See You in LA

Thanks for reading my Diary today.

See you in LA - bright and early tomorrow morning.

Enjoy the evening.

Be safe.

BY Doug Kass · Apr 24, 2024, 3:32 PM EDT

Thanks for reading my Diary today.

See you in LA - bright and early tomorrow morning.

Enjoy the evening.

Be safe.

BY Doug Kass · Apr 24, 2024, 3:32 PM EDT

* From Arlo Guthrie to Mama Cass to Joni Mitchell to Randy Newman

* We love it!!

Coming in from London, from over the pole

Flyin' in a big airliner

Chickens flyin' everywhere around the plane

Could we ever feel much finer?

Comin' into Los Angeles

Bringin' in a couple of keys

Don't touch my bags if you please, mister customs man

- Arlo Guthrie, Coming Into Los Angeles (I was at Woodstock at this performance!)

I am about to prepare to board a plane in a few hours to visit my family in Los Angeles.

When I was a yute I had an intense crush on Michelle Phillips. (I still do!):

All the leaves are brown (all the leaves are brown)

And the sky is gray (and the sky is gray)

I've been for a walk (I've been for a walk)

On a winter's day (on a winter's day)

I'd be safe and warm (I'd be safe and warm)

If I was in L.A. (if I was in L.A.)

- Mamas and the Papas, California Dreamin'

And then there was Denny Gartman's favorite singer, Joni Mitchell:

Oh, but California

California, I'm coming home

I'm gonna see the folks I dig

I'll even kiss a sunset pig

California, I'm coming home

- Joni Mitchell, California

I love LA!

From the South Bay to the Valley

From the West Side to the East Side

Everybody's very happy

'Cause the sun is shining all the time

Looks like another perfect day

I love L.A. (we love it)

I love L.A. (we love it)

We love it

- Randy Newman, I Love LA

BY Doug Kass · Apr 24, 2024, 2:48 PM EDT

BY Doug Kass · Apr 24, 2024, 2:00 PM EDT

From Wally:

BY Doug Kass · Apr 24, 2024, 1:40 PM EDT

I moved back to market neutral - from small net long - on today's morning gap higher.

BY Doug Kass · Apr 24, 2024, 1:30 PM EDT

* As we move closer to a decision on rescheduling...

Adding to MSOS, GTBIF, (TSNDF), CURLF and TCNNF.

BY Doug Kass · Apr 24, 2024, 1:15 PM EDT

What follows is an email that I received from a very good friend:

I returned my leased car last week. I had been getting calls about a new lease from customer service for a while, but decided to go back to an Audi. When I brought the car back, I noticed they were offering a lease on the shorter range version of the model Y for $240 per month! They are almost giving these cars away.

When I returned the car they had me sign the odometer form which listed the mileage at 29997 which was below the actual mileage because I had extended the lease for six months, but they said mileage on the form would be used to calculate excess wear and tear.

I immediately received an email saying that my excess wear and tear charges were available to view on the app. However, when I returned the car, the car was disconnected from the app so I could not see the charges. And I was immediately charged almost $1900 which was deducted from my bank account, used to pay the monthly lease charge.

I reached out to the customer service rep and he gave me an email to contact for lease returns. It is almost impossible to talk to a human unless you want to buy something. After two days lease returns responded that the excess wear and tear charge was in error, and they were looking into it. However, they have my money.

My bottom line, when Tesla was selling a few cars to cool techies doing everything through the app may have worked. However, their customer service is inadequate for the mass market. The return was near the Red Hook cruise terminal in Brooklyn, and the people there admitted they need more and more convenient locations. Tesla's costs for customer service have to go up.

* I remain short of Tesla

"Smoke and mirrors" or extend and pretend?

I would argue the former - smoke and mirrors!

The "earlier than expected" launch of autonomy, Robotaxis and a low-priced auto offset the big reduction in last quarter's and future unit deliveries - as Tesla's shares rose swiftly following the after hours EPS report.

Wall Street numbers will go down measurably - yesterday's report will take billions of dollars of sales out of the sell-side estimates and take down the 2025 consensus EPS forecasts to around $3.00/share (from almost $8/share months ago).

And then there is the cash burn (h/t Jonesy at Hedgeye):

The only reason I didn't short more in the gap higher during the after hours was the magnitude of the share price decline leading up to the report.

That said, we are likely in the process in which investors begin to value Tesla more like an automobile manufacturer and less like an AI play.

This takes time - as the devotees slowly lose faith in their reasons for owning Tesla's shares.

But faith they are losing - as measured by the already sizeable absolute decline in the company's market capitalization.

Here was my Tesla Surprise in my Ten Surprises for 2024

It is revealed that Elon Musk suffers from a serious addiction. Entering an extended stay in rehab, Musk is forced to temporarily relinquish operating control over his companies. Tesla's (TSLA) shares fall back to the lows of 2023.

And, here was my Tesla surprise in my Ten Surprises for 2023

Surprise #6. Under the pressure of a further decline in Tesla's share price (to under $80/share) and Twitter's foundering fortunes, Elon Musk suffers from mental health issues and is briefly hospitalized. Upon his return, Musk reverses his decision to resign as Twitter's CEO and instead resigns his position at Tesla.

Surprisingly, under Musk's guidance, Twitter turns around and, by year end, it is debated whether Twitter is more valuable than Tesla, which is weighed down by a more challenging competitive landscape and rising customer dissatisfaction with Musk and his product.

Elon Musk admits that he is addicted to Twitter (TWTR) and liked the product so much that be purchased the company. This way, when he Tweets, he can say he is working.

Under fatigue and mental anguish, Musk is briefly hospitalized.

Though he recently announced that he is looking for a CEO to replace him, he reneges on the promise and stays on as Twitter's chief executive officer and resigns as head of his other ventures to concentrate his efforts on Twitter.

Tesla's (TSLA) shares drops badly on the announcement (to under $80/share) and, in coming months the lack of new product, increasing competition and growing customer dissatisfaction cause a demand collapse. The company's growth stalls out at a run-rate of less than two million cars and, in late 2023, factory production is reduced. In the wealthy, left-leaning population centers, driving a Tesla becomes a politically embarrassing statement and Tesla's core customer base swiftly erodes.

Musk's management of Twitter -- eliminating costs, free speech moderating -- succeeds beyond anyone's imagination. By the second half of the year it is learned that Twitter's revenues and profits achieve record results.

In late 2023 Musk is made whole as Twitter is taken public by Goldman Sachs and Morgan Stanley at an initial valuation of between $50 billion and $75 billion.

A Barron's cover story debates whether Twitter has become more valuable than Tesla.

BY Doug Kass · Apr 24, 2024, 12:55 PM EDT

* All weather? No, stormy weather may lie ahead...

Market structure remains a key concern of mine - though you will rarely hear a discussion of it in the business media.

The market is dominated by products and strategies that worship at the altar of price momentum. Though they are termed "passive" - they operate actively by chasing momentum up and down.

They know nothing about value but everything about price - and they are all on the same side of the boat.

Quants represent the tail that wags the market dog. It is an unhealthy condition that can lead to unexpected market dislocations - much like portfolio insurance did in October, 1987.

Over the last few years we have had some wild intraday swings As an example, today META was +$15 this morning and is now -$10 on no news.

I am fearful that something worse lies ahead.

Just when investors have gotten all bulled up.

BY Doug Kass · Apr 24, 2024, 12:35 PM EDT

At 11:15 am:

- NYSE volume 130M shares, flat to its one-month average

- Nasdaq volume 1.33B shares, 4% below its one-month average

- VIX up 2.74% to 16.12

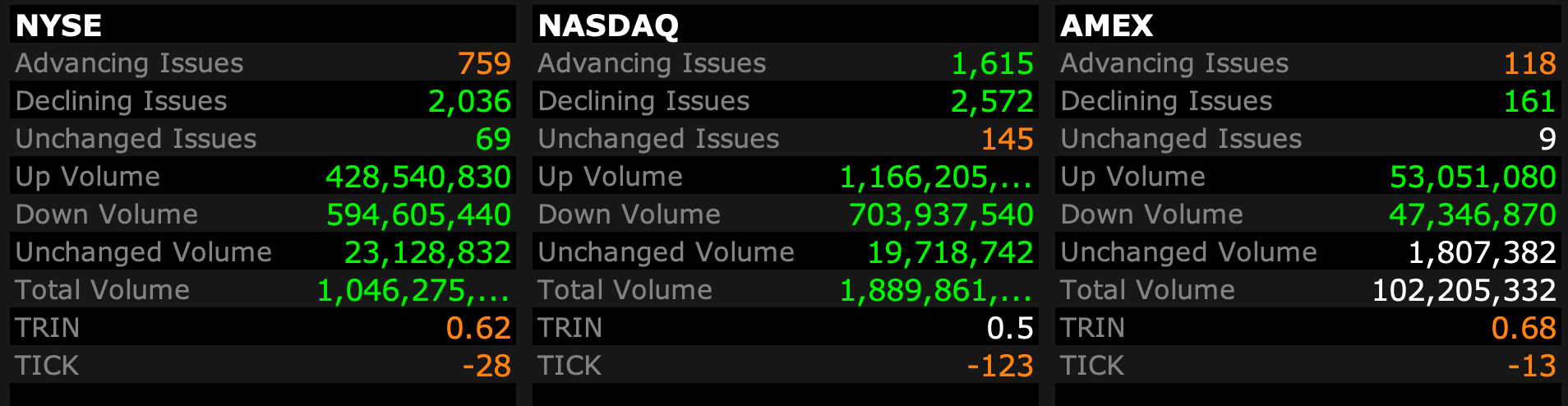

Breadth

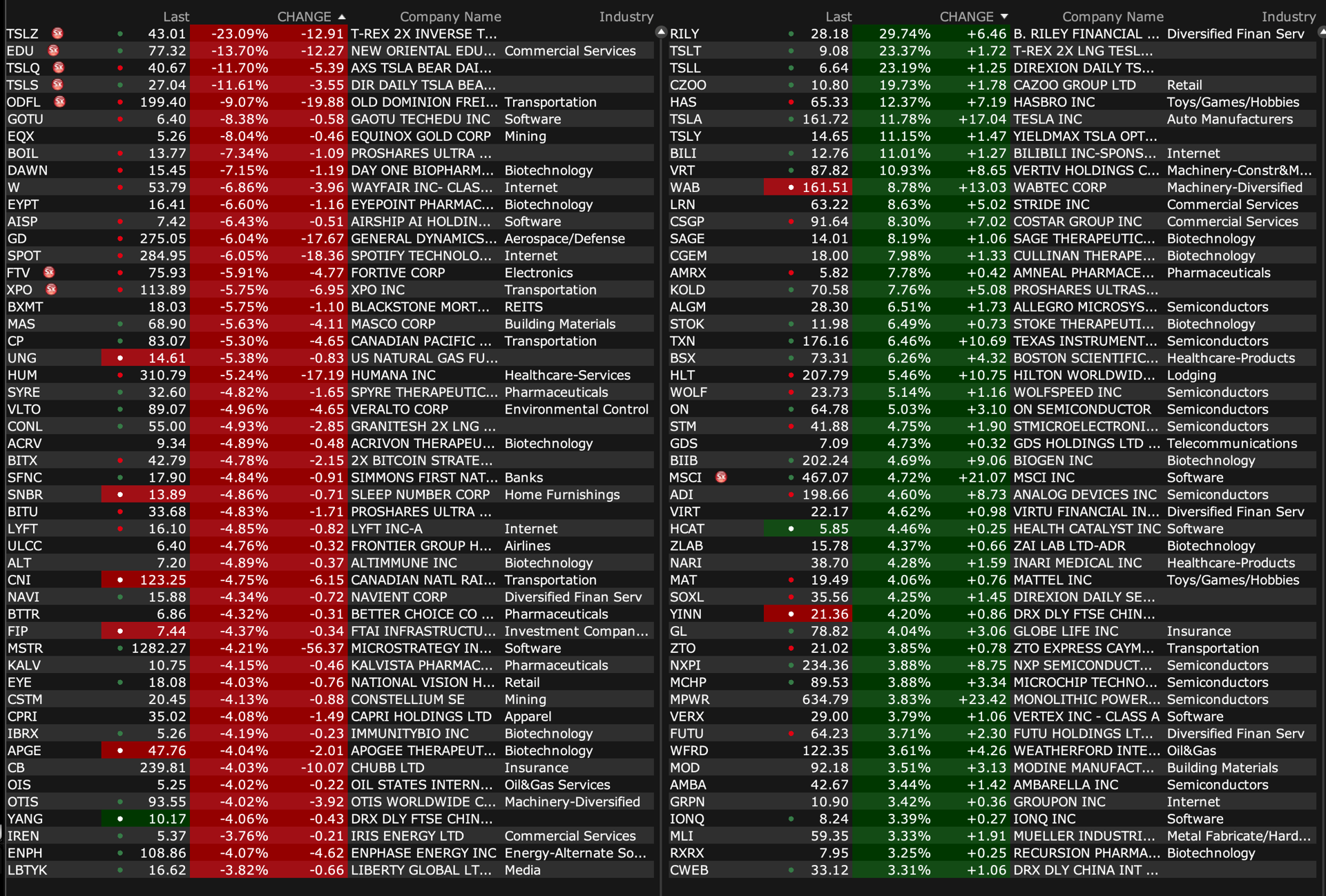

Biggest Movers

View larger here.

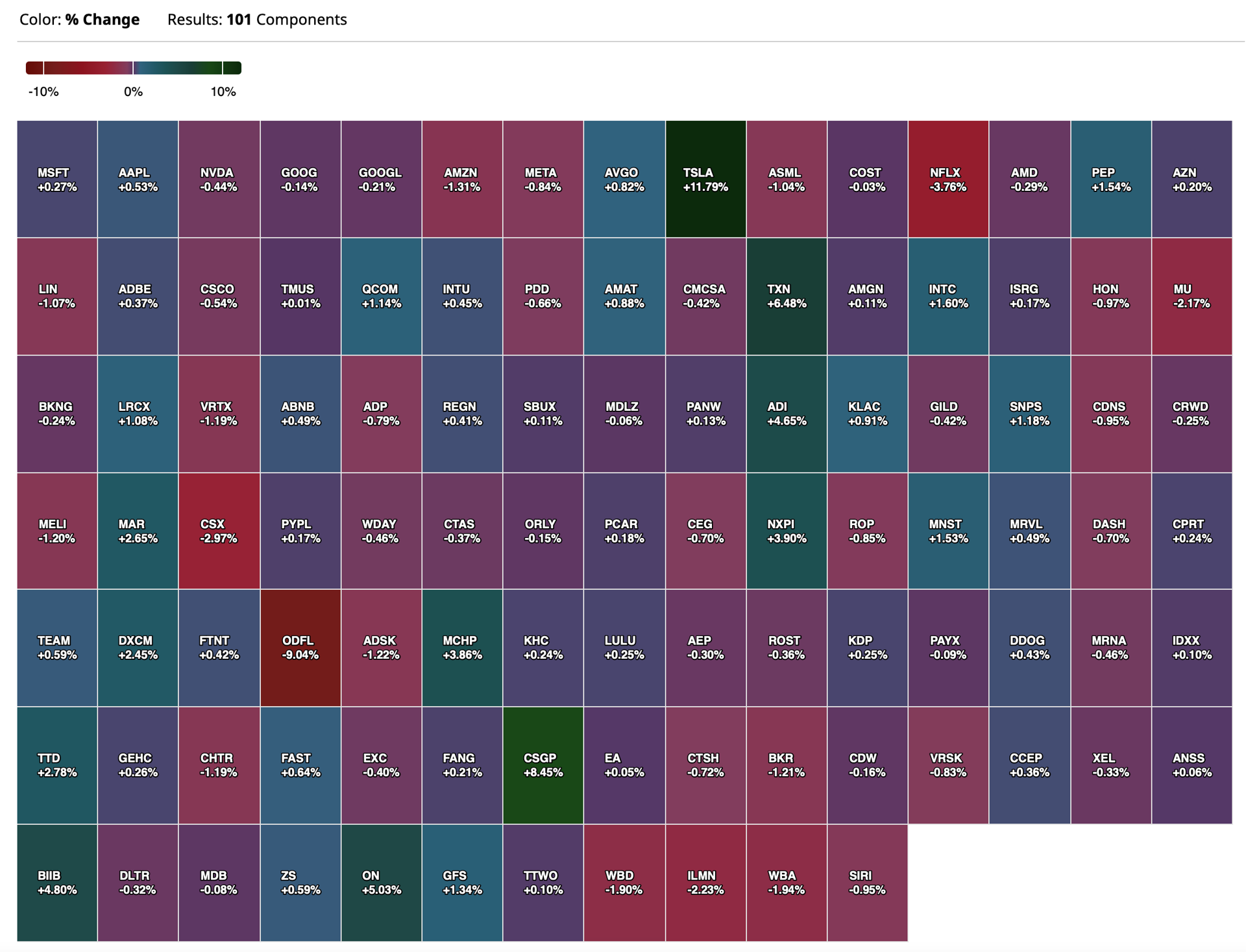

Nasdaq 100 Heat Map

View larger here.

BY Doug Kass · Apr 24, 2024, 11:55 AM EDT

Peapack-Gladstone Financial PGC is down by -6% after a few pennies earnings miss.

The shortfall was from increased expenses associated with hires from Signature/NYCB.

Another penny of the miss was credit and the shape of the yield curve.

It seems to be to be an extreme reaction as the bank's wealth franchise is solid, healthy and expanding market share.

I will be on the 1 pm analyst conference call and will give feedback after it!

I am adding on a scale.

BY Doug Kass · Apr 24, 2024, 11:40 AM EDT

The S&P Index has reversed markedly, -35 handles from the high, to the downside and the Nasdaq has slipped from the highs.

I have a nice and quick profit on the Index calls I shorted late yesterday and today:

In the premarket gap higher, I added to short SPY/QQQ in the money calls for May.

But still small-sized.

Position: Short SPY calls (S), QQQ (X)

So, I am covering some of my SPY/QQQ short calls and selling some SPY/QQQ puts (out of the money for June) - and moving back to the balance of a straddle.

BY Doug Kass · Apr 24, 2024, 11:25 AM EDT

Viking Therapeutics VKTX has risen from a low of $61, where I was adding, to over $67 in the last few trading sessions.

I have reduced my position at $67.20.

Though I expect the EPS release after the close to be a non event, it is probably the conservative thing to do.

BY Doug Kass · Apr 24, 2024, 11:02 AM EDT

I am leaving to Los Angeles tonite to visit my family.

I will be writing over the next few days but my output will be less than usual.

BY Doug Kass · Apr 24, 2024, 10:15 AM EDT

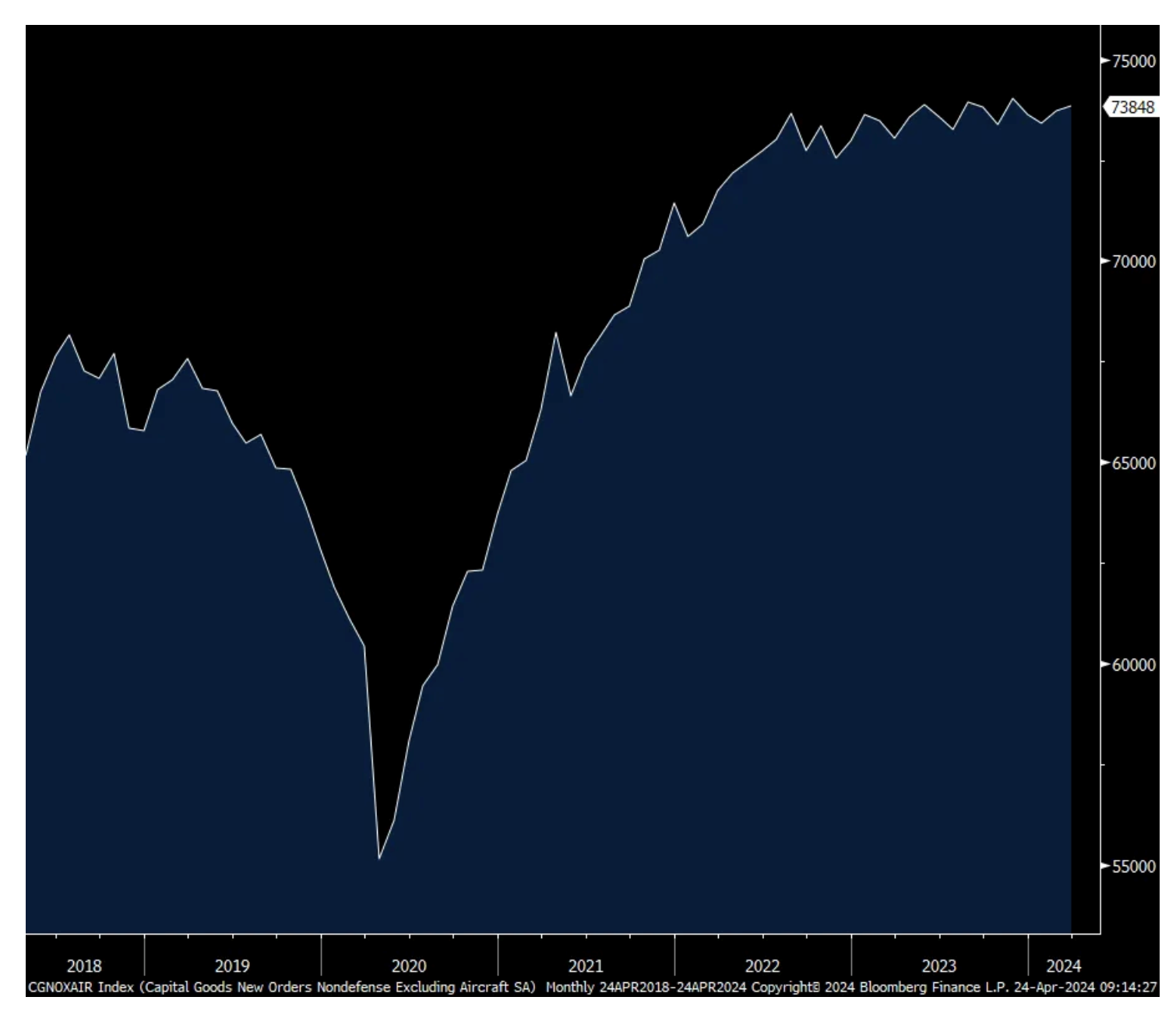

Core durable goods orders in March rose .2% m/o/m as expected but off a lower than estimated base as February was revised down by 3 tenths. Vehicle/parts orders rose 2.1% m/o/m but still down 2% y/o/y. After a 1.9% drop in February, orders for computers/electronics (and thus including AI stuff), rose .8% and are little changed y/o/y, higher by .5%.

Electrical equipment orders were about flat and down 2% y/o/y even with all the renewable incentives out there. Machinery orders were flattish too and down 1.8% y/o/y. Orders for metals were mixed.

Bottom line, in Q1, core orders are up just .3% in total in nominal terms and down .8% y/o/y in March. As seen for the past few quarters (and we’ll get another read tomorrow for Q1), capital spending has basically flat lined in totality.

Yes, many billions are being spent on anything AI but it seems that the spend there is being pulled from other places, with little impact on the entire cap ex pie.

Core Durable Goods Orders in nominal dollars

BY Doug Kass · Apr 24, 2024, 9:50 AM EDT

In the premarket gap higher, I added to short SPY/QQQ in the money calls for May.

But still small-sized.

BY Doug Kass · Apr 24, 2024, 9:36 AM EDT

The answer over the question of whether the Federal Reserve policy is restrictive or not is, of course, it depends. We know that anything reliant on borrowing is more challenged and that was seen today with the March US Architecture Billings Index which fell sharply to 43.6 from 49.5 with all four regions of the country well below 50. The Commercial/Industrial component fell the most, to 42.9 from 46.1 while multi family remains well under 50 at 44.2 vs 44.9 in February.

The chief economist there said simply, "Elevated construction costs coupled with prolonged high interest rates continue to discourage new project activity."

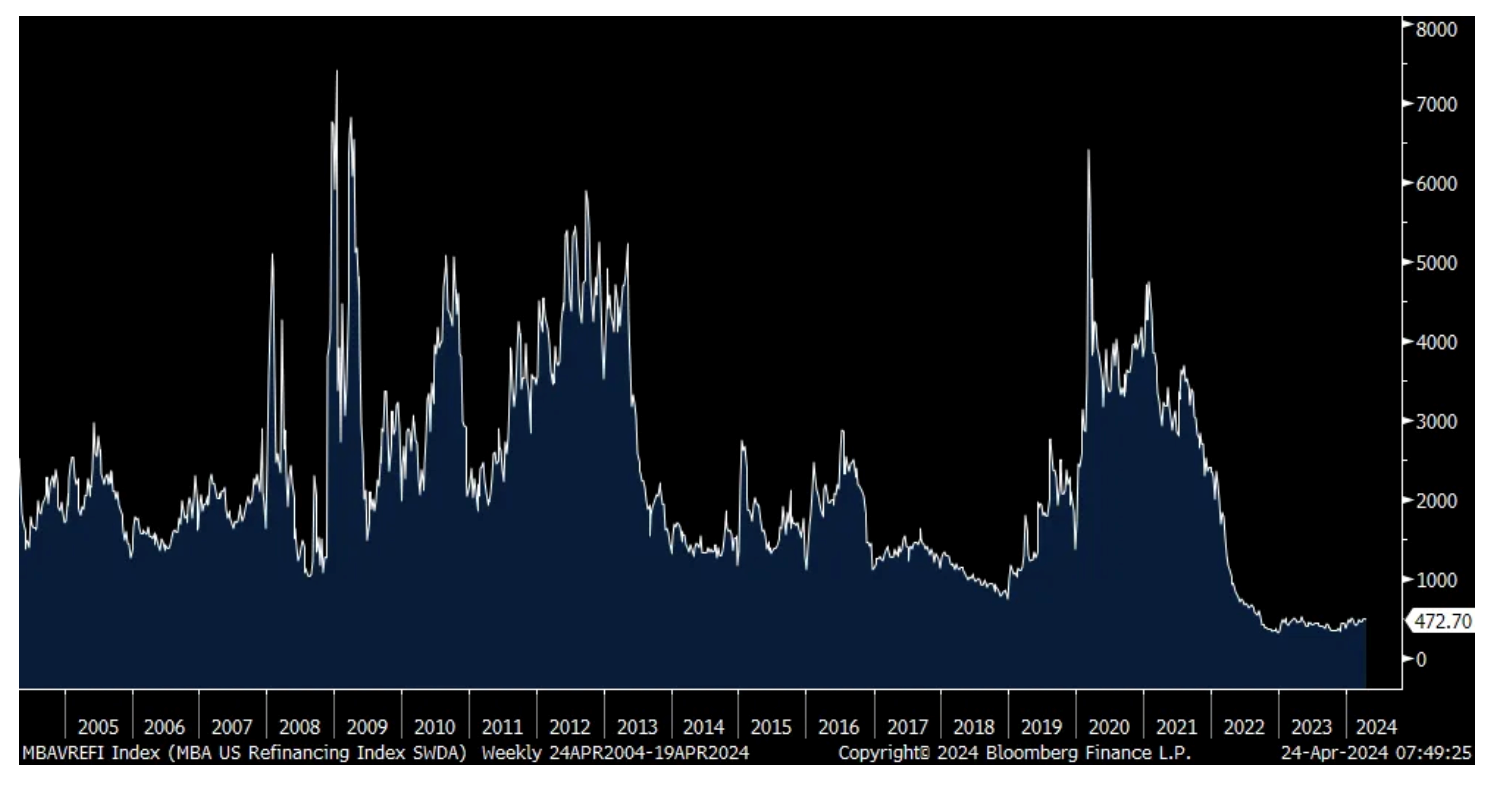

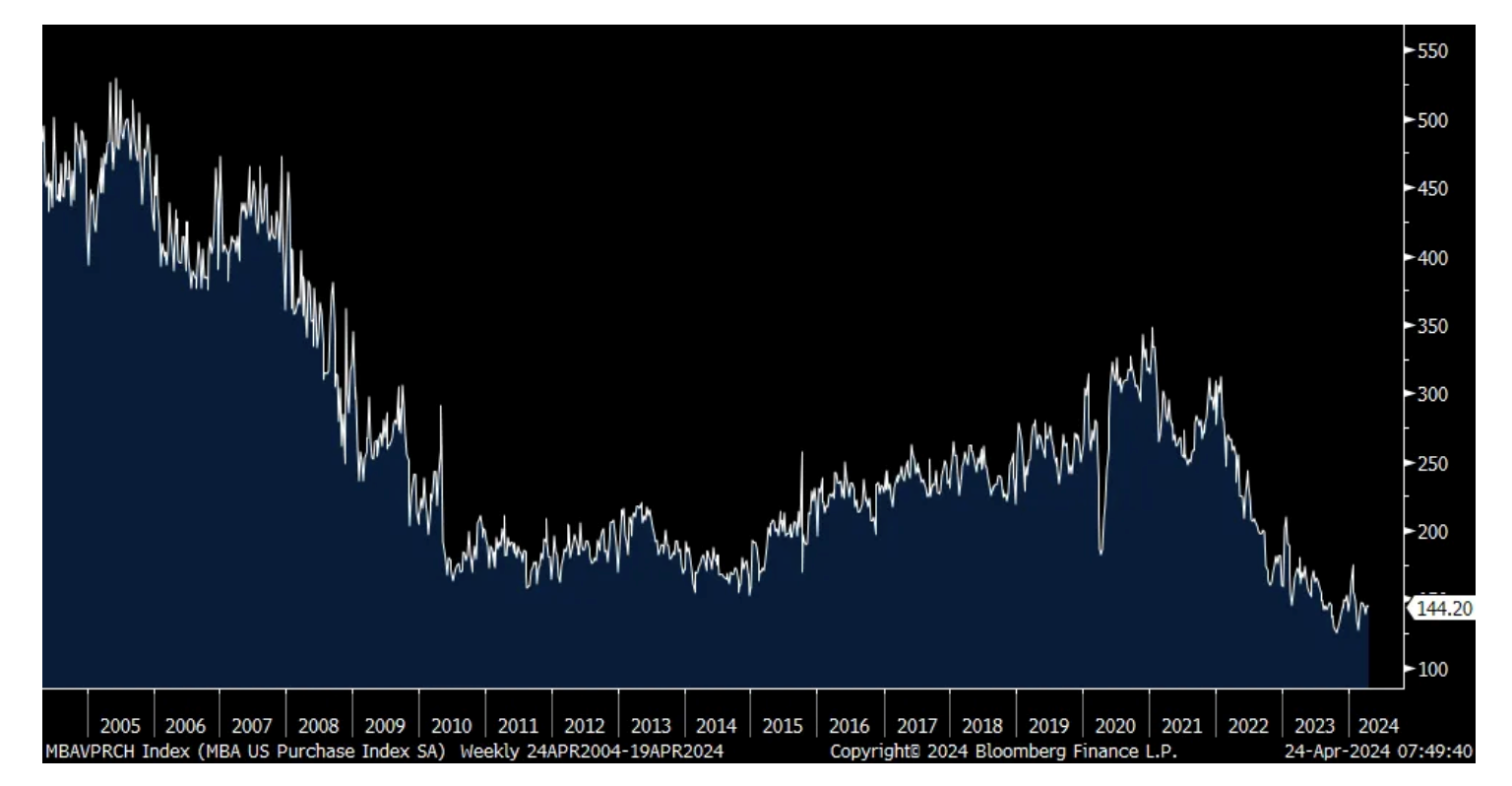

Housing too is feeling the rate pressure as we know. With mortgage rates ticking up again, purchase applications fell 1% w/o/w and are down 15% y/o/y. Refi's were down 5.6% w/o/w, though are up 3.3% y/o/y, bouncing along a multi decade bottom for obvious reasons.

Refi's

Purchases

With so many earnings reports, lets jump right in to a few of note.

From Visa, who continues to benefit from more people using card and less cash when they spend as the source of payment:

"US payment volume grew 6% y/o/y and international payments volume grew 11%...Cross border volume growth excluding intra-Europe was up 16% y/o/y in constant dollars." E-commerce they said was particularly as was 'tap to pay.'

"First, the extra day for the leap year was a benefit to the quarter. This was offset primarily by slowing payments volume growth in Asia-Pacific, mostly due to macroeconomic weakness in Mainland China."

Further with cross border with Asia-Pacific, "We see the primary drivers being; one, macroeconomic weakness in key markets like Australia and Mainland China; two, weakness in some Asia-Pacific currencies, which is impacting consumer purchasing power, particularly for Japan; and three, airline capacity that is still below 2019 levels, particularly the Mainland China and North American corridor." Cross border business outside of this seems to be better.

In the US, “Consumer spend across all segments from low to high spend has remained relatively stable.”

From Texas Instruments, whose stock is popping this morning:

"Revenue declined sequentially across all of our end markets. Our results reflect the current environment as customers continue to reduce their inventory levels. Similar to last quarter, our focus is on sequential performance as it's more informative at this time. First, the industrial market was down upper single-digits. The automotive market was down mid-single digits. Personal electronics was down mid-teens. Next, communications equipment was down about 25%. And lastly, enterprise systems was down mid-teens."

Maybe this is why the stock is rallying pre market:

"So we've got some of the later cycle sectors that are continuing to decline and declining at double-digit rates. But there are some that are beginning to slow in the declines and even a couple that grew sequentially. So that I would just describe as being more mixed this quarter, which is certainly different than last quarter."

From UPS:

"The first quarter turned out as we expected, starting with a decline in average daily volume. US ADV declined y/o/y, but the rate of decline slowed as the quarter progressed, ending with March down less than 1%. And on a sequential basis, the ADV decline rate in the 1st quarter showed marked improvement compared to the 4th quarter of 2023. This improving performance is primarily due to the efforts of our sales team to win and pull-through new volume into our network."

"While the macro environment in the 1st quarter showed improvement in some areas, continued soft demand pressured all three parts of our business...So from a ADV perspective in domestic, with a little bit of a slight tick up in positive volume in the 2nd quarter, we'll likely finish low single-digits decline in the first half. 2nd half, we'd expect that to be low single-digit increase."

"Moving to our international segment. The macro environment remained challenged, primarily in Europe and Asia. However, volume growth in the Americas region showed early signs of nearshoring."

From Sherwin Williams whose paint/coatings end up on just about everything:

With sales coming in at the lower end of their guidance range, "While uncertainties persist in the macroeconomic environment, we see opportunity. We are encouraged by pro-architectural sentiment in April and customers in several end markets are optimistic about an improving demand environment as the year progresses."

They talked about 'choppiness' in packaging, auto refinish, industrial wood, coil and protective/marine.

"We don't expect to get material help from the macro environment this year, but a few bright spots are emerging. Single family housing starts have improved. Existing home sales are unlikely to get much softer...the remodeling outlook continues to improve with declines easing and momentum building later in the year. On the industrial side, the manufacturing PMI has stabilized or improved in several regions."

On their raw material input basket, "we're still looking at down low single digits for the year. We'll see if there's some upside as the year progresses." That said, "we went out with a 5% February price increase and we said we would realize the full price increase over the next few quarters."

From GM:

"We again grew retail shares and market share in the US during the quarter with incentives that remained well below the industry average, especially in our truck business."

"Dealer inventory levels ended the quarter slightly above our 50 day to 60 day of year target at 63 days. However, we believe we are well-positioned from an inventory standpoint as we head into a seasonally stronger part of the year and incur a few weeks of planned downtime in Q2 on our full-size pickups to prepare for future launches and to install new equipment."

From Tesla and Elon Musk:

"As people have seen, the EV adoption rate globally is under pressure, and a lot of other auto manufacturers are pulling back on EVs and pursuing plug-in hybrids instead. We believe this is not the right strategy, and electric vehicles will ultimately dominate the market."

In the update of their future vehicle lineup, he mentioned "more affordable models" which has been the challenge for them in delivering.

"And I'll go back to something I said several years ago, that in the future, gasoline cars that are not autonomous will be like riding a horse and using a flip phone, and that will become very obvious in hindsight."

There was a lot of Musk focus on full self driving and he said this, "Cathie Wood said it best, really, we should be thought of as an AI or robotics company. If you value Tesla as just like an auto company, it's just the wrong framework. If you ask the wrong question, then the right answer is impossible. So, if somebody doesn't believe Tesla is going to solve autonomy, I think they should not be an investor in the company. That is - but we will and we are." Therein lies the major investor debate.

The CFO cited the "uncertain macroeconomic environment" as one of a few reasons why revenues fell q/o/q.

From Pulte Homes:

"Consistent with the favorable conditions in the first quarter, almost all our markets displayed pricing dynamics that were stable or improving, which allowed us to raise net pricing in more than half of our communities...The result being that net pricing in the quarter across many of our markets was up between 1% and 5%."

Pulte has pushed back on using price discounts to move product but instead has focused more on "targeted incentives, particularly mortgage rate buydowns" and they called it "a powerful tool that can help bridge the affordability gap." They also referred to their ability to buydown rates as a "greater competitive advantage."

"Against generally favorable demand conditions, the supply of available housing remains tight. We have the long term structural issue resulting from a decade of under building that has the country short approximately 4 million housing units. At the same time, the available inventory of existing homes for sale continues to be low as homeowners remain locked into their low mortgage rates. Life happens, so we are seeing some additional existing homes come to market, but the numbers remain well below historic rates."

Australian bonds got hit hard overnight after Q1 CPI exceeded expectations and with the March read in particular doing the same. In particular, the trimmed mean y/o/y increase of 4% was 2 tenths above expectations. So, the 10 yr Australian yield jumped by 14 bps to the highest since early December. Yields are jumping too in Europe and higher in the US.

Also of note, Bank Indonesia unexpectedly raised interest rates by 25 bps to 6.25%. It was done in part to defend their currency and where the Governor told us at what levels of the rupiah he'd be more comfortable with.

This comes right ahead of the BoJ meeting and where the weak yen will be a big topic of discussion.

The April German IFO business confidence index rose to 89.4 from 87.9 with the Expectations mostly leading the way with the Current Assessment up too but less so. The IFO said "The economy is stabilizing, especially thanks to service providers." This upside surprise is also why bund yields are rising to the highest since late November.

10 yr Bund yield

BY Doug Kass · Apr 24, 2024, 9:15 AM EDT

View larger here.

BY Doug Kass · Apr 24, 2024, 9:10 AM EDT

View larger here.

BY Doug Kass · Apr 24, 2024, 9:00 AM EDT

View larger here.

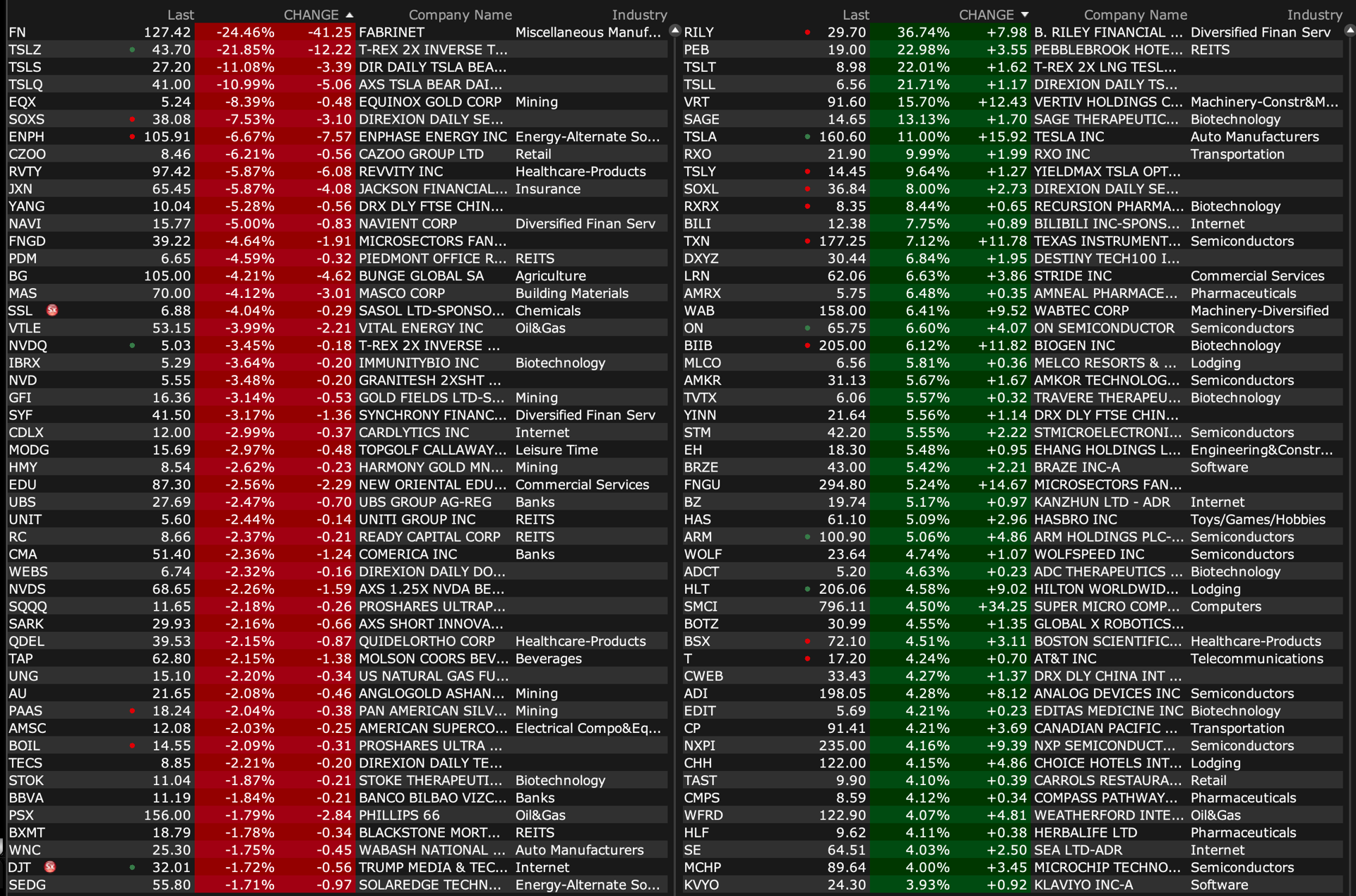

BY Doug Kass · Apr 24, 2024, 8:52 AM EDT

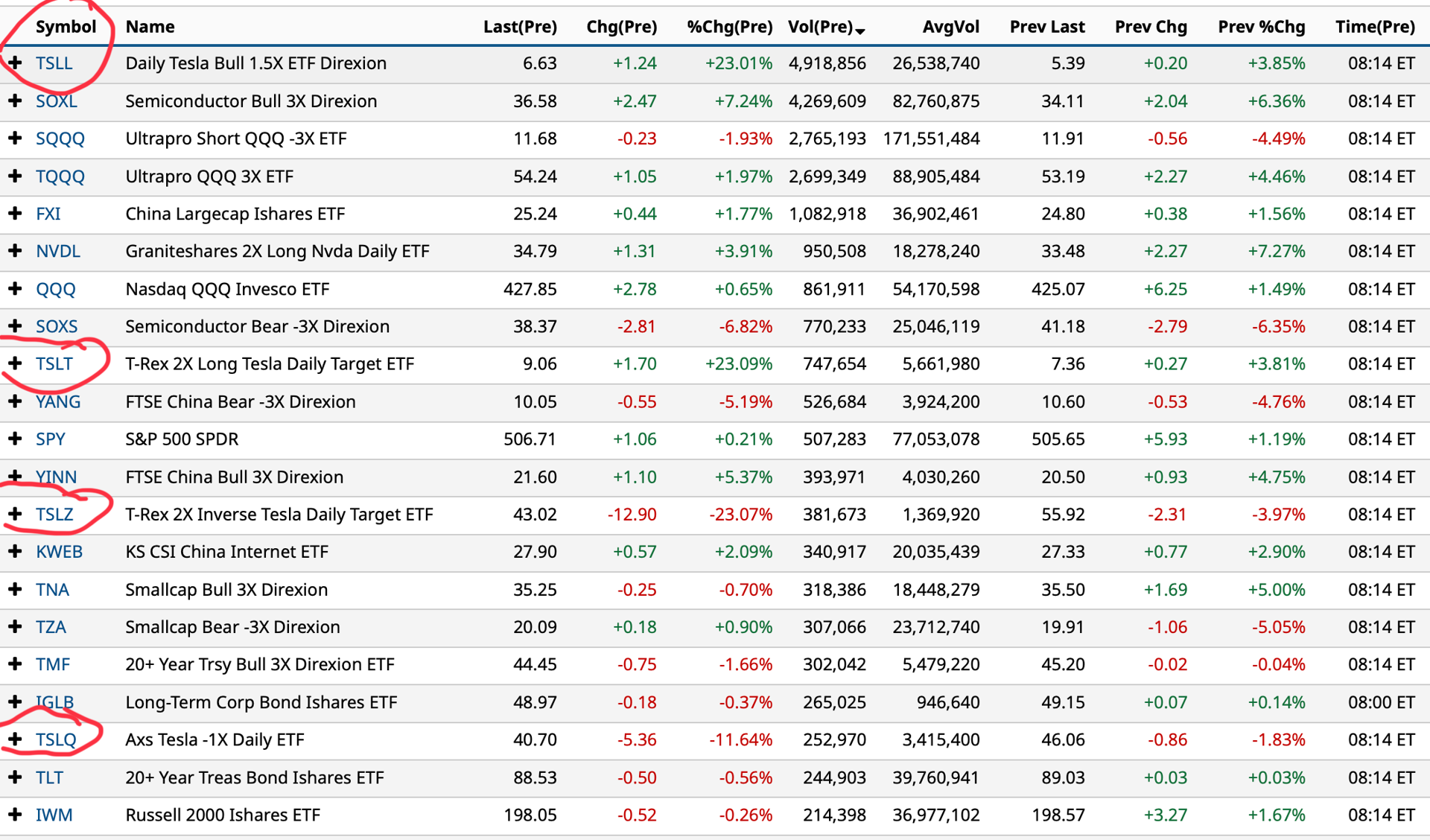

Upside

-RILY +29% (confirmed that the company and its executives had no involvement with, or knowledge of, any of the alleged misconduct concerning Kahn or any of his affiliates)

-VRT +17% (earnings, guidance)

-AEYE +16% (earnings, guidance)

-TSLA +12% (earnings, guidance)

-TXN +6.8% (earnings, guidance)

-BIIB +6.6% (earnings, guidance)

-WAB +6.4% (earnings, guidance)

-VFS +5.4% (momentum following officially signing agreements with 12 new dealers in the US)

-HAS +4.5% (earnings, guidance)

-T +4.4% (earnings, guidance)

-BSX+3.9% (earnings, guidance)

-APH +3.3% (earnings, guidance; announces new $2B share buyback program)

-BA +3.3% (earnings, affirms undertaking comprehensive actions to strengthen quality and safety)

-IPG +3.3% (earnings, guidance)

-HUM +3.2% (earnings, guidance)

-STLD +2.9% (earnings)

-CSGP +2.5% (earnings, guidance)

-VIRT +2.5% (earnings; authorizes $500M share buyback)

-V+2.3% (earnings, guidance)

Downside

-ENPH -8.4% (earnings, guidance)

-TDY -7.0% (earnings, guidance)

-LAD -6.4% (earnings, guidance)

-MAS -5.4% (earnings, guidance)

-NAVI -5.1% (earnings, guidance)

-HELE -4.3% (earnings, guidance)

-SCLX -3.8% (files to sell $15M registered direct offering; enters definitive agreement with institutional investors to sell 15M common shares at $1.00/shr)

-BG -3.2% (earnings, guidance)

BY Doug Kass · Apr 24, 2024, 8:42 AM EDT

* With machines and algos dominating: Insane in the membrane, insane in the brain

* Look for the new regime of volatility to continue in the weeks ahead

* The market's multi day move higher continued in force on Tuesday

* Low volume rally yesterday:

* Stock futures fell towards breakeven overnight after being up close to +25 handles - in the market with no memory from day to day

* The S&P Short-Range Oscillator grows remains oversold - but less so at -3.28%

* Bond yields are higher by 4bps - reversing yesterday's similar decline

* The U.S. dollar is mixed v. currencies

* Oil is little changed

* Gold is -$13.00 and silver is -$0.18

* Bitcoin is unchanged

As it relates to Tesla/Musk:

- Cypress Hill, Insane in the Brain

This daily Futures feature is like inside baseball. I try to show you and write about what I believe thoughtful hedge fund managers are looking at when they awake -- let's call it our normal routine -- setting the stage for their strategy for the day. The market is a complicated mosaic and the more info you have, the better trader and investor you will be!

The market (and money) never sleeps -- and neither do I, it appears! I have previously described the importance that overnight futures trading hold for me here. It is a guidepost to my strategy in the regular trading session. Moreover, the overnight/early morning futures hold opportunities as they are (1) inefficient, though liquid and (2) it seems fear and greed are often exaggerated outside the regular trading session. I frequently try to capture those efficiencies by trading actively both in the pre- and after-market sessions.

Here are brief observations I wanted to highlight and provide a summary of overnight price movements in various asset classes:

* Stock futures were up and then the gain was taken back overnight. S&P futures peaked at +24 and bottomed at -1. Nasdaq futures peaked at +141 and bottomed at +57. At 6:12 a.m. ET, S&P futures were +6 and Nasdaq futures were +92.

* Commodities are mixed to lower. Brent crude was -$0.35 to $88.08 after a brisk run higher in recent days.

* The S&P Short-Range Oscillator has moved back into a lesser oversold at -4.74% v. -5.64%

* The VIX is at 15.83 (+0.15). We have been successfully putting on straddles on VIX strength and taking off on VIX weakness.

* There is little change in the currency markets this morning.

* Interest rates are higher by about 3-4 bps across the board. The yield on the two-year Treasury is 4.941% (+3 basis points). The yield on the 10-year Treasury is +4 basis points at 4.636%. The long bond yield is +3 basis points at 4.754%.

* Overnight, the inversion of the 2s/10s Treasuries curve is down to -30 basis points.

* Gold is -$12 at $2,330. Silver is -16 cents.

Here is a synopsis of some of my columns I believe were important, or in the event you were out for the day and/or did not read my Diary. The principal intent is to review the logic of my market moves and other factors:

My Short Investment Case for Apple

Here were yesterday's trades:

* Day traded Indexes after the close for a small profit.

* Back in very small Index short calls

* Covered my DJT short

BY Doug Kass · Apr 24, 2024, 7:40 AM EDT

* I remain short of Tesla

"Smoke and mirrors" or extend and pretend?

I would argue the former - smoke and mirrors!

The "earlier than expected" launch of autonomy, Robotaxis and a low-priced auto offset the big reduction in last quarter's and future unit deliveries - as Tesla's shares rose swiftly following the after hours EPS report.

Wall Street numbers will go down measurably - yesterday's report will take billions of dollars of sales out of the sell-side estimates and take down the 2025 consensus EPS forecasts to around $3.00/share (from almost $8/share months ago).

And then there is the cash burn (h/t Jonesy at Hedgeye):

The only reason I didn't short more in the gap higher during the after hours was the magnitude of the share price decline leading up to the report.

That said, we are likely in the process in which investors begin to value Tesla more like an automobile manufacturer and less like an AI play.

This takes time - as the devotees slowly lose faith in their reasons for owning Tesla's shares.

But faith they are losing - as measured by the already sizeable absolute decline in the company's market capitalization.

Here was my Tesla Surprise in my Ten Surprises for 2024

It is revealed that Elon Musk suffers from a serious addiction. Entering an extended stay in rehab, Musk is forced to temporarily relinquish operating control over his companies. Tesla's (TSLA) shares fall back to the lows of 2023.

And, here was my Tesla surprise in my Ten Surprises for 2023

Surprise #6. Under the pressure of a further decline in Tesla's share price (to under $80/share) and Twitter's foundering fortunes, Elon Musk suffers from mental health issues and is briefly hospitalized. Upon his return, Musk reverses his decision to resign as Twitter's CEO and instead resigns his position at Tesla.

Surprisingly, under Musk's guidance, Twitter turns around and, by year end, it is debated whether Twitter is more valuable than Tesla, which is weighed down by a more challenging competitive landscape and rising customer dissatisfaction with Musk and his product.

Elon Musk admits that he is addicted to Twitter (TWTR) and liked the product so much that be purchased the company. This way, when he Tweets, he can say he is working.

Under fatigue and mental anguish, Musk is briefly hospitalized.

Though he recently announced that he is looking for a CEO to replace him, he reneges on the promise and stays on as Twitter's chief executive officer and resigns as head of his other ventures to concentrate his efforts on Twitter.

Tesla's (TSLA) shares drops badly on the announcement (to under $80/share) and, in coming months the lack of new product, increasing competition and growing customer dissatisfaction cause a demand collapse. The company's growth stalls out at a run-rate of less than two million cars and, in late 2023, factory production is reduced. In the wealthy, left-leaning population centers, driving a Tesla becomes a politically embarrassing statement and Tesla's core customer base swiftly erodes.

Musk's management of Twitter -- eliminating costs, free speech moderating -- succeeds beyond anyone's imagination. By the second half of the year it is learned that Twitter's revenues and profits achieve record results.

In late 2023 Musk is made whole as Twitter is taken public by Goldman Sachs and Morgan Stanley at an initial valuation of between $50 billion and $75 billion.

A Barron's cover story debates whether Twitter has become more valuable than Tesla.

BY Doug Kass · Apr 24, 2024, 6:45 AM EDT

Notably, S&P futures peaked at +23 handles last night - in part due to the positive response in Tesla's shares to the Musk commentary - but are now slightly lower.

Meanwhile, the S&P Short Range Oscillator slipped to -3.28% (from -6.68% last Wednesday evening) over night. Meaning the market is less oversold.

More in "Futures" column ahead.

BY Doug Kass · Apr 24, 2024, 6:35 AM EDT

“You will be much more in control if you realize how much you are not in control.”

- Benjamin Graham

Bonus - Here are some great links:

The Month of May Is Typically Weak During Election Years

BY Doug Kass · Apr 24, 2024, 6:20 AM EDT

From Charlie, here.

BY Doug Kass · Apr 24, 2024, 6:10 AM EDT

Wolf Street howls about an elongated downcycle in CRE.

BY Doug Kass · Apr 24, 2024, 6:00 AM EDT