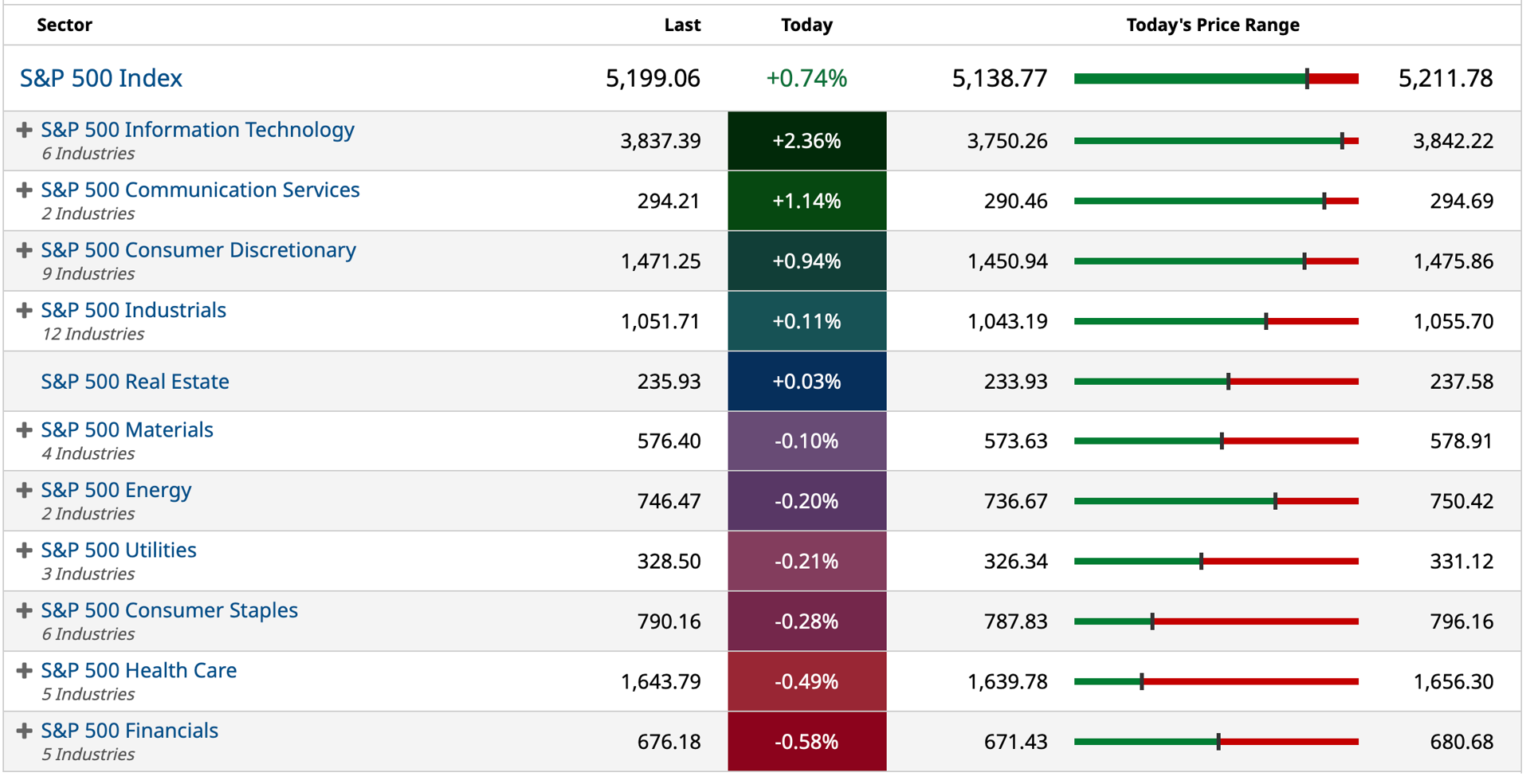

S&P Closing Sectors: Another Divergence

* You wouldn't know from the price action but six of the 11 sectors were negative.

BY Doug Kass · Apr 11, 2024, 4:59 PM EDT

* You wouldn't know from the price action but six of the 11 sectors were negative.

BY Doug Kass · Apr 11, 2024, 4:59 PM EDT

For a larger view of this table, please click here.

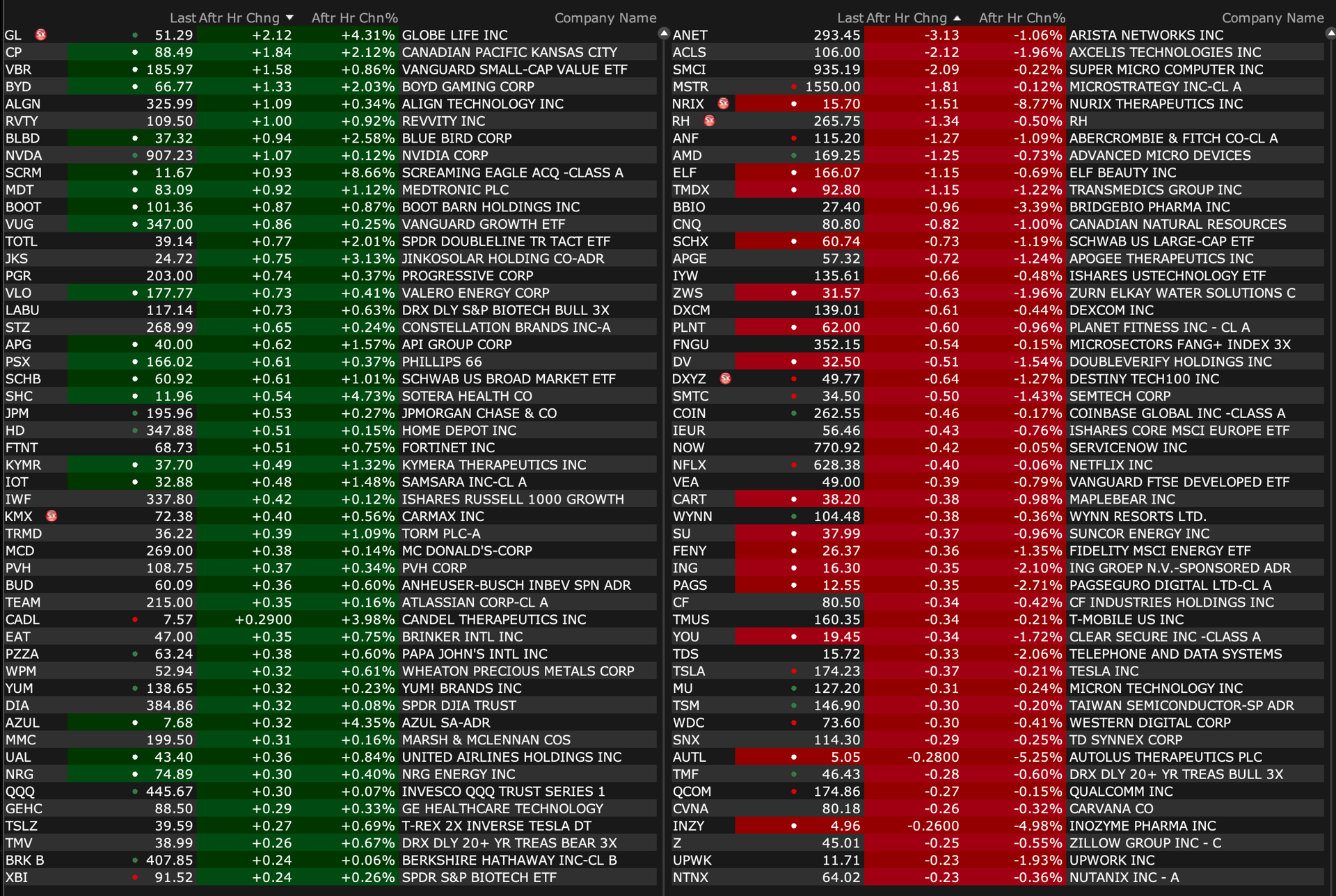

BY Doug Kass · Apr 11, 2024, 4:55 PM EDT

Adding to speculative VKTX.

Liking the risk/reward - $10 down, $70 up.

BY Doug Kass · Apr 11, 2024, 3:28 PM EDT

Starbucks price target lowered to $90 from $102 at Stifel Stifel analyst Chris O'Cull lowered the firm's price target on Starbucks (SBUX) to $90 from $102 and keeps a Hold rating on the shares. The firm evaluated year-over-year visitation performance for several restaurant chains and found mixed results among several major chains, the analyst tells investors.

While the firm's analysis confirmed comments recently made by McDonald's (MCD) and Olive Garden's (DRI) management teams, and the firm estimates that Starbucks is also seeing some challenges with lower-income consumers, several restaurant chains, ranging from Chipotle (CMG) to Chili's (EAT), appear to be performing well among this income group, the analyst noted.

Freshpet price target raised to $135 from $115 at Stifel Stifel raised the firm's price target on Freshpet to $135 from $115 and keeps a Buy rating on the shares. The firm sees upside to Q1 consensus sales expectations and thinks 31% growth is "reasonable," compared to consensus of 29%, the analyst tells investors in an analysis of sales by channel, including grocery, pet specialty, and contribution from untracked channels.

Apple price target lowered to $210 from $215 at JPMorgan JPMorgan lowered the firm's price target on Apple to $210 from $215 and keeps an Overweight rating on the shares. Contrary to the deterioration of fundamentals relative to both hardware demand as well as outlook for Services growth, interest in Apple shares has improved from the broader group of investors who have otherwise been averse to the stock's premium valuation multiple, the analyst tells investors in a research note.

The firm says iPhone sales data points are highlighting headwinds, including in China, cancellation of the future opportunity around automotive revenues, as well as downside risks to Services on account of higher regulatory scrutiny in multiple geographies are all adding to the headwinds that long-term investors are grappling. However, at the same time, hedge funds are eyeing the headwinds to create more tactical entry point ahead of the artificial intelligence upgrade cycle for Applet, adds JPMorgan.

BY Doug Kass · Apr 11, 2024, 3:10 PM EDT

The market without memory from day to day continues.

BY Doug Kass · Apr 11, 2024, 2:52 PM EDT

The FDA appears to be "jawboning" the DEA on marijuana rescheduling.

BY Doug Kass · Apr 11, 2024, 2:30 PM EDT

After the weak 3 yr and bad 10 yr Treasury auctions, the 30 yr was not good but better than the others. The yield of 4.671% was only 1 bp above the when issued as opposed to 3 seen yesterday.

The bid to cover at 2.37 was only slightly below the one year average of 2.41. And dealers were left with 17.3% of the auction, the most since last November.

Bottom line, the 30 yr maturity is for two types, one who wants a very leveraged bet on long duration and the other is for someone who wants to hold for a long time like a pension fund or insurance company.

Thus, in terms of messaging I think it’s the least helpful. That said, it was not a good one but as stated, better than the 3s and 10s. Yields aren’t moving much in response but stocks are likely breathing a sigh of relief that it wasn’t worse.

BY Doug Kass · Apr 11, 2024, 2:00 PM EDT

Here are some signposts that make me add to my short exposure:

* The continuing risk in bond yields

* Underperformance - absolute and relative - in bank stocks

* The narrowing leadership of technology, note: RSP is flat, S&P equal weighted

BY Doug Kass · Apr 11, 2024, 1:45 PM EDT

Adding to SPY short $517.81 and QQQ short $443.92.

BY Doug Kass · Apr 11, 2024, 1:35 PM EDT

* Added to May (in the money) SPY and QQQQ calls short.

* Reshorted SPY $517.50 (small).

* Reshorted QQQ $443.90.

BY Doug Kass · Apr 11, 2024, 1:25 PM EDT

Getting my sealegs back.

BY Doug Kass · Apr 11, 2024, 1:18 PM EDT

I will be back close to 1 pm!

BY Doug Kass · Apr 11, 2024, 11:40 AM EDT

8:45 AM: Fed Bank of New York President Williams (Voter) speaks before the Federal Home Loan Bank of New York 2024 Member Symposium, Metropolitan Club, NYC (Text and moderated Q&A expected. Media availability to follow);

10:00 AM: Fed Bank of Richmond President Barkin (Voter) speaks before the National Council of Textile Organizationa Annual Meeting, Washington, DC (No new text. Audience Q&A expected. No media Q&A. No livestream);

12:00 PM: Fed Bank of Boston President Collins (Non-Voter) speaks on the economy before an Economic Club of New York (Livestream and embargoed text available. Audience Q&A expected. No media Q&A);

1:30 PM: Fed Bank of Atlanta President Bostic (Voter) participates in moderated conversation on "Leadership in Financial Services" before the Urban Financial Services Coalition 50th Anniversary Celebration hosted by the Federal Reserve Bank of Kansas City, Kansas City, MO (No livestream. Audience Q&A expected. No media Q&A. No embargoed text)

BY Doug Kass · Apr 11, 2024, 10:30 AM EDT

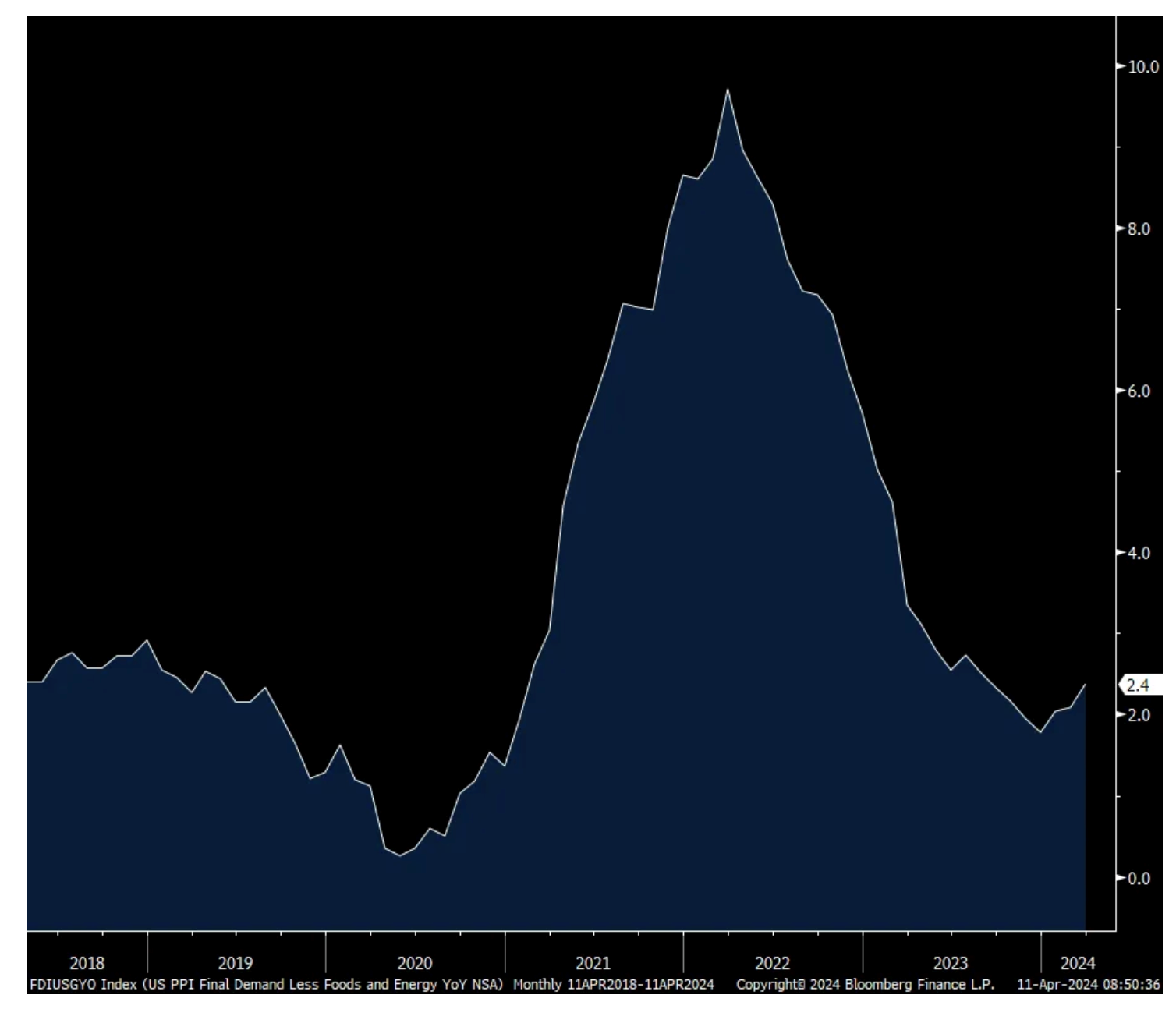

March PPI rose .2% headline and core with the former one tenth below expectations while the latter was as expected. Versus last year, wholesale prices grew by 2.1% headline and 2.4% core. Energy prices fell by 1.6% m/o/m and is down 1%, led by a drop in gasoline but I don’t see how that’s sustainable with the rise being seen.

Food prices on the other hand jumped by .8% m/o/m after a 1.1% rise in February. They are up 1% y/o/y. Chicken prices in particular jumped by 10.7% and fresh and dry vegetable prices rose.

Goods prices ex food and energy were higher by .1% m/o/m and 1.4% y/o/y with help from motor vehicles.

Service prices were up by .2% m/o/m and 2.4% y/o/y. Higher stock prices helped to drive that according to the BLS as prices for securities brokerage, dealing, investment and related services were up 3.1%. Prices rose too for professional and commercial equipment wholesaling, airline passenger services, computer/software retailing.

They fell for auto retailing, hotels, and machinery and equipment. Seemingly not yet capturing the jump in air cargo prices, the BLS said ‘air transportation of freight’ prices fell .1% m/o/m and up just .4% y/o/y. Truck transportation prices were up by .4% m/o/m but down almost 4% y/o/y.

Bottom line, the in line core number took the edge off after the more market relevant CPI with Treasury yields slightly lower post release. However, inflation breakevens are little changed, holding yesterday’s jump. At least on the goods side, if commodity prices continue higher, it will eventually be reflected in parts of the supply chain. And looking at the chart, wholesale price disinflation I believe has bottomed.

Core PPI y/o/y

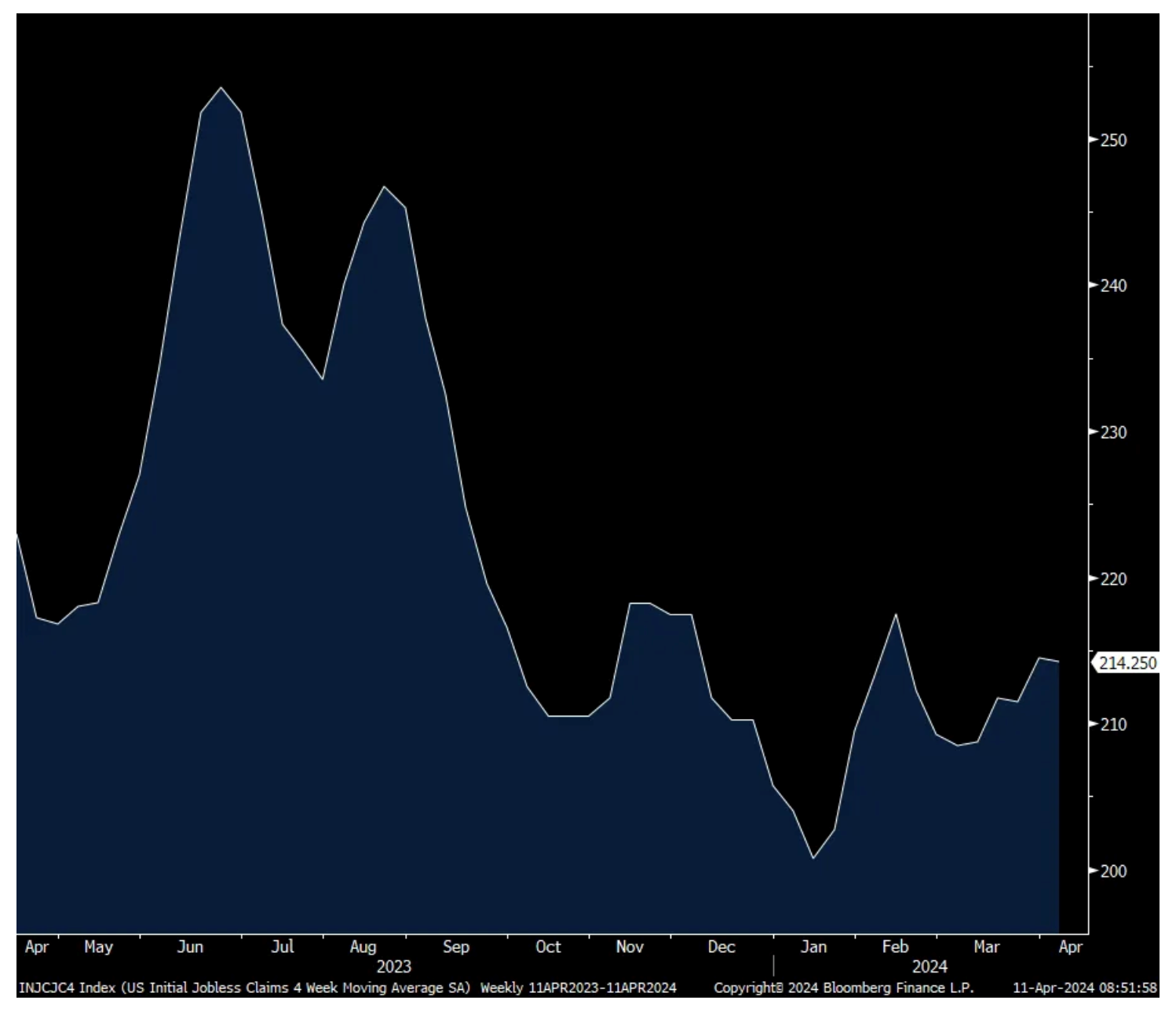

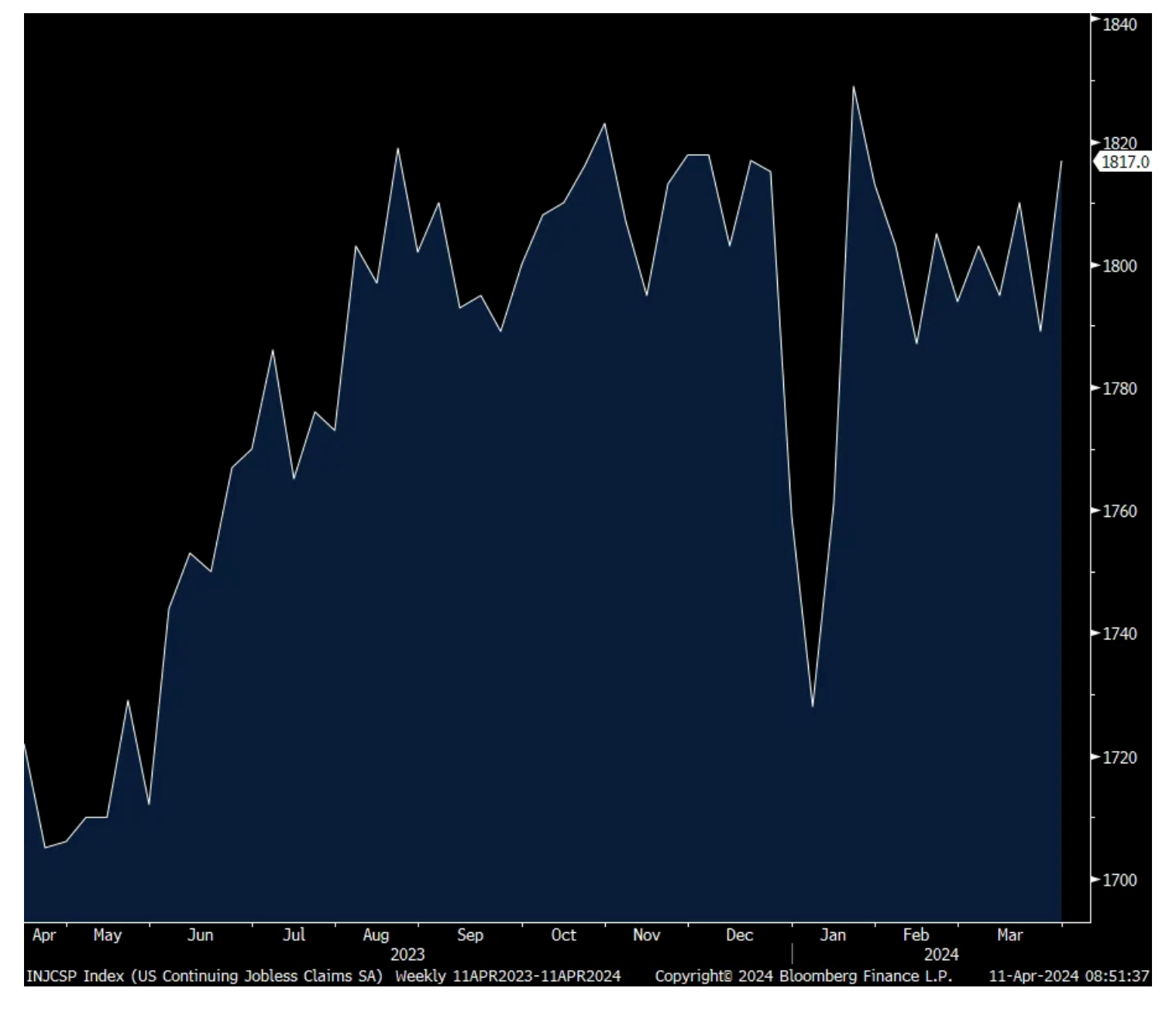

Initial jobless claims remain low, printing 211k, 4k less than expected and down from 222k last week. The 4 week average was little changed at 214k. Continuing claims on the other hand reflects the slowdown in hiring we’re seeing everywhere except in the BLS data. This figure rose to back above 1.8mm at 1.817mmk, the highest since mid January.

Bottom line, for those losing their jobs and putting aside that some are receiving severance, some are not eligible for unemployment benefits and some just don’t bother filing, the pace of firing’s as measured here remains low. But, the rate of hiring for those on benefits remains slow.

4 week avg Initial Claims

Continuing Claims

With respect to the ECB and president Lagarde’s current press conference, there is nothing yet new to report. They do though seem to be looking for every reason to cut rates in June as the European economy is “weak” said Lagarde and something we all are aware of. She also cited the slowing pace of inflation.

BY Doug Kass · Apr 11, 2024, 9:50 AM EDT

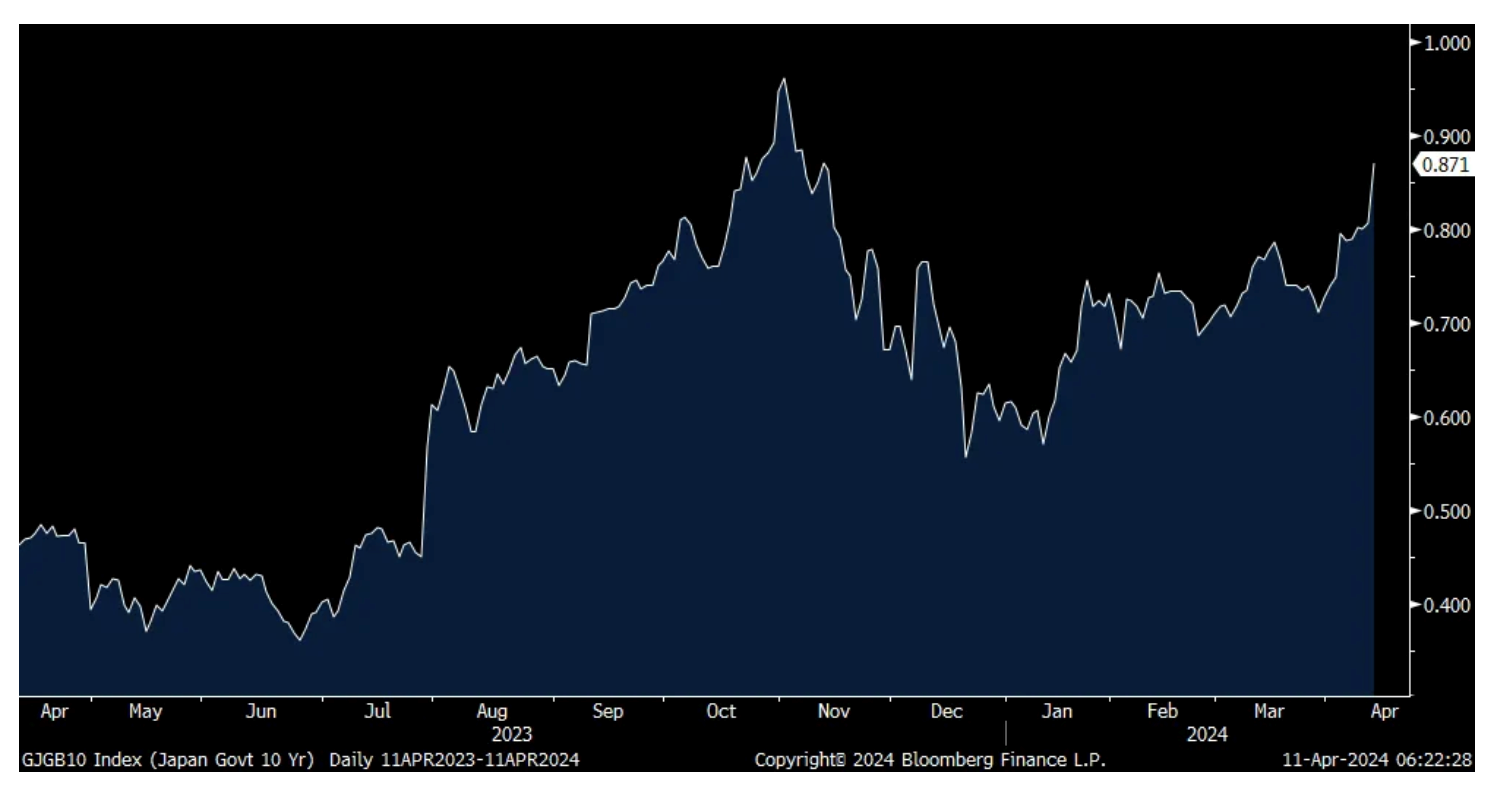

The selloff in US Treasuries yesterday went global as European bond yields rose in sympathy and Asian sovereign bonds got hit hard overnight, particularly in Japan. The 10 yr JGB yield rose 6.5 bps to .87% to the highest since mid November. The 40 yr yield jumped by 9 bps to 2.27%, a level last seen in 2011. These are big moves for the JGB market.

I'll say again, and sorry to sound hyperbolic, but the unwind of the great sovereign bond bubble that peaked when $18 trillion of negative yielding securities floated around in Europe and Japan continues on. People everyday are debating whether some stocks/AI related are in a bubble but the real bubble, that being in sovereign bonds, was epic and is popping still.

10 yr JGB Yield

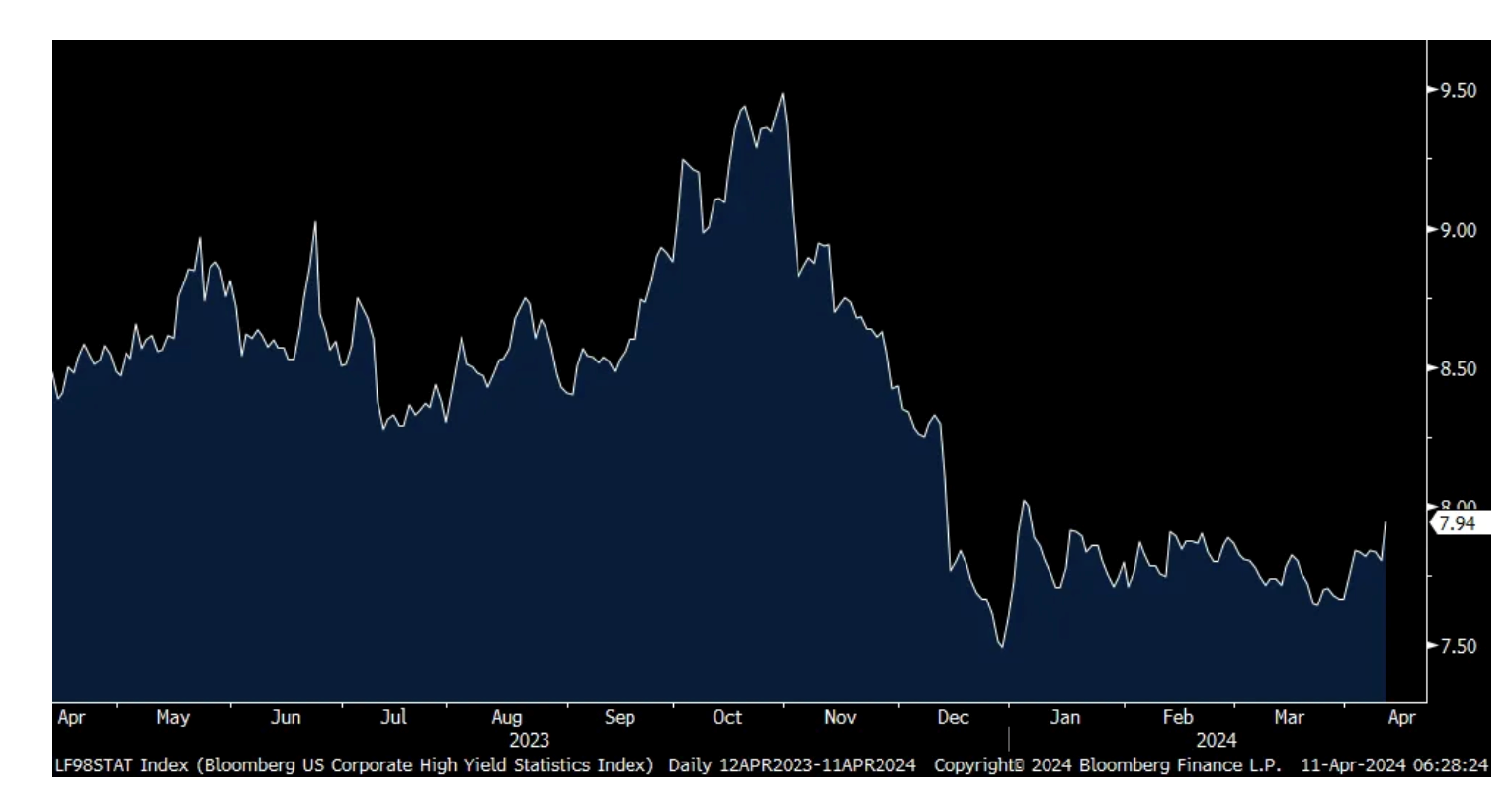

And keep your eye on corporate credit as yields rise here too, though after a ferocious rally. Here is a chart of the yield on the Bloomberg high yield index, it closed last night at the highest level since early January at just under 8%, though spreads remain tight.

Bloomberg High Yield

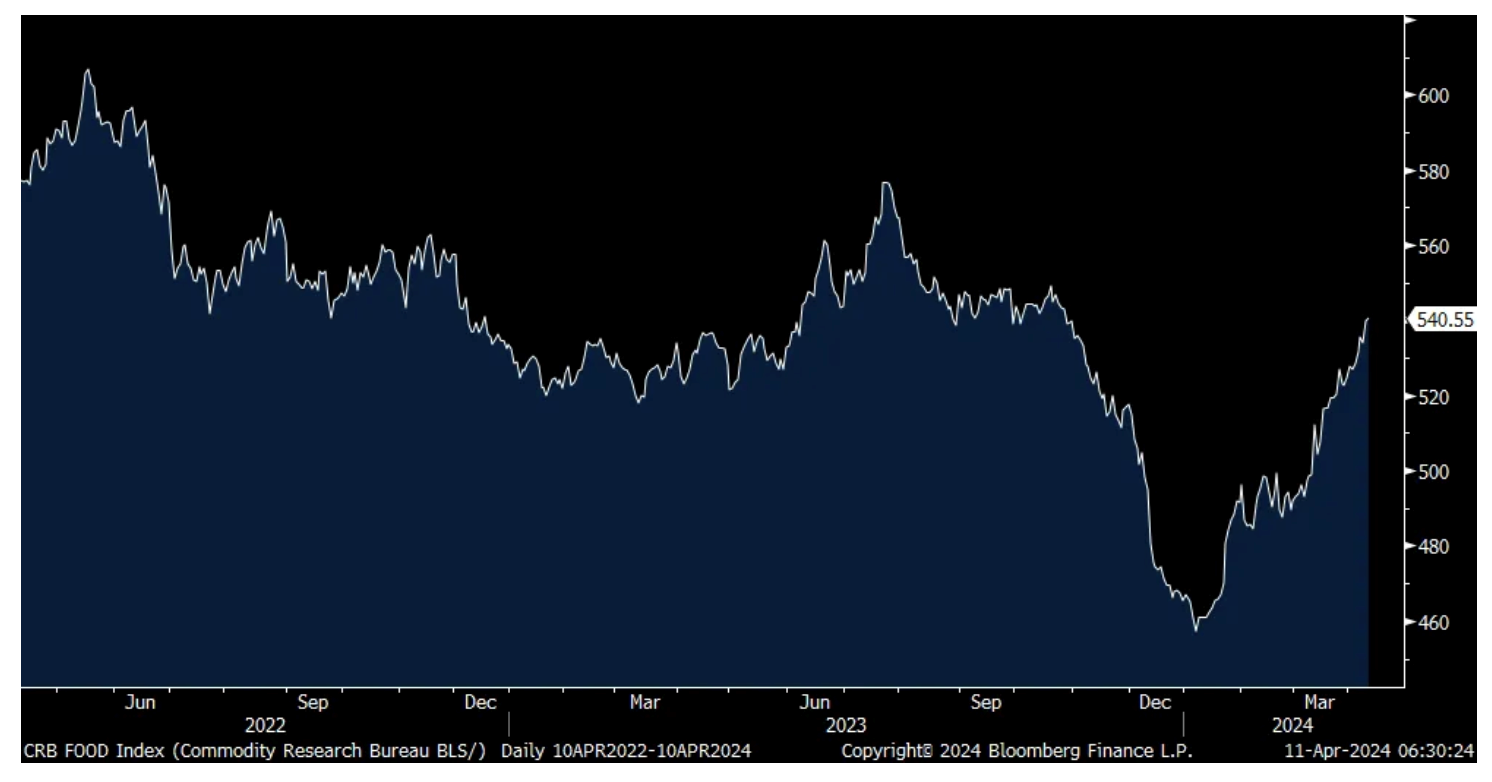

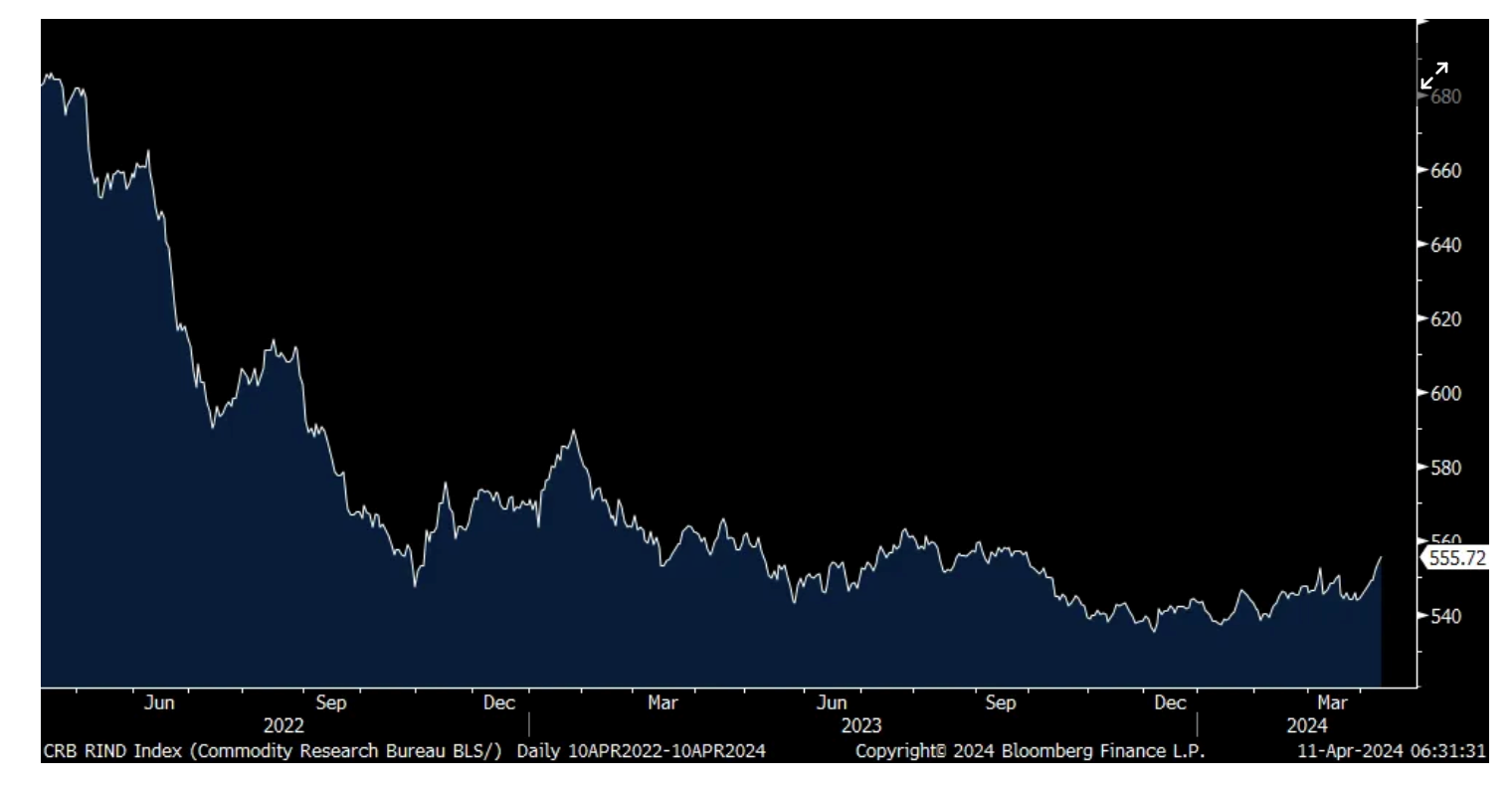

Inflation breakevens in the TIPS market yesterday jumped not only because of the CPI report but because commodity prices continued to rise. The CRB Food Stuff index closed yesterday at the highest level since late October. The CRB Raw Industrials index rose .30% yesterday to the highest since September, though still well off its highs. It's up in 11 out of the last 12 days. We remain bullish and long a variety of commodity stocks, including the precious metals, as you likely already know as I've talked about it seemingly forever.

As for those inflation breakevens, they were up 9 bps yesterday for the 2 yr to 2.90%, a 13 month high. The 5 yr was up 5 bps to 2.54%, also a 13 month high. The 10 yr was up 4 bps to 2.40%, a 5 month high.

Ahead of the ECB meeting today where no rate change is expected but they can't wait to cut in June, the 5 yr 5 yr euro inflation swap is at the highest since December.

I want to say this about inflation breakevens in the TIPS market and the rate cut/hike odds that we all keep talking about priced into the swaps/fed funds futures market. They reflect how market participants/traders feel today about what will take place but those feelings change everyday depending on what data/Fed comments come our way. So predictive in a sense that people are placing their daily bets but predictions that remain dynamic each day.

CRB Food Stuff Index

CRB Raw Industrials Index

The Bank of Canada did nothing yesterday as expected but is also looking for space to cut in June, though that remains uncertain. Governor Macklem said "We are seeing what we need to see, but we need to see it for longer to be confident that progress toward price stability will be sustained." With regards to a June rate cut, "Yes, it's within the realm of possibilities" Macklem said in answering a question.

Delta said this on their earnings call and its a particular area of continued strength in what is a very mixed economy:

"Demand continues to be strong and we see a record spring and summer travel season with our 11 highest sales days in our history, all occurring this calendar year. Spending on services recently surpassed goods for the first time in five years and there is further runway to return to their long term trends.

"Delta's core consumers are in a healthy position and travel remains a top purchase priority. Generational shifts and evolving consumer preferences are driving secular growth in premium experiences. And business travel demand has taken another meaningful step forward this year with growth accelerating into the mid-teems over last year." The CEO ended this view all bulled up by saying "this may be the most constructive backdrop that I've seen in my airline career."

Fastenal just reported and missed by a touch both top and bottom line relative to expectations. They are a great tell on the state of the industrial side of the US economy. They mentioned "weakening end markets." But, "while our non-residential and reseller end markets remain relatively weak, they are beginning to come across easier comparisons in the preceding periods."

With inflation, where overall goods prices are back to zero y/o/y: "Incremental pricing actions over the past 12 months have been modest in scope, resulting in mostly stable price levels through the first quarter of 2024."

Carmax missed badly both its top and bottom line, its stock is down sharply pre market, and said this: "We believe affordability challenges continued to impact our 4th quarter unit sales performance, with ongoing headwinds due to widespread inflationary pressures, higher interest rates, tightened lending standards and low consumer confidence."

Off an uber extreme bullish reading last week, Investors Intelligence said Bulls fell to 58.1 from 62.5 and almost all went to the Correction side as Bears rose just .4 pts to 14.5. The Bull/Spread of 43.6 remains above the extreme threshold of 40. In today's AAII, Bulls fell by 3.9 pts to 43.4 and back to where it was 3 weeks ago. Bears were up by 1.8 pts to 24 and its spread to the Bull camp remains wide.

Bottom line, as seen too with the Citi Panic/Euphoria index which rose to Euphoria territory, when sentiment is all in one direction, from a contrarian perspective it creates tinder for something out there to change trend. Yesterday's CPI report and the global jump in interest rates might have been that spark to cool the giddy mood.

Moving overseas, China's CPI was up .1% y/o/y, below the estimate of up .4% but lower food prices remains the main reason. Prices ex food and energy were higher by .6% y/o/y which is not much different than the trend seen over the past year. Price stability actually. PPI was as expected, down 2.8%. With the rise in commodity prices, maybe a bottoming in global manufacturing trends (I emphasize 'bottoming' but not yet a recovery), and easier comparisons, this should start inflecting higher this year.

Chinese stocks were mixed overnight and did not follow the US selloff. The Shanghai comp was up .2% while the H share index and the Hang Seng were down just .2% each. My long Hang Seng trade is finally in the green, though barely, after the brutal start to the year.

BY Doug Kass · Apr 11, 2024, 9:30 AM EDT

I got sick on the commute back and forth from NY yesterday so I will be visiting my doctor for a prescription at 10 am.

BY Doug Kass · Apr 11, 2024, 9:20 AM EDT

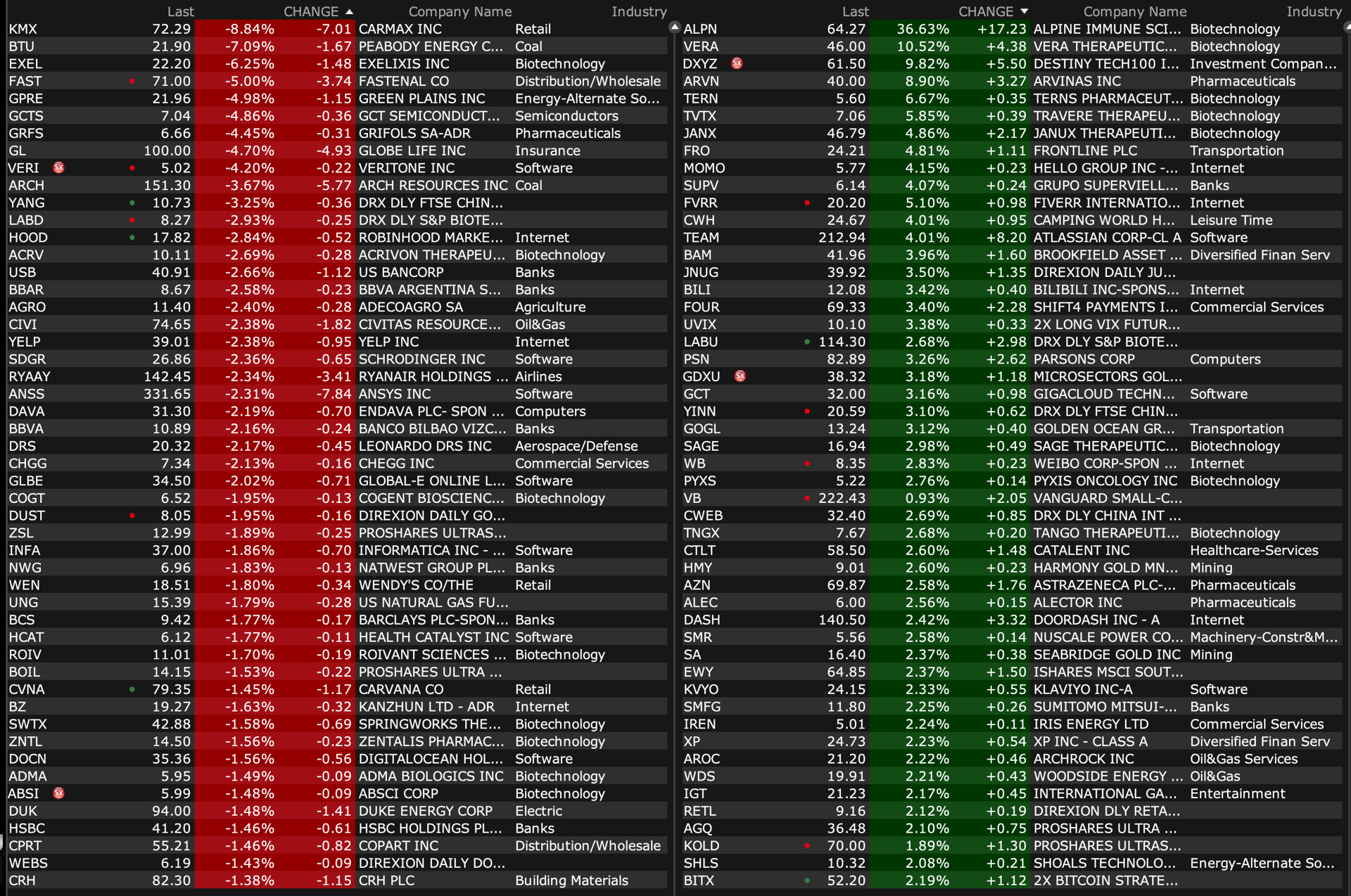

Upside

-RLYB +91% (to collaborate with Johnson & Johnson to advance therapeutic solutions for pregnant individuals at risk of Fetal and Neonatal Alloimmune Thrombocytopenia)

-ELYM +57% (to acquire privately held Tenet Medicines in all-stock deal; announces concurrent $120M private placement)

-ALPN +37% (Vertex enters into agreement to acquire Alpine Immune Sciences for $65/shr in cash, valuing it at $4.9B)

-RENT +34% (earnings, guidance)

-LPTX +11% (files to sell $40M private placement)

-NKGN +7.9% (secures additional financing of $5M to continue advancing its clinical programs)

-BW +6.5% (raises FY guidance; files to sell $50M on behalf of B. Riley Securities, Inc., Seaport Global Securities LLC, Craig-Hallum Capital Group LLC and Lake Street Capital Markets, LLC)

-ARVN +5.5% (enters global license agreement with Novartis for development and commercialization of PROTAC Androgen Receptor (AR) Protein Degrader ARV-766 for treatment of prostate cancer)

-INDP +5.0% (presents positive Mechanism of Action Data at the American Association for Cancer Research Annual Meeting)

-KORE +4.9% (earnings, guidance)

-INBP +4.5% (subsidiary Intelligent Fingerprinting Limited broadens IP portfolio with grant of new European patent with unitary effect for innovative intelligent fingerprinting DSR-plus cartridge reader)

-CRMD +4.0% (announces abstracts at upcoming Society for Healthcare Epidemiology of America Conference)

-TEAM +3.1% (Barclays Raised TEAM to Overweight from Equal Weight, price target: $275)

-LPCN +2.5% (announces positive LPCN 2401 clinical results showing improved body composition in participants with obesity)

-RELL +2.3% (earnings)

Downside

-APVO -59% (prices $4.6M public offering; selling 3.4M common shares at $1.35/shr)

-LOVE -19% (earnings, guidance)

-ONCY -8.9% (advances toward registration-enabling trial for Pelareorep in breast cancer with submission of Type C Meeting request to FDA)

-KMX -8.2% (earnings, guidance)

-BTU -5.6% (reports prelim Q1 metrics)

-FAST -4.6% (earnings, guidance)

-PCSA -3.8% (presents two abstracts at the AACR Annual Meeting 2024 including new data on the NGC-Cap Phase 1b Trial)

-HOOD -3.7% (CitiGroup Cuts HOOD to Sell from Neutral, price target: $16)

BY Doug Kass · Apr 11, 2024, 9:10 AM EDT

BY Doug Kass · Apr 11, 2024, 9:00 AM EDT

To view this chart in a new window, click here.

BY Doug Kass · Apr 11, 2024, 8:52 AM EDT

* As Mr. Market's elevated valuation meets the reality of prickly inflation...

* The Fed's 2024 narrative that inflation was coming under control is as feckless and wrong-footed as its 2021 narrative that inflation would be transitory

Baroness Elsa Frankenstein: Listen to me, Frank. I saw my father become obsessed by his power. He died a horrible death, just as my grandfather did.

Dr. Frank Mannering: Yes, I know.

Baroness Elsa Frankenstein: You promised the people to rid Vasaria of his monstrous creation. I want to be sure that nothing, nothing whatsoever, can sway you. It is in your hands to undo the crimes my father and grandfather committed. We must clear the name of Frankenstein.

- "Frankenstein Meets the Wolf Man"

"Frankenstein Meets the Wolf Man" is an iconic 1943 horror film starring Lon Chaney Jr. as Larry Talbot (The Wolf Man) and Bela Lugosi as Frankenstein's monster.

The script, written by Curt Siodmark, follows "The Ghost of Frankenstein" and "The Wolf Man." In the movie, Talbot only transforms into werewolf form during a full moon (rather than every night while wolfsbane is in bloom, as in The Wolf Man), which became a standard part of werewolf lore. The film centers on Talbot, who is brought back to life when his tomb is disturbed and his search for a way to end his seeming immortality, which leads to his befriending Frankenstein's monster.

There were some possible tipoffs to yesterday's market schmeissing -- my "Sell, Mortimer! Sell" column covered many of my continuing concerns, as did my April 1 Trade of the Week to sell short SPY/QQQ:

* Financials began to conspicuously underperform earlier in the week:

BY DOUG KASS APR 9, 2024 10:10 AM EDT

Weak Financials

Today is the first day in several weeks that financials have been weaker in a strong tape.

I am not certain what that means, though.

Position: Short XLF (M)

* The slow but persistent rise in interest rates was ignored as animal spirits and FOMO were emotional factors that captured all the available air in the investing room:

* We were at a bullish sentiment extreme. From Peter Boockvar:

I'm going to start with stock market sentiment, which I usually do on Thursday's after I see both the Investors Intelligence and AAII surveys, because the weekly Citi Panic/Euphoria index I see via Barron's on Saturday's has entered Euphoria and at .40 is the highest since mid January 2022 (and which spent almost the entire year in the Euphoria category in 2021 so tough to time).

The importance of this survey according to Citi itself is while it is a "gauge of investor sentiment" like others, "It identifies 'Panic' and 'Euphoria' levels which are statistically driven buy and sell signals for the broader market. Historically, a reading below panic supports a better than 95% likelihood that stock prices will be higher one year later, while euphoria levels generate a better than 80% probability of stock prices being lower one year later."

So, as markets are higher most of the time and Citi has statistical metrics that say there is "a better than 80% probability of stock prices being lower one year later" when Euphoria has been realized, we should all take note. As stated though, it was very euphoric all throughout 2021 and markets kept elevating (though the most speculative stuff peaked in February 2021) so no one can be sure of the timing of when this matters but for those of us managing other people's money and in the risk management business, we should take heed. Especially when we combine this with the more than 40 point spread in II between Bulls and Bears which rarely occurs.

* Geopolitical concerns were growing. (See the rising tension between Israel and Iran)

* And, then, of course was the solar eclipse!

But, seriously... risk happens fast.

We have argued that, against interest rates, equities are more overvalued than at any time in the last two decades. I used as an example of this the thinnest equity risk premium since 2007.

Moreover, short-dated Treasuries have been providing a risk-free and reasonable return against stocks, especially with the S&P 500 dividend yield of only 1.35% compared to 1.47% last month and 1.66% last year and lower than the long-term average of 1.84%.

All we needed was a catalyst to redirect the markets back to reality. That reality, as also captured in the last few months in my Diary, was a likely reacceleration in inflation that produced the worst one-day selloff in Treasuries in almost two years.:

Source: Hedgeye

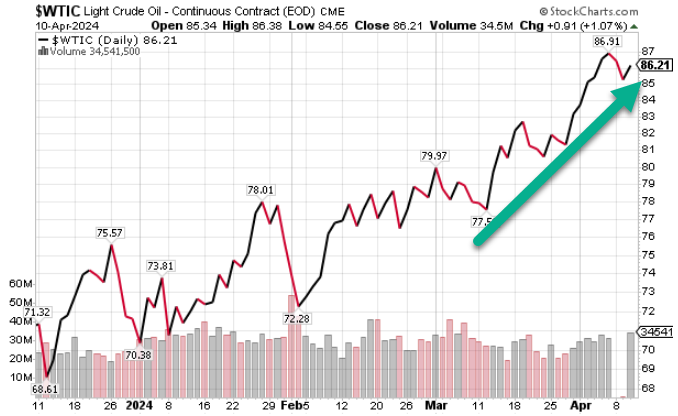

Crude, in particular, was marching higher.:

Source: Hedgeye

That came at 830 a.m. Wednesday morning, with the hot March inflation print.

President Ronald Reagan was right when he said, "Inflation is a tax. In fact, inflation is the cruelest of taxes."

Risk happens fast.

BY Doug Kass · Apr 11, 2024, 8:20 AM EDT

* Frankenstein met the Wolf Man on Wednesday - as both equities and fixed income got schmeissed

* The Oscillator has moved from overbought to oversold -- to -0.86% from 0.81%

* Bond yields fell modestly overnight after yesterday's large climb in yields, with declines of 1-2 bps

* The U.S. dollar is slightly weaker against the yen

* Oil is down (-$0.54) after this week's ramp higher - Brent is at $89.94

* Gold is +$6 following a move to all-time highs... silver is +$0.03

* Bitcoin is +$300 to $70.4k

* Chart of the Day:

* Stagflation lies ahead:

I won't wear makeup on Thursday

I'm sick of covering up

I'm tired of feeling so broken

I'm tired of falling in love

Sometimes I'm shy, and I'm anxious

Sometimes I'm down on my knees

Sometimes I try to embrace all my insecurities

So I won't wear makeup on Thursday

'Cause who I am is enough

- Thursday, Jess Glynne

"Workin' on our night moves Trying to lose the awkward teenage blues Workin' on our night moves In the summertime And oh the wonder Felt the lightning And we waited on the thunder Waited on the thunder."

- Bob Seger, "Night Moves"

This daily Futures feature is like inside baseball. I try to show you and write about what I believe thoughtful hedge fund managers are looking at when they awake -- let's call it our normal routine -- setting the stage for their strategy for the day. The market is a complicated mosaic and the more info you have, the better trader and investor you will be!

The market (and money) never sleeps -- and neither do I, it appears! I have previously described the importance that overnight futures trading hold for me here. It is a guidepost to my strategy in the regular trading session. Moreover, the overnight/early morning futures hold opportunities as they are (1) inefficient, though liquid and (2) it seems fear and greed are often exaggerated outside the regular trading session. I frequently try to capture those efficiencies by trading actively both in the pre- and after-market sessions.

Here are brief observations I wanted to highlight and provide a summary of overnight price movements in various asset classes:

* Stock futures were flat most of the evening but began to tail off at around 5 am. S&P futures peaked at +27 and bottomed at -19. Nasdaq futures peaked at +22 and bottomed at -53. At 7:08 am ET, S&P futures were -15 and Nasdaq futures were -41.

* Commodities are higher. Brent crude -$0.50 to $90 -after a brisk run higher in recent days.

* The S&P Short-Range Oscillator has moved back into negative territory (oversold) - from 0.81% to -0.86%

* The VIX is at 16.44 (+0.64). I reestablished some straddles on the recent VIX run over 15 .

* The U.S. dollar is weaker against the yen and pound but stronger v. euro.

* Interest rates are now flattish. The yield on the two year Treasury is 4.97% (unchanged). The yield on the 10 year Treasury is also flat at 4.554%. The long bond is at 4.643% (no change). Gilts +5 bps.

* Overnight, the inversion of the 2s/10s Treasuries curve is back up to -42 basis points

* Gold is +$7.70 and sits at $2,355. Silver - on everyone's radar now - is +$0.04 to $28.09

Here is a synopsis of some of my columns I believe were important, or in the event you were out for the day and/or did not read my Diary. The principal intent is to review the logic of my market moves and other factors:

I didn't write on Wednesday

Here were yesterday's trades:

* Added to private equity shorts - they were downside features on Wednesday

* Added to short Index calls

* Day traded (profitably) Indexes common

BY Doug Kass · Apr 11, 2024, 7:55 AM EDT

From my pal and best-selling author Larry McDonald:

BY Doug Kass · Apr 11, 2024, 7:10 AM EDT

* The herd of "groupstink" is near unanimous in the view that the market's advance is broadening.

* The only thing that broadened yesterday was the breadth and magnitude of the decline in equities...

From yesterday:

SPY -1.23%

QQQ -1.12%

RSP (Equal Weighted S&P) -1.90%

IWM -2.94%.

BY Doug Kass · Apr 11, 2024, 6:56 AM EDT

"If you need to ask someone whether we’re in a bear market, we’re not."

- Walt Deemer

Bonus - Here are some great links:

Inflation Fight - Far From Over

BY Doug Kass · Apr 11, 2024, 6:45 AM EDT

BY Doug Kass · Apr 11, 2024, 6:25 AM EDT

From Rick Rieder:

BY Doug Kass · Apr 11, 2024, 6:15 AM EDT

From my friends at Miller Tabak:

Wednesday, April 10, 2024

Although the March CPI report is disappointing, markets are again overreacting. In late 2023, we warned readers that inflation would tick back up as productivity growth reverts to normal. The bad news is that while this is proving correct, we underestimated the magnitude. We expected core-inflation readings, ex-shelter, to rise to around 3%, but the past three months of core-CPI, ex-shelter: 2.5%, 3.6%, and 3.8% are even higher. This will slow the Fed down. Given the solid economic outlook, the FOMC can afford to wait until either GDP growth falls below 2% or inflation declines before it starts cutting. We expect this to happen by July. We now predict 25 bps cuts in July, November, and February, a one-meeting delay from our previous view of June, September, and December. This implies only two cuts this year.

Figure 1: Core-CPI (Blue), Supercore-CPI (Green) and Core-Services, ex-shelter (red)

Another aspect of the March data that will bother the FOMC is the continuing gap between inflation in services versus goods. Higher core-inflation in March was entirely driven by services with core-services, ex-shelter, coming in at 8.0%, and goods showing a continuing deflation. Some FOMC members have worried that service inflation is especially persistent. We disagree. This gap is simply part of consumers’ ongoing shift towards services, and we are confident that it will dissipate by the end of 2024.

There is, however, good news in the recent inflation data. A closer look at the January and February data (which we discuss below) shows that higher inflation is coming from supply rather than demand factors. This fits with out view that the near-record productivity growth of 2023 led to inflation readings that were better than they seemed, but that slowing productivity growth is now creating readings that are worse than they appear. We expect that this is also true with the March data. Supply-driven inflation is far less likely to persist than demand-driven inflation and the bigger picture of the FOMC beginning a rate cut cycle later this year that takes the Fed Funds rate to 275-300 bps in 2026 is unaffected.

BY Doug Kass · Apr 11, 2024, 6:05 AM EDT

Wolf Street howls about the spike in interest rates.

BY Doug Kass · Apr 11, 2024, 5:55 AM EDT