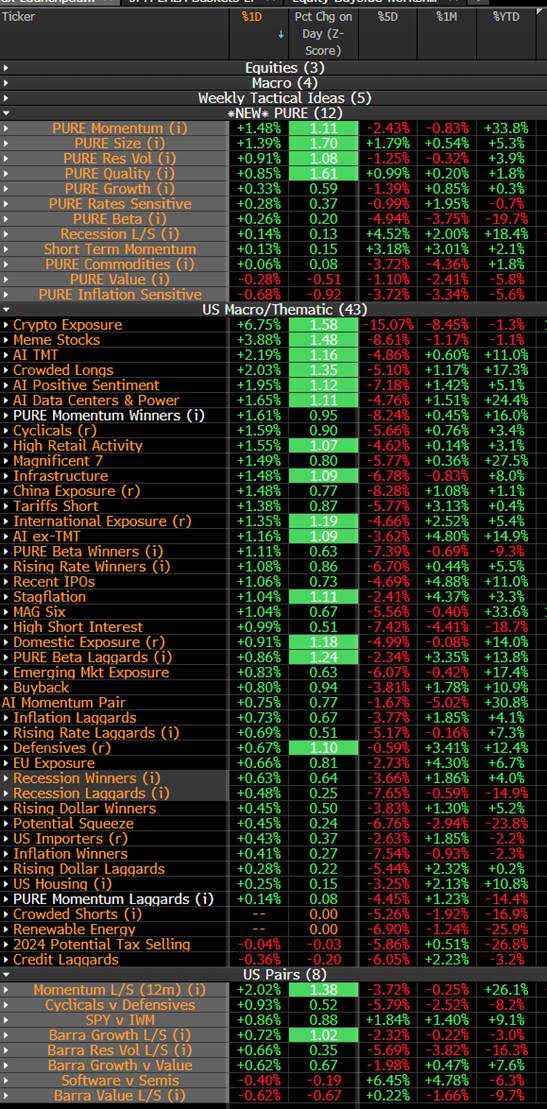

This table is a valuable resource for momentum-based short-term traders:

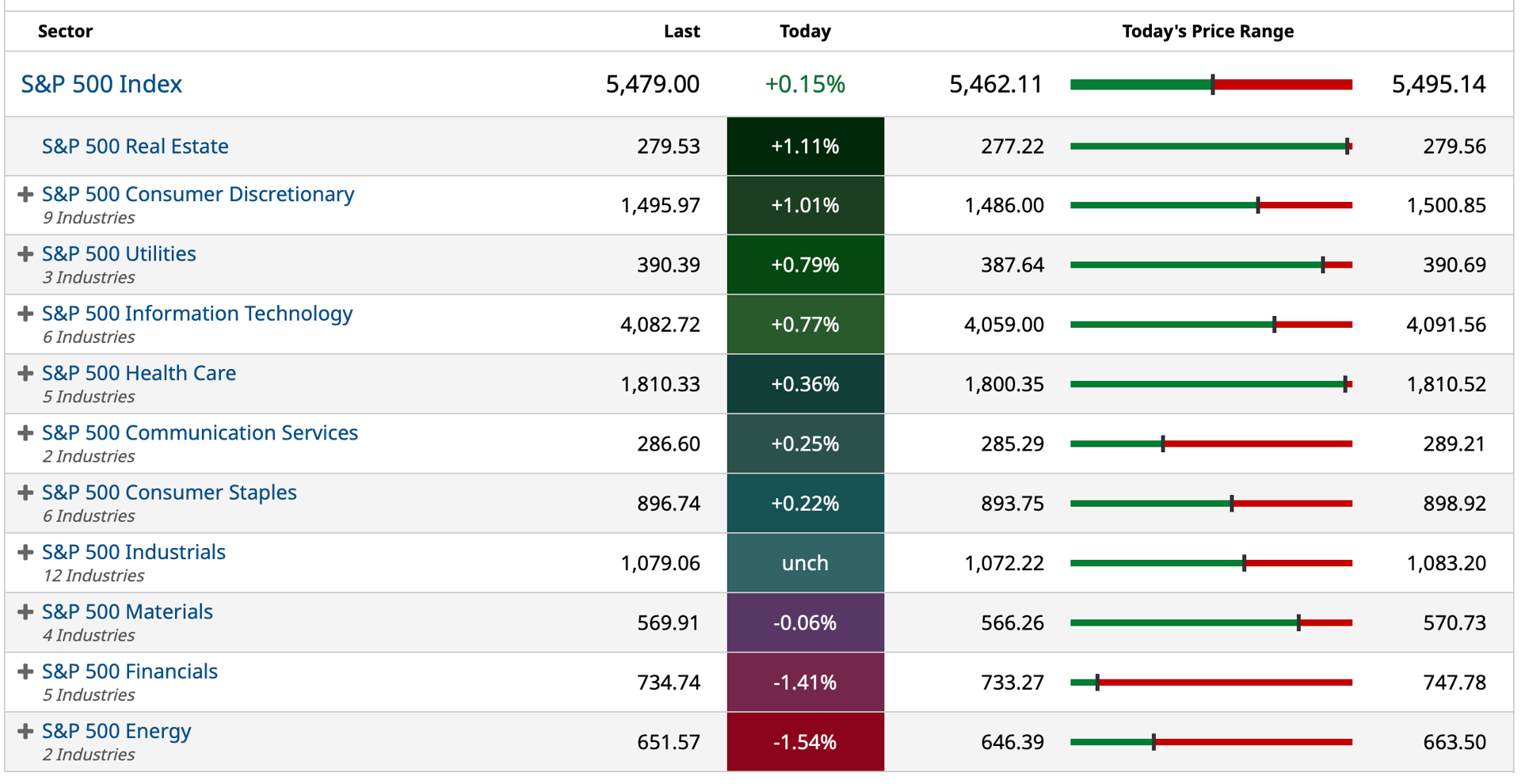

BY Doug Kass · Sep 10, 2024, 7:30 AM EDT

From JPMorgan:

US: Futs are lower but have bounced off their overnight lows; pre-mkt Mag7 and Semis are weaker and Financials higher following an industry conference and lower capital requirements. Bond yields are higher by 1-2 bps while the USD is flat. Cmdtys mixed with Metals up, Energy down, and Ags mixed. The macro data focus is on the Small Biz Optimism print and the Presidential Debate.

and...

EQUITY AND MACRO NARRATIVE: As investors weigh whether last week was the worst of the current downdraft, this week is important for removing uncertainty surrounding the Fed and the US Election, so tonight’s debate sets up as an important data print. CPI/PPI this week are expected to show another step-down in inflation and recent China weak macro data will likely continue to pull PPI lower. Recent weakness in oil/gasoline may aid Consumer Sentiment, where we receive an update on Friday. I think the bigger catalyst for shaping the narrative comes next week with Retail Sales to either assuage or fuel growth concerns.

BY Doug Kass · Sep 10, 2024, 7:20 AM EDT

*Like Amazon...

It is always a function of entry points and timeframes:

BY Doug Kass · Sep 10, 2024, 7:10 AM EDT

I made a mistake in covering my Apple AAPL short.

End of message.

BY Doug Kass · Sep 10, 2024, 6:40 AM EDT

After the close it was announced that the banking industry would be subject to less stringent capital rules. Biggest US Banks’ Capital Hike Chopped in Half in Latest Plan by Regulators - Bloomberg.

This should come as no surprise as about a halving in the increase of capital requirements (from the previous proposal of +19% to +9%) was assumed by most. Feds to unveil lightened bank-capital requirements in coming days, report says - MarketWatch

Also after the close, Goldman Sachs GS reported weak trading activity and results (its shares retreated in the after market).

I am back shorting JPMorgan Chase JPM ($220.25 at around 7 p.m. last night, on a small gap higher) and American Express AXP (during the trading session).

I plan to re-short Goldman Sachs and add to my XLF short as, it is my view that this is the wrong time in the economic and bank profit cycle to own financials. As well, valuations are rich — both absolutely and relative to the broader market.

BY Doug Kass · Sep 10, 2024, 6:30 AM EDT

BY Doug Kass · Sep 10, 2024, 6:15 AM EDT

BY Doug Kass · Sep 10, 2024, 6:08 AM EDT

Doomberg on "the imminent end of the British steel industry."

BY Doug Kass · Sep 10, 2024, 5:57 AM EDT

The S&P Short Range Oscillator is back in negative territory at -0.42% (that's moderately oversold).

That compares to Friday night's 0.91% (modestly overbought).

BY Doug Kass · Sep 10, 2024, 5:45 AM EDT