SPY, QQQ Profits

S&P cash retreated -17 handles from highs of the move so I covered my short SPY and QQQ calls for a quick profit.

No Index positions on into the Mr. Softee print after the close.

BY Doug Kass · Apr 25, 2024, 3:10 PM EDT

S&P cash retreated -17 handles from highs of the move so I covered my short SPY and QQQ calls for a quick profit.

No Index positions on into the Mr. Softee print after the close.

BY Doug Kass · Apr 25, 2024, 3:10 PM EDT

I am heading out early for family stuff.

I will report back early tomorrow morning on the after hours EPS releases.

Enjoy the evening.

Be safe.

BY Doug Kass · Apr 25, 2024, 3:00 PM EDT

Housekeeping item.

After a good EPS report I have cut back St. Joe JOE to tag ends at $58.10.

Persistently high interest rates are the reason for the continued reduction in this long term holding.

My guess is I have a chance to buy back in the low $50s.

BY Doug Kass · Apr 25, 2024, 2:45 PM EDT

JP Morgan cuts Blackstone Mortgage Trust BXMT price target to $17.50.

BY Doug Kass · Apr 25, 2024, 2:30 PM EDT

With S&P cash rallying to only -20 handles. I am back shorting May in the money SPY calls (short).

Scaling in.

Same way on QQQ calls - shorted.

BY Doug Kass · Apr 25, 2024, 2:15 PM EDT

BY Doug Kass · Apr 25, 2024, 2:05 PM EDT

The S&P Short Range Oscillator is less oversold now - falling from -3.28% to 1.66%.

BY Doug Kass · Apr 25, 2024, 1:55 PM EDT

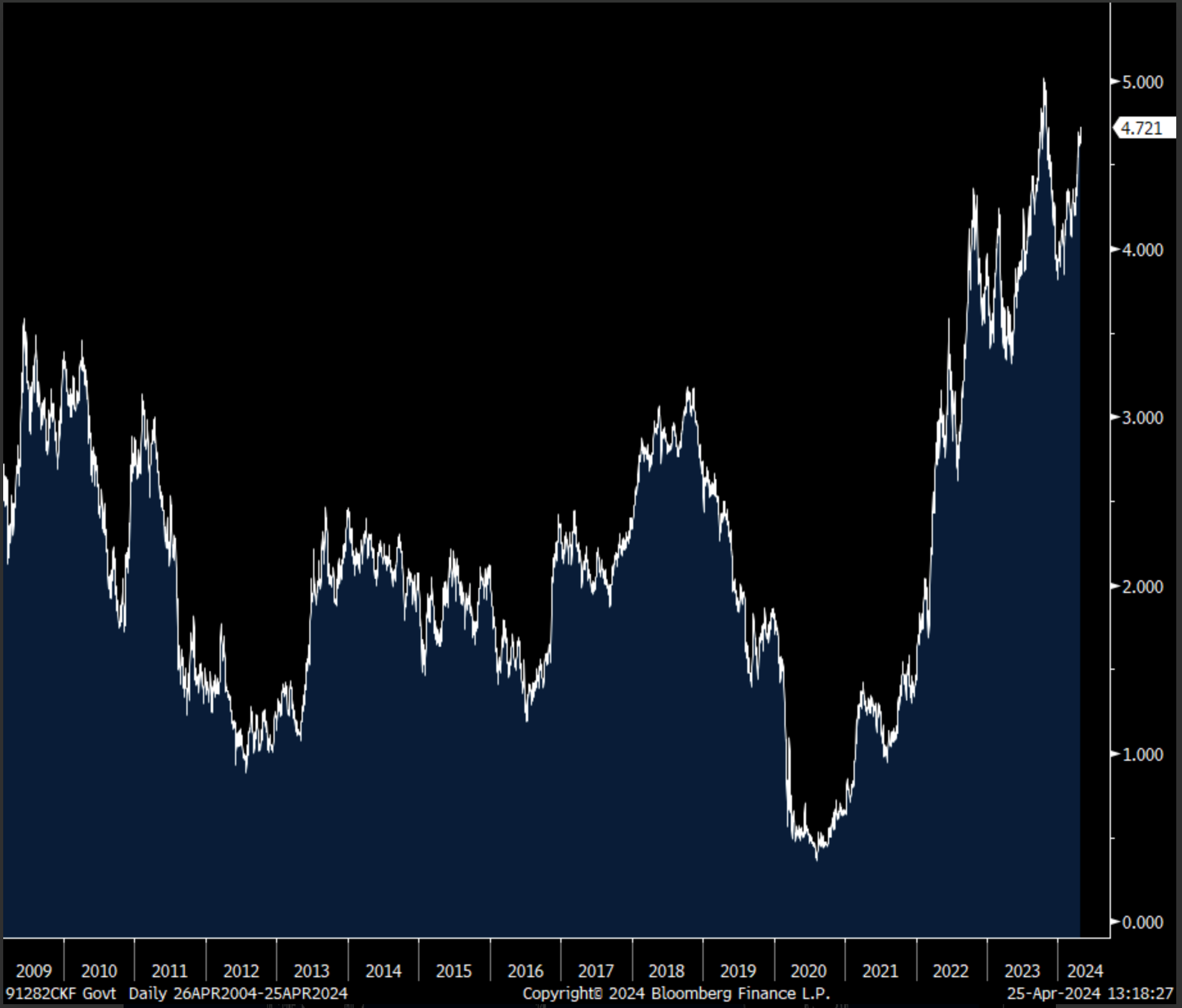

The 7 yr note auction finishes a blah week of auctions. The 2 yr was mixed, the 5 yr was soft and the 7 yr was mediocre. The yield of 4.716% was right in line with the when issued pricing but the bid to cover of 2.48 was below the one year average of 2.56. The combined direct and indirect bidders totaled 86% which is in line with the average over the last 12 months.

Bottom line, all of these auctions come in record sizes and while I do think it’s important to see how the supply is absorbed on the day of sale, the market impact is never really more than one day. Treasuries are more focused today on the GDP figure, the internals and the hotter than expected PCE deflator, along with still subdued initial jobless claims. I still expect a retest of 5% on the 10 yr yield this year.

With regards to rate cut odds, a full 100% cut is not priced in until the day after the presidential election.

7 yr Yield

BY Doug Kass · Apr 25, 2024, 1:45 PM EDT

From yesterday:

* All weather? No, stormy weather may lie ahead...

Market structure remains a key concern of mine - though you will rarely hear a discussion of it in the business media.

The market is dominated by products and strategies that worship at the altar of price momentum. Though they are termed "passive" - they operate actively by chasing momentum up and down.

They know nothing about value but everything about price - and they are all on the same side of the boat.

Quants represent the tail that wags the market dog. It is an unhealthy condition that can lead to unexpected market dislocations - much like portfolio insurance did in October, 1987.

Over the last few years we have had some wild intraday swings As an example, today META was +$15 this morning and is now -$10 on no news.

I am fearful that something worse lies ahead.

Just when investors have gotten all bulled up.

BY Doug Kass · Apr 25, 2024, 1:30 PM EDT

In my opener this morning, I suggested that the CapEx increase at META should buoy NVDA and semis.

Indeed, NVDA and semis are green in a sea of red.

BY Doug Kass · Apr 25, 2024, 12:52 PM EDT

BY Doug Kass · Apr 25, 2024, 12:30 PM EDT

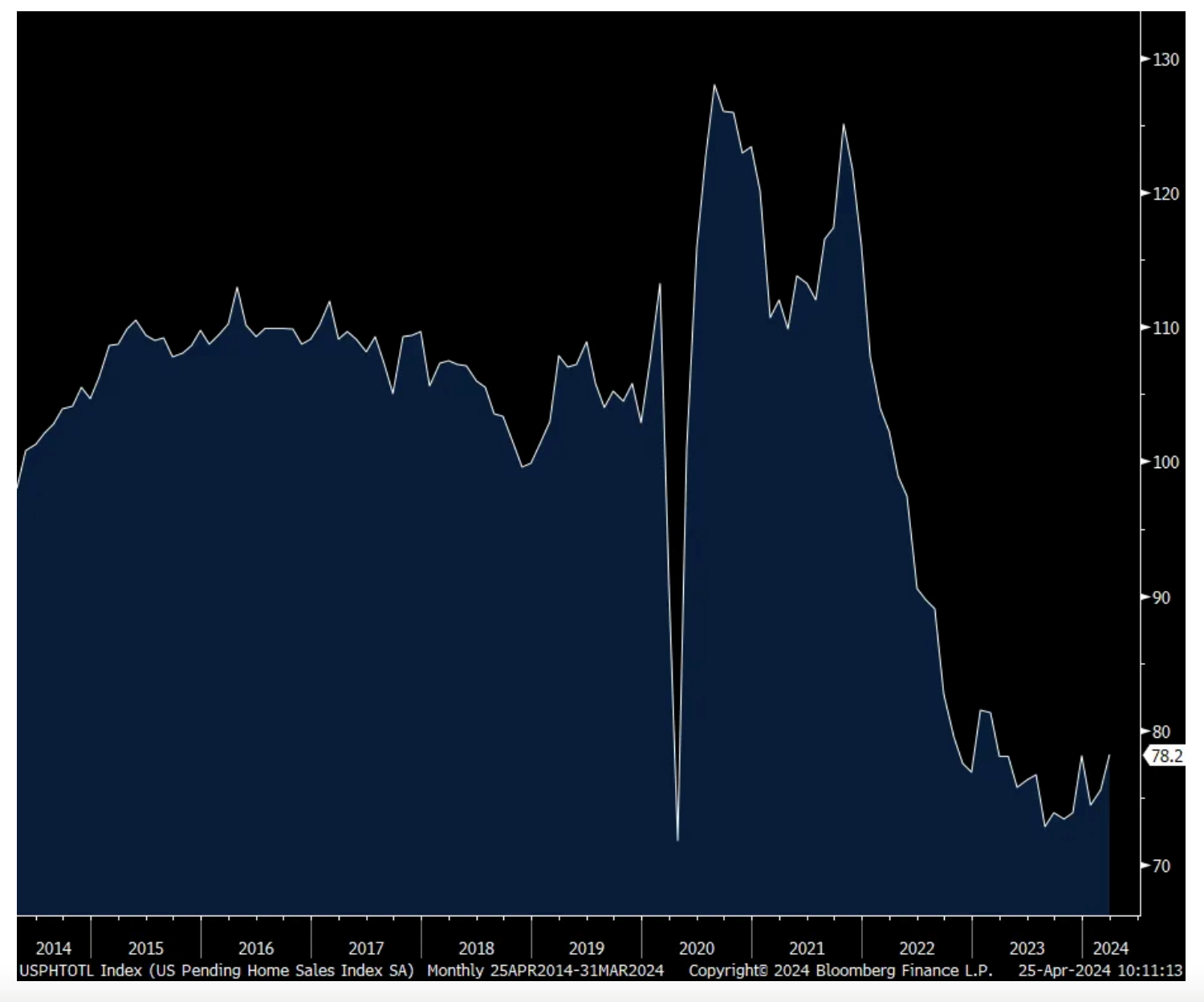

Pending home sales in March rose by 3.4% m/o/m, above the forecast of up .4%. Three out of the 4 national regions saw a rise but as seen in the chart, we’re sort of bouncing along the bottom both due to limited inventory of existing homes and high prices along with a 7%+ mortgage rate which makes it tough for many first time buyers.

The NAR said the index level of 78.2 is the highest since February 2023 but “still remains in a fairly narrow range over the last 12 months without a measurable breakout. Meaningful gains will only occur with declining mortgage rates and rising inventory.”

Bottom line, we’re well aware of the bizarre housing market with a near 30 yr low in the pace of existing home transactions but with a better situation for new homes that are needed to fill the inventory vacuum.

Pending Home Sales

BY Doug Kass · Apr 25, 2024, 11:55 AM EDT

I initiated a long investment in DraftKings DKNG this morning - on weakness.

More next week on my return to Florida.

BY Doug Kass · Apr 25, 2024, 11:40 AM EDT

Reading61

Roche mentioned VKTX, wow.

BY Doug Kass · Apr 25, 2024, 11:28 AM EDT

If cannabis stocks fall from here I am prepared to super size the position.

My conviction is growing that weed will be leadership in 2024 for a host of reasons mentioned in my Diary.

I might be wrong, so do your own work!

BY Doug Kass · Apr 25, 2024, 10:45 AM EDT

BY Doug Kass · Apr 25, 2024, 10:30 AM EDT

Apropos to my previous comments, VKTX is +$3 in a sea of red.

BY Doug Kass · Apr 25, 2024, 10:20 AM EDT

How many times have you heard me say that the economy seems to me - based on all the work I do, including a voracious read of earnings conference calls - more like a 1.5% type growth rate and that it is much more mixed than the consensus of it being ‘strong’ and something around 2.5%?

Q1 GDP grew by 1.6% vs. the estimate of 2.5% with a particular miss with personal spending which was up 2.5% q/o/q annualized rather than the 3% that was estimated. Spending on services added 187 bps to GDP but there was no contribution from spending on goods. Services spend was led by healthcare and ‘financial services and insurance.’

On the investment side, residential construction added 52 bps while commercial structures added nothing. Spending on equipment added 10 bps and intellectual property spend which includes R&D and software added 29 bps with a particular contribution from software spend as R&D investment was flattish. Inventories were a drag of 35 bps.

Trade was a drag of 86 bps to GDP with all of that due to imports (the quirk of imports rising, raising the trade deficit, and lowering the GDP calculation) as exports added 10 bps. Government spending on the state and local side contributed 22 bps to growth while federal was little changed q/o/q.

The price deflator of 3.1% was about was estimated with core PCE up 3.7% q/o/q which is likely what Treasuries are keying off with the rise in yields as the 10 yr yield is back to 4.70%.

Bottom line, I’ll say again, there are so many cross currents rolling thru the US economy with a lot of pros and cons that ultimately lead to a mixed economy and one that resembles about 1.5% growth which is where I think Q2 is shaping up to be as well.

The claims data too could be lifting yields. Initial claims remained low at 207k, 8k under the estimate and down from 212k last week. Continuing claims, delayed by a week, fell back under 1.8mm at 1.781mm.

The bottom line here remains the same.

BY Doug Kass · Apr 25, 2024, 10:10 AM EDT

* The momentum movie is now in reverse...

Usually I would be picking here on weakness but I am influenced by market structure concerns.

The movie (momentum) is now in reverse as a new regime of volatility takes hold.

Outsized cash reserves seem prudent especially against equity-like opportunities with little volatility and downside risk in fixed income.

BY Doug Kass · Apr 25, 2024, 9:59 AM EDT

Aggressively adding to MSOS at $8.66.

BY Doug Kass · Apr 25, 2024, 9:38 AM EDT

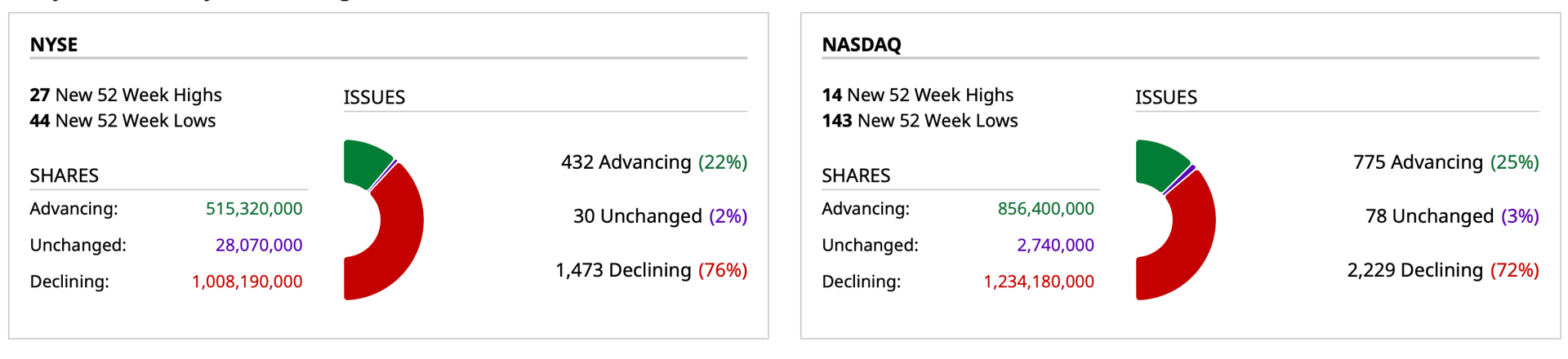

View larger here.

BY Doug Kass · Apr 25, 2024, 9:24 AM EDT

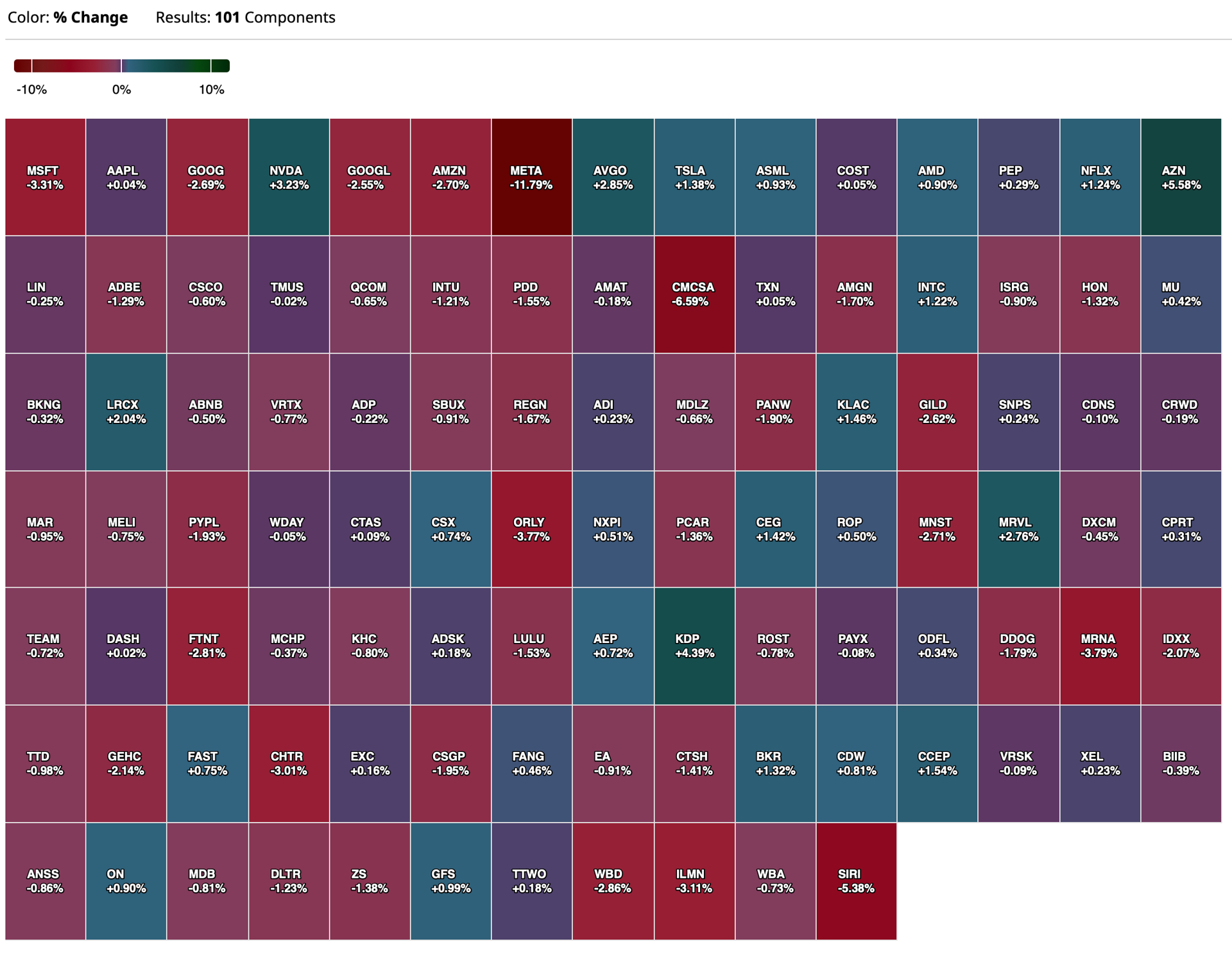

View larger here.

BY Doug Kass · Apr 25, 2024, 9:18 AM EDT

Upside

-CDTX +16% (reacquires global development and commercial rights to CD388 (in development for prevention of all strains of influenza A and B) and announces private placement financing of $240M; announces divestiture of Rezafungin to Mundipharma for $128M in cost savings over patent life)

-PTSI +12% (commences self-tender offer to purchase up to 550K shares)

-TRU +12% (earnings, guidance)

-TER +8.6% (earnings, guidance)

-CYH +7.3% (earnings, guidance)

-VTGN +6.1% (announces Positive Results from Phase 2A Pilot Study of PH15 for Improvement of Psychomotor Impairment Caused by Mental Fatigue)

-AAL +5.8% (earnings, guidance)

-DB +5.6% (earnings, guidance)

-LAB +5.4% (to cut 10% of jobs in restructuring aiming to save $45-50M in annual opex in 2025)

-ACRV +5.3% (reports Initial Positive Clinical Data for ACR-368 and Pipeline Program Progress Today at Corporate R&D Event)

-ALGN +5.2% (earnings, guidance)

-CLS +5.1% (earnings, guidance)

-HCP +5.1% (confirms to be acquired by IBM at $35.00/shr in cash, valuing it at $6.4B)

-CARR +4.1% (earnings, guidance; expects to resume share repurchases in 2024)

-RCL +3.9% (earnings, guidance)

-KDP +3.8% (earnings, guidance)

-CHDN +3.7% (earnings)

-PUMP +3.6% (increases share repurchase authorization by additional $100M for total of $200M)

-CMG+3.2% (earnings, guidance)

-WU+2.9% (earnings, guidance)

-OII +2.5% (earnings, guidance)

-MDWD +2.4% (to Present New Data from EscharEx Phase II Studies at Three Leading Wound Care Conferences)

-STM +2.3% (earnings, guidance)

-HON +2.2% (earnings, guidance)

-WHR +2.2% (earnings, guidance; to cut jobs)

-MRK +2.1% (earnings, guidance)

-UHS +2.0% (earnings)

Downside

-META -15% (earnings, guidance)

-JAKK -10% (earnings)

-HZO -9.1% (earnings, guidance)

-IBM -8.7% (earnings, guidance)

-LUV -8.4% (earnings, guidance)

-TXT -5.9% (earnings, guidance; to reduce headcount)

-MXL -5.3% (earnings, guidance)

-NOW -4.5% (earnings, guidance)

-CAT -4.0% (earnings, guidance)

-ORLY -4.0% (earnings, guidance)

-GOOGL -3.3% (said to be increasing hardware development and R&D team in Taiwan)

-ITGR -3.1% (earnings, guidance)

-BHPLF -2.9% (BHP confirms to offer 0.7097 shares for each share in Anglo American (implies £25.08/shr offer) in all-stock deal valued at £31.1B)

-BMY -2.6% (earnings, guidance)

-IP -2.6% (earnings)

-HTZZW -2.2% (earnings)

BY Doug Kass · Apr 25, 2024, 9:13 AM EDT

* More than ever stay away from "groupstink"

I am working off a laptop today so my normal flow in my Diary will not be possible.

Here are some general observations about post EPS reports:

* Viking Pharmaceuticals quarter was better -but based on the conference call remarks I should not have pared some of my position above $67 on Wednesday as I am more convicted than ever that the company will be sold. I will explain in a more expanded column later today. I will be adding on weakness.

* META revives my critical view of "groupstink." A higher than expected capital spending guide took the shares -$80 or so. A consensus long - see CNBC Halftime yesterday and at many shows during the last week - the lack of analytical process though my friends at independent boutique Hedgeye got it very right for the right reasons. The same logic applies to CAT, NOW and many others recently. I will stop there before I get into more trouble!

* Based on META's higher cap ex needs - I wouldn't be surprised to see NVDA and semis rallying - even in a very weak tape.

* Yesterday I warned about the underappreciated risk of market structure. More than ever I remained concerned about a flash-crash like incident, or market accident, given the disproportionate role of quants in our market place . Too many are on the same side of the boat and momentum can be a sweet thing but it can also be fatal.

* As a corollary I expect the VIX to rise - late yesterday I took off ALL of my straddles and strangles for a profit - prior to the META release.

I start the day in market neutral exposure.

I am fairly certain that we are in a new regime of volatility.

I suspect there is more downside. See my revised Market Outlook and my continuing concerns earlier this week.

Most importantly, given still historically high multiples, equity investors - facing rising geopolitical and political risks- are not being sufficiently compensated for the overall risks on one hand and the risk free rate of return for short dated Treasuries on the other hand.

My defensive positioning allows me to be opportunistic in trading and investing in this uncertain, risky and volatile investing backdrop.

I am already finding some long values that I am beginning to accumulate, and even a potential homerun and 10x bagger to be disclosed shortly - I am accumulating already.

As I wrote this week I am not a Perma Bear, I am not a Perma Anything.

I am excited to get long and, for the first time, expecting opportunities on the long side that may lie ahead.

I have no emotional attachment to an all weather commitment to "compounders" or a need to follow price momentum for fear of business risk and other reasons.

I am consistent. My modus operandi is based on a patient and disciplined assessment of reward v. risk with a sense of "margin of safety" a cherry on the top of my sundae that I hope to soon digest.

BY Doug Kass · Apr 25, 2024, 8:57 AM EDT

Before we get to all the most notable earnings news, let's start with stock market sentiment with the correction going on. As it always seems to be, when the mood gets very one sided, its most likely that the trade shifts the other way and this time was no different. That said, the extreme bullishness seen last month that was the perfect contrarian set up for a pullback has cooled down.

Investors Intelligence yesterday said Bulls fell to 46.2 from 56.5 while Bears were up by 7 pts to 21.5. As stated here many times, a spread over 40 is considered extreme and we got to almost 50. AAII today said Bulls fell for a 4th week, by 6.2 pts to 32.1 which is the least since early November. They all went to the Neutral side though as Bears were little changed at 33.9, holding at the highest since early November.

The CNN Fear/Greed index closed yesterday at 40, in the Fear camp and it was 33 one week ago. The Citi Panic/Euphoria index remains in Euphoria as of last weekend at .43 but that moves more slowly.

Bottom line, now that the pendulum is swinging in the other, less bullish direction, we eventually then set us up for a rally with the timing and level from which to be determined.

The earnings comments below still point to a lot of moving parts with pockets of strength and those seeing weakness.

The generative AI hype machine is now broken. Attention is now on the massive capital spending needed to build out large language models, the uncertain returns and timing on this investment and the intense competition from not just the other huge companies but from so many scrappy smaller ones too.

From Meta:

"As we're scaling CapEx and energy expenses for AI, we'll continue focusing on operating the rest of our company efficiently. But realistically, even with shifting many of our existing resources to focus on AI, we'll still grow our investment envelope meaningfully before we make much revenue from some of these new products. I think it's worth calling that out, that we've historically seen a lot of volatility in our stock during this phase of our product playbook, where we're investing and scaling a new product but aren't yet monetizing it."

"In addition to our work on AI, our other long-term focus is the metaverse" and we know that's been expensive too. "For Reality Labs, we continue to expect operating losses to increase meaningfully y/o/y due to our ongoing product development efforts and our investments to further scale our ecosystem."

On their add business, likely helped by Shein and Temu, "the online commerce vertical was the largest contributor to y/o/y growth, followed by gaming and entertainment and media. On a user geography basis, ad revenue growth was strongest in rest of world and Europe at 40% and 33% respectively. Asia Pacific grew 25% and North America grew 22%."

With their outlook, "we remain pleased with engagement trends and have strong momentum across our product priorities...Video also continues to grow across our platform, and it now represents more than 60% of time on both Facebook and Instagram." They are also improving their "monetization efficiency."

On guidance, "we aren't giving full year 2024 guidance. And obviously, our revenue for the full year will be influenced by many factors, including macro conditions and things that are harder to predict the further out you go."

Here were some macro comments from IBM:

"We expect the global economy to behave similarly to last year, albeit with some uncertainty due to persistently high interest rates. There are reasons to believe technology will be even more important in 2024 as clients focus on productivity improvements and customer experience." Of course they mentioned AI as part of driving productivity.

On their outlook for 2024 where they maintained their revenue and cash flow guidance, they see a solid start to the year in their software business but in consulting, "we are seeing some pressure on smaller, more discretionary projects" and overall see mid single digit growth in this division. I think this is what is contributing to the stock weakness this morning.

Because of the strength of the US dollar, they see a 150 to 200 bps FX clip to earnings growth this year.

In case you missed it, the Dow Jones Transportation index yesterday was down 2.3% with an 11% drop on Old Dominion leading the way followed by softness in the rails and airlines.

Old Dominion said that their "financial results improved during the 1st quarter of 2024, despite the continued softness in the domestic economy."

"Our customers have had fewer shipments to give us as a result of the slower economic environment." They are hopeful though, "I would say right now, underlying demand has felt relatively consistent, but it does feel like things are improving a bit...we've seen some sequential acceleration."

Norfolk Southern said this, "The macro landscape presents a mixed bag with uncertainty regarding inflation and future Fed rate actions overshadowing the recent recovery in manufacturing...Starting with our view on the widely varying merchandise markets, we generally see support from volume from the normalization of auto production and the continued strength in infrastructure projects across our network. A positive price environment will continue."

Specifically on the auto side, Group 1 Automotive, the car retailer, said this yesterday:

On the 8% comp gain, "These strong unit sales reflect the resiliency of demand and our emphasis on driving volume." Pricing "performed about as expected and continue on their slow glide path down as inventories return." Auto sales though overall nationally remain below the 2019 trend and likely in part due to affordability challenges.

With respect to lending, "We expect some continued pressure on used vehicle finance penetration due to existing interest rates and higher lender requirements for some buyers. However, we expect continue improvement on new vehicle finance penetration due to increasing OEM incentives."

Chipotle continues to rock and roll with 7% comp growth, "driven by over 5% transaction growth. Our strong sales trends were fueled by our focus on improving throughput in our restaurants as well as successful marketing campaigns."

How did they respond to the new $20 minimum wage bump in California? "We subsequently took a 6% to 7% menu price increase in our California restaurants just to cover the cost in dollar terms. This will add almost a full point to total company pricing beginning in Q2."

As for their input costs, "We anticipate cost of sales inflation will be in the mid-single digit range for the remainder of the year." Their wage inflation will be about 6%, helped by California.

Lastly from them on the breakdown of their customer base, "It's really broad based. So from the low income consumer to the middle income to the higher income consumer, we're just seeing gains with all income cohorts. And when we ask the question, why is that? What we hear back from every group is, it's a great value proposition."

Shifting to the home, Ethan Allen reported and mentioned, not surprisingly, "currently operating in a challenging home furnishings industry...Overall demand patterns across our industry have been sluggish. Our written order trends in the quarter were impacted by continued softening of the market, elevated interest and inflation rates, reduced designer center traffic, partially due to adverse winter weather conditions, and a strong prior year demand."

They are hopeful though too, "But as we went into March, we did start seeing some improvements, and in April, we have seen more interest in the consumers getting back into the home from travel and all other areas."

Also supplying to the home in the repair/remodel side, Masco said this in a quarter where sales were down 2% in North America and by 5% internationally:

"For the remainder of the year, we remain cautiously optimistic as we continue to monitor inflation data, the likelihood of current year interest rate cuts, and changes in consumer confidence levels. However, we continue to believe the fundamentals of our repair and remodel markets are strong and that structural factors, such as the age of housing stock, consumers staying in their homes longer, and higher home equity levels, will drive increased repair and remodel activity over the mid to long term."

We know travel and leisure spend has been an economic bright spot and this was from Hilton where international travel did better than domestic:

"System wide RevPAR increased 2% y/o/y, which was at the low end of our guidance range as renovations, inclement weather, and unfavorable holiday shifts weighed on results more than we anticipated."

That said, "Leisure transient RevPAR exceeded our expectations even with tough y/o/y comparisons, given continued strength in international markets and holiday shifts. Business transient recovery remained steady with RevPAR across large corporates up more than 3%, driven by strong demand in consulting and government contracting." We certainly know what is driving 'government contracting.' Group was strong too, "led by strong convention and social demand."

They maintained their guidance and said "the broader economy is reasonably strong, seems to be very resilient. Obviously, employment numbers are quite good. Corporate profits, depends on the industry, are quite strong...when you talk to customers, which we do all the time, you get a very positive view about their people traveling more for business transient...While leisure certainly is normalizing from super high levels, it give you, I think, a reasonable amount of confidence that it's still going to be relatively strong, modest growth, mostly in the form of rate, because we continue to have a decent amount of pricing power."

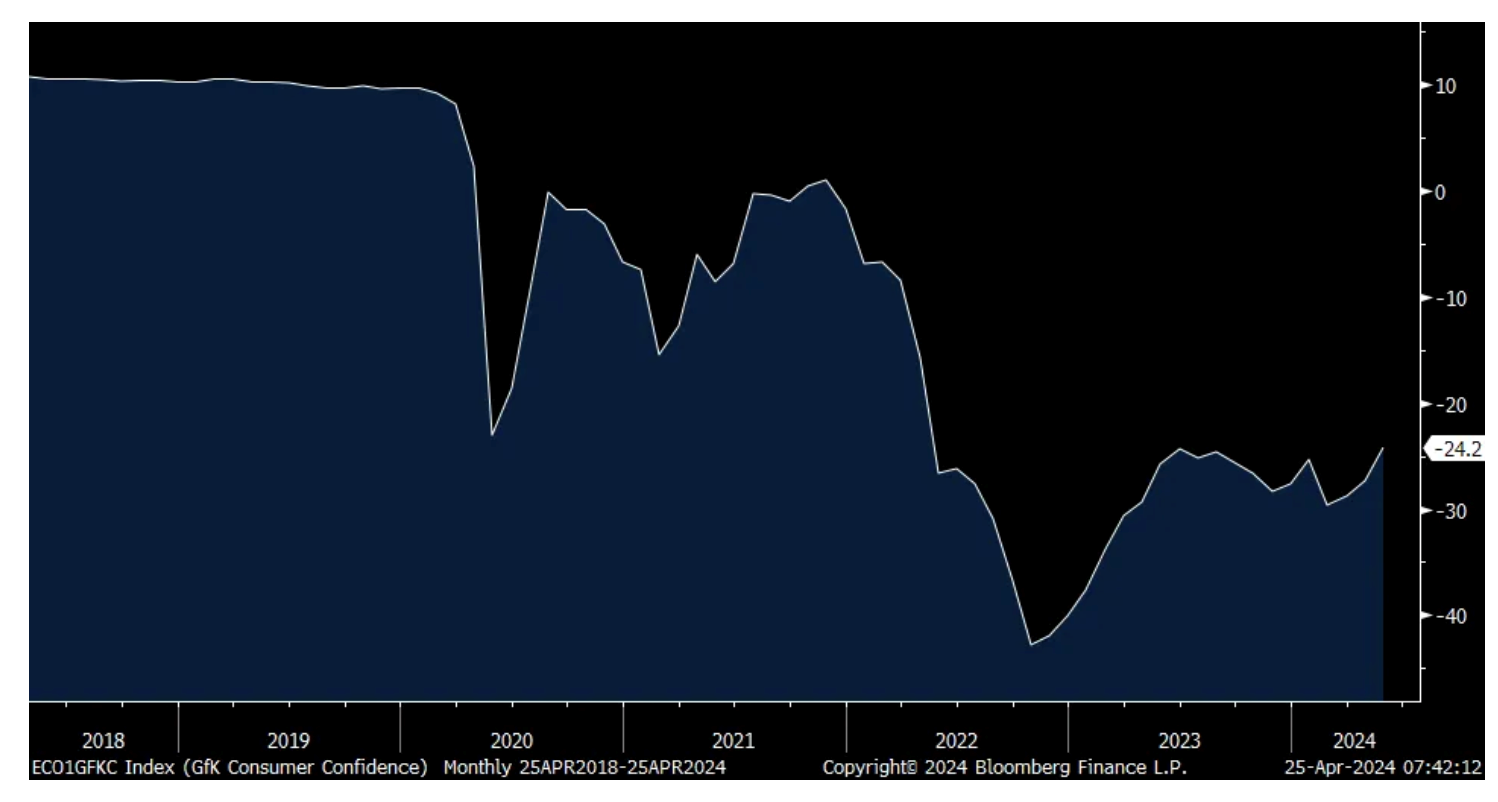

Overseas and following the slight improvement in German business confidence, French business confidence in April fell 1 pt to 99 vs the estimate of 101. For perspective, in February 2020 it was at 105.7. Manufacturing, services and building confidence all fell m/o/m while retail and employment ticked up. Nothing market moving here but European yields are slightly up as is the euro. The CAC though is down 1%.

German consumer confidence was less bad again at -24.2 vs -27.3 in the month before. That's the best since May 2022. A comment there was this, "Rising wages and salaries combined with a recent decline in the inflation rate form the foundation for increasing purchasing power among private households." Maybe the German economy can come out of their slight recession.

German Consumer Confidence

BY Doug Kass · Apr 25, 2024, 8:32 AM EDT

I am adjusting to the California time zone!

Back in a few.

BY Doug Kass · Apr 25, 2024, 7:56 AM EDT