Signing Off Before Tonight's Earnings

I am going to sign off in advance of some important EPS reports - which I need to digest.

Thanks for reading my Diary today.

Enjoy the evening.

Be safe.

BY Doug Kass · Apr 23, 2024, 3:48 PM EDT

I am going to sign off in advance of some important EPS reports - which I need to digest.

Thanks for reading my Diary today.

Enjoy the evening.

Be safe.

BY Doug Kass · Apr 23, 2024, 3:48 PM EDT

iShares 20+ Year Treasury Bond ETF TLT turns lower on the day.

More paper at auction tomorrow.

BY Doug Kass · Apr 23, 2024, 3:32 PM EDT

BY Doug Kass · Apr 23, 2024, 3:20 PM EDT

BY Doug Kass · Apr 23, 2024, 2:58 PM EDT

Wolf Street howls about existing and new home prices.

BY Doug Kass · Apr 23, 2024, 2:46 PM EDT

I intend to short DJT on strength if I can get a borrow.

BY Doug Kass · Apr 23, 2024, 1:18 PM EDT

BY Doug Kass · Apr 23, 2024, 12:22 PM EDT

Pressing a bit harder - with S&P cash +54 handles - on the short call side.

BY Doug Kass · Apr 23, 2024, 11:42 AM EDT

From Peter:

The April US services and manufacturing PMI fell to 50.9 from 52.1 and that matches the lowest print since November 2023. Manufacturing slipped back under 50, by a hair, at 49.9 from 51.9. Services moderated to 50.9 from 51.7. Of note, “inflows of new business fell for the 1st time in six months and firms’ future output expectations slipped to a 5 month low amid heightened concern about the outlook.”

Here were some other snippets from the press release:

“Some service providers suggested that elevated interest rates and high prices had restricted demand during the month.” Employment weakened as “The overall reduction in workforce numbers was centered on services, where employment decreased solidly and to the largest extent since mid 2020. In fact, excluding the opening wave of Covid, the decline in services staffing levels in April was the most pronounced since the end of 2009.”

Price pressures did ease though, “Service providers often noted higher staff and shipping costs, though reported the 2nd lowest overall cost increase for 3 ½ years.” On the pass thru side, “output prices increased at a solid but slower rate during April,” though off a 10 month high in March. I bolded for emphasis as it’s another anecdote that doesn’t fit with the BLS payroll data.

We know a key drag on manufacturing has been a few things. One, the shift to spending on services from goods, the desire on the part of many retailers to have lean inventories and the lack of desire to restock those inventories because of uneven end demand.

S&P Global said, “US manufacturers drew down their stocks of purchases for the 2nd consecutive month in April, and to a solid degree that was the most marked since August last year. Firms made some efforts to limit the pace of depletion, however, raising their purchasing activity slightly following a fall in the previous survey period.” And inventories on the whole did tick up but not for good reason, “the slight rise in post-production inventories reflected a slowdown in demand which left firms holding unsold goods.”

Employment did tick up “modestly” in contrast to the service side. Also in contrast to the service side, input costs rose to the highest in “a year amid rising raw material prices.” Price pressures have risen in “three of the past four months.”

The bottom line according to S&P Global, “The US economic upturn lost momentum at the start of the 2nd quarter.” US Treasuries are rallying in response with the 10 yr yield back below 4.60%. This squares with the Beige Book bottom line that the US economy grew slightly over the survey period. By the way, the Q1 GDP report this week is expected to print 2.5% but it still sounds more like a 1.5% ish type economy we’re in.

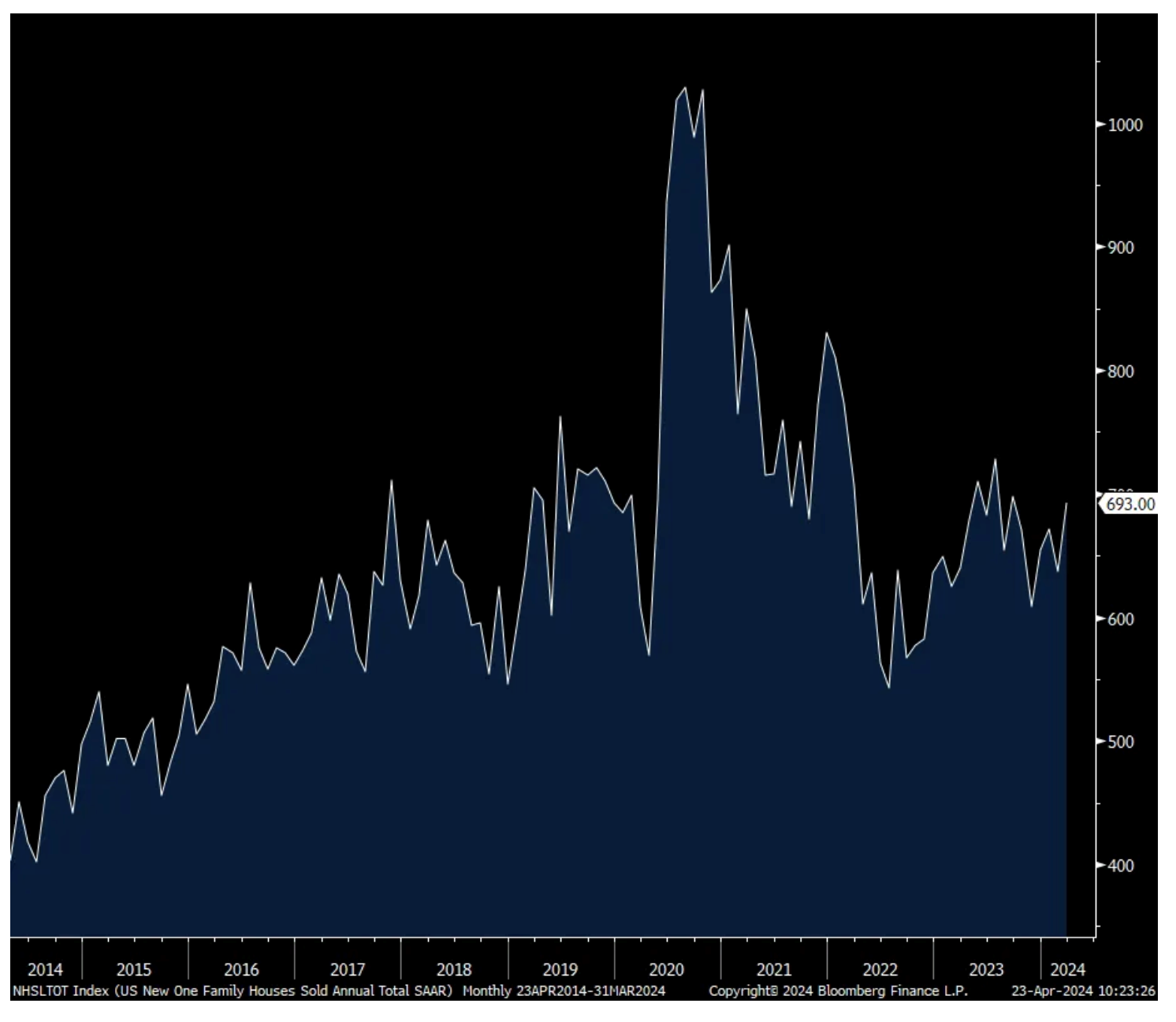

New home sales in March, always volatile month to month, totaled 693k, 25k more than expected but February was revised down by the exact same amount to 637k. While the absolute number of homes again rose, the higher sales in the month saw a drop in months’ supply to 8.3 from 8.8. and vs 8.2 in the month before that. Thanks to mix, the median home price fell 1.9% y/o/y, though was up 6% sequentially.

Bottom line, we know we need more homes on the market but because the existing home market is just not giving it to us, the new build market needs to fill in. However, we know the challenges with pricing and rates, especially for the 1st time buyer, and why the bigger builders are discounting their product, whether via mortgage rate buydowns, teaser rates, and/or pricing discounts. Smaller, non publicly traded, builders though are having a tougher time because of higher cost capital and less room to discount.

New Home Sales

BY Doug Kass · Apr 23, 2024, 11:18 AM EDT

* Cliff Notes version!

"Risk is good. Not properly managing your risk is a dangerous leap."

- Evel Knievel

I have been of the (mistaken) view since late last year that upside reward was modest relative to downside risk and that, in the aggregate, the market's 'margin of safety' was not visible.

As a result - since December 2023 - I have undertaken a low-risk strategy and positioned our portfolio with a sliver of shorts, some straddles and an abundance of "pairs trades."

Despite my protestations, equities rolled higher during 1Q2024 as animal spirits and FOMO ("the fear of missing out") flourished - perpetuated and extended by the influence of a changing market structure in which momentum-based strategies and products dominate the market landscape.

The market's upside momentum over the last four or five months became almost intoxicating to many traders and investors who, seeing a new paradigm, embraced the promises of AI - while ignoring the many emerging challenges we have been warning about:

* Rising geopolitical risks

* Higher interest rates for longer

* Prickly inflation and slowing economic growth - "slugflation"

* Reckless and undisciplined fiscal policy that has led to an ever-larger annual deficit and cumulative US debt load

* Heady valuations

But, as demonstrated by the weakening performance of equities during the month of April, risk happens fast. The market broadened - but unlike the bullish cabal expected ... that broadening has occurred to the downside.

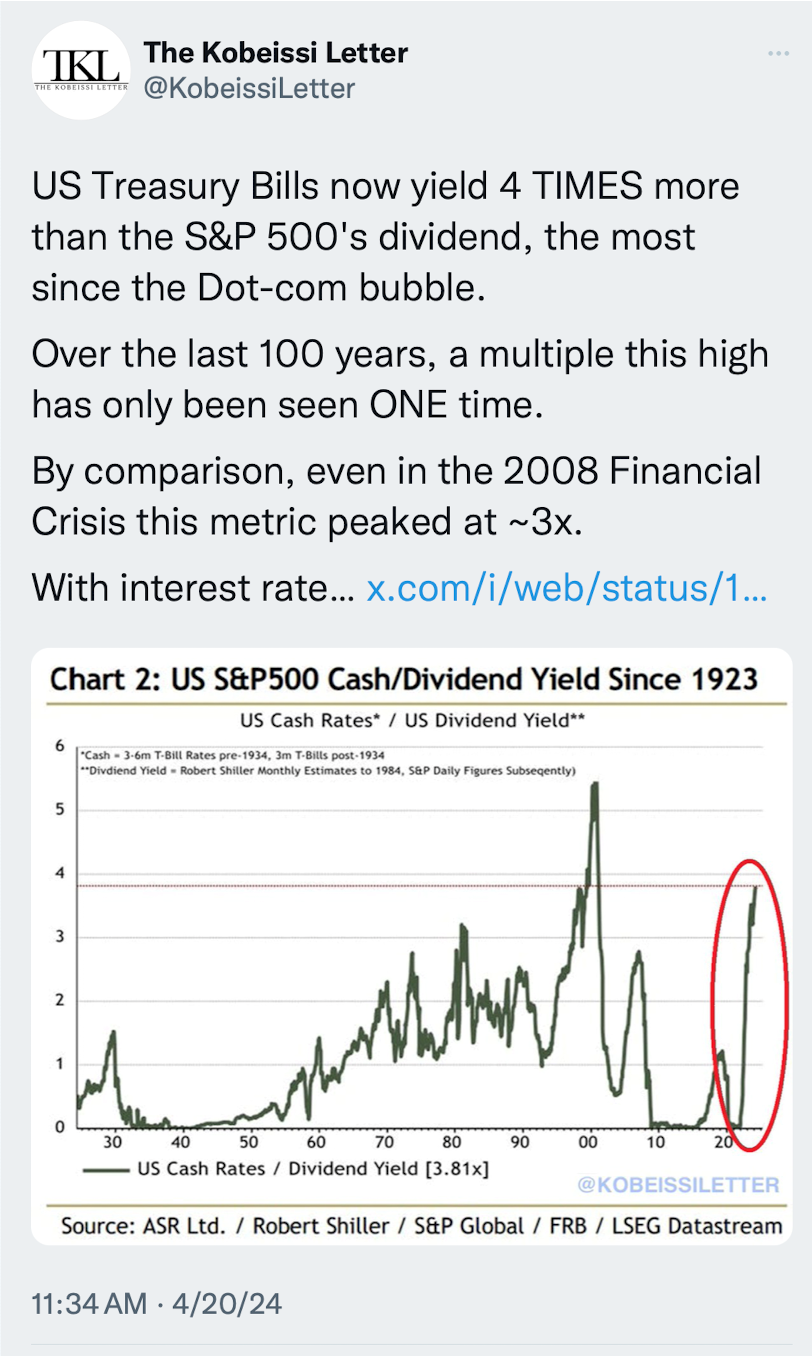

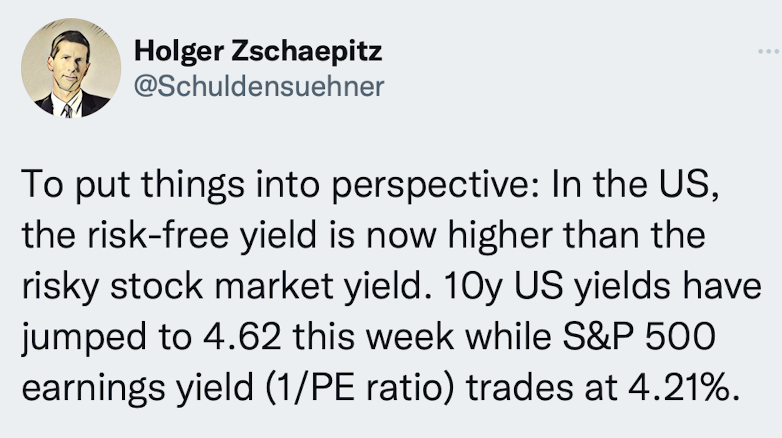

Given the recent fall from grace, stocks have become less overvalued but still remain relatively expensive, especially against interest rates and when compared to the paper-thin equity risk premium:

As well, it is increasingly clear, as we have feared, that the world is a more dangerous place.

Persistent inflation continues to be a concern - a headwind we have identified over the last twelve months.

And, our leaders in Washington, D.C. continue to display a level of partisanship that argues against any foresight or fiscal discipline. Frankly, the timing of this issue on the stock market continues to be vague!

Positioning on the short side, when done effectively, protects capital while positioning on the long side creates capital. We are not Perma Bears - we aren't Perma Anything. We simply assess risks relative to reward.

All this said, although I anticipate a continued market correction, a few individual equities are beginning to become attractive - finally providing some attractive opportunities on the long side. Indeed, two or three of the recent long positions we have put on hold very large upside promise. One of those, a potential home run, I have promised to deliver shortly in my Diary.

In the market decline over the last few days I have moved from modestly net short to modestly net long - with a continued heavy exposure to lower-risk "pairs trades."

I anticipate getting longer if more values emerge, but we will remain unemotional, disciplined, and analytical in our investment process.

BY Doug Kass · Apr 23, 2024, 9:35 AM EDT

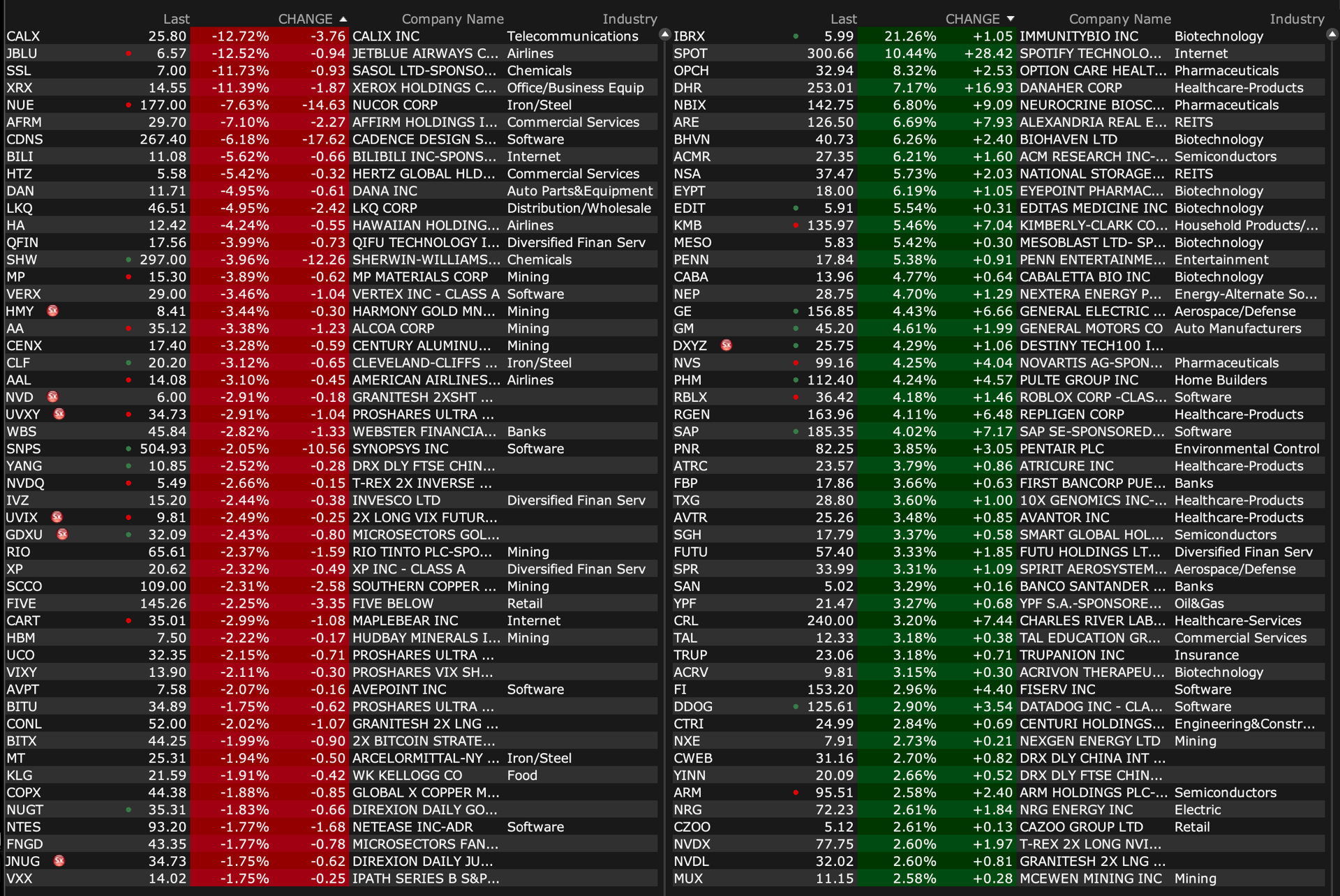

Upside

-PALI +38% (enters strategic collaboration with Strand Life Sciences to advance precision medicine approach)

-HIBB +19% (to be acquired by JD Sports for $87.50/shr in cash at EV of $1.11B)

-IBRX +19% (US FDA approves combination bladder cancer therapy)

-OPRT +15% (reports prelim Q1)

-SPOT +8.3% (earnings, guidance)

-DHR +8.0% (earnings, guidance)

-CANG +7.5% (announces up to $50M new share repurchase program)

-ARE +6.7% (earnings, guidance)

-TOVX +6.2% (announces positive topline data from Investigator Sponsored Phase 1 Trial of Intravitreal VCN-01 in Pediatric Patients with Refractory Retinoblastoma)

-KMB +5.0% (earnings, guidance)

-GM +4.7% (earnings, guidance)

-GE +4.3% (earnings, guidance)

-PENN +4.1% (Truist Raised PENN to Buy from Hold, price target: $23)

-PHM +3.9% (earnings)

-PNR +3.9% (earnings, guidance)

-RBLX +3.8% (JPMorgan Chase and Co Raised RBLX to Overweight from Neutral, price target: $48)

-FL +3.5% (earnings, guidance)

-ANRO +3.4% (announces positive Phase 1 results for ALTO-101, a novel PDE4 Inhibitor in development for Schizophrenia)

-DGX +3.0% (earnings, guidance)

-DDOG +2.8% (Wells Fargo Raised DDOG to Overweight from Equal Weight, price target: $150)

-MLI +2.3% (earnings)

-PII +2.0% (earnings, guidance)

Downside

-ABEO -46% (receives FDA CRL on Pz-cel based on need for additional CMC information)

-JBLU -10% (earnings, guidance)

-XRX -8.7% (earnings, guidance)

-AFRM -7.7% (Walmart-backed and majority-owned fintech One introduces buy now, pay later as it prepares bigger push into lending)

-NUE -7.1% (earnings, guidance)

-MSCI -6.8% (earnings, guidance)

-CDNS -6.3% (earnings, guidance)

-LKQ -5.0% (earnings, guidance)

-SHW -3.5% (earnings, guidance)

-CLF -2.9% (earnings, guidance)

-CPRI -2.5% (FTC has filed suit to block Tapestry deal to acquire Capri, as expected)

-VERX -2.5% (reports prelim Q1; files to sell private offering of $250M convertible senior notes)

-IVZ -2.4% (earnings)

-FIVE -2.1% (JPMorgan Chase and Co Cuts FIVE to Neutral from Overweight, price target: $170)

-FCX -2.0% (earnings, guidance)

BY Doug Kass · Apr 23, 2024, 9:27 AM EDT

View larger here.

BY Doug Kass · Apr 23, 2024, 9:14 AM EDT

View larger here.

BY Doug Kass · Apr 23, 2024, 9:09 AM EDT

From Peter:

I'll chime in for a second here. In the mind of the FTC, the world should just stop changing now. Don't move, everything should stay in place and all companies should stay in their lane with no lateral/vertical movement. The market cap of Capri is all of about $4b and is there a more competitive industry than fashion?

This attempt at blocking this deal is ridiculous. What they don't seem to understand too is the ripple effect this has on the entire private market funding ecosystem where many investor/VC funded companies end up getting bought by larger competitors because they need the help in taking their business to the next level. If every single deal is going to get blocked, whether public or private, irrespective of size and relevance, it clouds the exit strategy of private investors and could thus inhibit funding of new and exciting start ups.

Also, is the FTC familiar with the European luxury powerhouses like LVMH and Kering that just maybe a bulked up US competitor would be a good thing on the competitive stage? Bureaucratic overkill is what this is.

Global PMI's start to roll out today for April and economic growth is still being led by services while manufacturing remains in contraction. Also, pay attention to the commentary on inflation.

The Eurozone services PMI rose to 52.9 from 51.5 with the French seeing its services PMI back above 50 at 50.5 while Germany's improved to 53.3 from 50.1. Both were better than expected. As for manufacturing, the region's PMI fell to 45.6 from 46.1 with Germany's in particular deeply below 50 still at 42.2 vs 41.9 in March.

Highlighting the continued divergence in economic trends, "New orders for services rose in April at the fastest pace since May of last year, up for a 2nd straight month, but new orders for manufactured goods fell at an increased rate. The latter have now fallen continually for two years."

Just as the ECB is now comfortable enough with the trend in inflation to have them cut rates in June, S&P Global said "Price pressures intensified slightly in April, remaining elevated by pre-pandemic standards, with higher rates of inflation seen for both input costs and average selling prices. Average input costs across the goods and services sectors re-accelerated in April after having cooled in March, recording the joint-fastest increase seen over the past year."

On what can be recaptured via higher prices to the end customer, "Selling price inflation likewise accelerated in April, reviving from March's four month low to run well above the pre-pandemic long-run average and hint at stubborn inflation pressures." Manufacturing prices fell again but "prices levied by service providers rose at an increased rate, "continuing to climb at a strong pace by historical standards."

This economic bifurcation was seen too in the UK where services improved to 54.9 from 53.1 but fell in manufacturing to 48.7 from 50.3. Price pressures were seen here on the input side as this accelerated to an 11 month high. "Service providers continued to record a much faster rise in input prices than manufacturing companies, although the latter saw the greatest increase since February 2023 amid higher transportation and raw material prices. The rate of cost inflation in the service sector was the steepest since last July."

Passing it along though was more difficult as "Survey respondents suggested that competitive pressures and efforts to stimulate sales had limited their scope to pass on higher salary costs to clients." In other words, margin pressure.

Not much of a response in either European sovereign bonds and FX but stocks are rallying for a 2nd day.

In Asia, Japan's service sector also led the way in April as this component of its PMI rose to 54.6 from 54.1 while manufacturing about flat lined at 49.9, though up 1.7 pts m/o/m.

Ahead of the BoJ meeting Friday, S&P Global said "April data also brought with it additional signs of intensifying price pressures. Average input prices rose at a quicker rate, attributed to higher rates of input cost inflation among both goods producers and service providers. Higher material, energy and wage costs were key sources of rising average cost burdens, with the weaker yen having played a significant part as well. Firms thereby passed on rising costs to clients, leading to the fastest increase in average charges in a year." I bolded for emphasis. Expect the BoJ to hike rates again this year, but not by much more, and QE to fully end. While the Nikkei rallied, JGB yields and the yen are little changed.

Australia's PMI saw services at 54.2 and manufacturing at 49.9, following the trend seen elsewhere as stated.

India remains the outlier where manufacturing is doing almost as well as its service sector. Services rose .5 pt to 61.7 and manufacturing held well above 50 at 59.1 and we know the latter is benefiting from supply chain diversification.

Globalization is still alive and well, it is just finding new homes.

Moving to earnings.

From Verizon:

"As we saw in the quarter, it was a little bit slow in the beginning of the quarter, both for consumer and for business when it comes to wireless...At the same time, the team has spent a lot of time to be disciplined, both with promotions and churn management."

From Truist Financial:

"Average loans decreased 1.3% sequentially, reflecting overall weaker client demand and our decision to deemphasize certain lending activities during 2023, which impacted growth during the first quarter. Average commercial loans decreased by .9%, primarily due to a 1.2% decrease in C&I balances due mostly to lower client demand. In our consumer portfolio, average loans decreased 2%, primarily due to further reductions in indirect auto and mortgage."

There are hopes by management that loan growth will improve. "And here in the first quarter, we've seen pipelines improve, particularly on the commercial side. You know, how they get to execution and how they get to finalization will depend on a lot of market conditions. But the good news is clients are having the discussions, they're having the debate about the new warehouse or the new fleet of trucks, the things that they want to do to continue to expand their businesses."

"Asset quality metrics continue to normalize in the first quarter, but overall remained manageable." We've heard that word a lot, 'normalize' over the past few weeks with bank earnings.

"The increase in net charge-offs for the quarter reflects increases in our CRE and consumer portfolios, offset by lower C&I and CRE construction losses."

Pepsi's Q1 revenue growth was all price/mix as volumes fell .5% y/o/y. We await the call.

Kimberly Clark's revenue number got clipped hard by FX as that trimmed 5 percentage points off revenue growth. Price added 4 pts back and volume did by 1.

BY Doug Kass · Apr 23, 2024, 8:15 AM EDT

Doomberg on "Friends Like These."

BY Doug Kass · Apr 23, 2024, 7:48 AM EDT

BY Doug Kass · Apr 23, 2024, 7:20 AM EDT

BY Doug Kass · Apr 23, 2024, 7:10 AM EDT

“The four most dangerous words in investing are: this time it's different.”

- John Templeton

Today's "Charting the Technicals" is rich in content. Moreover, the unusual nature of the market over the last few days is interesting to observe (strength in S&P equal weight, lower gold, crypto halving, financial strength, SP breakdown (?), oil meets resistance (?)_etc:

Bonus - Here are some great links:

BY Doug Kass · Apr 23, 2024, 7:00 AM EDT

* Continuing the Apple theme...

Throughout the last twelve months "Groupstink" and herd thinking have captured the consensus of bullish Apple-Think.

The business media does viewers no favor in generally interviewing Apple AAPL bulls day in and day out. It would take only a little bit more effort in finding Apple bears — but producers are lazy and uncreative.

"Groupstink" has even enveloped Warren Buffett's Berkshire Hathaway, whose investment position in Apple dwarfs all of his other holdings.

From Hedgeye, an independent voice:

Cartoon of the Day: Falling $AAPL (hedgeye.com)

As noted, in an earlier column this morning (and throughout the last year) we don't believe in indexing or benchmarking and we remain short of Apple — principally based on both demand and supply issues facing the company in China.

We are willing to go against the grain — ignoring the business risk of not being long of Apple (a sizeable component of most indexes)... and being short of Apple.

If you want consensus, look at the rear-view mirror (where investment vision is 20/20) and dutifully watch FIN TV.

But that is not for me.

BY Doug Kass · Apr 23, 2024, 6:45 AM EDT

BY Doug Kass · Apr 23, 2024, 6:30 AM EDT

* China represents both demand supply challenges:

* For emphasis...

* Seabreeze remains short of TSLA and AAPL...

It has been my non-consensus view (over the last six to 12 months) that the share prices of Apple (AAPL) and Tesla (TSLA) were vulnerable to a related factor (China demand and supply exposure) -- and that the share prices of both companies have meaningful downside risk.

Though I suspect there may be near-term risk in the other (AI-fueled) members of The Mag 7, I continue to believe that Apple (in particular with its outsized weighting in many indices) and Tesla represent potential downside leadership in the market correction I expect.

Indeed, my Surprise List for 2024 incorporated two related surprises in my Top Ten Surprises.

From my 10 Surprises for 2024:

Surprise #5. The biggest and most popular stock in the world, Apple, suffers a large percentage loss in 2024 as trade tensions with China escalate. With China supporting Huawei, Apple loses substantial market share in that country and overall revenues decline again in 2024 (over 2023). Meanwhile, as a result of the Google Anti-Trust case, Google undefined stops paying Apple $18 billion in search fees. Apple's shares drop to below $130/share. Berkshire Hathaway BRK.B "doubles down" on its already large Apple stock holdings - raising its position to nearly two billion shares.

Surprise #8. What would a surprise list be without mention of Elon Musk? It is revealed that Elon Musk suffers from a serious addiction. Entering an extended stay in rehab, Musk is forced to temporarily relinquish operating control over his companies. Tesla's (TSLA) shares fall back to the lows of 2023.

Position: Short TSLA (S), AAPL (S)

MAR 5, 2024 8:00 AM EST

Position: Short TSLA (S), AAPL (S)

MAR 13, 2024 12:30 PM EDT

BY Doug Kass · Apr 23, 2024, 6:20 AM EDT

Wolf Street howls about brick-and-mortar meltdown.

BY Doug Kass · Apr 23, 2024, 6:05 AM EDT

BY Doug Kass · Apr 23, 2024, 5:53 AM EDT

China is throwing a kink in the US Big Tech bonanza story. Apple is down today after a report that its China sales plunged 24% in the first six weeks of the year, and AMD is falling after the US blocked it from selling a tailor-made AI chip to China. bloomberg.com/news/articles/…

Just hours to go until the 4th #Bitcoin halving! Looking to understand exactly *what* is happening? We've got you covered - bit.ly/SOTN-255 #PutTruthToWork