Enjoy the Weekend

Thanks for reading today and all week.

I am going back to bed.

Enjoy the weekend.

Be safe.

BY Doug Kass · Jul 26, 2024, 4:15 PM EDT

Thanks for reading today and all week.

I am going back to bed.

Enjoy the weekend.

Be safe.

BY Doug Kass · Jul 26, 2024, 4:15 PM EDT

From Randorama:

Randy

On occasion, back-to-back 80% Upside Days (such as August 1 and August 2, 1996) have occurred instead of a single 90% Upside Day to signal the completion of the major reversal pattern. Back-to-back 80% Upside Days are relatively rare except for these reversals from a major market low. 7 6. In approximately half the cases in the past 69 years, the 90% Upside Day, or the backto-back 80% Upside Days, which signaled a major market reversal, occurred within five trading days or less of the market low. There are, however, a few notable exceptions, such as January 2, 1975 or August 2, 1996. As a general rule, the longer it takes for buyers to enthusiastically rush in after the market low, the more investors should look for other confirmatory evidence of a market reversal

BY Doug Kass · Jul 26, 2024, 3:45 PM EDT

I would observe that the first sector to weaken during any "weakness" is technology.

BY Doug Kass · Jul 26, 2024, 3:35 PM EDT

Wolf Street howls about core PCE inflation.

BY Doug Kass · Jul 26, 2024, 3:20 PM EDT

BY Doug Kass · Jul 26, 2024, 3:09 PM EDT

Peter Boockvar's Succinct Summation of the Week's Events:

Positives,

1)The US July manufacturing and services composite PMI rose a touch to 55 from 54.8 with services still dominating the business action as this component rose to 56 from 55.3. Understand that this DOES NOT include retail and wholesale trade for some reason. The manufacturing side fell back below 50 at 49.5 from 51.6.

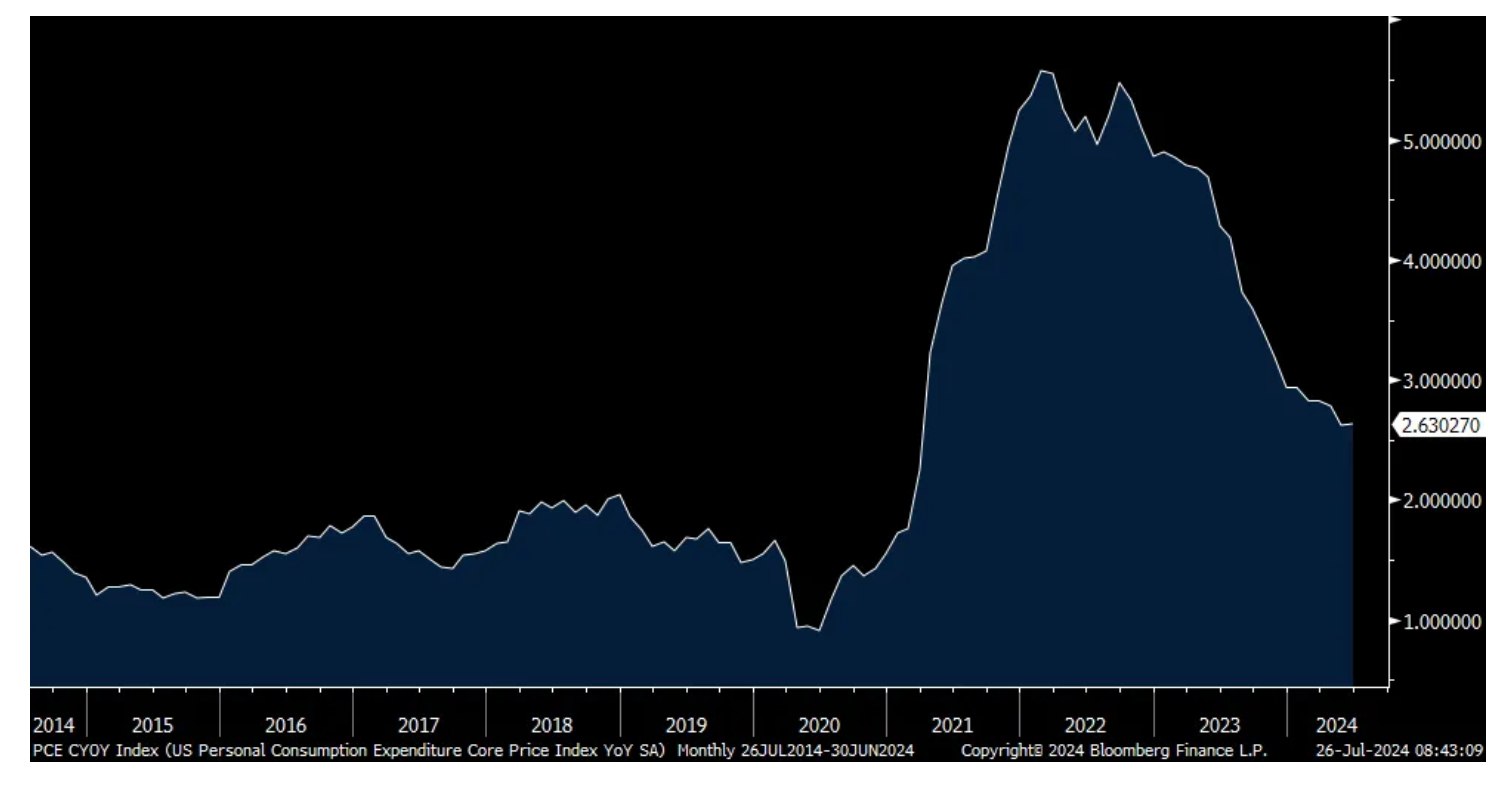

2)Headline and core PCE in June were spot on with expectations with one tenth headline and two tenths core m/o/m gains. The y/o/y change was 2.5% and 2.6% for each respectively vs 2.6% for each in May.

3)June personal spending rose as expected by .3% m/o/m but May was revised up by 2 tenths so we could get a slight tweak up in the Q2 GDP revision whenever it comes, all else equal.

4)US Q2 GDP growth was 2.8%, above the estimate of 2%. Three tenths of this upside was due to a lower than expected price deflator of 2.3% vs the estimate of 2.6%. Core PCE though of 2.9% was two tenths higher than expected. Personal spending, equipment and IP spend, along with higher inventories and government spending all drove the gain.

5)Initial jobless claims totaled 235k, remaining elevated relative to recent trends but 3k less than expected and down from 245k last week which included people filling after the July 4th holiday. Smoothing all this out puts the 4 week average at 236k vs 235k last week, hovering around the highest since last September. Continuing claims slipped by 9k to 1.851mm, but after rising by 13k in the week before.

6)Container shipping prices were mixed w/o/w but didn't rise. The Shanghai to Rotterdam trip was down a slight $7 at $8,260 and as a reminder it started the year at just under $1,700. The route to LA fell $354 w/o/w to $6,934 vs $2,100 at the beginning of the year.

7)The June US Architecture Billings Index came out and it rose to 46.4 from 42.4 as hopes grow for interest rate cuts. The AIA chief economist said, "Architecture firms continue to face a period of headwinds in the construction sector, driven by elevated interest rates, high construction costs, and generally weak property values. This is the 17th consecutive month of a billings decrease and yet, despite the softness firms remain generally optimistic that conditions will start to improve once interest rates begin to ease."

8)Mostly captured in the Q2 GDP report, core durable goods orders in June were better than expected (will actually how up in Q3 as shipments) but the shipments figure was a touch light.

9)From Chipotle: "We have leaned in and reemphasized generous portions across all of our restaurants as it is a core brand equity of Chipotle."

10)From Royal Caribbean: "The demand and pricing environment remained very strong since the last earnings calls. Booking volumes were higher than the corresponding period in 2023 and at record pricing levels. The company continues to be in a record booked position for 2024 sailings. Consumer spending onboard, as well as pre-cruise purchases, continue to significantly exceed 2023 levels driven by greater participation at higher prices."

11)From Texas Roadhouse: "there has been significant discussion within the restaurant industry concerning the health of the consumer as well as the increased focus on promotions and discounting from others in the industry. Through the first half of the year, we have not seen a measurable impact on our overall business from these issues. Our guests continue to recognize the quality and value we offer and do not appear to be changing their dining habits."

12)From Google/Alphabet: Their results "showed tremendous ongoing momentum in Search and great progress in Cloud with our AI initiatives driving new growth. Search had another excellent quarter."

13)From Deckers Outdoor: "HOKA performance driven by the brand's compelling product assortment, including new launches, which experienced strong demand across the brand's global marketplace...The UGG brand's more focused assortment of relevant franchises is driving the majority of consumer demand, which contributed to lower promotion as compared to prior first quarters, where the DTC business has historically been more influenced by end-of-season discounting on seasonal colors."

14)From Hermes: they referred to its quarter "against a more complex global economic and political backdrop" but seemed to outperform many of its peers. Sales rose 15% "driven by our loyal and new customer base. All regions recorded double digit growth and the division recorded good progress in a more complex environment."

15)From LVMH: "On the positive side, I would mention the continuation of the group's organic revenue growth with consistent trends throughout the first half. Good results in fashion and leather goods...continued growth from the Chinese clientele and double digit revenue growth at Sephora on very demanding comps."

16)From American Express: "At the same time, growth in our largest T&E category, restaurants, remained strong and goods and services strengthened a bit vs the prior quarter when excluding the impact of the Leap year."

17)From Group 1 Automotive: “I can’t, looking at our data for Group 1, say that we saw or are seeing any changes in the consumer – any material changes in the consumer.”

18)From GM: “So demand for our vehicles is strong…So I think we’ve been saying for a long time that our consumer has held up really well and it’s been resilient, and we expect that to continue to be the same way. I think a big part of that is the strategy that we’ve undertaken about being very disciplined in inventory and the more data flow about producing the vehicles that we know that customers are demanding.”

19)From IBM: "We had strong performance in software and infrastructure above our model as investment in innovation is yielding organic growth, while consulting remained below model. Our results underscore the continued success of our hybrid cloud and AI strategy and the strength of our diversified business."

20)From Texas Instruments: "Personal Electronics grew mid-teems with broad based growth while demonstrating continued improvement compared to its low point in the first quarter of 2023. Next, Communication Equipment was up mid-single digits. And finally, Enterprise Systems was up about 20%."

21)Tokyo reported July CPI and it rose 2.2% y/o/y headline vs 2.3% in June and one tenth less than expected. The core/core rate moderated to 1.5% y/o/y from 1.8% in June and that too was one tenth under the estimate. Part of the deceleration is the easy comp as July 2023 saw a 4% core/core rate increase.

22)As expected the Bank of Canada cut its benchmark rate by 25 bps to 4.50%. This is now their 2nd 25 bps cut this year while they continue on with “balance sheet normalization,” aka, shrinking it. Their bottom line for cutting, “With broad price pressure continuing to ease and inflation expected to move closer to 2%, Governing Council decided to reduce the policy interest rate by a further 25 bps.” They did lay out the factors they are balancing, “excess supply” lowering inflation on one hand but persistent shelter and services inflation, as stated, on the other.

23)Not that it will help much but China cut rates too.

24)Strength remains in India as its July PMI index rose to a solid 61.4 from 60.9 with both components higher.

25)Japan's July composite PMI index rose to 52.6 from 49.7 but it was all due to a 4.5 pt rise in services to 53.9 as manufacturing fell to 49.2 from 50.

26)The UK PMI was 52.7 from 52.3 with better performance in manufacturing as it rose to 51.8 from 50.9 and services was up to 52.4 from 52.1.

27)Germany saw a rise in consumer confidence to -18.4, up by 3.2 pts and GFK said some of that was due to the Euro 2024 football tournament along with "increased income expectations."

Negatives,

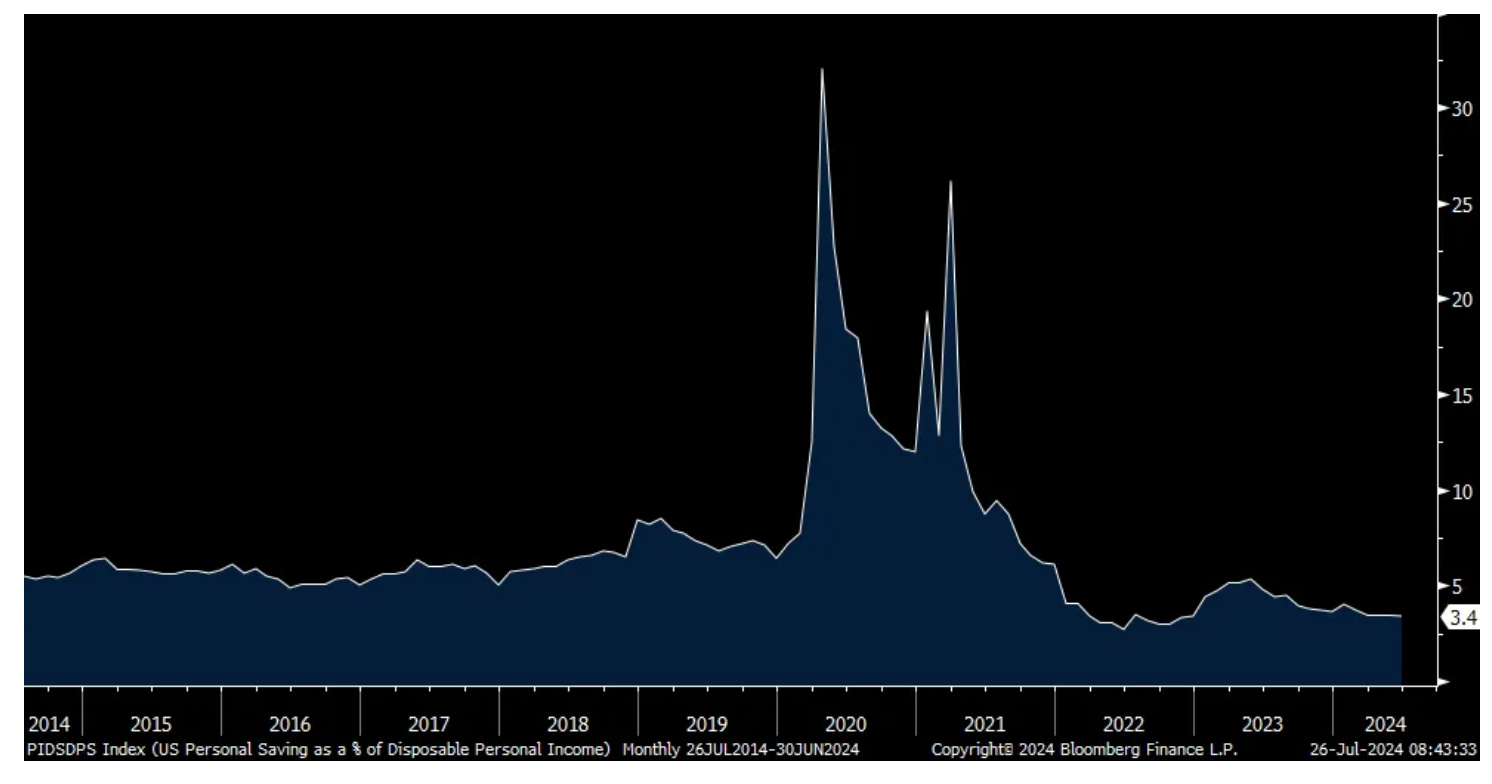

1)June personal income was light relative to the estimates. Combining this with the upside in spending puts the savings rate at 3.4% from 3.5% in May and that is the lowest since November 2022.

2)The final July UoM consumer confidence index was 66.4, the lowest since November and down from 68.2 in June, 69.1 in May, 77.2 in April and 79.4 in March. Both main components fell. It helps to own stocks though, "Not surprisingly, consumers with larger holdings tend to exhibit higher levels of sentiment than those with smaller (or no) holdings, due in part to the financial security and purchasing power afforded by more wealth" said the UoM. One year inflation expectations were 2.9% vs 3% in June but the same as the preliminary read. The 5-10 yr look was unchanged at 3%.

3)New home sales in June totaled 617k, 23k below expectations and little changed with the 621k seen in May but it is the smallest print since November. Smoothing out the monthly volatility in this figure puts the 3 month average at 656k vs the 6 month average of 660k and the 12 month average of 662k. Months’ supply, which includes homes completed, under construction and not yet started as does the headline sales number, rose to 9.3 months from 9.1 in May and 7.7 in April. That’s the highest since October 2022. Remember what Zillow said last week about more existing homes sitting for longer before being sold. According to Redfin today, “Redfin reports 65% of home listings have been sitting on the market longer than a month, up from 60% a year ago.”

4)Weekly mortgage apps fell 2.2% w/o/w all because of a 4% drop in purchases after the 2.7% fall last week. So, no real response yet from the dip below 7% in the average 30 yr mortgage rate. Purchases are back to the lowest since late May and just off the lowest level since 1995. Refi's were little changed w/o/w after last week's 15% jump.

5)June existing home sales totaled 3.89mm, about 100k below expectations, down from 4.11mm in May and that is just off the lowest since 2010 and not far from levels seen in the mid 1990’s. The key first time buyer made up 29% of purchases, a 4 month low. Supply did rise, as it does in the spring, with months’ supply now up to 4.1 from 3.7 and getting closer to what is normal. It was 4.3 months in June 2019. The 20 yr average is 5.4 months. The median home price was up 4.1% y/o/y. The NAR said something similar to what we heard from Zillow last week, “We’re seeing a slow shift from a seller’s market to a buyer’s market. Homes are sitting on the market a bit longer, and sellers are receiving fewer offers. More buyers are insisting on home inspections and appraisals and inventory is definitely rising on a national basis.”

6)The July Philly non-manufacturing index fell to the lowest level since December 2020.

7)The July Richmond manufacturing index fell to -17 from -10.

8)From Robert Half: “Client and candidate caution continues to impact hiring activity and new project starts as macroeconomic and interest rate uncertainty persist...Client budgets remain constrained and candidates are selectively changing jobs. This subdues short term demand and elongates sales cycles."

9)From Google/Alphabet: YouTube missed expectations with 13% y/o/y ad revenue growth. Worries grow about all that spend as it's mostly expense right now rather than a revenue driver, "Looking forward, we continue to expect to deliver full year 2024 Alphabet operating margin expansion relative to 2023. However, in the 3rd quarter, operating margins will reflect the impact of both the increases in depreciation and expenses associated with the higher levels of investment in our technical infrastructure as well as the increase in cost of revenues due to the pull forward of hardware launches into Q3." About $50b this year will be their cap ex spend. "I think the one way I think about it is when you go through a curve like this, the risk of under-investing is dramatically greater than the risk of over-investing for us here."

10)From Tesla: "So to recap, we saw a large adoption acceleration of EVs and then a bit of a hangover as others struggled to make compelling EVs. So there have been quite a few competing electric vehicles that have entered the market. And mostly, they have not done well, but they have discounted their EVs very substantially, which has made it a bit more difficult for Tesla."

11)From Brunswick: "With high interest rates continuing to pressure consumer budgets and suppress discretionary spending, the introduction of new model year products at the beginning of the important month of June did not catalyze boat purchases as we had anticipated, and our 2nd quarter results were slightly below expectations."

12)From Marine Max: "At the industry level, the aggressive promotional environment continued in Q3, amid elevated inventories, interest rates, and persistent concerns about inflation. The weakened consumer sentiment was evident in US powerboat registrations...While the premium end of the market is performing better than the value segment, and as we have said all year, it's not without its challenges."

13)From Polaris: “We saw an increasingly challenging environment in the 2nd quarter, resulting in sales and adjusted EPS that came in below our expectations...These headwinds included persistent inflation in addition to a prolonged cycle with elevated interest rates. We’ve seen consumer confidence weaken, especially for larger discretionary purchases, and as a result, the industry is seeing lower retail. Additionally, dealers are conservatively managing their inventory due to the higher flooring costs driven by higher interest rates and are reducing orders accordingly.”

14)From Nestle: "we're still seeing significant value-seeking behavior on the part of the consumer. There's stress, in particular, at the lower end of the income scale in North America, but also in select other geographies. And so people are value-seeking, and hence, our promotional intensity has been particularly strong."

15)From LVMH: "The main points to bear in mind are on the negative side. Continued economic and geopolitical uncertainties are still impacting certain businesses, notably wine and spirit although there are signs of the situation improving for Cognac in the US."

16)From Visa: "In the US, while growth in the high-spend consumer segment remained stable compared to prior quarters, we saw a slight moderation in the lower-spend consumer segment."

17)From Ryder: "we continue to see freight conditions that remain weak and the timing of the cycle inflection remains uncertain."

18)From Masco: "As uncertainty within the broader macroeconomic environment has continued, we are tempering our expectations for sales in the 2nd half of the year from up low single digits to roughly flat, leaving our full year sales within our previously guided range of plus or minus low single digits."

19)From Sherwin Williams: Specifically in North America and with their consumer business, sales fell "high single digit percentage, where weakness in existing home sales remains a headwind. Inflation, depleted savings, and household debt also continue to pressure consumers who currently appear to be spending their modest available discretionary dollars elsewhere. We understand where we are in this cycle and eventually expect to see an upturn in DIY demand." As for guidance, "It's clear that the macroeconomic environment has been softer for longer than many economists anticipated at the start of the year. We don't expect to get material help from the market in our back half."

20)From Pulte Home: "As good as our 2nd quarter numbers are, it's fair to say that as we navigated through the period demand was a little less consistent than we experienced in the 1st quarter of 2024."

21)From O'Reilly Automotive: “Our comparable store sales results were below our expectations for the 2nd quarter, as the soft demand environment we experienced at the beginning of the quarter persisted through May. Sales trends improved in June, in line with our expectations, aided by strong performance in summer weather related categories in many of our markets.”

22)From Genuine Parts: "Our quarterly results reflect softer than expected market conditions, which are tempering demand particularly in our Industrial and US and European Automotive businesses." They also mentioned the "challenging macro-environment."

23)From Lamb Weston: “Our financial results for the 4th quarter and for the year are disappointing, reflecting executional challenges both commercially and in our supply chain, as well as soft global demand for fries.” Being blamed in part to “softer than expected restaurant traffic trends in both the US and many of our key international markets.”

24)From STMicroelectronics: "During the quarter, contrary to our prior expectations, customer orders for industrial did not improve and automotive demand declined."

25)From NXP Semi: “Y/o/Y performance was a result of lower revenue in the automotive and communications infrastructure markets.”

26)From Texas Instruments: "First, the Industrial market was down low-single digits. The Automotive market was down mid-single digits."

27)From Kering: "In Western Europe, local demand was rather subdued, while tourism spending was more or less supportive, with some contrasts across brands and nationalities...North America remained in negative territory, but polarization based on brand positioning persisted, and Bottega Veneta in the higher end segment continued to outperform...Japan was up 22% comparable, with Q2 accelerating up 27%. The market is fueled by strong tourism spending, notably from China and other Asian countries. Most of our houses implemented tactical price increases to account for the weak yen, but the price gap remains attractive."

28)From Comcast: “Now let’s turn to Parks, where our results were down in both revenue and EBITDA when compared to last year’s record performance with 2/3rds of the decline driven by lower attendance at our domestic parks. We attribute this to a number of factors. First is what now appears to be a Covid recovery pull forward of a magnitude we hadn’t previously appreciated…More recently, other travel options including cruises and international tourism, given the strength of the dollar, have experienced their own surge in demand, which caused visitation rates at our parks to normalize.”

29)From Coca Cola: “overall, it’d be fair to say that consumer sentiment in aggregate is actually pretty strong, pretty resilient. Within that, there are some softer spots…some softness in away from home channels, with a little lower traffic, and certainly some increase in value seeking for combo meals. So, definitely there’s a piece of the lower income consumer which are either going out slightly less, or when they do go somewhere, looking for greater value through combo meals. And then, of course, in the at-home channels, there’s a slightly greater focus by those consumers on getting kind of value deals or promo deals."

30)From UPS: “we did see customers favoring our more economical products, so going from air to ground and within ground, from ground to SurePost. And that was across the broad base of customers.”

31)From Heartland Express: “We continue to believe that the freight market will improve as more capacity exits the market so the industry as a whole can return to more disciplined operating decisions and improved financial results. But, our current expectations of the timing of that favorable change likely extends into 2025.”

32)Blackstone Mortgage Trust cut their dividend sharply.

33)From Truist Financial: "Average loans decreased .7% on a sequential basis, reflecting overall weaker client demand." And, "we expect client loan demand to remain relatively muted in the third quarter." Stress in office continues and they did raise their reserve "on this portfolio from 9.3% to 9.7% during the quarter to reflect continued stress in the sector. Approximately 6.3% of our office portfolio is currently classified as non-performing compared with 5.5% at March 31st...We expect stress to remain in the office sector and believe that the size of our portfolio is manageable and well reserved, but our position is to be very proactive in identifying and resolving issues in this portfolio."

34)From Ryanair: "Consumers are just a little bit more frugal. People want to get out there, but they're just a bit more cautious in how they're spending their money."

35)From American Express: "We did see some slower growth in certain T&E categories vs the prior quarter, such as in airline and lodging...Obviously, organic spending, we'd like to see a little bit higher, but it is a slower growth economic environment." On the corporate side, "Spending growth from our US small and medium enterprise customers increased a bit sequentially vs last quarter but remained modest."

36)While the yen needed to rally, for the sake of the Japanese citizenry, the violence of the moves, reflecting too large carry trade unwinds, is not good.

37)South Korea said its economy unexpectedly contracted in Q2 from Q1 by .2% vs the estimate of slight growth of .1%. Lower private spending and investment were the main factors.

38)Australia's composite index fell .5 pt to 50.2 with manufacturing staying under 50 at 47.4 and services falling to 50.8 from 51.2.

39)Taiwan disappointed with a June export orders figure up 3.1% y/o/y vs the estimate of up 12.3%. There was a slowdown in exports to Japan (maybe weaker yen having an influence) and to China. Taiwan's economy ministry said "The growth of the global economy will continue to be affected by high interest rates, and risks from US-China trade and geopolitical issues remain, which may inhibit the momentum of global trade growth."

40)There was a notable drop in French business confidence in July, likely influenced by the political mess. The index fell to 94 from 99 and the estimate was for no change. That's the weakest since February 2021.

41)The German business confidence index, the IFO, fell to 87 from 88.6 and the forecast was for a gain to 89. Both the Current Assessment and Expectation components fell m/o/m. The IFO said simply, "Skepticism regarding the coming months has increased considerably. The German economy is stuck in crisis."

42)The July UK CBI industrial orders index weakened to -32 from -18 and vs the estimate of -20. There is optimism though that things will improve from here as the expectations piece of the survey rose to "the strongest in over two years. Firms are looking to increase stock levels to meet expected demand."

43)The July Eurozone PMI fell to 50.1 from 50.9 with manufacturing remained depressed at 45.6 mostly because of weakness in Germany and France. The services side fell to 51.9 from 52.8. S&P Global said, "Is this the summer lull? It feels a bit like it as the Eurozone economy barely moved in July." With respect to prices, "Input prices increased sharply again in July, with the pace of inflation ticking up to a 3 month high. The latest rise was also sharper than the series average. Cost pressures continued to be more pronounced in the service sector than in manufacturing, with services input prices up substantially in the latest survey period. That said, manufacturing cost inflation also picked up and was the fastest for a year and a half."

BY Doug Kass · Jul 26, 2024, 1:44 PM EDT

I am still feeling like crap — taking a nap.

I'll be back later!

BY Doug Kass · Jul 26, 2024, 12:45 PM EDT

I have a visit with a company management until noon today. Radio silence.

BY Doug Kass · Jul 26, 2024, 11:20 AM EDT

From Boockvar:

Headline and core PCE in June were spot on with expectations with one tenth headline and two tenths core m/o/m gains. The y/o/y change was 2.5% and 2.6% for each respectively. As these figures come after CPI, PPI and yesterday's Q2 GDP report which incorporated these numbers, it was hard to deviate much from the estimates. I'll argue again, PCE's heaviest weighting is healthcare and mostly which is determined by Medicare and Medicaid reimbursement rates unlike CPI. Why no one has asked why Powell thinks this is a better gauge of inflation than CPI is beyond me, and where CPI runs usually about 100 bps higher than PCE because of this.

Anyway, June spending rose as expected by .3% m/o/m but May was revised up by 2 tenths so we could get a slight tweak up in the Q2 GDP revision whenever it comes, all else equal. Income though was light relative to the estimates. Combining the two puts the savings rate at 3.4% from 3.5% in May and that is the lowest since November 2022.

With respect to the consumer, that savings rate drop points to little cushion and helps to explain why so many are price conscious and budget seeking, as we've heard countless times. On the other hand, those that have savings are certainly enjoying getting paid well on it via higher interest rates. Ironically, many who have that savings don't want the Fed to be cutting short term rates.

While the Fed has the data to cut rates next week, the market has already fully priced in two cuts this year already so it really doesn't matter. The bottom line from here is whether we are going to see a rate tweaking cycle or a real rate cutting cycle, where the former would be driven by both moderating growth and inflation but with each still holding up or the latter which would be because the unemployment rate continues to inflect higher and disinflation really catches on. I expect a complicated middle where growth continues to slow, unemployment moves higher, and inflation remains stuck above 2%.

Core PCE y/o/y

Savings Rate

BY Doug Kass · Jul 26, 2024, 11:00 AM EDT

Because everything now is “AI,” CEOs think it is important, due to all the buzz.

In many cases investors expect an AI story from companies they invest in. Just like they expected a green story or whatever other story was trendy a few years ago. But the employees who are actually using it indicate it lowers productivity. Eventually executives will figure out they have spent a lot of money and are getting a negative return. Frankly, the same for those providing the service (MSFT, Chat GPT, etc), and losing massive amounts of money doing it.

Right now, the only ones making money off of this are those selling the plumbing (infrastructure). Everyone else loses money and productivity.

Look at this one from Forbes:

77% Of Employees Report AI Has Increased Workloads And Hampered Productivity, Study Finds

The new global study, in partnership with The Upwork Research Institute, interviewed 2,500 global C-suite executives, full-time employees and freelancers. Results show that the optimistic expectations about AI's impact are not aligning with the reality faced by many employees. The study identifies a disconnect between the high expectations of managers and the actual experiences of employees using AI.

Despite 96% of C-suite executives expecting AI to boost productivity, the study reveals that, 77% of employees using AI say it has added to their workload and created challenges in achieving the expected productivity gains. Not only is AI increasing the workloads of full-time employees, it’s hampering productivity and contributing to employee burnout.

To add insult to injury, nearly half (47%) of employees using AI say they don’t know how to achieve the expected productivity gains their employers expect and 40% feel their company is asking too much of them when it comes to AI. ..

BY Doug Kass · Jul 26, 2024, 10:30 AM EDT

From Peter Boockvar:

Yea, about a 2% growth economy ytd but we must continue to look under the hood

I read an interesting stat in yesterday's FT citing JP Morgan, "Vehicle prices have accounted for 79% of the decline in core goods prices over the past year." I knew it was a chunk but not that much.

Jumping right in to the earnings calls and we continue to see a highly mixed economy. Looking at the GDP headline read, averaging about 2% this year, at face value just doesn't give much information of what is going on under the hood.

From Royal Caribbean, where demand is still pretty solid but where the stock sold off because of moderating yield growth expectations for the back half of the year:

"The demand and pricing environment remained very strong since the last earnings calls. Booking volumes were higher than the corresponding period in 2023 and at record pricing levels. The company continues to be in a record booked position for 2024 sailings. Consumer spending onboard, as well as pre-cruise purchases, continue to significantly exceed 2023 levels driven by greater participation at higher prices."

"The further increase in yield expectations for the year is the result of higher pricing and onboard revenue expectations across key products, with particular strength in European and Alaskan itineraries."

"We continue to see very positive sentiment from our customers bolstered by a resilient economy, low unemployment, stabilizing inflation, and record high household net worth."

And, "our research suggests that consumers are spending more on travel than any other leisure category, and that they intend to increase their travel spend in the next 12 months." And the boomers are a big help as "Based on our research, retirees take 50% more vacation than non-retirees. The baby boomer generation also holds 50% of the $156 trillion of US wealth, and they are expected not only to spend more on travel, but also to transfer $72 trillion of their wealth to other generations over the next two decades, including traveling together."

Speaking of boats, but much smaller ones, this from Brunswick, the boat maker:

"With high interest rates continuing to pressure consumer budgets and suppress discretionary spending, the introduction of new model year products at the beginning of the important month of June did not catalyze boat purchases as we had anticipated, and our 2nd quarter results were slightly below expectations."

"Without strong peak season momentum, the continued slower retail sales, combined with higher levels of discounting and carrying costs, have increased pressure on dealer and channel partner profit margins, resulting in ongoing conservative wholesale ordering patterns, even for new model year products. In turn, this is causing OEM's to maintain lower boat production rates through the main selling season."

And from a retail seller of boats, Marine Max:

They somehow drove 4% same store sales growth and said "With aggressive marketing and promotions, we were able to generate an increase in boat revenue, complemented by nice contributions from our super yacht's group, marinas and finance and insurance business."

"At the industry level, the aggressive promotional environment continued in Q3, amid elevated inventories, interest rates, and persistent concerns about inflation. The weakened consumer sentiment was evident in US powerboat registrations...While the premium end of the market is performing better than the value segment, and as we have said all year, it's not without its challenges."

Texas Roadhouse is feeling good about their business:

"there has been significant discussion within the restaurant industry concerning the health of the consumer as well as the increased focus on promotions and discounting from others in the industry. Through the first half of the year, we have not seen a measurable impact on our overall business from these issues. Our guests continue to recognize the quality and value we offer and do not appear to be changing their dining habits."

"In addition to strong traffic growth, we also experienced encouraging mix trends within our check."

To a question about them seeing any trade down dynamics and any differences among income cohorts, "I think we have people trading up to us, trading down to us, trading across to us. So we're pleased with the guests' decision to visit with us. We're not seeing any degradation in what they are ordering as seen by kind of our flat mix trends right now."

On inflation, "At this time, we are updating our full year commodity inflation guidance to approximately 2%." On the labor side, "Our guidance remains at 4% to 5% wage and other labor inflation for the full year." I'll add, that remains well above pre Covid trends.

From Nestle:

"we're still seeing significant value-seeking behavior on the part of the consumer. There's stress, in particular, at the lower end of the income scale in North America, but also in select other geographies. And so people are value-seeking, and hence, our promotional intensity has been particularly strong."

From Deckers Outdoor where HOKA continues to crush it with 30% y/o/y revenue growth and UGG saw 14% growth:

"HOKA performance driven by the brand's compelling product assortment, including new launches, which experienced strong demand across the brand's global marketplace."

With UGG, "The UGG brand's more focused assortment of relevant franchises is driving the majority of consumer demand, which contributed to lower promotion as compared to prior first quarters, where the DTC business has historically been more influenced by end-of-season discounting on seasonal colors."

They did though acknowledge "a very dynamic consumer environment." 'Dynamic' has been code word for uneven and they forecast 10% revenue growth for fiscal year 2025.

Hermes referred to its quarter "against a more complex global economic and political backdrop" but seemed to outperform many of its peers. Sales rose 15% "driven by our loyal and new customer base. All regions recorded double digit growth and the division recorded good progress in a more complex environment."

From Ryder:

"we continue to see freight conditions that remain weak and the timing of the cycle inflection remains uncertain."

With respect to their earnings guidance range, "The high end of our forecast range continues to assume a gradual recovery in rental and used vehicle sales, although later in the year, and the bottom end reflects ongoing weak conditions for these businesses."

"The extended freight downturn and economic uncertainty have been causing some customers and prospects in lease Dedicated and Supply Chain to delay decisions or downsize their fleets. These near term contractual sales headwinds are consistent with where we are in the cycle and the current economic environment."

Dow Chemical talked about its "sequential top and bottom line growth, as well as the 3rd consecutive quarter of y/o/y volume growth...despite a slower than expected global macroeconomic recovery, particularly in areas like building and construction and consumer durables."

"Looking across our four market verticals, packaging demand is seeing global growth, primarily in the US and Canada as the industry experiences robust domestic and export demand for polyethylene. In Europe, soft demand across the value chain is reflected in manufacturing PMI levels, which despite stabilizing remains in contractionary territory. And in Asia, packaging demand has remained steady, but the region has been impacted by poor congestion and rising transportation costs."

"Infrastructure demand primarily residential construction continues to be soft across most regions."

"Consumer spending has shown resilience in most regions, except Europe where consumer confidence remained negative in July. In the US, retail sales are up 2.3% year to date through June, but furniture and bedding sales remain low. In China, retail sales increased 2% y/o/y in June, but marked the first month of deceleration since July 2023. And in mobility, China auto production was down 2.1% y/o/y in June." Auto sales fell in the US in June too after rising in May.

Masco, selling everything from faucets to kitchen cabinets, said "As uncertainty within the broader macroeconomic environment has continued, we are tempering our expectations for sales in the 2nd half of the year from up low single digits to roughly flat, leaving our full year sales within our previously guided range of plus or minus low single digits."

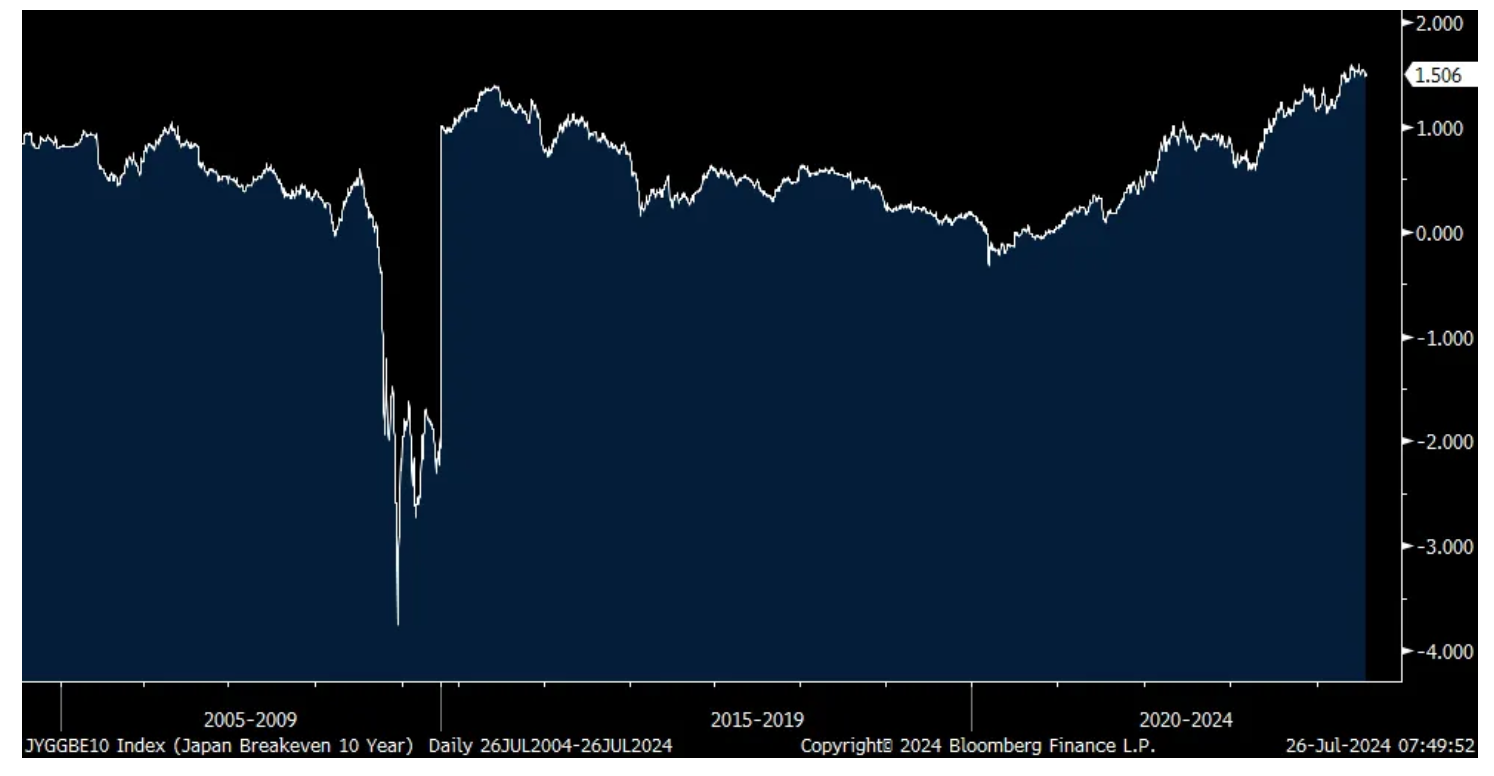

Turning overseas, Tokyo reported July CPI and it rose 2.2% y/o/y headline vs 2.3% in June and one tenth less than expected. The core/core rate moderated to 1.5% y/o/y from 1.8% in June and that too was one tenth under the estimate. Part of the deceleration is the easy comp as July 2023 saw a 4% core/core rate increase. While the numbers were around expectations, the 10 yr inflation breakeven rose 2.3 bps to 1.51%, a one week high and still hovering around multi decade highs. The 10 yr JGB yield was up 1 bp to 1.07% and after a wild few weeks, the yen is weaker by .5%.

Japan 10 yr Inflation Breakeven

BY Doug Kass · Jul 26, 2024, 10:00 AM EDT

Goldman Sachs on oil prices:

Oil Analyst: Trump Scenarios: Upside Risk to Volatility; Downside Risk to Prices

25 July 2024 | 7:09PM EDT

■ We still forecast a $75-90 range for Brent given our base cases of trend-like growth in GDP and oil demand (under steady US policies), and OPEC+ market balancing. We analyze the risks to this call from a potential second Trump term.

■ No quick US policy supply boost. The next US President will have limited tools to significantly boost 2025 oil supply. Regulatory easing may only significantly boost US long run supply, and SPR stocks are low. While OPEC+ decisions and US sanctions can in principle shift international supply, we don't expect a large US policy driven supply boost because 1) OPEC+ is independent, 2) sanctions don't significantly constrain Russia volumes, and 3) Iran supply is already high.

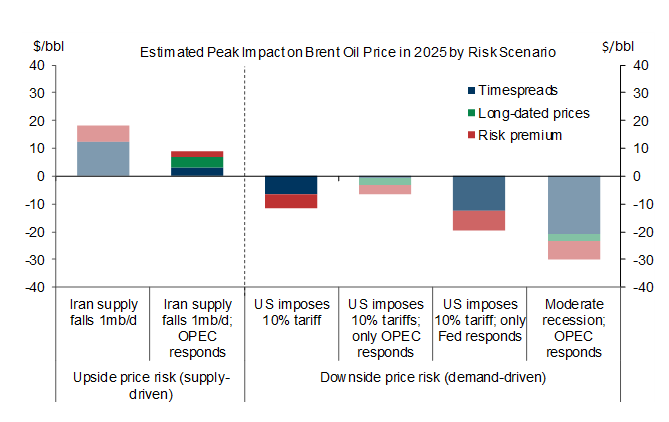

■ Downside to Iran supply. The sanctions-driven drop in Iran supply under Trump in 2018 suggests that the risks to our flat Iran 2025 supply assumption skew to the downside. In a scenario where Iran supply drops 1mb/d, other OPEC+ producers would likely gradually fill in the shortfall, which would limit the peak boost to oil prices from reduced inventories and spare capacity to $9/bbl.

■ Downside to demand from tariffs. While there is a lot of uncertainty about trade policy, tariffs on US crude imports seem unlikely. We do estimate a peak hit to 2025 oil prices of $11/bbl as a result of weaker GDP and oil demand in a scenario where the US imposes an across-the-board tariff of 10% on goods imports. Our estimated tariffs hit to oil prices rises to $19/bbl in a scenario where the Fed delays cut beyond 2025 due to higher core inflation (with Brent at $62/bbl in 2025Q4 vs. our $81 forecast), but moderates to $6/bbl if the Fed doesn't delay cuts and OPEC+ reverses its announced supply increases.

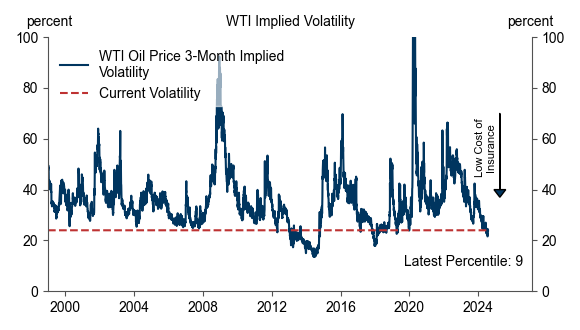

■ Upside risk to volatility. While the ongoing observed drop in oil price volatility was always a key implication of our OPEC range framework, sizable two-sided US policy risks could trigger a pick up in volatility from record lows.

■ Downside risk to prices. Downside risks from US policy strengthen our view that the risks to our 75-90 range skew to the downside given high spare capacity, and somewhat looser summer oil nowcasts than our balance. Given the drop in implied volatility to percentile 9 over the last 25 years, put options are now attractively priced to hedge 2025 price downside.

Hedging Downside Risk to 2025 Oil Prices Screens Attractive as 1) Risks to our $75-90 Range Forecast for Brent Skew to the Downside...

The saturation of the bars rises with our subjective probability for each risk scenario.

Source: Goldman Sachs Global Investment Research

... and 2) Crude Oil Price Implied Volatility Has Dropped to Percentile 9 Over the Last 25 Years

BY Doug Kass · Jul 26, 2024, 9:43 AM EDT

Chart as of 8:34 a.m. ET:

BY Doug Kass · Jul 26, 2024, 9:26 AM EDT

As of 8:52 a.m. ET:

BY Doug Kass · Jul 26, 2024, 9:13 AM EDT

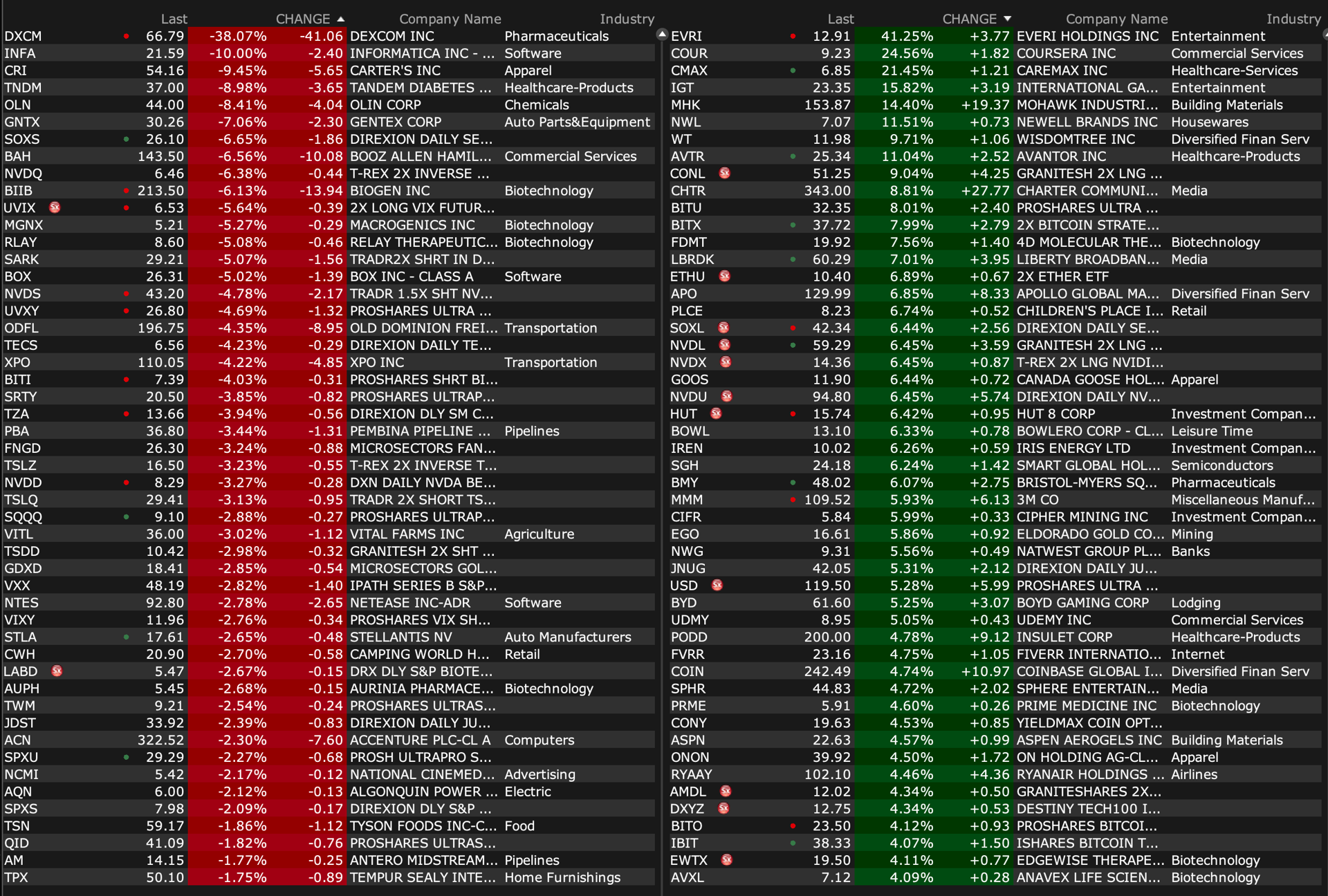

U.S. Select premarket movers as of 8:29 a.m. ET:

-BFI +69% (reaches legal settlement agreement with Lion Point Capital, LP)

-EVRI +40% (IGT's Gaming and Digital Business and Everi to be acquired simultaneously by Apollo Funds in all-cash transaction that values combined businesses at ~$6.3B)

-COUR +26% (earnings, guidance)

-IGT +17% (IGT's Gaming and Digital Business and Everi to be acquired simultaneously by Apollo Funds in all-cash transaction that values combined businesses at ~$6.3B)

-MHK +13% (earnings, guidance)

-DECK +12% (earnings, guidance)

-APO +6.9% (IGT's Gaming and Digital Business and Everi to be acquired simultaneously by Apollo Funds in all-cash transaction that values combined businesses at ~$6.3B)

-NSC +6.8% (earnings, guidance)

-FIX +6.5% (earnings)

-BYD +5.9% (earnings)

-BMY +5.2% (earnings, guidance)

-PODD +4.8% (reports prelim Q2 Rev, raises FY24 guidance)

-AVTR +4.5% (earnings, guidance)

-BKR +2.9% (guides Q3, raises FY guidance)

-SKX +2.8% (earnings, guidance)

-VLTO +2.7% (earnings, guidance)

-DXCM -37% (earnings, guidance)

-POAI -24% (announces exercise of warrants for $1.3M gross proceeds)

-ZYXI -24% (earnings, guidance)

-URG -18% (prices 57.2M shares at $1.05/shr)

-SAIA -15% (earnings, guidance)

-CRI -9.5% (earnings, guidance)

-B -6.2% (earnings, guidance)

-GNTX -6.2% (earnings, guidance)

BY Doug Kass · Jul 26, 2024, 9:01 AM EDT

On the economic release I re-shorted SPY at $543.63 and QQQ at $464.15 common.

BY Doug Kass · Jul 26, 2024, 8:40 AM EDT

* I think the thing AI is best at is separating investors from their money.

Everything is AI?

Beware the buzzword.

Yesterday my friend relayed that he made investments in three different startups, that are now AI. Same software they had 2-3 years ago when he made the investments, but now it is “AI.” Interesting.

Handset AI? It is really just typical evolutionary photo editing features, and circle text to web search. Nothing exciting. Nothing having to do with AI. But that is what they call it. AI. It has been on Google GOOGL and Samsung handsets for about two years now, and nobody really cares. When Apple AAPL rolls out with theirs, once again they will be late, and it won’t be as good as what is out there, but it will be hyped as the most innovative thing ever.

Video image and audio generation, not a new idea, and just the typical evolution of technology, but now it is AI. It was around before ChatGPT, and nobody called it AI.

Below is just the typical evolution of normal data analytic and other software. Same thing. Everything is being called AI. None of it thinks. None of it is a new idea. All of it is evolutionary, and not revolutionary. Yet now it is all “AI”?

Traditional dealership advertising focuses on popular vehicle models but neglects a lot of inventory. Lotlinx, an AI-driven automotive inventory management company, says 80% of dealership ad budgets target just 26% of inventory, leaving 56% unseen.

One application for A.I? Turning dealership data into actionable insights and automatically optimizing that online ad spend. Creating and tweaking ad campaigns without lifting a finger… that will happen soon (and not just with dealerships, but all businesses).

I think the thing AI is best at is separating investors from their money.

Here is another one. More AI. If you can even figure out what all the BS in here even means:

I still think most of the stuff that works, and adds value, is actually just machine learning, continues at its evolutionary pace, and lives in the background. Most of what is being hyped does not work well (gen AI) and is a bunch of baloney — at least for now.

BY Doug Kass · Jul 26, 2024, 8:20 AM EDT

BY Doug Kass · Jul 26, 2024, 7:44 AM EDT

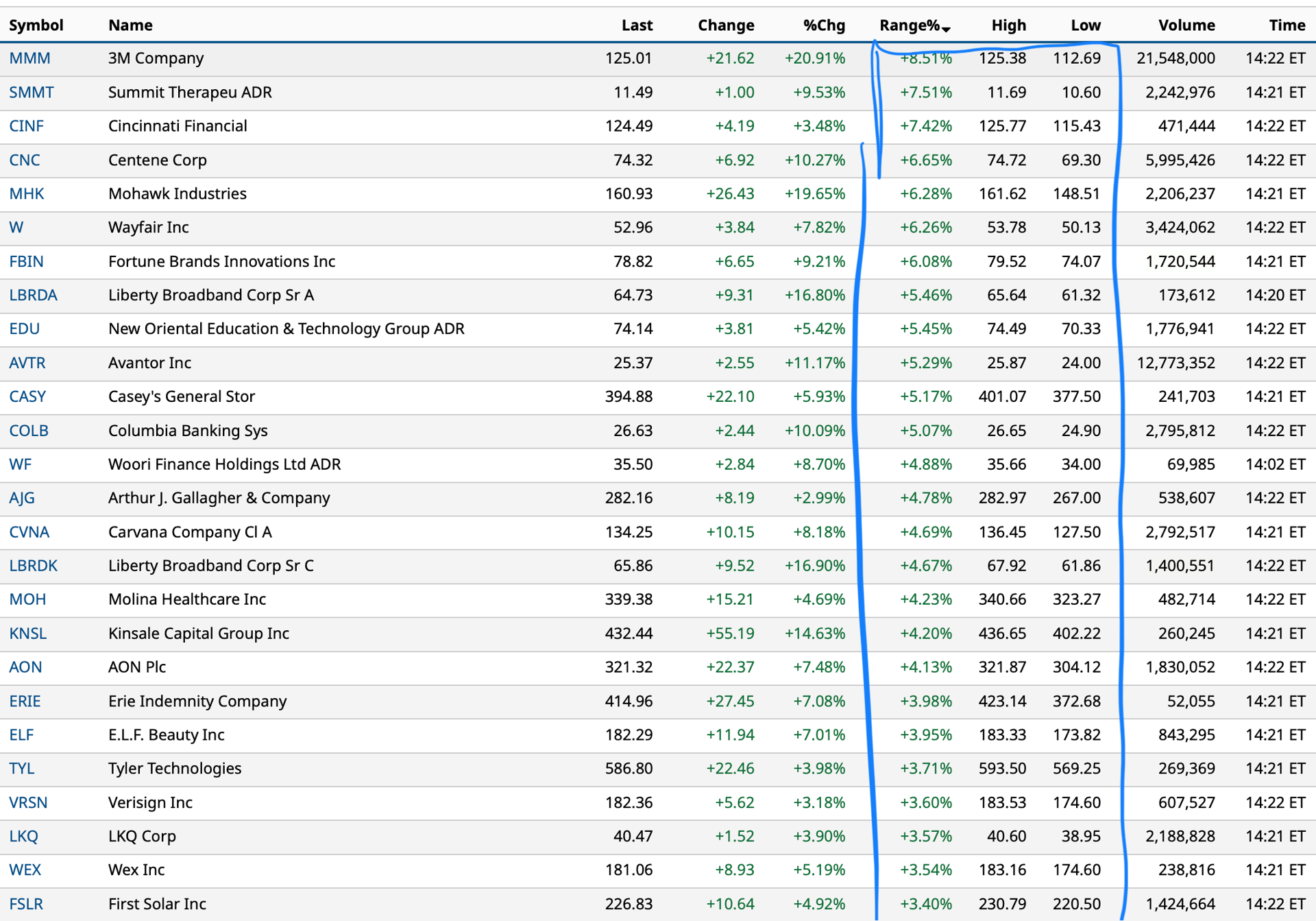

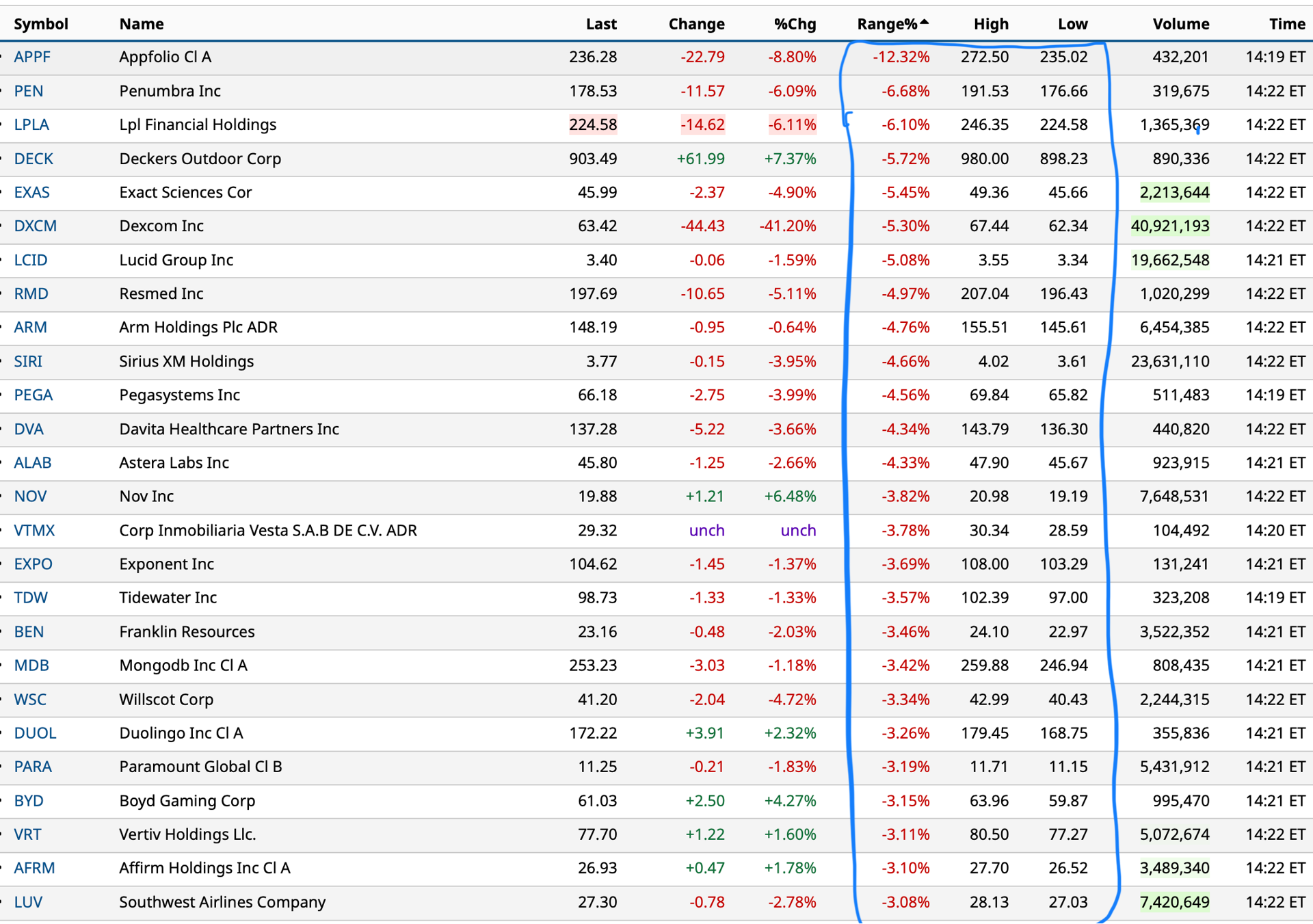

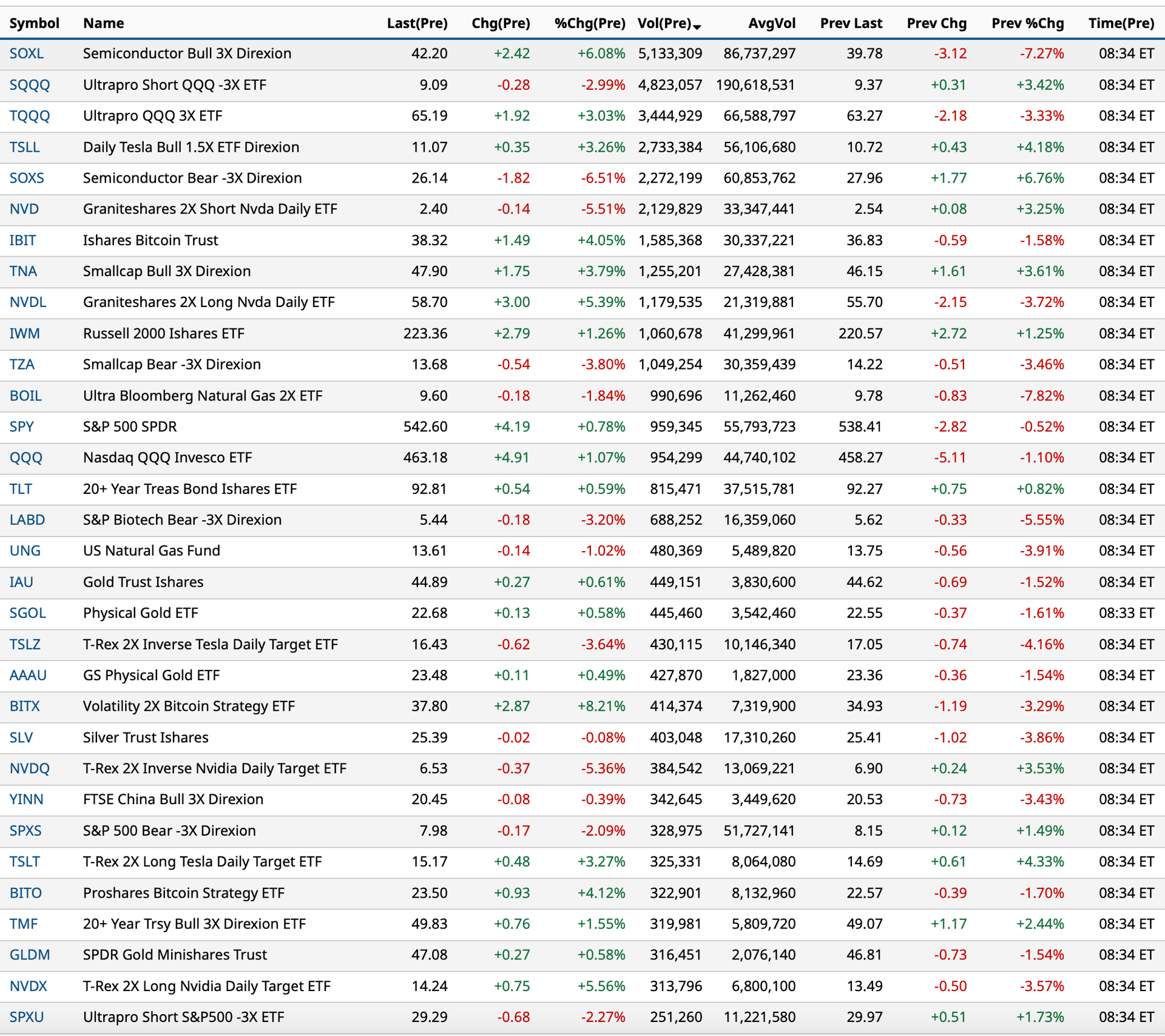

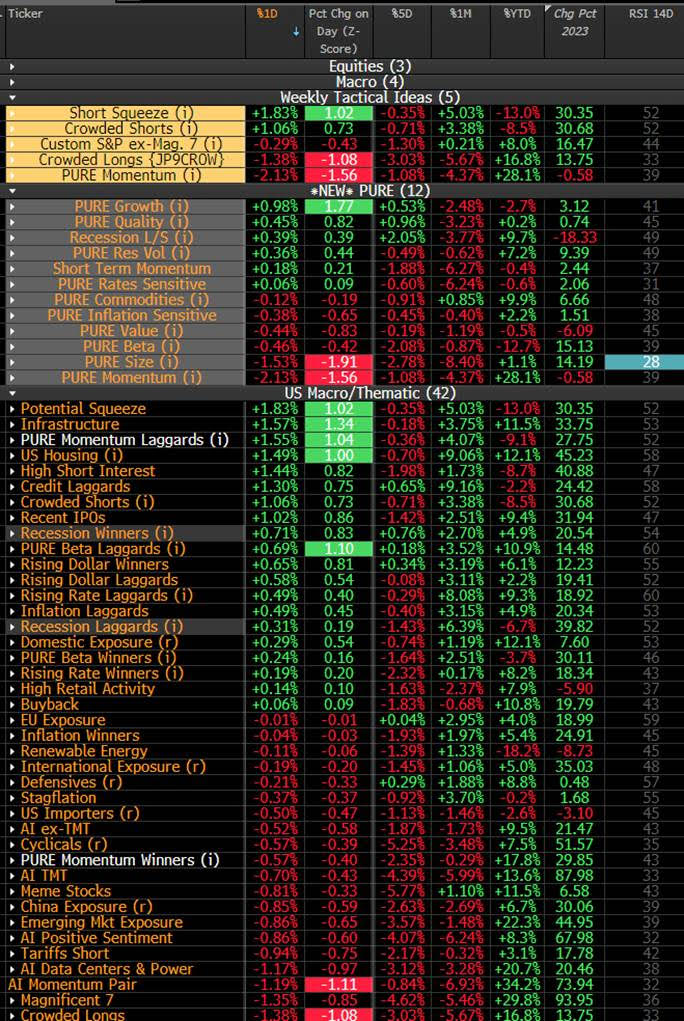

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Jul 26, 2024, 7:30 AM EDT

From JPMorgan:

US: Futs are higher led by RTY. Pre-mkt, MegaCap Tech are higher: NVDA +2.4%, META +2.0%, AMZN +1.2%, AAPL +97bp, GOOG/L +72bp. Bond yields are mostly unchanged. USD is flat. Commodities are mixed: oil is lower while base metals/gold are higher. Today the key macro focus will be July PCE: Feroli expects core PCE to print 2.6% vs. 2.5% survey vs. 2.6% prior.

and...

EQUITY AND MACRO NARRATIVE: Equities appear to reverse some of yesterday’s loss this morning, despite a still quiet macro calendar today. Manish Sinha from D1 tells us that historical comparison shows that the current rotation is close to the 95th percentile (his full note is below). Are we close to the end of the rotation? The main market focus is still on earnings: next week, ~40% of the SPX stocks will report, along with the rest of Mag 7 (ex-NVDA) results. Supportive earnings, along with clearer guidance from the FOMC, could help the equities sentiment. Today, we will receive the July PCE: Feroli expects core PCE to print 2.6% vs. 2.5% survey vs. 2.6% prior.

BY Doug Kass · Jul 26, 2024, 7:12 AM EDT

* Slugflation equals prickly inflation and slowing economic growth...

BY Doug Kass · Jul 26, 2024, 7:00 AM EDT

* Some editorial comments about hubris and full dependency on charts this morning.

* I previously warned that the plethora of technical analysts quoted in 'Charting the Technicals' have been confidentally bullish into the recent market decline.

* To me, though, the only certainty is the lack of certainty — as Grandma Koufax often reminded me ("to be aware of the Cossacks").

* A contrarian, independent and fundamental view is often important to consider and sometimes to implement.

* That is why, to me, a sense of fundamental value is so important (vs. a blind eye towards price momentum — which is the foreplay of machines and algos).

* In looking at the charts I find extreme readings in RSI and in the S&P Short Range Oscillator as guiding technical stars to be superimposed with a fundamental understanding of value in the Indices, sectors and individual stocks.

“The best plan is to profit by the folly of others.”

- Pliney The Elder

Bonus — Here are some great links:

BY Doug Kass · Jul 26, 2024, 6:45 AM EDT

Yesterday I suggested that the Oscillator would begin to move back to neutral (from overbought):

The S&P Short Range Oscillator has declined from a deep overbought of over 8% last week to 3.15% last night (from 6.35% the night before).

Given that this is a 30-day moving average, I expect the number to continue to drop this week.

Position: None

BY DOUG KASS JUL 25, 2024 5:53 AM EDT

Indeed, the Oscillator moved from 3.15% to 1.94% on Thursday evening.

That is dramatically lower than the deep overbought of 8.28% on July 16.

BY Doug Kass · Jul 26, 2024, 6:32 AM EDT

From my friends at Miller Tabak:

Thursday, July 25, 2024

For many months, we have predicted that mid-2024 would bring falling inflation and relatively slow U.S economic growth. The 2Q2024 GDP growth rate of 2.8% defies our latter prediction. This strong growth is just not due to the noisiest components of GDP; inventories added 0.8% to growth but net exports subtracted 0.7%. Nevertheless, we expect this figure to be an outlier with growth returning to 1.5% for the rest of 2024.

Higher growth is mostly due to consumption, which grew at 2.3%, adding 1.5% to GDP, Households also moved back towards goods, a sector that contracted in the first quarter. We suspect that this is partly a response to high-profile price reductions. It is good news in the short-term, another signal that the U.S. is not at much risk of recession in the next year (more on this later). Longer-term, however, it is concerning. This rate of consumption growth is unsustainable and will accelerate the deterioration in household balance sheets that may eventually make the U.S. ripe for recession. We expect consumption growth to slow to the 1.0%-1.5% range for the rest of the year.

One puzzle in the GDP report is investment, which is especially interest rate sensitive. Housing, which for now remains the best leading economic indicator, contracted by 1.4% under the weight of higher mortgage rates. Non-residential investment, which includes equipment and intellectual property, grew at 5.3%. Non-residential investment is more forward looking than housing and continued growth likely requires that the FOMC cut rates as we, and markets, expect.

Although we do not expect GDP growth above 2% to last, the FOMC will rightly see the data as evidence of the soft landing that we have predicted since rate hikes began in 2022. With inflation falling, the Fed is still on track to begin a cautious rate cut cycle in September. For next week’s July meeting, our focus is on whether the Fed lays the groundwork for a fall rate cut. It will be hawkish if the FOMC does not change its current language that “the Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.” We expect the FOMC to soften this language to signal a September rate cut. Our baseline case is language like “recent data show that inflation is moving closer to the Committee’s 2% target. If upcoming inflation data show continued progress, the Committee expects it will soon be appropriate to lower the target range for the Federal Funds rate.”

BY Doug Kass · Jul 26, 2024, 6:22 AM EDT

Wolf Street howls about economically drunken sailors.

BY Doug Kass · Jul 26, 2024, 6:12 AM EDT

* Brokedown palace...

Going to leave this broke-down palace

On my hands and my knees I will roll, roll, roll

Make myself a bed by the waterside

In my time, in my time, I will roll, roll, roll

— Grateful Dead, Brokedown Palace

Down -40 handles in the premarket. 9:15 AM

Up +25 handles soon thereafter. 10:15 AM

Flat. 10:40 AM

Up +60 handles. 12:15 PM

Flat. 1:40 PM

Up +30. 2:25 PM

Down -29 handles at the close

That was the intraday action of the S&P futures on Thursday.

Count up the price changes on an intraday basis — it was mind boggling.

No rhyme, no reason — just machines and algos.

Great for opportunistic traders — but not so great for the buy and hold crowd!!!

I saw this coming eight days ago:

The market's rotation over the last few weeks has been as extreme and as violent as I can ever recall. As an example, I noted yesterday that the Russell Index is a nearly unprecdented 4.5 standard deviations above the 50-day moving average.

And so has hourly/intraday volatility increased.

The violence and lack of predictability of the moves are unplayable for most.

If you do "play" I would strongly recommend to consider your portfolio's VAR ("value at risk") — and reduce your trading positions in size to accommodate the above volatility and uncertainty.

I am taking my own advice.

Position: None

BY DOUG KASS JUL 18, 2024 8:25 AM EDT

BY Doug Kass · Jul 26, 2024, 5:57 AM EDT

BY Doug Kass · Jul 26, 2024, 5:47 AM EDT

86% upside day at 2:15.