Howling About Car Prices

Wolf Street on rising used and new car prices.

BY Doug Kass · Aug 7, 2024, 5:16 PM EDT

Wolf Street on rising used and new car prices.

BY Doug Kass · Aug 7, 2024, 5:16 PM EDT

Occidental Petroleum OXY beats on the top and bottom line.

Here is the earnings release and conference call slides.

BY Doug Kass · Aug 7, 2024, 4:49 PM EDT

As of 4:29 p.m.:

BY Doug Kass · Aug 7, 2024, 4:41 PM EDT

I will be busy after the close in digesting the EPS reports.

So back at five-ish.

BY Doug Kass · Aug 7, 2024, 3:55 PM EDT

I'm long ARM, NVDA and GOOGL.

BY Doug Kass · Aug 7, 2024, 3:10 PM EDT

I'm long Amazon AMZN at $162.01.

BY Doug Kass · Aug 7, 2024, 3:06 PM EDT

Adding to SPY at $519.20 and QQQ at $436.20

BY Doug Kass · Aug 7, 2024, 2:57 PM EDT

* For a long rental...

Long SPY at $519.85 and QQQ at $436.45.

BY Doug Kass · Aug 7, 2024, 2:47 PM EDT

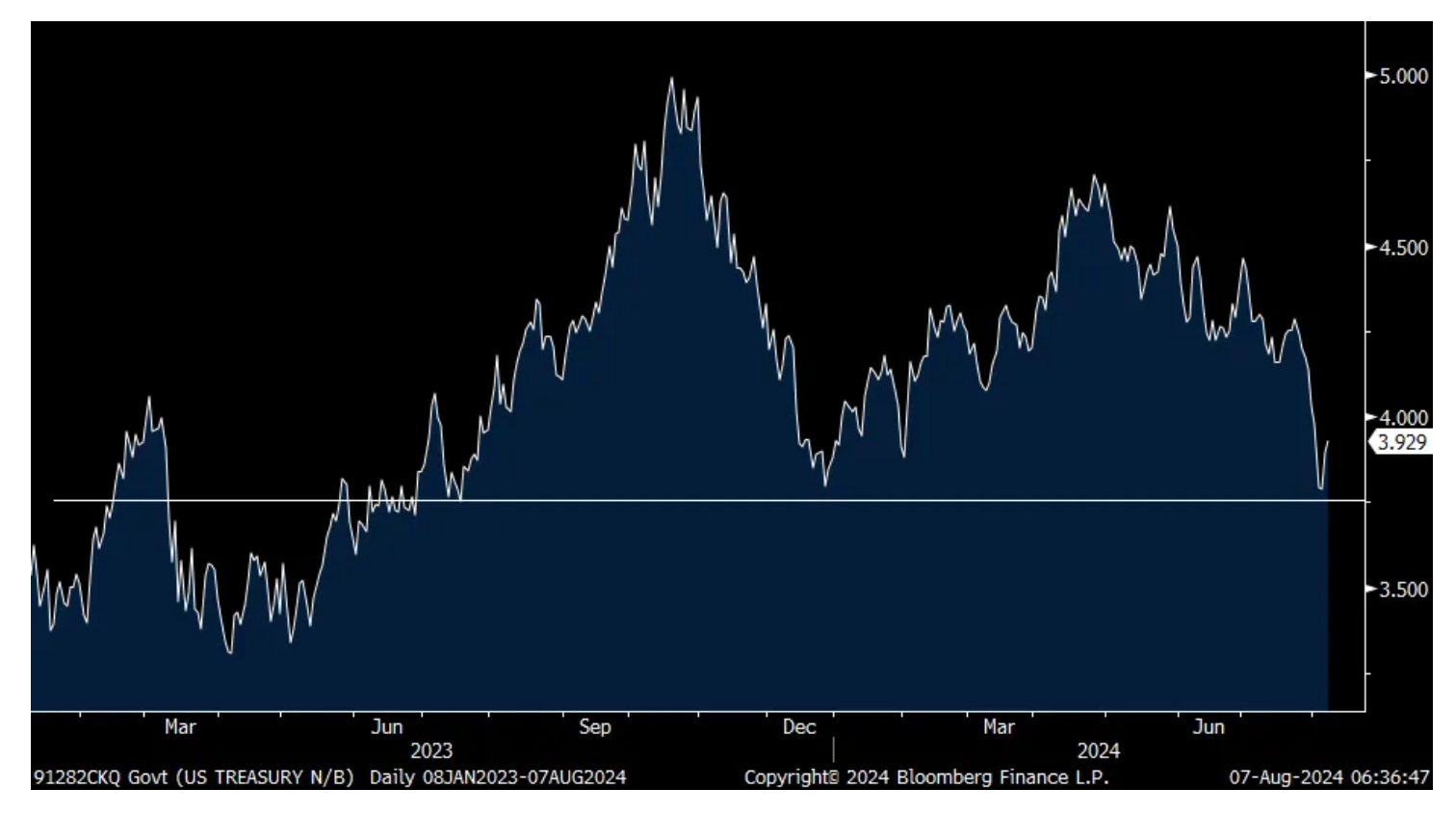

From Peter Boockvar:

Terrible 10 yr auction

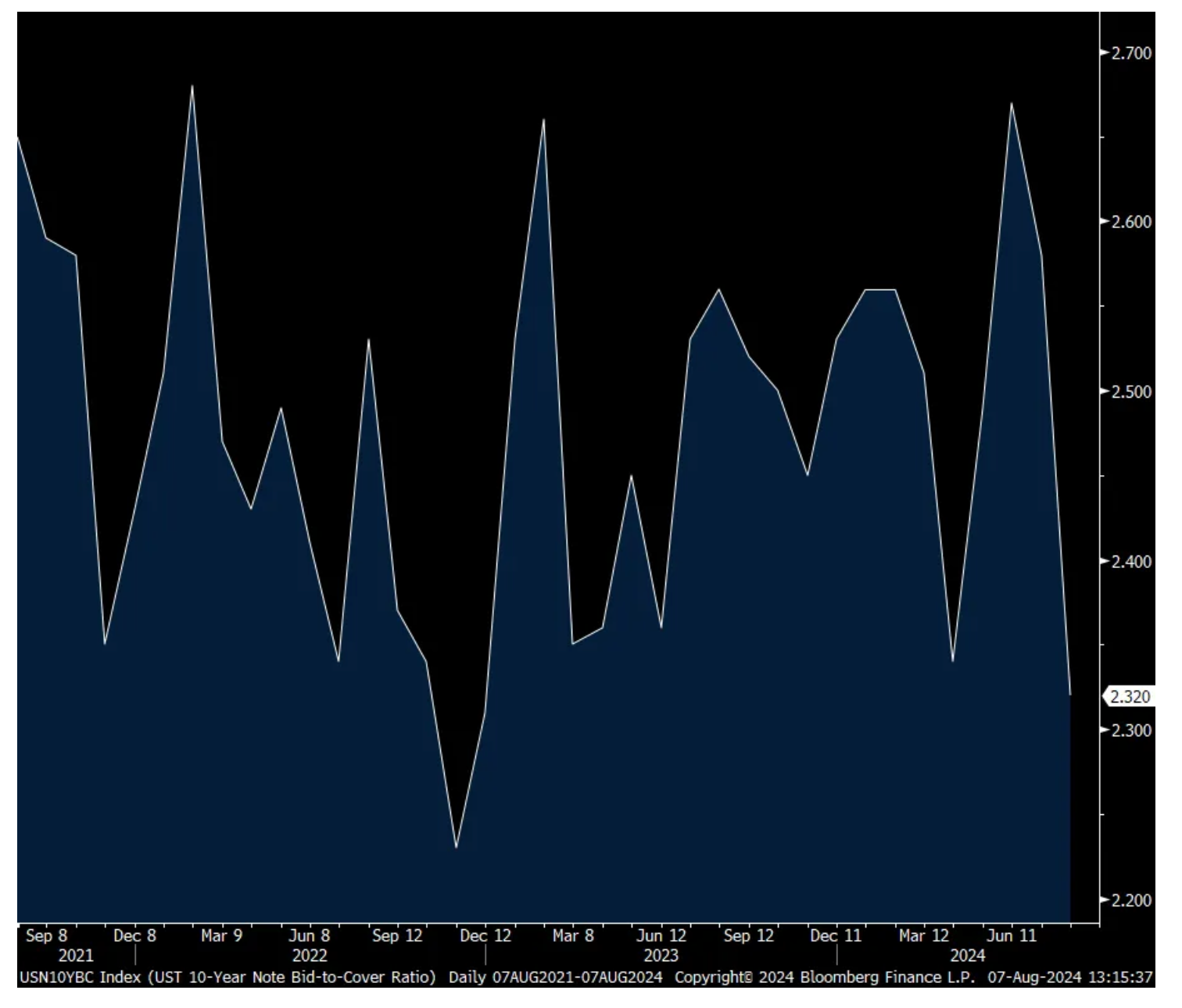

We’ve had a crazy few trading days (though was building up over the past 3 weeks), growing worries over economic growth, wild FX moves and a 10 yr yield that touched 3.66% early Monday morning and was at 3.93% just before the 10 yr auction. One would have thought that the 10 yr note auction today would do just fine with that backdrop but no, the auction was terrible.

The yield of 3.96% was well above the when issued of 3.93%. The bid to cover of 2.32 was well below the one yr average of 2.52 and the weakest since December 2022. And dealers were left with 82% of the auction, the 2nd highest since last October.

There is the simple trade of buying duration when inflation moderates and worries grow that the economy will slow but maybe it’s just not that easy. Maybe these wild FX moves are dissuading foreigners from buying US Treasuries? Maybe debts and deficits really do matter this time and if the economy rolls over and the unemployment rate rises, the US government will collect less in tax receipts and that $2 trillion deficit becomes $3 trillion and that 6% budget deficit as a % of GDP will be 10%. That would entail a lot more supply? Maybe the Fed is not going to cut 50 bps in September as they have more faith in the US economy?

I believe that 3.66% Monday morning yield will stick for a while as the low and I still think there is a good chance that long term rates stay higher for a while and for not all good reason, aka, debts and deficits finally matter and foreigners are not much of a help anymore. I get the economic bull case for longer term Treasuries but as said, maybe it’s just not that easy as the bond bull market of 40 years is over.

10 yr Bid to Cover

10 yr Yield

BY Doug Kass · Aug 7, 2024, 2:30 PM EDT

Adding to MSOS and OXY (earnings to be reported after the close).

BY Doug Kass · Aug 7, 2024, 2:13 PM EDT

BY Doug Kass · Aug 7, 2024, 1:50 PM EDT

* And I expect the move in a sutherly direction to continue...

Homebuilders, the object of my recent dissaffection, are a downside leader today (as they have been all week).

Here is a summary of my short thesis on this sector from July 24:

BY Doug Kass · Aug 7, 2024, 1:30 PM EDT

META and NVDA turn red.

From earlier today:

(META) and (NVDA) intraday charts stink.

An observation.

Position: None

BY DOUG KASS AUG 7, 2024 11:23 AM EDT

BY Doug Kass · Aug 7, 2024, 12:20 PM EDT

META and NVDA intraday charts stink.

An observation.

BY Doug Kass · Aug 7, 2024, 11:23 AM EDT

I took a small, quick profit in my Index shorts:

* SPY $528.40

* QQQ $445.57

From 45 minutes ago:

With S&P cash +70 handles following short rentals:

* (SPY) $530.04

* (QQQ) $447.60

Position: Short SPY (vs) QQQ (vs)

BY Doug Kass · Aug 7, 2024, 10:38 AM EDT

With S&P cash +70 handles following short rentals:

* SPY $530.04

* QQQ $447.60

BY Doug Kass · Aug 7, 2024, 9:48 AM EDT

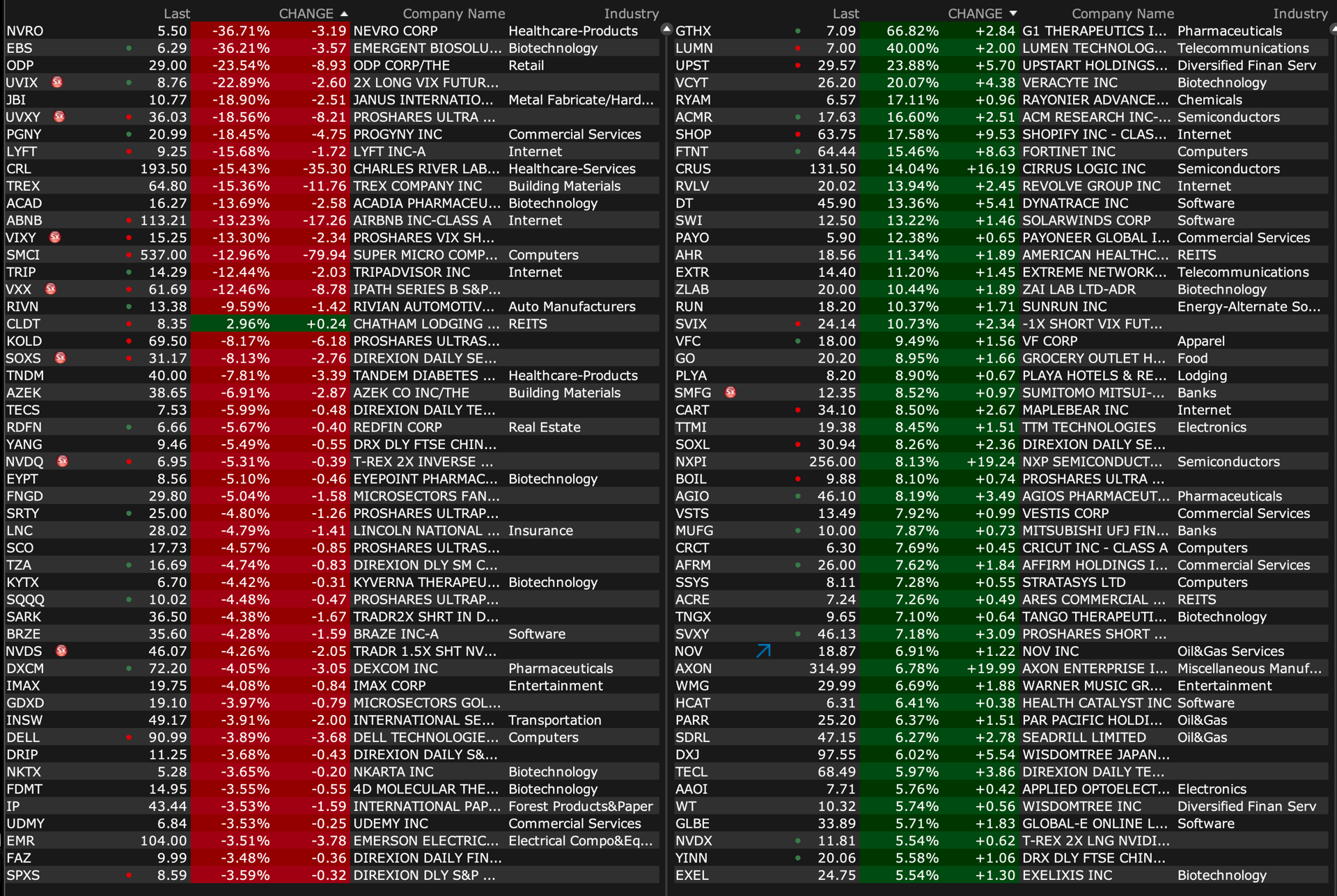

As of 8:48 a.m. ET:

-GTHX +66% (to be acquired by Pharmacosmos Group at $7.15/shr in cash in ~$405M deal)

-LUMN +35% (earnings, guidance)

-INGN +25% (earnings, guidance)

-UPST +24% (earnings, guidance)

-SWIM +21% (earnings, guidance)

-VCYT +21% (earnings, guidance)

-ACMR +17% (earnings, guidance)

-FTNT +15% (earnings, guidance)

-RVLV +14% (earnings, guidance)

-CRUS +13% (earnings, guidance)

-GO +12% (earnings, guidance)

-RUN +12% (earnings, guidance)

-EMKR +11% (earnings, guidance)

-SMWB +11% (earnings, guidance)

-VFC +9.5% (earnings, guidance)

-CART +9.4% (earnings, guidance)

-ANGI +8.9% (earnings, guidance)

-ALTO +8.7% (earnings)

-COOK +7.0% (earnings, guidance)

-FGEN +6.7% (earnings)

-RPD +6.0% (earnings, guidance)

-AAOI +5.9% (earnings, guidance; files to sell up to $60M of common stock)

-EXEL +5.5% (earnings, guidance)

-HALO +5.0% (earnings, guidance)

-MU +4.5% (stock repurchase program may resume)

-IFF +3.4% (earnings, guidance)

-OSCR +2.0% (earnings, guidance)

-STEM -39% (earnings, guidance)

-EBS -36% (earnings, guidance)

-NVRO -32% (earnings, guidance)

-CYRX -18% (earnings, guidance)

-PGNY -17% (earnings, guidance)

-PRCH -17% (earnings, guidance)

-ABNB -14% (earnings, guidance)

-TREX -16% (earnings, guidance)

-LYFT -14% (earnings, guidance)

-SMCI -14% (earnings, guidance)

-REAL -12% (earnings, guidance)

-FLYW -10% (earnings, guidance)

-HDSN -8.8% (earnings, guidance)

-RIVN -8.5% (earnings, guidance)

-PGEN -7.4% (reducing workforce by 20%; files to sell $30M public offering of common stock)

-VECO -5.5% (earnings, guidance)

-SVC -3.5% (earnings)

-HLT -3.4% (earnings, guidance)

-AMSC -2.9% (earnings, guidance)

-IRBT -2.9% (earnings, guidance)

-TOST -2.9% (earnings, guidance)

-CPNG -2.1% (earnings)

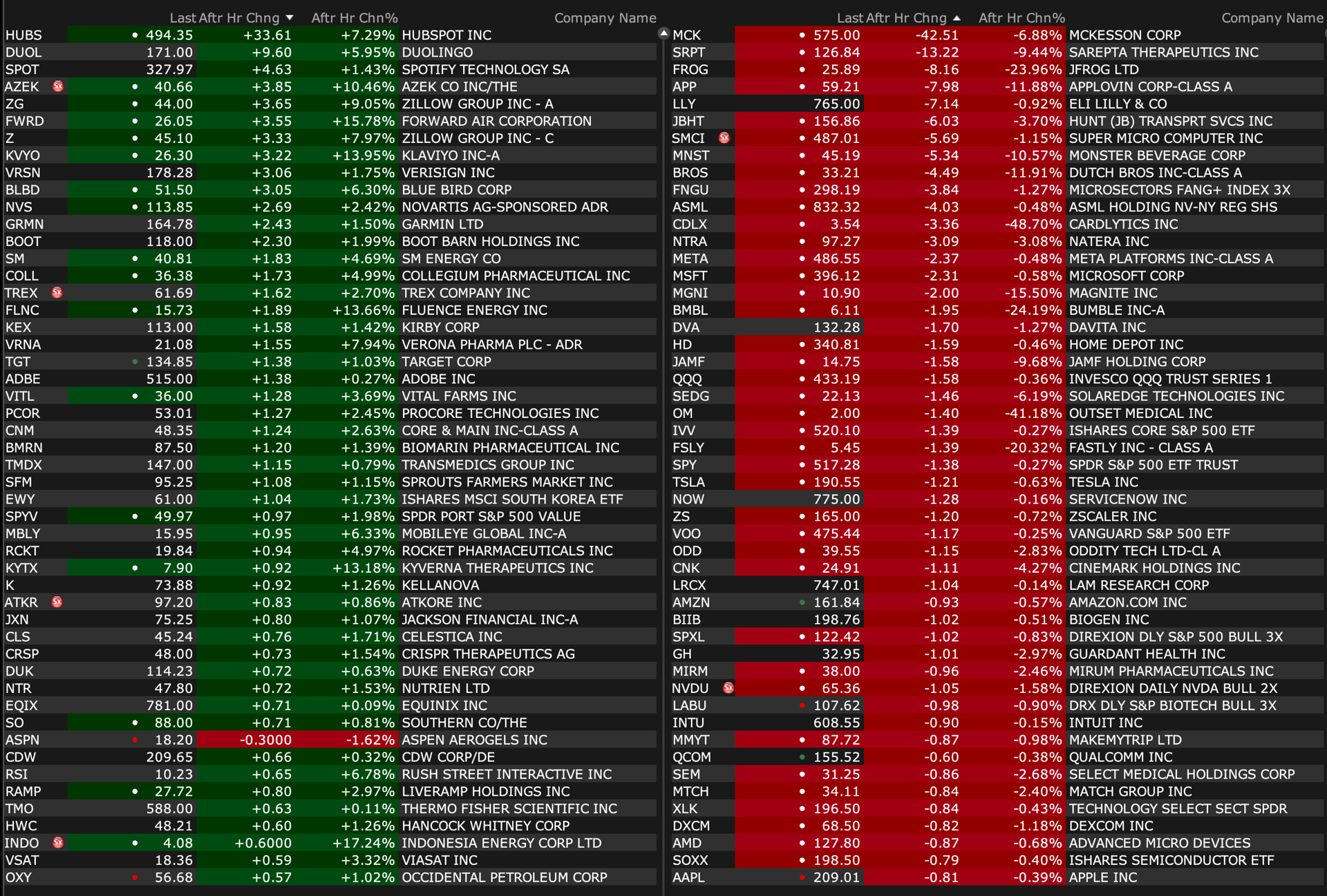

BY Doug Kass · Aug 7, 2024, 9:20 AM EDT

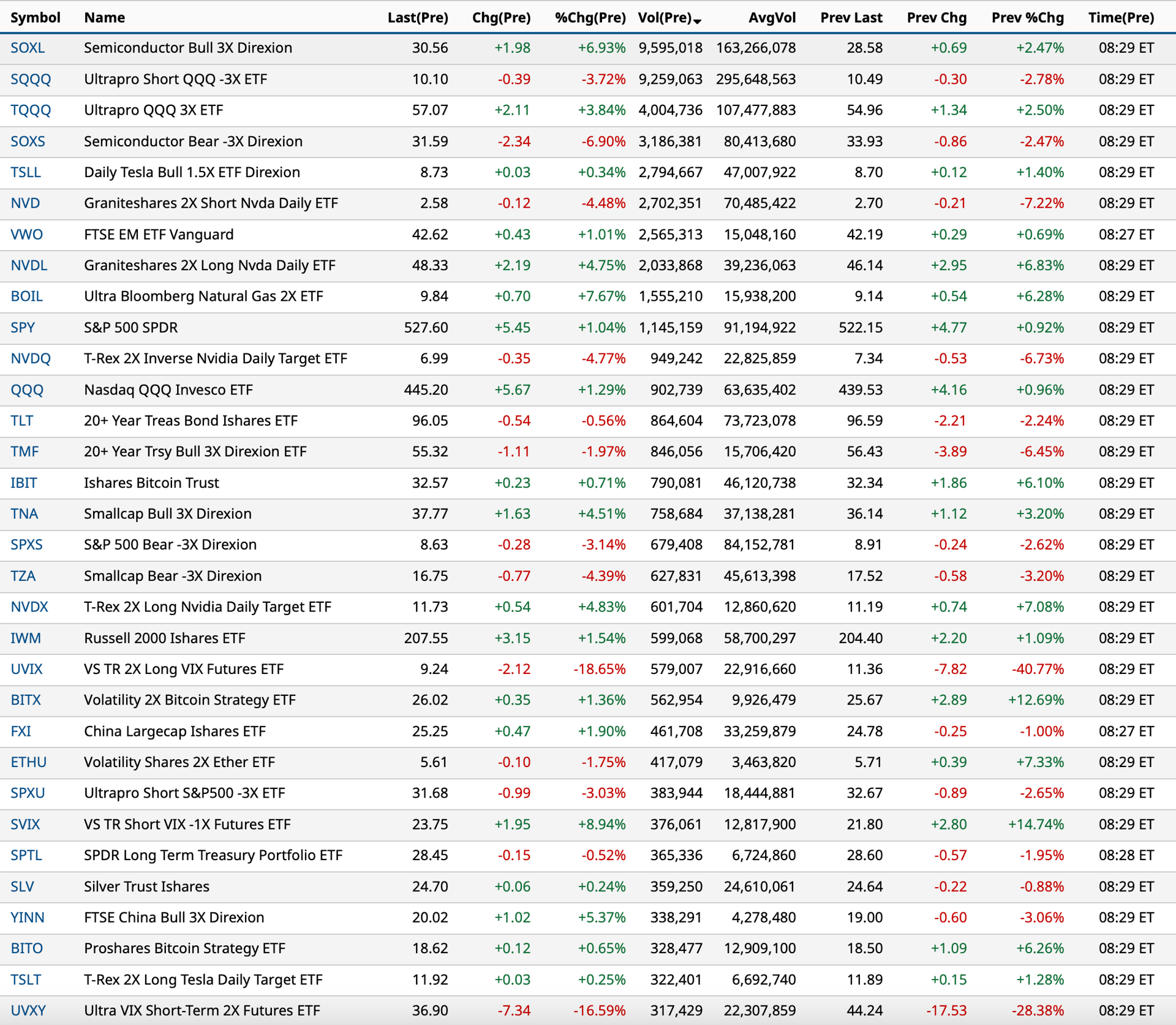

Most active exchange-traded funds as of 8:29 a.m. ET:

BY Doug Kass · Aug 7, 2024, 9:12 AM EDT

Chart as of 8:48 a.m. ET:

BY Doug Kass · Aug 7, 2024, 9:05 AM EDT

From Peter Boockvar:

The BoJ already has shaky knees with tightening/Travel & leisure story becoming more mixed

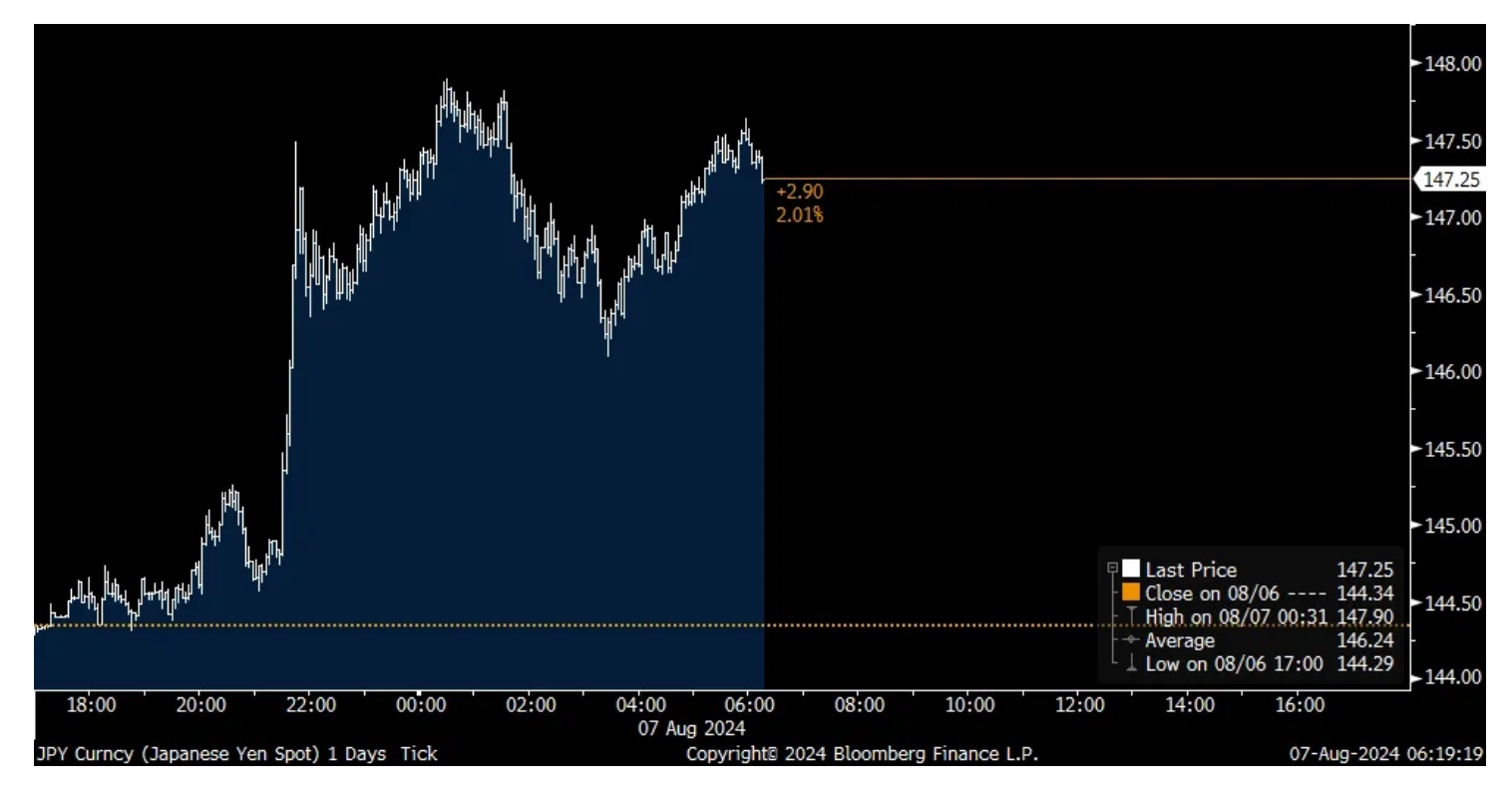

We know markets love the soothing talk of a central banker who tries to calm markets. The Deputy Governor of the BoJ, Shinichi Uchida, came out today and said "As we're seeing sharp volatility in domestic and overseas financial markets, it's necessary to maintain current levels of monetary easing for the time being...Personally, I see more factors popping up that require us being cautious about raising interest rates." This committee just can't get anything right as if now they don't hike again, the carry trade will just resume again, and inflation and a weak currency will continue to eat away at the standard of living of the Japanese people. They are trapped.

Here is the yen intraday move when he said it:

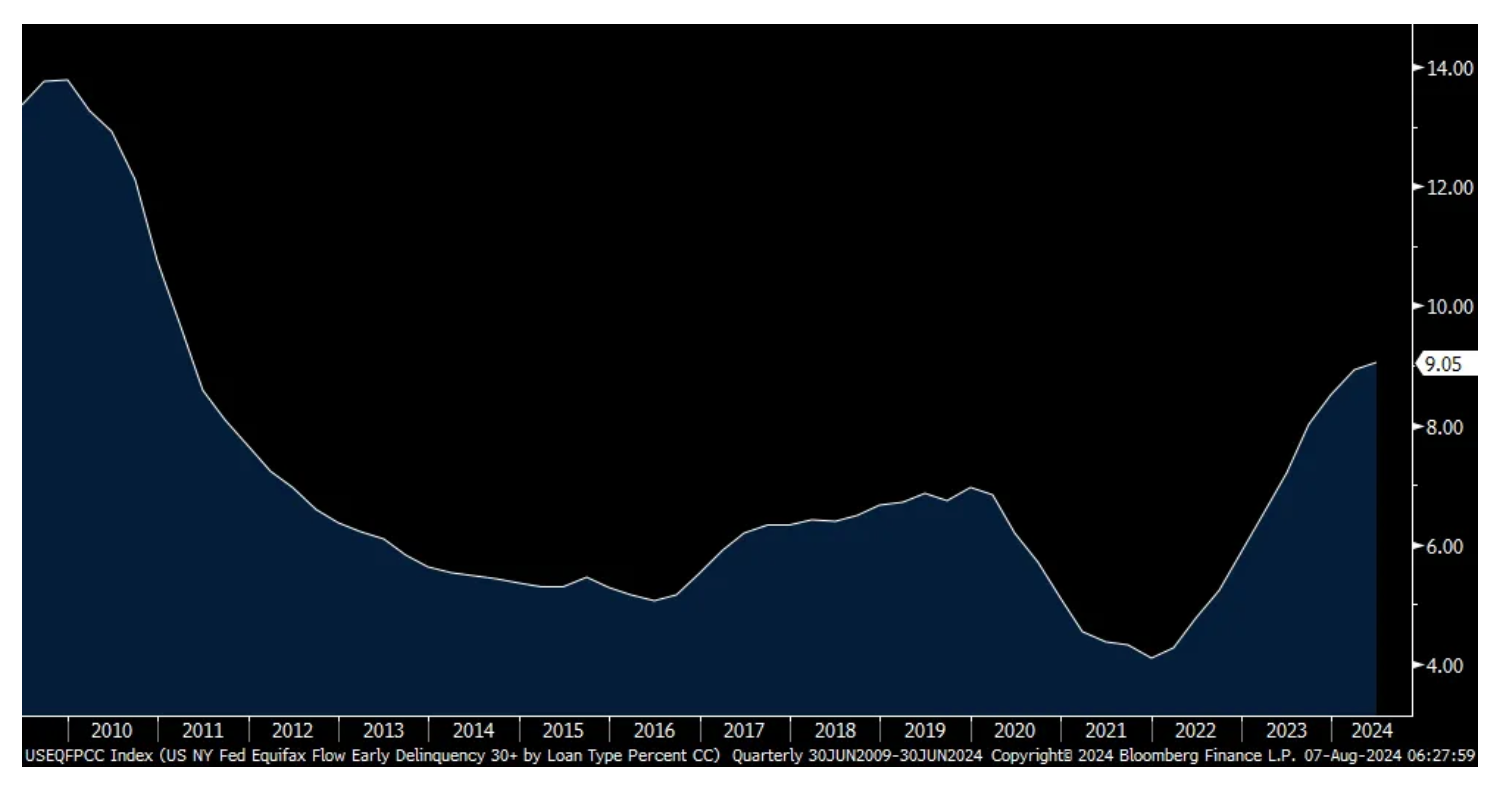

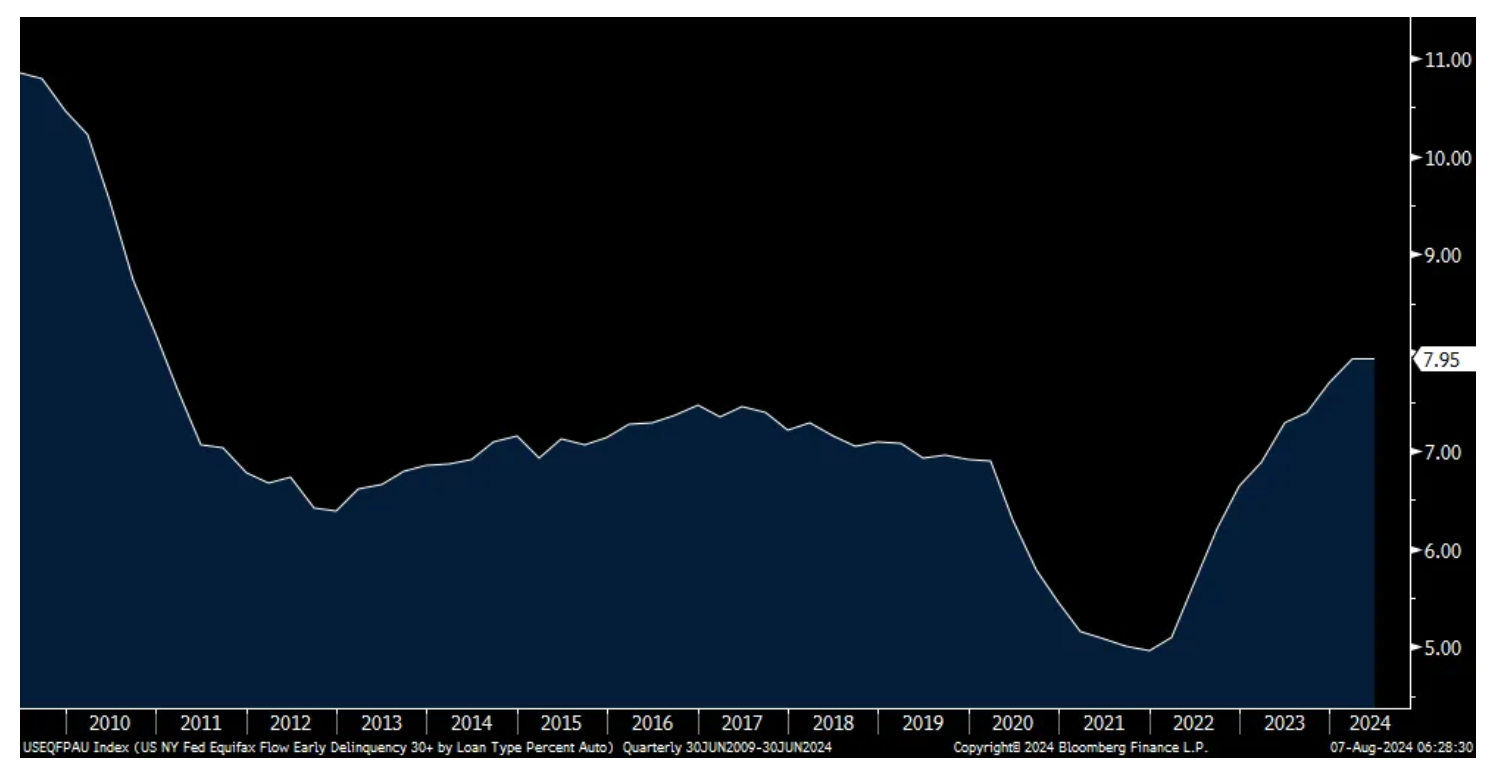

Yesterday the NY Fed came out with its Household Debt and Credit Report and they said that aggregate debt at the household level rose to $17.8 trillion, up $109 billion q/o/q. It's important though to compare with GDP rather than just on an absolute basis. With regards to delinquency rates, they were unchanged from the prior quarter at 3.2%. Specifically, "Delinquency transition rates for credit cards, auto loans, and mortgages increased slightly." However, the 30 day delinquency rate for credit cards at 9.1% and autos at 8% are the highest since 2011.

Also of interest, "Homeowners continued to increase HELOC balances as an alternative way to extract home equity." At current rates, they'd only be doing so if they needed the money. https://www.newyorkfed.org/microeconomics/hhdc

Credit Card 30 day Delinquency Rate

Auto Loan 30 day Delinquency Rate

Out a few days ago, the quarterly Senior Loan Officer said this:

"Regarding loans to businesses, survey respondents reported, on balance, tighter standards and basically unchanged demand for commercial and industrial (C&I) loans to firms of all sizes over the second quarter. Meanwhile, banks reported tighter standards and weaker demand for all commercial real estate (CRE) loan categories."

"For loans to households, banks reported, on balance, basically unchanged lending standards and weaker demand across all categories of residential real estate (RRE) loans. In addition, banks reported basically unchanged lending standards and unchanged demand for home equity lines of credit (HELOCs). Moreover, standards reportedly tightened for credit card and other consumer loans but remained basically unchanged for auto loans, while demand weakened for auto and other consumer loans but remained basically unchanged for credit card loans."

Note that the HELOC comment here doesn't square with what the NY Fed said about increased demand.

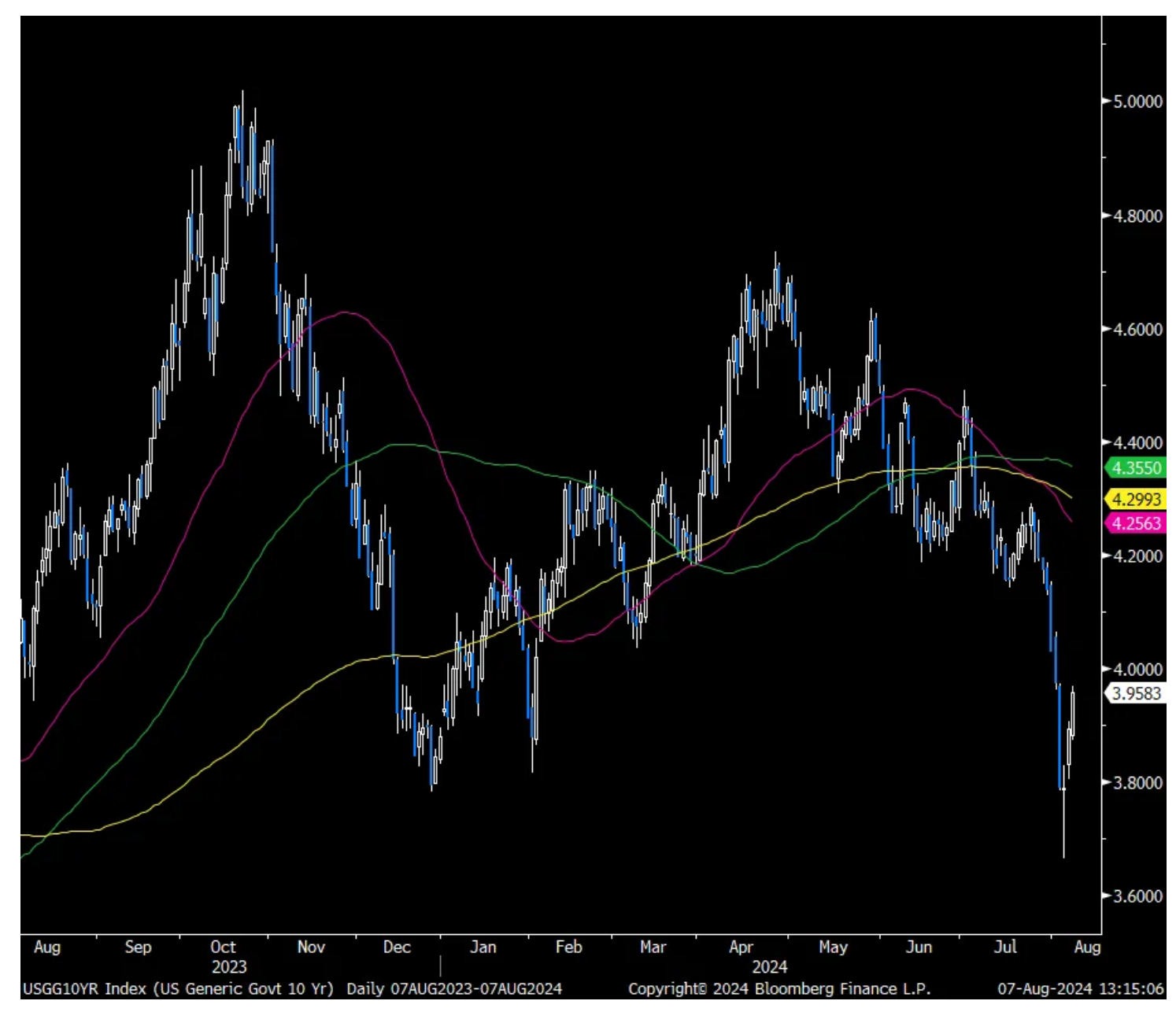

For perspective I mentioned Monday that key 10 yr Treasury yield level of around 3.75-3.80% level as it was the launching point for the move last year to 5% when the BoJ widened YCC. As seen the past two days, it's at least providing a level of support.

10 yr US Yield

To some earnings calls and the travel and leisure story is becoming more mixed.

From Airbnb, trading down post earnings:

With regards to their Q3 guidance, "we are seeing shorter booking lead times globally and some signs of slowing demand from US guests, and our Q3 outlook incorporates these recent trends. We're watching these trends closely, along with the impact any macroeconomic pressures might be causing."

Here was more elaboration, "What we've seen more recently, and in particular in July, is a shrinking of the lead times. And in particular, what we've seen is that there continues to be very strong growth of the shorter lead times, so anything from same day to next week to a couple of weeks from now. But what we're not seeing the same level of strength is in those longer lead times. So two months from now, what you're booking for Thanksgiving, what you're booking for Christmas. And so it's that, I would say softness in terms of longer lead times. That is a big factor in terms of the outlook that we've provided."

From Wynn Resorts:

At Wynn Las Vegas, "demand has remained healthy in 3Q with RevPAR up and slot handle broadly in line y/o/y during July despite this year having two fewer weekend days."

At Boston Encore, "More recently, demand has remained healthy through July with table drops, slot handle and RevPAR all up on a touch y/o/y comp."

In their Macau business, they had 99% hotel occupancy in the month of July. The Chinese consumer is still alive.

To what MGM talked about last week on their shorter booking window, particularly with F1, and what we heard from Airbnb above, "the booking window is relatively short other than for group and then certain special events, F1 in particular...we're not seeing anything of concern per se with respect to Q4. F1 specifically, which I know was mentioned extensively again on a previous call (the MGM one), F1, they're really top notch operators. And unlike last year when they heavily marketed throughout the year, they just started their big marketing push for the race this month, August. So I'm sure the race will be well executed."

On the outlook, "Q3 continues to pace very well. It's solid. August and September look even better than July. And when we look to Q4, pacing well for the year, will be the best year we've ever had in group and convention and '25 seems to be pacing actually ahead of that, all with strong ADR growth."

From Hyatt Hotels:

"While there are signs of slowing demand in lower chain scales, we saw strength among the high end consumer as luxury RevPAR increased 6.9%, driven by hotels in Europe and Asia Pacific excluding China. The solid quarter of group and business travel is reflected in our upper upscale brands, which produced RevPAR growth of 4.2%."

"unfavorable macro conditions and greater outbound Chinese travel negatively impacted results in the quarter." Domestic travel there fell 9% y/o/y off tough comps when last year saw the post Covid snapback.

From Disney's press release on the theme park business, and a stock we own:

"Segment revenue growth was impacted by moderation of consumer demand towards the end of Q3 that exceeded our previous expectations...While results at Domestic Parks decreased modestly in the quarter, attendance was comparable y/o/y and per capita spending was slightly up."

From Yum Brands:

"While we take comfort in improving global trends and still expect the first quarter will mark the low for same-store sales growth, significant volatility remains and we recognize sales in some markets are not where we want them to be."

Specifically, "The impacts from the Middle East conflict, in addition to a more cost conscious consumer have presented headwinds to same store sales."

Also of note, and to compete against the $5 short term deal offer from McDonald's, "ensuring we provide consumers affordable options has been an area of greater focus for us since last year will all of our brands having offered disruptive deals or reintroduced attractive everyday value with examples in the US such as KFC's Taste of KFC Deals, Pizza Hut's $7 Deal Lover's, and Taco Bell's Cravings Value menu."

From Avis Budget Group, benefiting from all that travel:

"The environment for our business remains robust with record setting 2nd quarter volume in the Americas. Pricing improved sequentially in May and June from April, with June exiting down 2% y/o/y, but still up significantly compared to 2019 with the Americas showing positive signs for summer pricing."

They spoke positively on their European business as we know summer travel there has been strong.

On the outlook, "the summer started off strong with positive pricing for the July 4th holiday in US rental car, setting us up well for the 3rd quarter where we expect pricing for the company to about flat for the quarter."

From Uber:

"While our consumers tend to be higher income, we're not seeing any softness or trading down across any income cohort. Were the current macroeconomic fears to materialize, we're confident that Uber can perform well because of the countercyclical nature of our platform."

On the delivery side, "in Q2, the number of first time consumers on Uber Eats in the US was higher than at any other point over the past five quarters. It's clear that delivery is much more habitual than many assumed and made even more so by our Uber One membership which now covers 50% of delivery gross bookings."

Even with another leg lower in mortgage rates, to 6.55% according to the Mortgage Bankers Association, purchase applications are yet to see any lift, rising by just .8% w/o/w after 3 weeks in a row of declines. Refi's though did as they jumped 16% w/o/w after dropping by 7.2% in the week before. As seen with the NY Fed data, people are increasing their use of HELOC's and maybe some with mortgages above 7% struck over the past year are refi'ing.

China gave us their trade data and exports in July rose 7% y/o/y, below the forecast of up 9.5%. It's possible that some goods disinflation was the reason as volumes were still pretty good. Imports though exceeded expectations with a 7.2% y/o/y rise, more than double the estimate of up 3.2% y/o/y and could reflect the front loading of orders ahead of any new trade and tariff restrictions.

Somewhat dated but Germany said its June exports fell 3.4% m/o/m, worse than the estimate of down 1.5% and reflecting the goods challenges they and others are experiencing.

BY Doug Kass · Aug 7, 2024, 8:50 AM EDT

* The consumer is spent up and not pent up.

* High theme park admission prices (and demand elasticity) have been long standing concerns of mine.

* And helps to explain why I have been reluctant to have a sizeable position in this name despite the share price drop and the apparent value.

I have continually warned about elasticity of demand in high priced consumer products.

Case in point - this morning Disney warned about weakness in theme parks (a continued refrain of mine) - from late July:

A core investment short McDonald's (MCD) spits the bit on earnings per share and announces weaker-than-expected organic sales.Here is the company's press release. McDONALD'S REPORTS SECOND QUARTER 2024 RESULTS (prnewswire.com)

I have long been of the view that the cumulative or "stacked" inflation since 2020 bodes poorly for personal consumption expenditures.

Whether it is the cost of admission for theme parks (at Disney (DIS) or Comcast (CMCSA) ) or the price of a latte - demand elasticity is hitting hard now.

A consumer-led economic slowdown likely lies directly ahead.

We are short 13 consumer related equities.

Position: Short MCD (S)

By Doug KassJul 29, 2024 7:19 AM EDT

And here are more big picture concerns that have kept me from building up the long position despite the share price decline:

In premarket trading Disney (DIS) was +$0.40.

However I view the news that Iger's contract is going to be extended as a negative. To me, the extension is a tacit statement that there is a lot more work to do than consensus suggests.

Here is my most recent critical column on Disney:

Jul 06, 2023 ' 09:18 AM EDT DOUG KASS

* Disney and Paramount may be instructive examples of high profile investing and activist mistakes from several market legends

* Rapid secular shifts in consumption, operating challenges and large debtloads have likely taken DIS and PARA out of the ranks of the "wonderful" class of American corporations

* The near to intermediate term outlooks for the share prices of Disney and Paramount look, for now, problematic... despite the large share price declines both may still represent value traps

"It's far better to buy a wonderful company at a fair price, than a fair company at a wonderful price."

- Warren Buffett

There is less than meets the eyes with regard to the futures of Disney (DIS) and Paramount Global (PARA) - two companies with a lot of debt and declining fundamental fortunes, as the media landscape undergoes a difficult, unprofitable and painful shift from linear to (content expensive) streaming.

Investment in these two companies appear to be examples how even some of the greatest money managers (Warren Buffett/Berkshire Hathaway (BRK.A) (BRK.B) , Michael Dell (DELL) ) and activists (Nelson Peltz and Dan Loeb) might have made meaningful mistakes by failing to recognize that the wonderful financial and operating profiles of the past are becoming a distant memory.

DISNEY

Despite an extensive list of well-recognized and popular product offerings - movies, theme parks, merchandise etc. - Disney's fortunes have deteriorated under the weight of legacy debt (from the Fox (FOX) deal), an historically bloated cost structure and other operational challenges -mainly the transition from previously profitable linear media to now unprofitable and capital/content intensive streaming:

Jun 22, 2023 ' 01:08 PM EDT DOUG KASS

* I continue to avoid Disney despite its sharp share price drop and serial underperformance

Under $90 I would normally be buying Disney (DIS) - especially with several activists as vocal and significant stakeholders.

But there is nothing normal about the accumulating threats to the company's near and intermediate term prospects:

* The legacy broadcasting business is deteriorating much faster than expected - for Disney and its competitors.

* The transition from formerly high margined linear broadcasting to streaming has become unexpectedly more difficult with, among other issues, content expenses out of control.

* A series of theatrical disappointments are raising red flags - particularly with the threat of AI oriented peers.

* Even the company recently admitted that the ridiculously high price of admission prices to Disney's theme parks has likely approached or is at the limit.

* Disney's future leadership is uncertain.

* To offset some of the above, the company has embarked on a cost cutting effort - but the low hanging fruit of cuts have likely been picked.

* The shares are "over owned" and given the erosion in fundamentals (2023-24 EPS estimates are too high) I don't know where the marginal buyer comes from.

PARAMOUNT GLOBAL

Paramount also faces the dual challenge of a large debt load and the formidable challenge of transition from linear to streaming:

Apr 25, 2023 ' 03:08 PM EDT DOUG KASS

I have shifted down in my exposure to Paramount Global (PARA) - from medium to small sized.

I did this based primarily on the likely weakening profit and cash flow picture at the company and at other streamers. As mentioned previously, despite cutting content expenditures, PARA will have to go into its cash account to cover the quarterly dividend.

I am also importantly influenced by the weakness in the share prices of PARA's streaming peers.

Not only is Disney's (DIS) share price lower but I am especially concerned about the weak price performance of Warner Discovery's (WBD) common shares - despite the strong buy issued at Goldman Sachs over the last few trading sessions.

May 04, 2023 ' 07:51 AM EDT DOUG KASS

* Good sale back in April

Back in late April I reduced my (PARA) long position dramatically - from medium sized down to tag ends:

Apr 25, 2023 ' 03:08 PM EDT DOUG KASS

I have shifted down in my exposure to Paramount Global (PARA) - from medium to small sized.

I did this based primarily on the likely weakening profit and cash flow picture at the company and at other streamers. As mentioned previously, despite cutting content expenditures, PARA will have to go into its cash account to cover the quarterly dividend.

I am also importantly influenced by the weakness in the share prices of PARA's streaming peers.

Not only is Disney's (DIS) share price lower but I am especially concerned about the weak price performance of Warner Discovery's (WBD) common shares - despite the strong buy issued at Goldman Sachs over the last few trading sessions.

My concerns were fulfilled this morning as the company reported an operating loss and reduced its dividend.

Paramount Global misses by $0.09, misses on revs (22.89)

Bottom Line

For the reasons mentioned in this morning's opening missive I am still avoiding the shares of Disney and Paramount.

Position: Long DIS calls

Jul 13, 2023 8:26 AM EDT

Whether it is the cost of admission for theme parks (at Disney (DIS) or Comcast (CMCSA) ) or the price of a latte - demand elasticity is hitting hard now.A consumer-led economic slowdown likely lies directly ahead.We are short 13 consumer related equities.Position: Short MCD (S)

By Doug Kass

Jul 29, 2024 7:19 AM EDT

BY Doug Kass · Aug 7, 2024, 8:00 AM EDT

BY Doug Kass · Aug 7, 2024, 7:41 AM EDT

VP Nominee Tim Walz is friendly towards cannabis legislation.

BY Doug Kass · Aug 7, 2024, 7:30 AM EDT

“Trends are not endless. In fact, the greater the consensus belief in the persistence of a trend, the less likely it is to persist.”

- Arthur Zeikel

Bonus - here are some great links:

Gauging The Market Bottom 6 Things to Watch for a Market Bottom (barrons.com)

Recent Volatility 10 Talking Points About the Recent Volatility - Carson Group Where

Are the New Lows? Where are the new lows? - All Star Charts -

Critical Nasdaq Levels QQQ: Critical Levels to Watch as Nasdaq Teeters on the Edge | Don't Ignore This Chart! | StockCharts.com

BY Doug Kass · Aug 7, 2024, 7:20 AM EDT

BY Doug Kass · Aug 7, 2024, 7:10 AM EDT

BY Doug Kass · Aug 7, 2024, 7:00 AM EDT

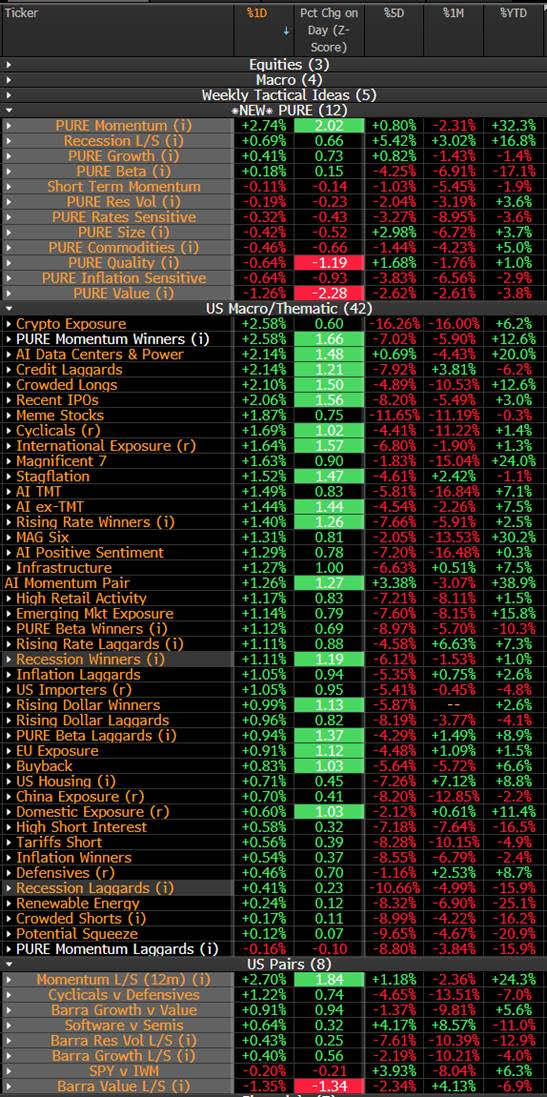

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Aug 7, 2024, 6:50 AM EDT

From JPMorgan:

US: Futs are higher with both Tech and small-caps outperforming as the relief rally continues as BOJ states it will not hike with markets are unstable. Pre-mkt, Mag7 are all higher and Semis are shrugging off SMCI earnings (-12%) ad NVDA, AVGO, AMD, and QCOM are leading the group higher each up 1%+. Bond yields are higher by 4-5bps, and USD is higher, now looking to erase its WTD loss. Cmdtys have caught a bid with WTI, base metals, and Ags all seeing strength. Mtge Applications and 10Y bond auction are the major macro data pts. Is the panic unwind finished? Detailed thoughts are below.

and...

EQUITY AND MACRO NARRATIVE: Yesterday was a broad rally with 78% of the SPX up on the day with VIX falling below 25 and Treasuries seeing some profit-taking from the recent move. SPX, +1%, helping to assuage some concerns about a market meltdown. The 10Y yield moved from 4.17% on July 29 to a low of 3.79% on Monday; it closed at 3.90% yesterday. The question is did we see the bottom?

YES, THAT WAS THE BOTTOM

· A SHEEP IN WOLF’S CLOTHING – what was characterized as a Growth Scare may have been a convenient way to describe a technical sell-off induced by the unwind of the carry trade and subsequent forced selling. Fundamentally, ISM-Mfg and NFP are not strong enough catalysts to trigger the magnitude of the recent price action. ISM-Mfg has been sub-50 every month since October 2022 except for the March 2024 print and the economy went on to rebound to above-trend level GDP over the last year. NFP printed 114k vs. 183k average from 2010 – 2019; still within the longer-term averages albeit slowing from historically low unemployment levels. Also, the US just printed +2.8% real GDP growth in 24Q2 so the probability of this pronounced a decline in growth, implied by the recent price action, without an exogenous shock seems low.

· MACRO AND MICRO FUNDAMENTALS REMAIN SOLID – The Atlanta Fed’s GDPNow estimate is 2.9% as of Aug 6. This comes after the economy printed above-trend growth in 3 of the last 4 quarters. US Real GDP QoQ: 23Q3 = 4.9%, 23Q4 = 3.4%, 24Q1 = 1.4%, 24Q2 = 2.8%. With 75% of the SPX having reported, revenue growth is 5.0% and earnings growth is 12.1% vs. expectations of 4.5% and 8.5%, respectively. Profit margins ~12% vs. 11.5% (5-year average) vs. 11.8% (24Q1).

· PULLBACKS ARE A COMMON OCCURRENCE – a 5% pullback happens ~3x per year and a 10%+ pullback happens ~1x per year. This recent episode saw a -9.7% peak-to-trough move in the SPX, and we had a 5% pullback in April.

NO, THERE IS MORE DOWNSIDE COMING

· THE FED CAN STILL MAKE A MISTAKE – the latest article from WSJ’s Timiraos (article is here) suggest that a further weakening of the data is necessary to push the Fed from a 25bps to 50bps cut in September. This could setup Jackson Hole to deliver a hawkish surprise as markets are pricing in ~44bps of cuts at the September meeting. If the Fed were to push back on going 50bps, it seems likely the bond market would have very negative response.

· CTAs HAVE MORE FIREPOWER – If we fail to see follow-through buying from here then were are near some selling levels, e.g., next week the 3-month momentum level is 5,254 (Bram Kaplan’s note is here). This is separate from behavior witnessed if we see another vol spike.

· NEGATIVE SEASONALITY – August and September have typically been weak points in the year before giving way to Q4, the best quarter of the year. During election years that negative seasonality can extend into October given the policy uncertainty. Combine that with heightened geopolitical risks and it is tough to see material re-risking that takes the market higher in the near-term.

o Yesterday was the second consecutive day of MOC orders that exceeded $7bn. I don’t have exact stats on average size but anything over $2bn - $3bn is big.

BY Doug Kass · Aug 7, 2024, 6:40 AM EDT

BY Doug Kass · Aug 7, 2024, 6:30 AM EDT

Wolf Street on drunken sailors.

BY Doug Kass · Aug 7, 2024, 6:20 AM EDT

The BOJ statement (a dovish signal after the recent rate rise) is the reason for the reversal higher in stock futures.

But I suspect market participants are overreacting to an obvious word of caution from the Bank of Japan.

This market remains difficult to navigate on any short-term horizon!

BY Doug Kass · Aug 7, 2024, 6:07 AM EDT

From my friends at Miller Tabak:

Tuesday, August 6, 2024

In response to the poor July jobs report and ensuing financial distress, we reiterate the position that we have held since mid-2023. 2024 will be a year where growth and inflation first normalize, followed by a period of slow, but positive, growth as the Fed’s previous interest rate hikes bite. We also wrote last week that the U.S. labor market is now vulnerable to a faster rise in unemployment. The past week of data is consistent with our position. The response to the jobs report is an overreaction, driven by those who mistakenly believed that the economy was re-accelerating, having to adjust their outlook.

We are increasing our odds of a recession beginning within the next year, but only from 15% to 20%. A recession remains unlikely because the U.S. economy is not yet ripe for one. Although household finances have deteriorated somewhat over the past few years, they are still solid. Businesses continue to have a good appetite for investment and housing should quickly recover once mortgage rates decline in the coming months. The unemployment rate of 4.3% is still below the CBO’s 4.4% estimate of full employment. 2.8% GDP growth from 2Q2024 was surely an outlier, but it still shows an economy far from recession. We instead expect slow GDP growth, around 1.0% (down from 1.5%), for the rest of the year.

Our recession odds are slightly higher for a pair of reasons. First, the labor market is weakening faster than we expected, giving the Fed less time to change course. Although we expect them to now begin an aggressive rate cutting cycle (more on this below), there is some risk that they will dally. More importantly, while the ongoing asset price volatility will not cause a recession by itself, there is a risk that it could spread. Recessions are fundamentally periods of de-leveraging and if fear is deep enough and lasts long enough, it is possible that households and firms pull back even though their balance sheets are in good shape. Economic fundamentals, however, suggest that this is unlikely.

BY Doug Kass · Aug 7, 2024, 5:55 AM EDT