Interesting Cannabis Post

BY Doug Kass · Mar 26, 2024, 5:25 PM EDT

BY Doug Kass · Mar 26, 2024, 5:25 PM EDT

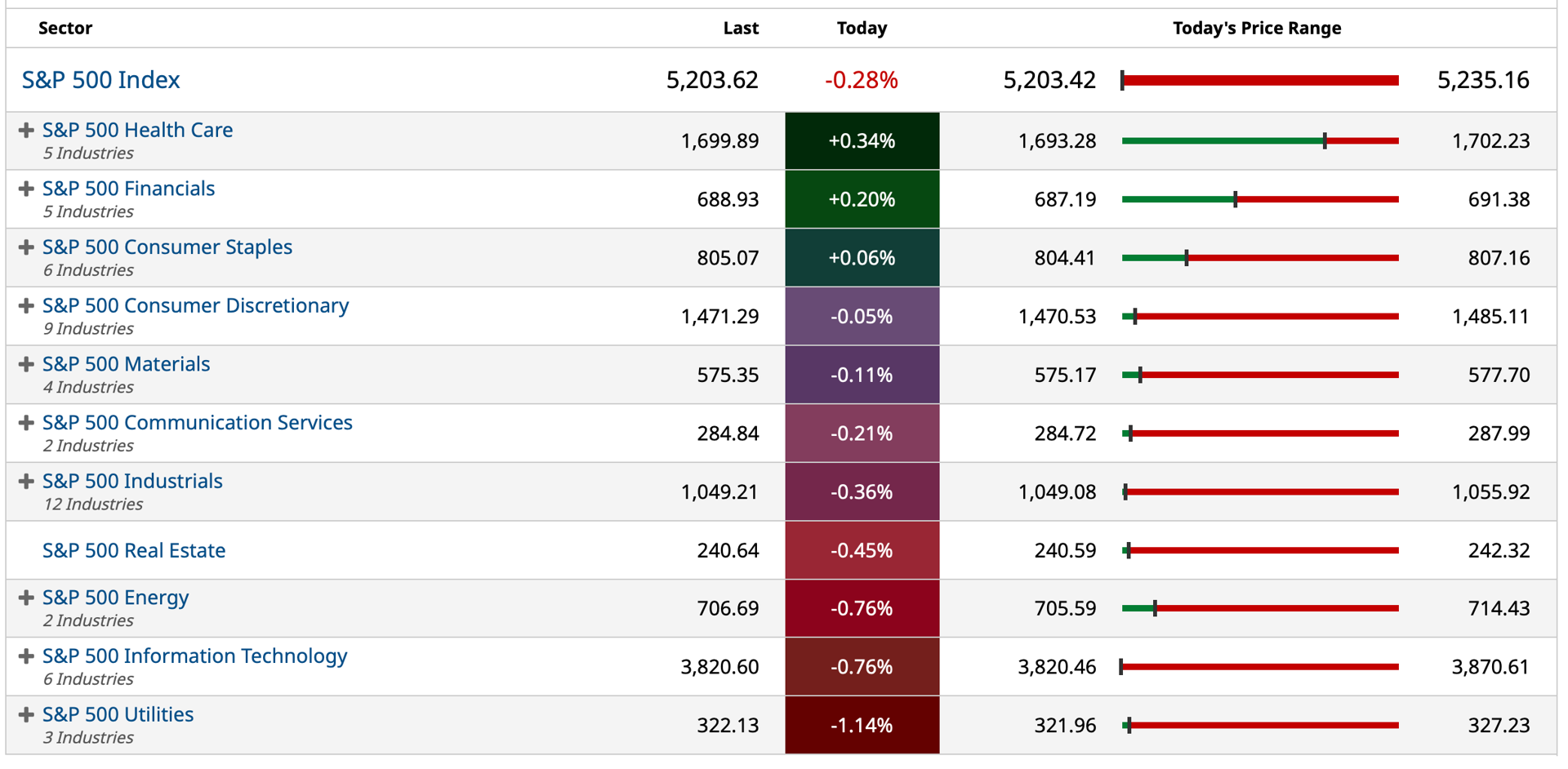

All go out near day low but for Financials and Healthcare

BY Doug Kass · Mar 26, 2024, 5:16 PM EDT

- NYSE volume 353M shares, 26% below its one-month average;

- NASDAQ volume 4.14B shares, 5% below its one-month average

- VIX up 0.68% to 13.28

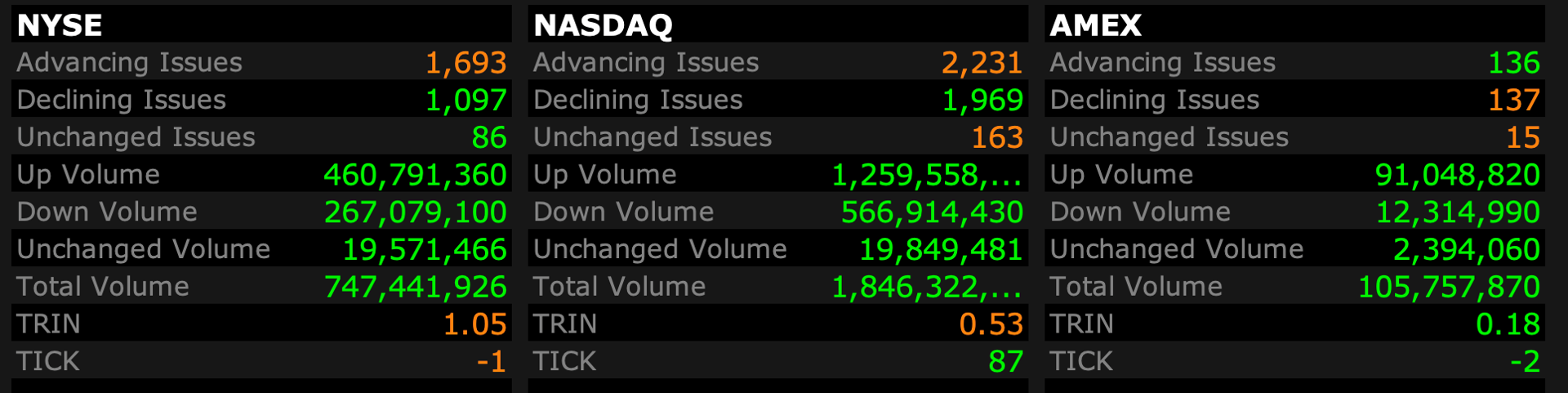

Breadth

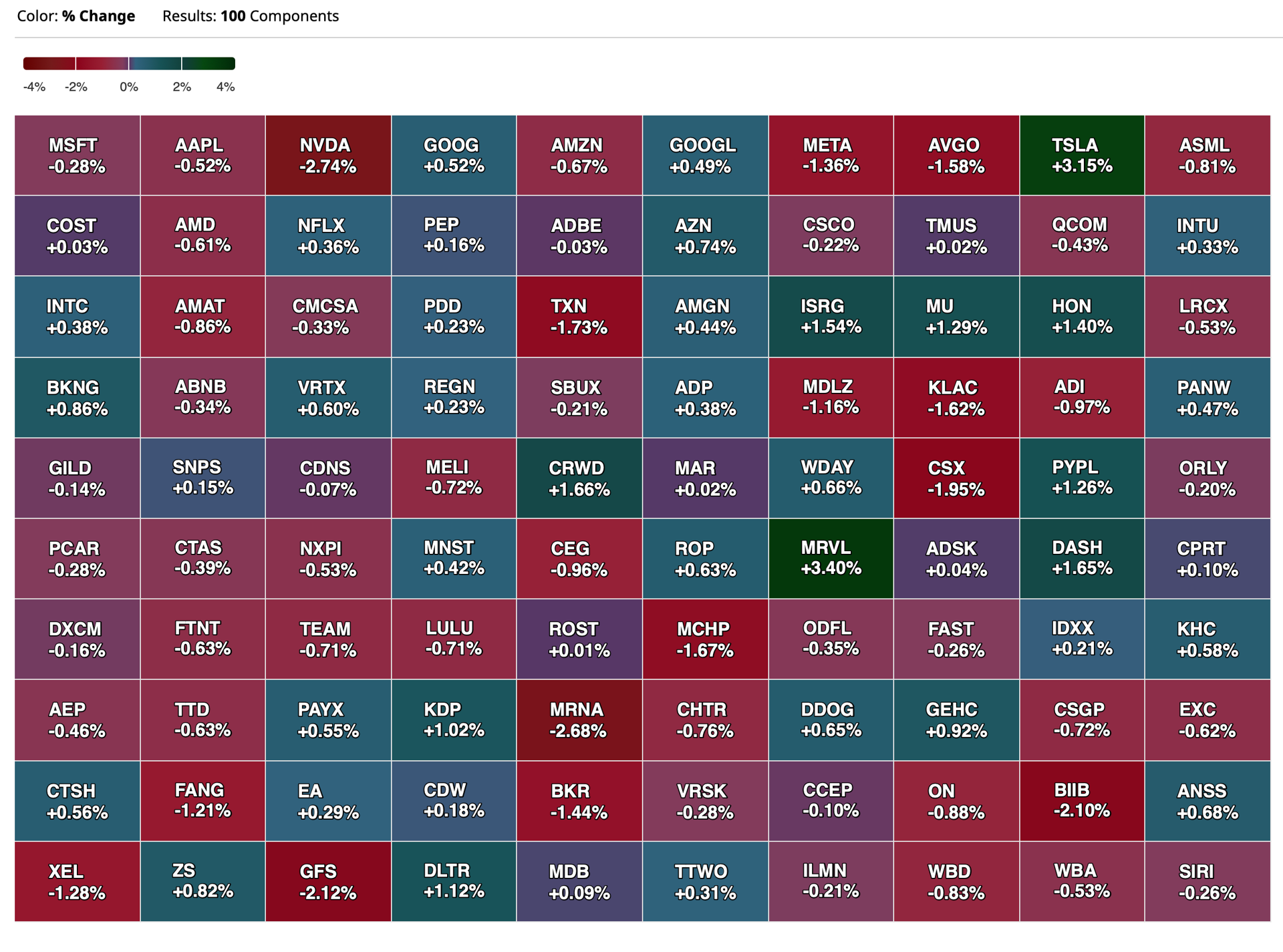

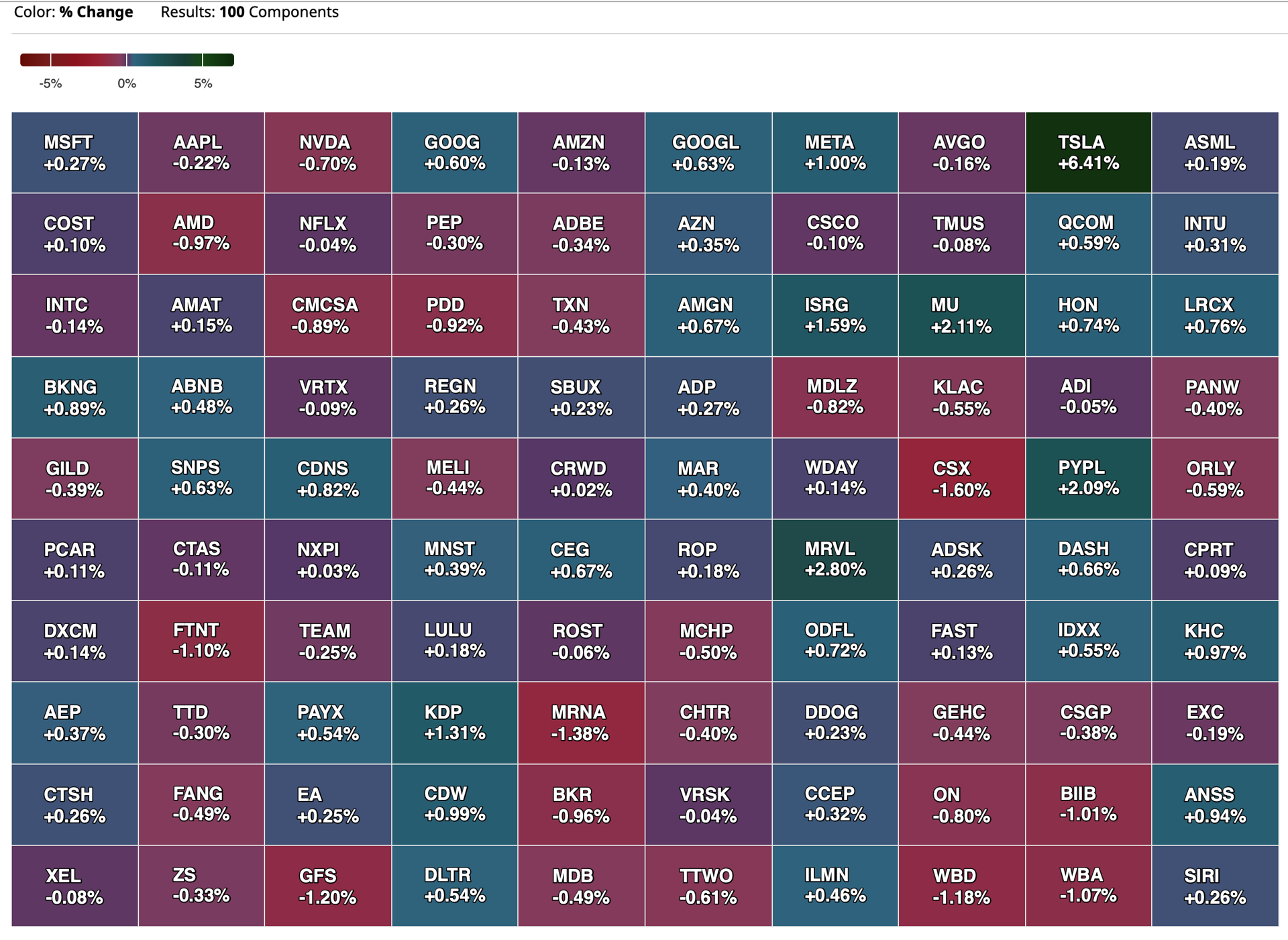

Nasdaq 100 Heat Map

BY Doug Kass · Mar 26, 2024, 5:02 PM EDT

For a larger version of this table, please click here.

BY Doug Kass · Mar 26, 2024, 4:54 PM EDT

All day long I have observed to my hedge fund's CEO, Scott, that the market "finally" looks like it was struggling a bit.

As Grandma Koufax used to say, "Dougie, last words are for fools who haven't said enough!"

Or was that Karl Marx?

BY Doug Kass · Mar 26, 2024, 3:35 PM EDT

Biden races to shift marijuana policy ahead of election.

BY Doug Kass · Mar 26, 2024, 3:14 PM EDT

Florida bankers say passage of SAFE Act for cannabis clients is in sight.

BY Doug Kass · Mar 26, 2024, 2:40 PM EDT

Here you go!

BY Doug Kass · Mar 26, 2024, 2:25 PM EDT

It's a quiet day trading as I continue to spend most of my time on researching new ideas.

Stay tuned.

BY Doug Kass · Mar 26, 2024, 1:25 PM EDT

Doomberg on "The Energy War Goes Kinetic"...

BY Doug Kass · Mar 26, 2024, 12:05 PM EDT

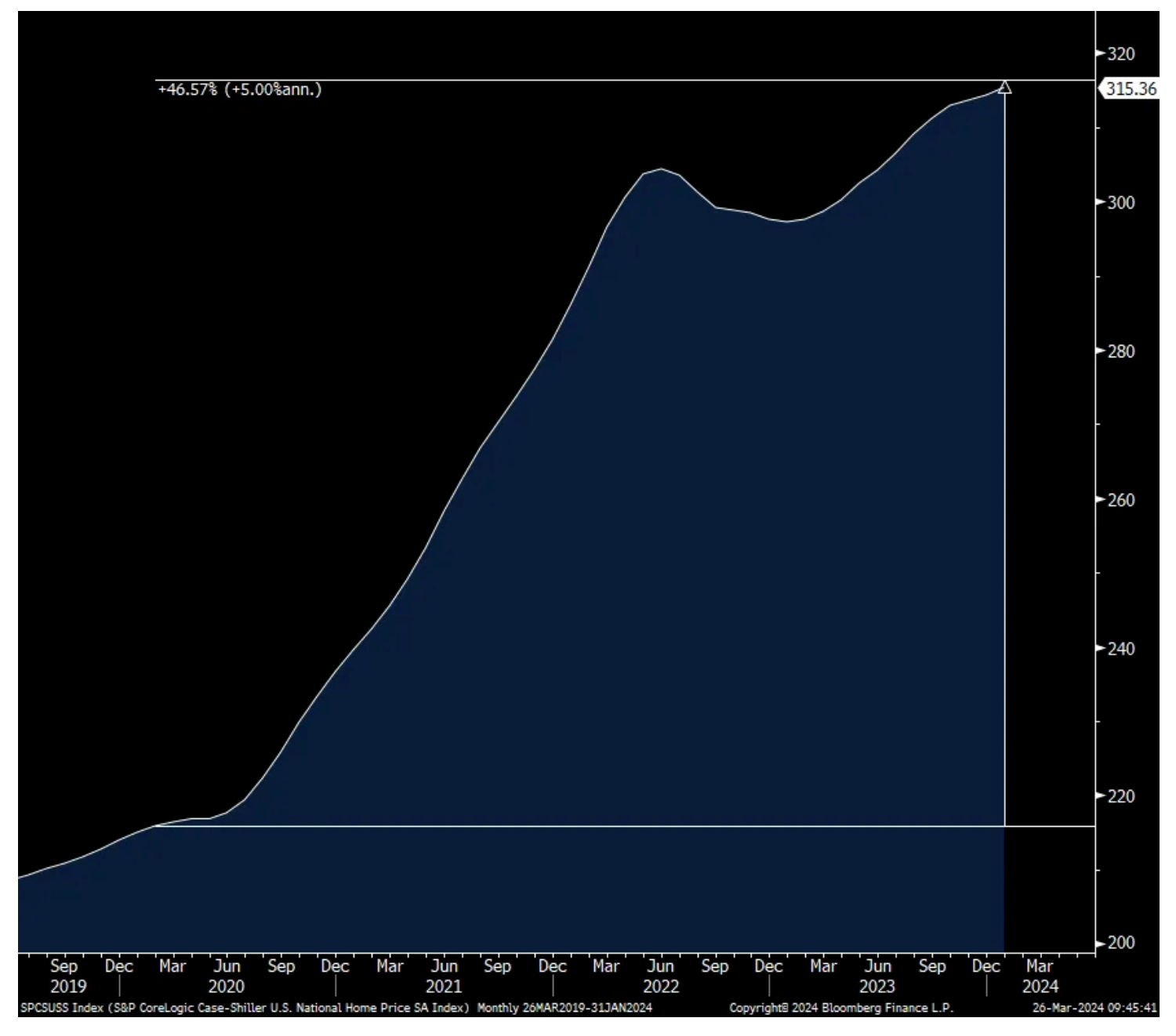

The deflationistas are sure lucky that rents are captured in CPI and PCE and not home prices. Since February 2020, right before the Federal Reserve went all in with QE and zero rates, the S&P CoreLogic home price index is up 46%. Owners Equivalent Rent is up "just" 22%. And the bulk of that home price rise happened before the Fed started hiking rates and was clearly in response to the buying of MBS and zero rates.

In other words, inflation would have been well into the double digits if home prices were the measure and the Fed was the cause of it. To those in Congress who think the housing market needs lower rates to ease affordability constraints don’t realize the main cause of the unaffordable challenges in housing over the past 20 years was easy money and that any savings on the mortgage rate side will be completely offset by even higher home prices.

The housing market needs to work through all the low cost mortgages and baby boomers need to downside in order to create more housing supply. That’s the cure but will take years to play out. Sorry to those looking for a quick fix.

In January, S&P CoreLogic said home prices rose 6% y/o/y, making a purchase for a young family even more expensive and why all those new apartments coming on line this year will be well absorbed.

S&P CoreLogic Home Price Index

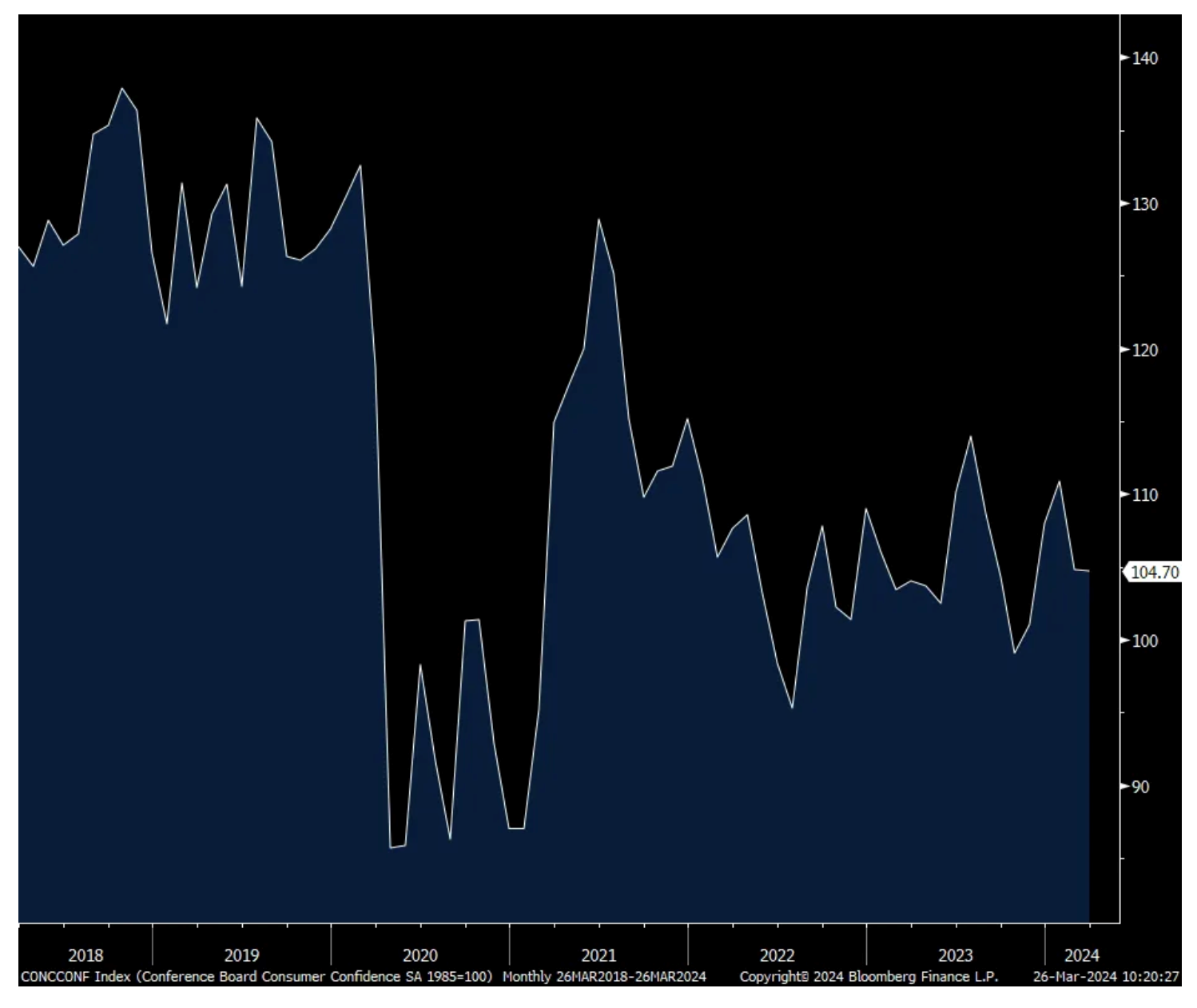

The March consumer confidence index as taken by the Conference Board was 104.7 and below the estimate of an increase to 107 from a downwardly revised 104.8 in February (from 106.7 initially). The components were mixed as the Present Situation was higher m/o/m but expectations fell. One yr inflation expectations were 5.3% vs. 5.2% in February and 5.3% in January.

The answers to the labor market questions were mixed with those saying jobs were "Plentiful" higher and "Hard To Get" falling. But, when looking out 6 months, those seeing ‘more jobs’ fell to the lowest since May 2023 and is just .1 pt from the least since 2016. Those expecting higher income rose .2 pts after a .8 pt drop last month.

Spending intentions were mixed too with a slight rise in plans to buy a car and home but a drop in plans to purchase a major appliance which fell to the lowest since July 2022.

Here was the bottom line from the Conference Board after citing the better current assessment but weaker expectations:

“Confidence rose among consumers aged and over but deteriorated for those under 55. Separately, consumers in the $50,000-$99,999 income group reported lower confidence in March, while confidence improved slightly in all other income groups. However, over the last six months, confidence has been moving sideways with no real trend to the upside or downside either by income or age group.” I bolded for emphasis.

Here’s more, “Consumers remained concerned with elevated price levels, which predominated write-in responses. March’s write-in responses showed an uptick in concerns about food and gas prices.”

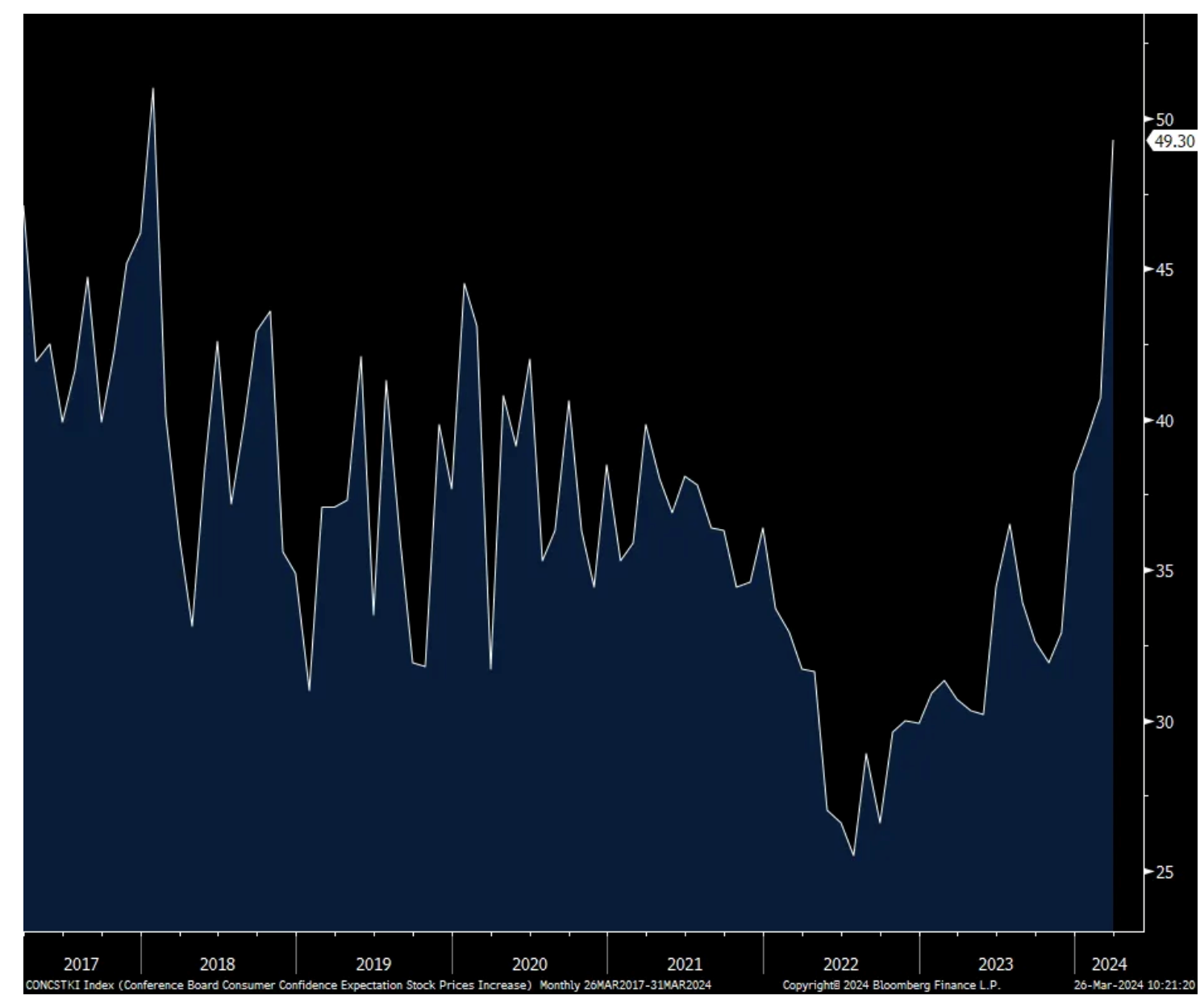

Finally, we can add another negative contrarian indicator as those who think stock prices will increase in the coming 6 months rose to the highest level since January 2018 (right after the corporate tax cut was signed and markets went straight up in 2017 in anticipation). Interestingly too, I’ve cited a few examples over the past two months of stocks going parabolic and this component itself has as well.

UoM

Expect Higher Stock Prices in Coming 6 Months

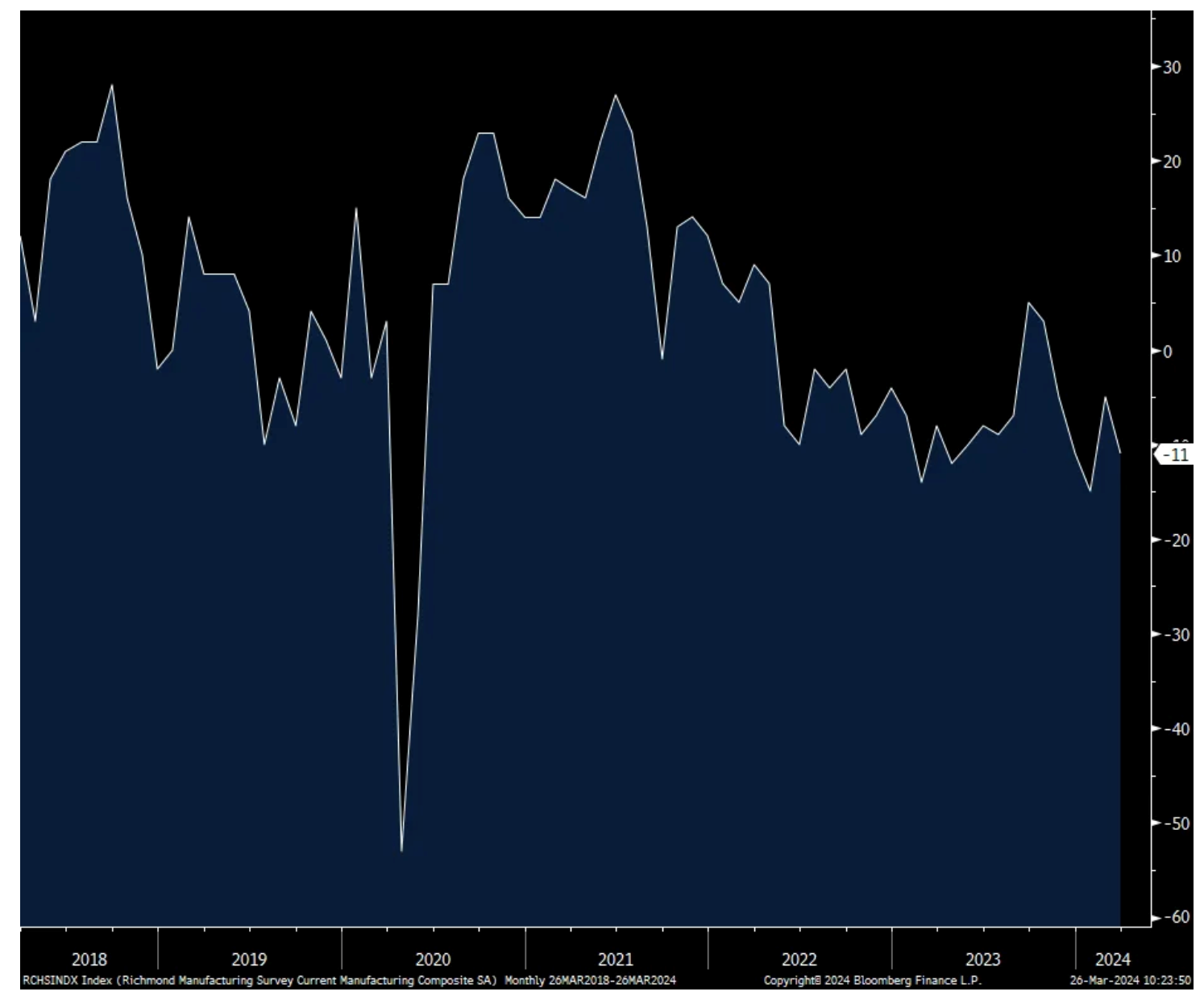

Lastly, the Richmond manufacturing survey joins NY and Dallas in still seeing contraction in activity. The March print was -11 vs. -5 in February and vs. the estimate of no change. The components are so volatile month to month that I will spare you more details.

Richmond Mfr’g

BY Doug Kass · Mar 26, 2024, 11:50 AM EDT

- NYSE volume 110M shares, 34% below its one-month average

- Nasdaq volume 1.57B shares, 5% above its one-month average

- VIX down 1.29% to 13.02

Breadth

Nasdaq 100 Heat Map

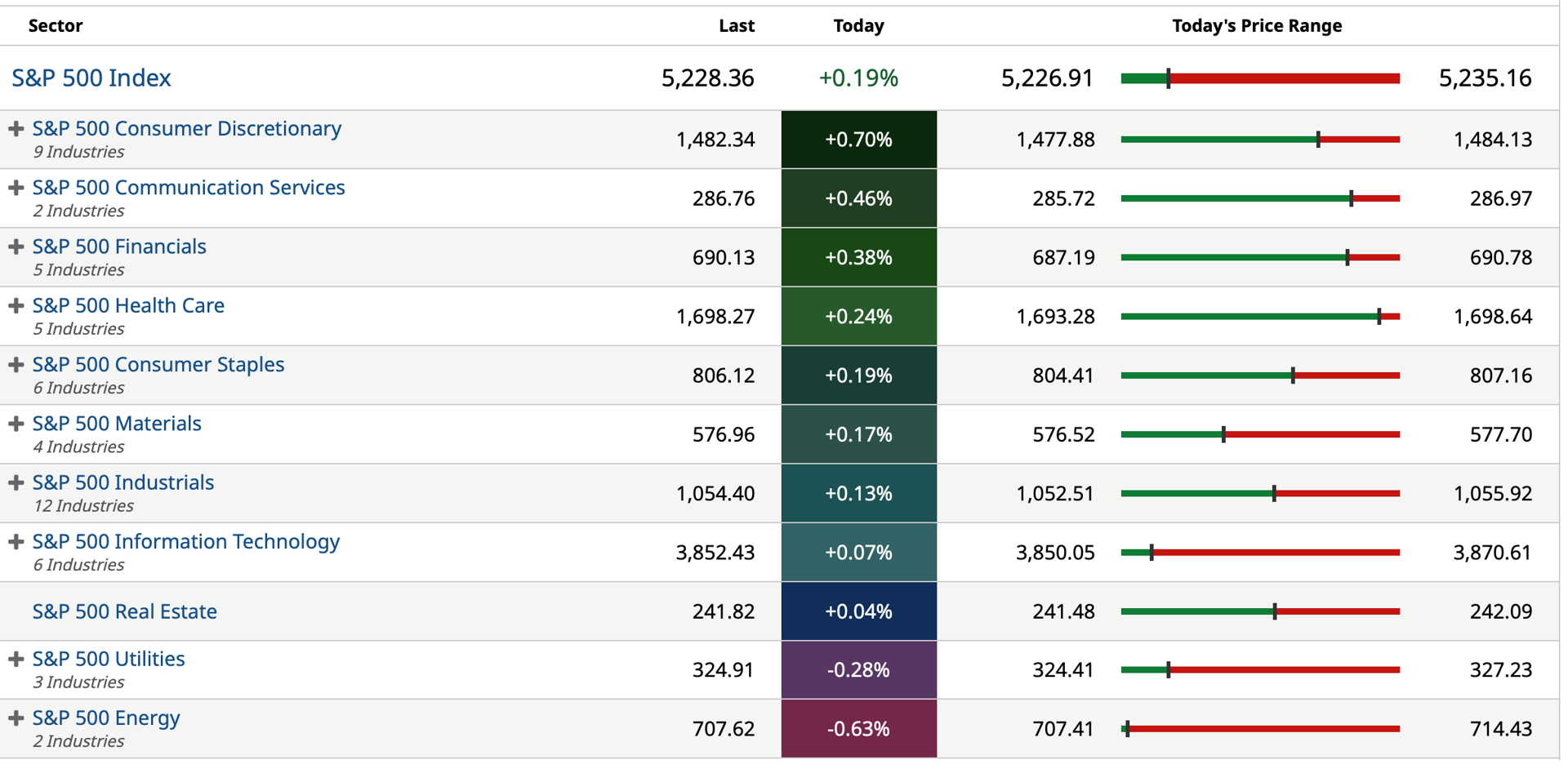

S&P 500 Sectors

BY Doug Kass · Mar 26, 2024, 11:33 AM EDT

From Charlie, see here.

BY Doug Kass · Mar 26, 2024, 10:55 AM EDT

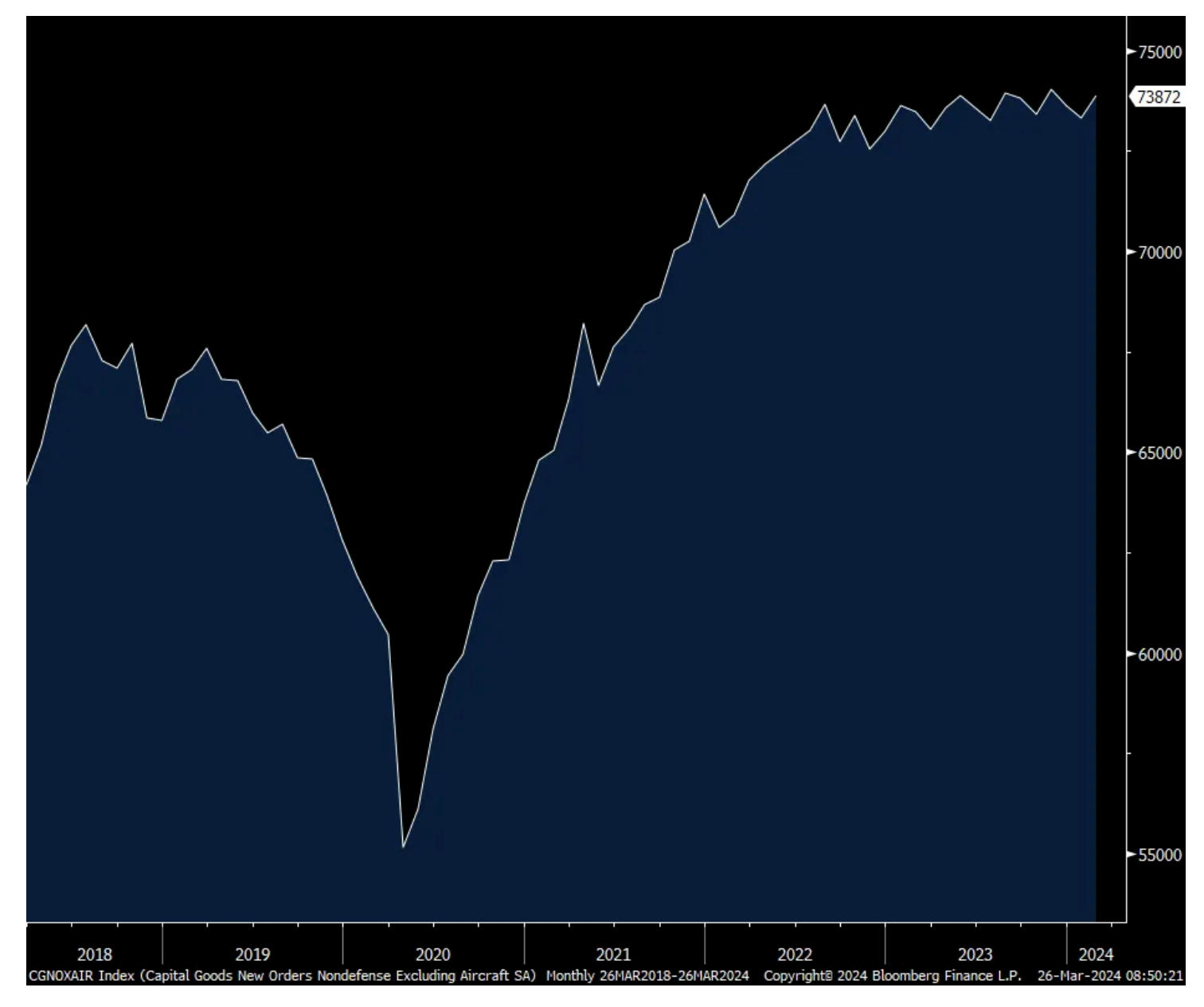

Core durable goods orders in February were a touch above expectations when we include the downward revision to January. We might though see a trimming of Q1 GDP estimates as core shipments were light with an unexpected drop in February of 4 tenths vs the estimate of up one tenth.

The internals were mixed with a lift in orders for vehicles/parts after a combined decline in the two prior months. Orders rose for machinery too but after 4 months of declines. After the drop in January, orders for metals rose. After the rise in January, orders for computers/electronics and electrical equipment was lower.

I’ll chime in for a second on IT spend based on what I’ve heard from the tech related conference calls over the past month. Stating the obvious, there has been an enormous rise in spend on anything AI related but what we’re seeing is the IT spending pie though is not really growing much as there is more of shift in spend from other things in order to pay for AI stuff.

Bottom line, core durable goods orders in dollar and nominal terms has been flat lining since August 2022 as interest rates inflected higher and down in REAL terms.

Core Durable Goods orders, in dollar/nominal terms

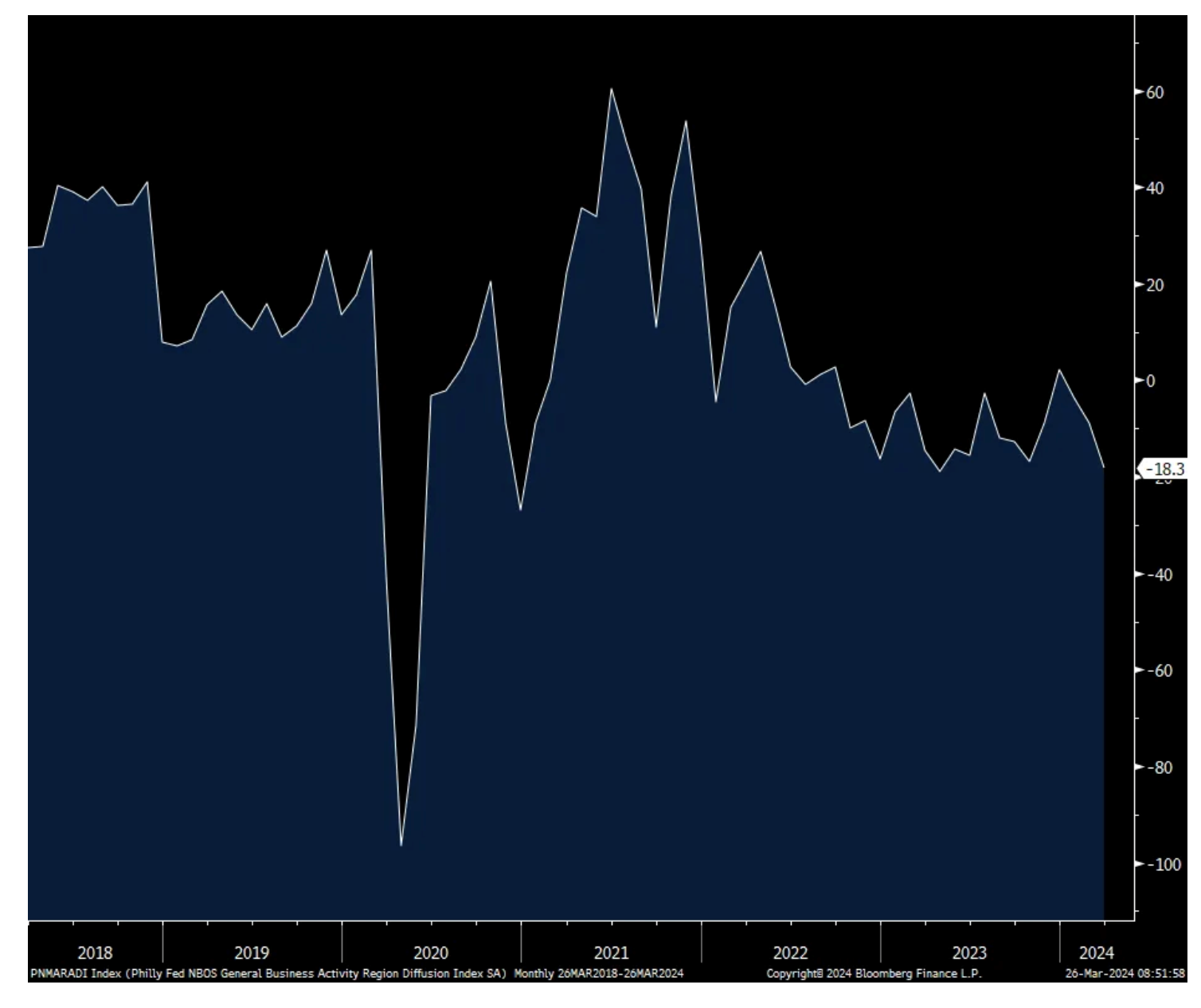

As its relatively new, there isn’t a long track record but the March Philly non-manufacturing index was not good, coming in at -18.3 from -8.8. It’s been negative for 17 out of the last 18 months in order to confuse us even more about the state of the US economy. While prices paid fell, prices received rose to the highest since last May.

Philly Non-mfr’g index

BY Doug Kass · Mar 26, 2024, 10:25 AM EDT

Covering more WBA and SNBR now - as both stocks are approaching my downside targets.

BY Doug Kass · Mar 26, 2024, 10:15 AM EDT

I added small to AdvisorShares Pure US Cannabis ETF MSOS on weakness this morning.

BY Doug Kass · Mar 26, 2024, 10:00 AM EDT

BY Doug Kass · Mar 26, 2024, 9:50 AM EDT

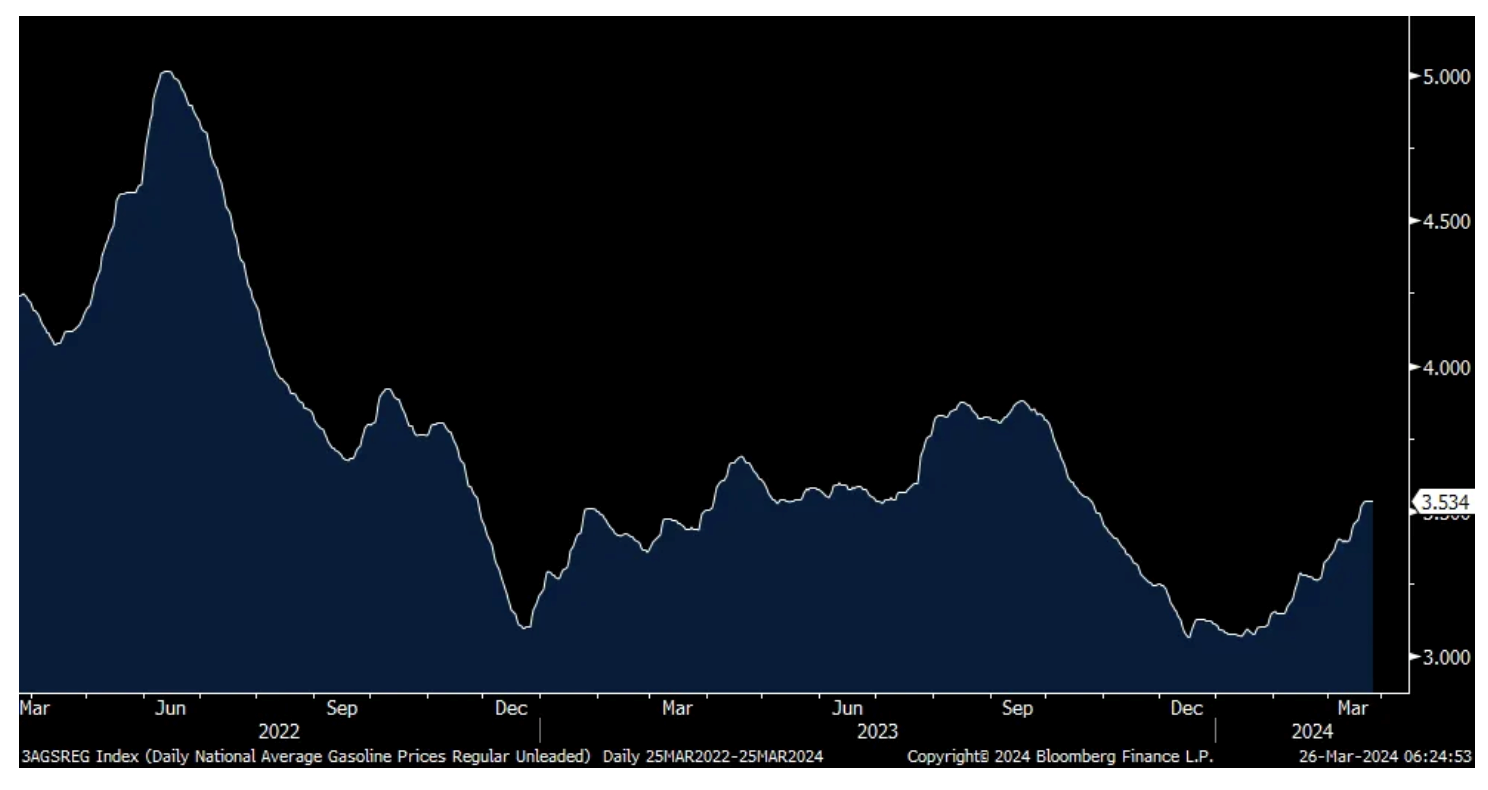

With the average gallon of gasoline at the highest level since October and higher by almost 3% y/o/y according to AAA, a Bloomberg News article yesterday cited AAA's estimate for where prices can go this summer during the summer travel season. It's $4, which if seen would be the most expensive since August 2022.

Let's hope they are wrong since the US consumer is already showing some shaky knees, especially the lower to middle income one, when seeing and listening to both the retail sales data and what we heard from a variety of retailers and restaurant companies over the past month.

They cite low inventories and "Attacks on Russian refineries have taken about 600,000 barrels a day of capacity" off the market and we know commodities are fungible. Also, "maintenance at US refineries and unexpected outages caused by leaks and fires also have had an impact on supplies and prices.

Avg Gallon of Gasoline

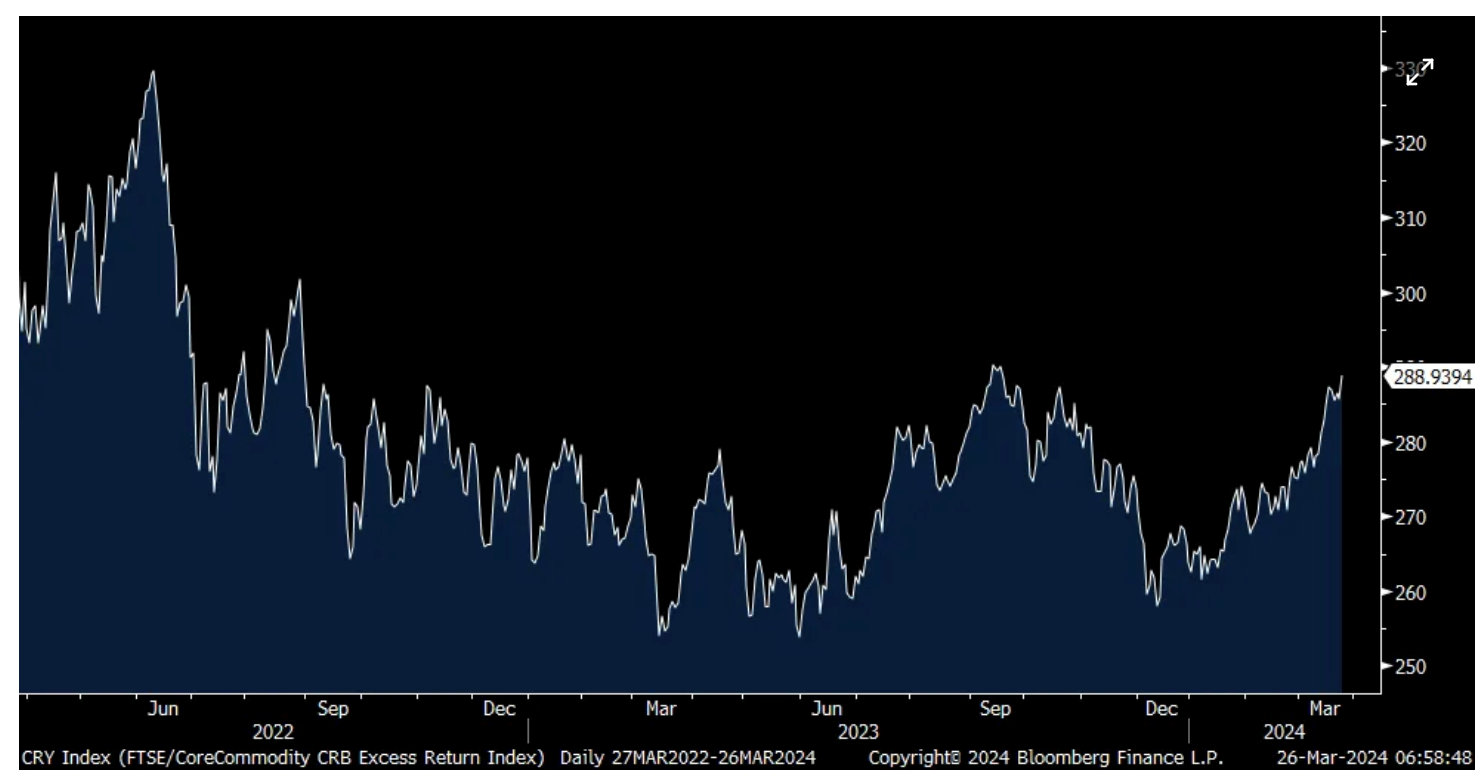

With another spike in cocoa prices (was up 8% yesterday and by another 4% today), along with other soft commodities, the CRB Food Stuff index was higher by another 1.3% yesterday. It's now up y/o/y and it's the last thing food companies, restaurants and consumers need right now as traffic and volumes are more squishy. And, the overall CRB index is within less than 1% of the highest closing print since August 2022, the last thing the Federal Reserve wants to see just as Powell gets dovish.

CRB Index

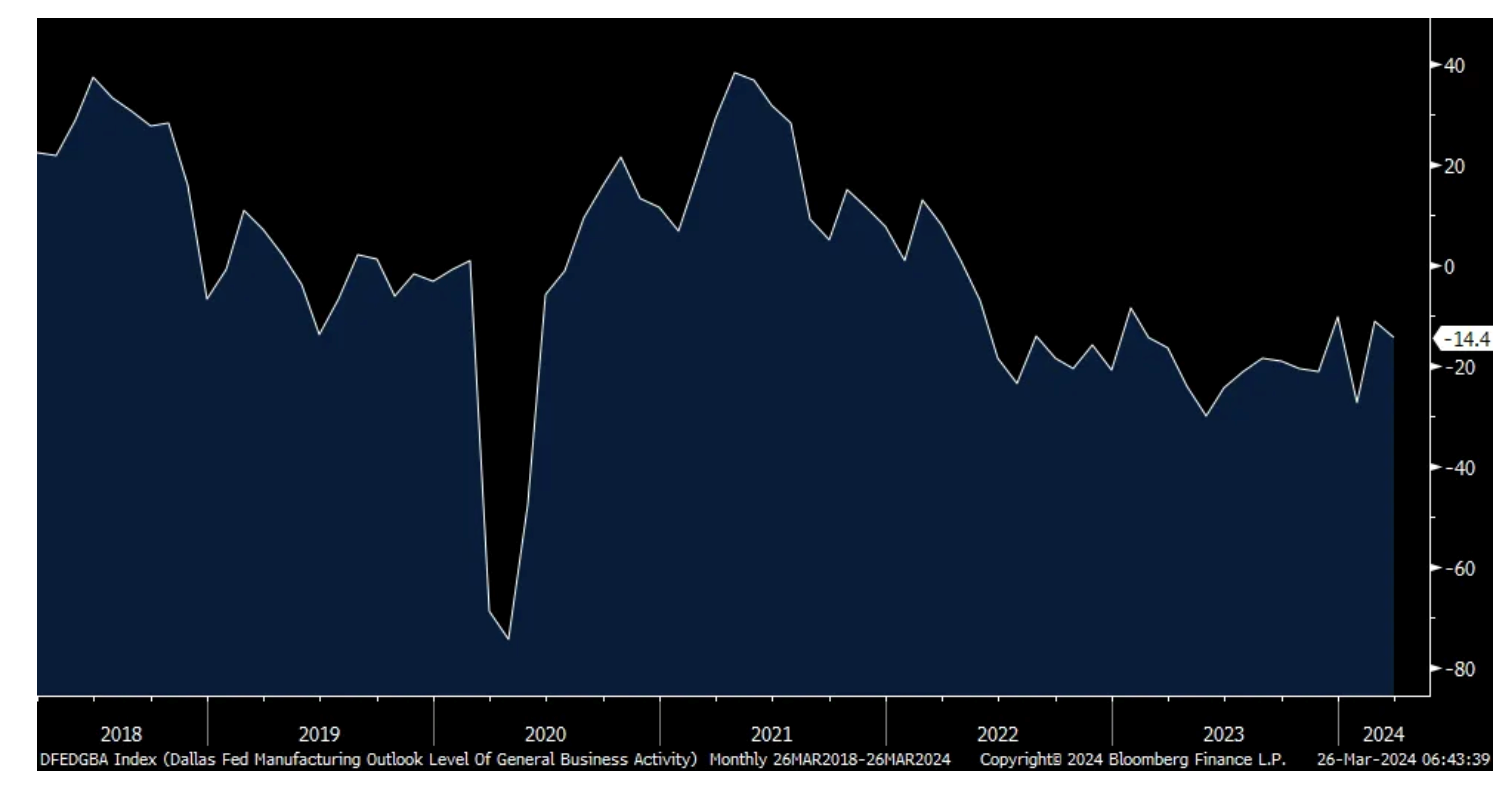

A few weeks ago we saw a negative print for the March NY manufacturing index and some hope when the Philly index went positive but Dallas reported yesterday that its survey remained deeply negative at -14.4 and has been now for 23 straight months. Of note, prices paid rose to a 6 month high and those received rose to the most since February 2023. The overall 6 month business outlook was around the flat line, at 1.3 vs +6.2 in February and -10.4 in January.

Here were some of the notable company comments in a variety of industries and mostly squares with another negative print in this survey:

Food Manufacturing

"Will the consumer continue to spend enough to promote growth? This is the question I cannot answer confidently."

"We are working on several new growth opportunities that are promising for late 2024. We are leaning into data driven processes and automation to improve the efficiency of this additional business. This includes AI and API (application programming interface) programs."

"Beef prices and availability are hurting margins and making it difficult to run product profitably. Chicken prices are also on the rise."

Printing and related support activities

"We have been on a 'hooray' roll regarding incoming orders, with a current huge uptick compared with the prior year to date. We are benefiting from a few diverse customer bases that need our services, plus we are coming up on our very busy time of the year, with growth forecast for that period as well. If not for these unique and somewhat isolated customer needs, I believe it would be very slow for us right now. Instead, we are adding workers in both the plant and office to handle the volume of work."

Nonmetallic Mineral Product Manufacturing

"The bad weather in January and February nationwide caused a downturn in new orders. This, coupled with the slight increase in interest rates (and no further decreases in mortgage rates), are not a good direction for homebuilding and remodeling and will cause us to miss our first-quarter expectation.

Primary Metal Manufacturing

"Capital expenditures are increasing to add new capabilities and new products. This is why our outlook is improved. Legacy business is declining sharply."

Fabricated Metal Product Manufacturing

"A business is only as good as its customers’ business and is completely dependent upon its customers' demand—and demand is weak. It's a far stronger, deeper recession than publicized. Whether a lack of customer economic confidence, post-COVID caution, interest rates, inflation or a combination of all, it has stopped demand beyond the essential spending of deferred maintenance and repairs that buyers cannot defer any longer. Even with 'competition retraction,' businesses are serving the same and similar market segments, closing permanently or ceasing operations. Order volume remains unimproved."

Machinery Manufacturing

"We kept thinking orders would pick up in the first quarter, but they have not. In fact, they've gotten even fewer and farther apart. Is it election uncertainly, a lack of peace overseas, money still being too expensive, or is it just a wet blanket over the entire economy? We don't know, but we're anxious to get some momentum going into the second half of the year."

"We are seeing general business activity slowing and competition increasing. We generally see this trend as business slows and our competitors become more hungry. However, we think that the third and fourth quarters will be better as the political landscape hopefully improves."

"After a very slow start for the year, we are seeing a slight increase in business. Hopefully, this trend will continue."

Computer and Electronic Product Manufacturing

"Only time will tell the true underlying health of the labor market. While there are no disclosures we’re in a recession, ask any manufacturer on the globe and they will tell you we are deep into it. The backbone manufacturing of this country isn’t looking good at all. What is clear is that economic risks abound, and a soft landing is far from the truth out here. I have never seen it this bad in the capital equipment industry in the last 30 years."

"We have seen a $400,000 decrease in sales this year. I am very concerned."

Transportation Equipment Manufacturing

"Election, energy and interest rate uncertainty makes business planning difficult."

Misc. Manufacturing

"Political discussions about taxes are extremely dishonest, and future proposed increases to taxes will further reduce U.S. manufacturing competitiveness globally. I find it very insulting and disingenuous when medium-sized companies are called out as not paying "our fair share" of taxes. Currently, if you look at our total tax paid versus our total profit, we are taxed at over 60 percent as a medium-sized manufacturing company. We can't expand employment, technology and innovation to compete with China with higher taxes."

"Our sales have been unusually low since October 2023, and we see the trend continuing but more dramatically in the next four months. We are laying off nonessential workers and cutting hours for employees, effective immediately. Our automotive OEM [original equipment manufacturer] business is down by about 20 percent. We are seeing a continued drop in our catalog sales. Our overall volumes have been gradually reducing for several years. We are unable to determine why this is occurring."

Dallas Manufacturing index

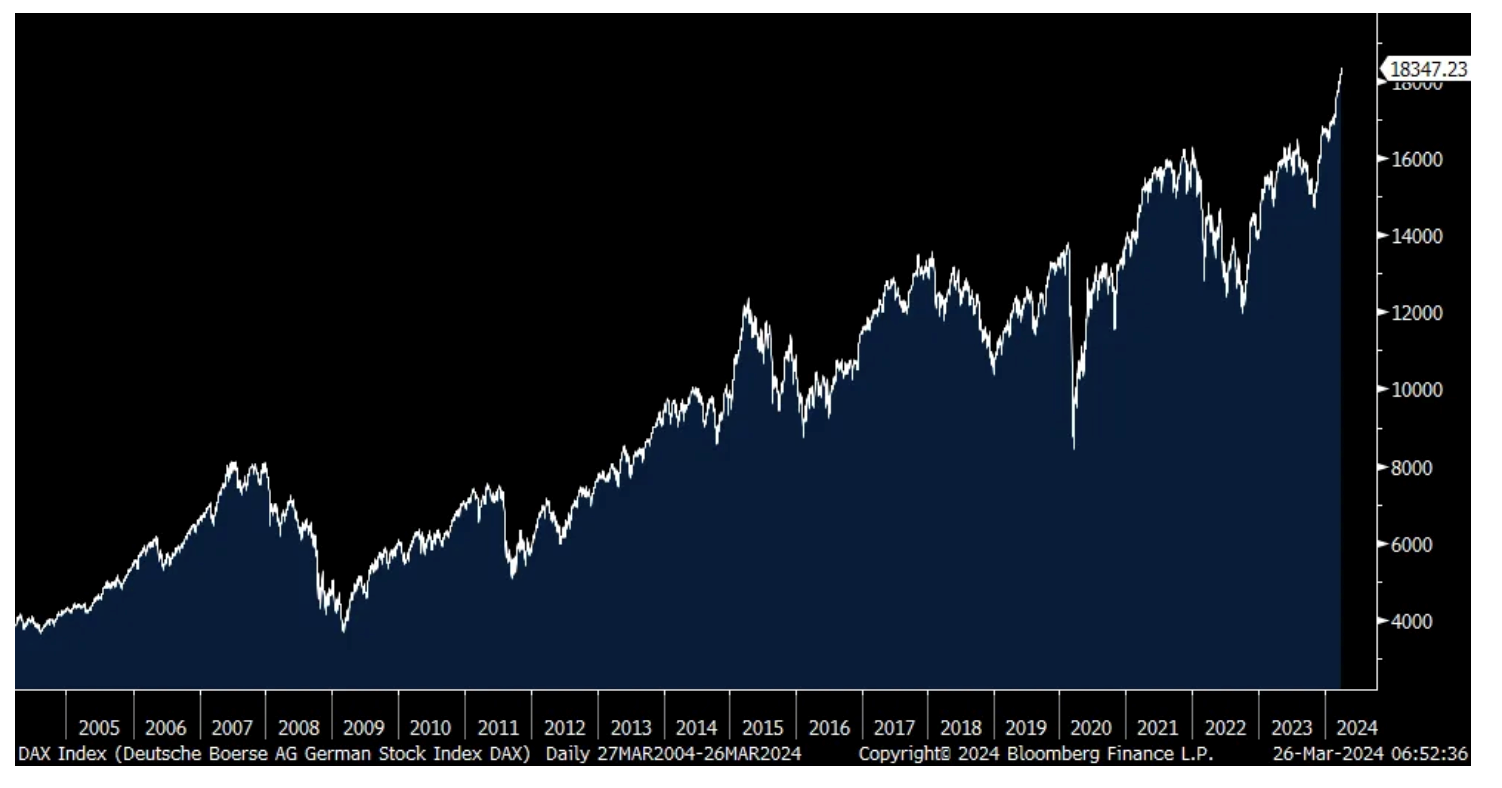

Last week we saw a lift in business confidence in Germany that hopes interest rate cuts will help as will a hoped for bottoming in China's economy. Today we saw a slight gain in German consumer confidence according to GFK and NIM to less bad at -27.4 from -28.8. They said, "The recovery in consumer sentiment is progressing slowly and very sluggishly...Real income growth and a stable labor market are in themselves very good prerequisites for a rapid recovery in the consumer economy, but consumers still lack planning security and optimism about the future."

This data point is not market moving but we are seeing a drop in European bond yields and notwithstanding this a lift in the euro while the DAX is up .50% to a fresh record high amazingly in the face of their modest recession.

DAX

BY Doug Kass · Mar 26, 2024, 9:35 AM EDT

BY Doug Kass · Mar 26, 2024, 9:25 AM EDT

BY Doug Kass · Mar 26, 2024, 9:20 AM EDT

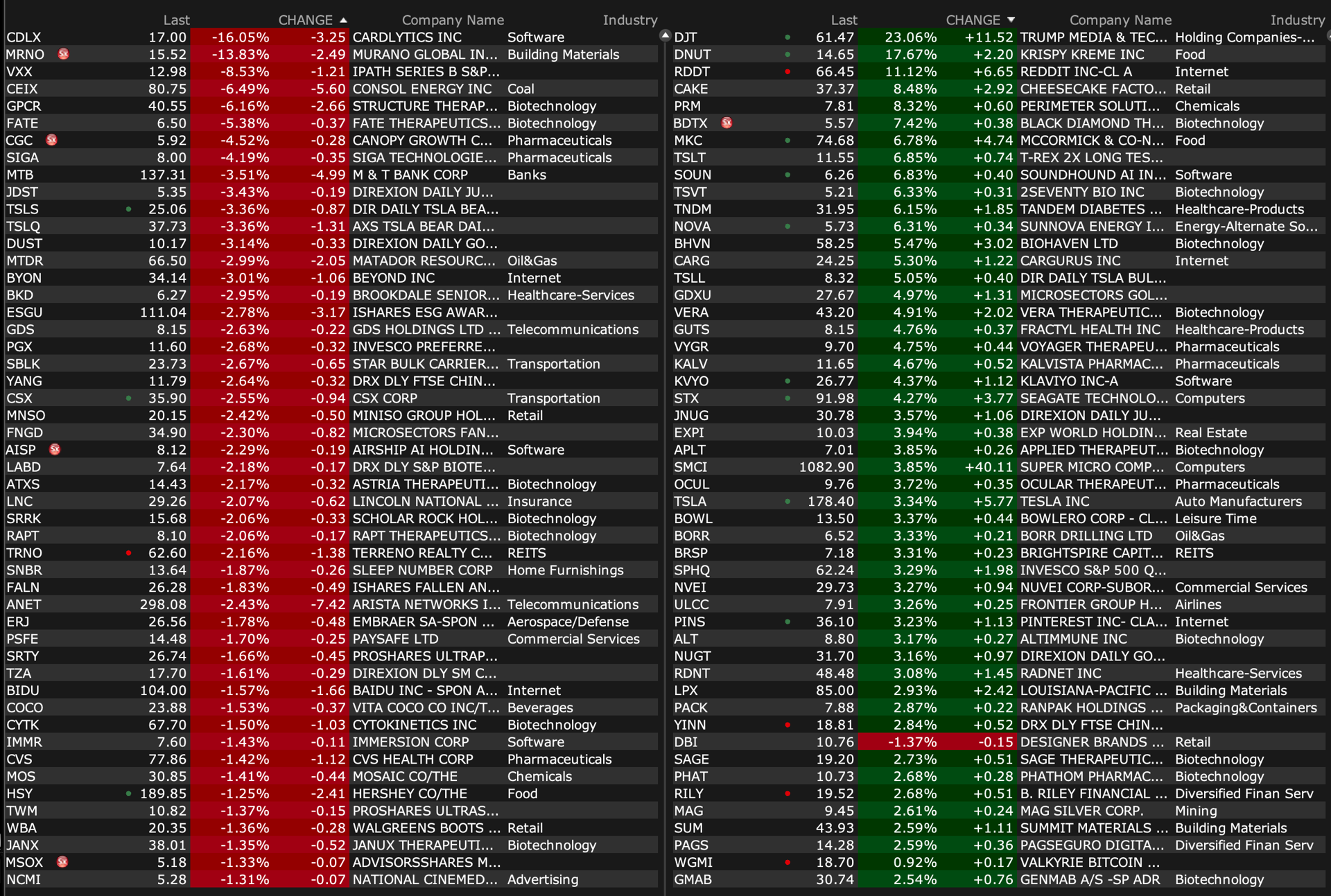

Upside

-STOK +90% (new data supports the potential for STK-001 to be the first disease-modifying medicine for treatment of patients with Dravet Syndrome)

-OPGN +78% (announces 3M shares at $1/shr of preferred stock acquired by David Lazar)

-KULR +35% (enters into an agreement with Lockheed Martin for heat sink advancements in Precision Missile Electronics)

-DJT +25% (strength ahead of NASDAQ debut)

-DNUT +20% (McDonald's to sell Krispy Kreme doughnuts nationwide by end-2026, following successful test at 160 McDonald’s restaurants)

-PRAX +19% (reports positive results of PRAX-628 study evaluating Photo Paroxysmal Response (PPR) achieving 100% response in treated patients)

-RDDT +14% (momentum following IPO)

-VKTX +14% (Phase 1 clinical trial of oral tablet formulation of Dual GLP-1/GIP Receptor Agonist VK2735 demonstrates up to 3.3% Placebo-Adjusted Mean Weight Loss (5.3% from Baseline) observed after 28 Days)

-MKC +6.2% (earnings, guidance)

-TNDM +6.2% (Stifel Nicolaus Raised TNDM to Buy from Hold, price target: $37 from $24)

-AMRX +5.8% (receives U.S. FDA Approval for Ciprofloxacin and Dexamethasone Otic Suspension)

-ENTX +5.8% (announce key regulatory milestone for Oral PTH(1-34) Peptide (EB613) Phase 3 Program)

-SMMT +4.6% (Stifel Nicolaus Initiates SMMT with Buy, price target: $8)

-STX +4.6% (Morgan Stanley Raised STX to Overweight from Equal Weight, price target: $115 from $73)

-SLS +3.9% (announces positive topline data from Phase 2a study of SLS009 in r/r AML)

-PINS +3.1% (recent notable strength being attributed to analysts saying Google partnership with Pinterest potentially being tested in the US)

-TSLA +3.1% (Italy said to have contacted Tesla for potential trucks production in Italy)

-UPS +2.6% (guidance from Investor Day)

Downside

-APCX -41% (prices $2M common stock and warrant offering)

-AMPE -30% (announces voluntary delisting and SEC deregistration)

-BZFD -16% (earnings, guidance)

-CDLX -13% (files to sell $150M in convertible notes)

-EFTR -8.0% (earnings)

-XOMA -5.2% (US FDA approves Medexus's sBLA for IXINITY to treat Hemophilia B in Pediatric Patients, under 12 years of age)

-OTLK -4.6% (Holders file to sell 21.4M common shares)

-GDS -3.2% (earnings, guidance; announces $587M equity raise for its international business)

-TRNO -2.5% (prices 5.5M shares at $62/share [upsized from 5M shares])

-MOV -2.0% (earnings, guidance)

BY Doug Kass · Mar 26, 2024, 9:12 AM EDT

* Markets weakened yesterday but futures indicate a higher opening

* The overbought remains in place as the S&P Short-Range Oscillator stands at 2.23% v. 2.55%

* Yields are mixed this morning and crude oil prices are slightly higher (+$0.16) and bitcoin is -$250 to $70.7k

* The U.S. dollar is virtually unchanged against the major currencies

* Chart of the Day (More inflation alerts!):

Tuesday heartbreak seem to be a drag

When you know that you love her especially

Catch up baby, catch up with my dreams

Maybe then I could see you all the time

- Stevie Wonder, Tuesday Heartbreak

"Workin' on our night moves Trying to lose the awkward teenage blues Workin' on our night moves In the summertime And oh the wonder Felt the lightning And we waited on the thunder Waited on the thunder."

- Bob Seger, "Night Moves"

This daily Futures feature is like inside baseball. I try to show you and write about what I believe thoughtful hedge fund managers are looking at when they awake -- let's call it our normal routine -- setting the stage for their strategy for the day. The market is a complicated mosaic and the more info you have, the better trader and investor you will be!

The market (and money) never sleeps -- and neither do I, it appears! I have previously described the importance that overnight futures trading hold for me here. It is a guidepost to my strategy in the regular trading session. Moreover, the overnight/early morning futures hold opportunities as they are (1) inefficient, though liquid and (2) it seems fear and greed are often exaggerated outside the regular trading session. I frequently try to capture those efficiencies by trading actively both in the pre- and after-market sessions.

Here are brief observations I wanted to highlight and provide a summary of overnight price movements in various asset classes:

* Stock futures were higher overnight. S&P futures peaked at +22 and bottomed at +3. Nasdaq futures peaked at +106 and bottomed at +2. At 7:58 a.m. ET, S&P futures were +20 and Nasdaq futures were +97.

* Commodities are mixed with Brent crude up +$0.14 at $86.89.

* The S&P Short-Range Oscillator is still overbought at 2.23% v. 2.55%.

* The VIX is at 13.06 (-0.13).

* The U.S. dollar is not materially changed against the yen, pound and euro.

* Treasury yields are also mixed. The 2-Year Treasury yield is +1 basis point at 4.597% and the 10-Year is -1 basis point to 4.24%. Over there, the yield on the 10-Year U.K. Gilt bond is -4 basis points.

* Overnight, the inversion of the 2s/10s Treasuries curve is down to -33 basis points. Real rates remain quite elevated; the 10-year is still about 1.85, again in real terms.

* Gold is ripping higher +$20.60 and sits at $2,219.

* Bitcoin is -$360 to $70.6k.

Here is a synopsis of some of my columns I believe were important, or in the event you were out for the day and/or did not read my Diary. The principal intent is to review the logic of my market moves and other factors:

At The Core of My Market Concerns (The Equity Risk Premium)

A Mind Melt With My Investment Rabbi

I am Still Not Loving It! (McDonald's)

Here are Monday's trades. I believe in my Diary's full disclosure and transparency of trades/investments -- this is not CNBC! How else can you evaluate the value of my actions without memorializing them?:

* Adding to PGC

BY Doug Kass · Mar 26, 2024, 8:35 AM EDT

You'll be swell! You'll be great!

Gonna have the whole world on the plate!

Starting here, starting now,

honey, everything's coming up roses!

Clear the decks! Clear the tracks!

You've got nothing to do but relax.

Blow a kiss. Take a bow.

Honey, everything's coming up roses!

- Ethel Merman, Everything's Coming up Roses

Equities continue to Decouple from the real economy, threats of rising inflation, undisciplined fiscal policy, an out of control deficit/debtload, and likely interest rate levels that will likely be higher for longer.

At the very least, as noted by my Investment Rabbi (in a discussion Sunday evening and early Monday morning), current market strength is borrowing from the future. At the worst, an important market high might be in the making.

In the rally over the last few days market breadth has deteriorated. Yesterday, was a good example:

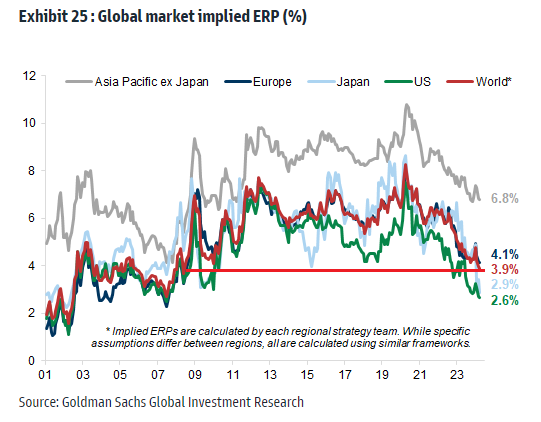

Meanwhile, equity risk premiums, one of the more accurate expression or predictors of future market returns, continue to be paper thin and, as expressed yesterday, the global equity risk premium is now at the lowest since 2008:

As divergences and fundamental concerns multiply, speculation and bullish investor sentiment are expanding - as indicated by this morning's climb in stock futures.

Valuations have now moved into thee 95%-tile as markets rejoice in a chorus of Ethel Merman's Everything Is Coming Up Roses.

Fear and doubt has left the building as cryptocurrencies and technology stocks record almost daily highs in a market dominated by momentum-based actors, and under the influence of ODTE options.

The short community has become like the flightless dodo bird, an extinct species who has virtually disappeared from the investment stage.

For some reasons mentioned in this column, and for others, I continue to look down as the consensus is looking up.

And, like Sisyphus...

BY Doug Kass · Mar 26, 2024, 7:37 AM EDT

* Optimism has been replaced by pure giddiness (see links below!)...

“The market cycle will once more prove to be the human-nature cycle; its economic background will have changed, but not its basic character nor the consequences of its character.”

- Benjamin Graham

Bonus - Here are some great links:

* Stocks Are Going Up With or Without You

BY Doug Kass · Mar 26, 2024, 6:38 AM EDT

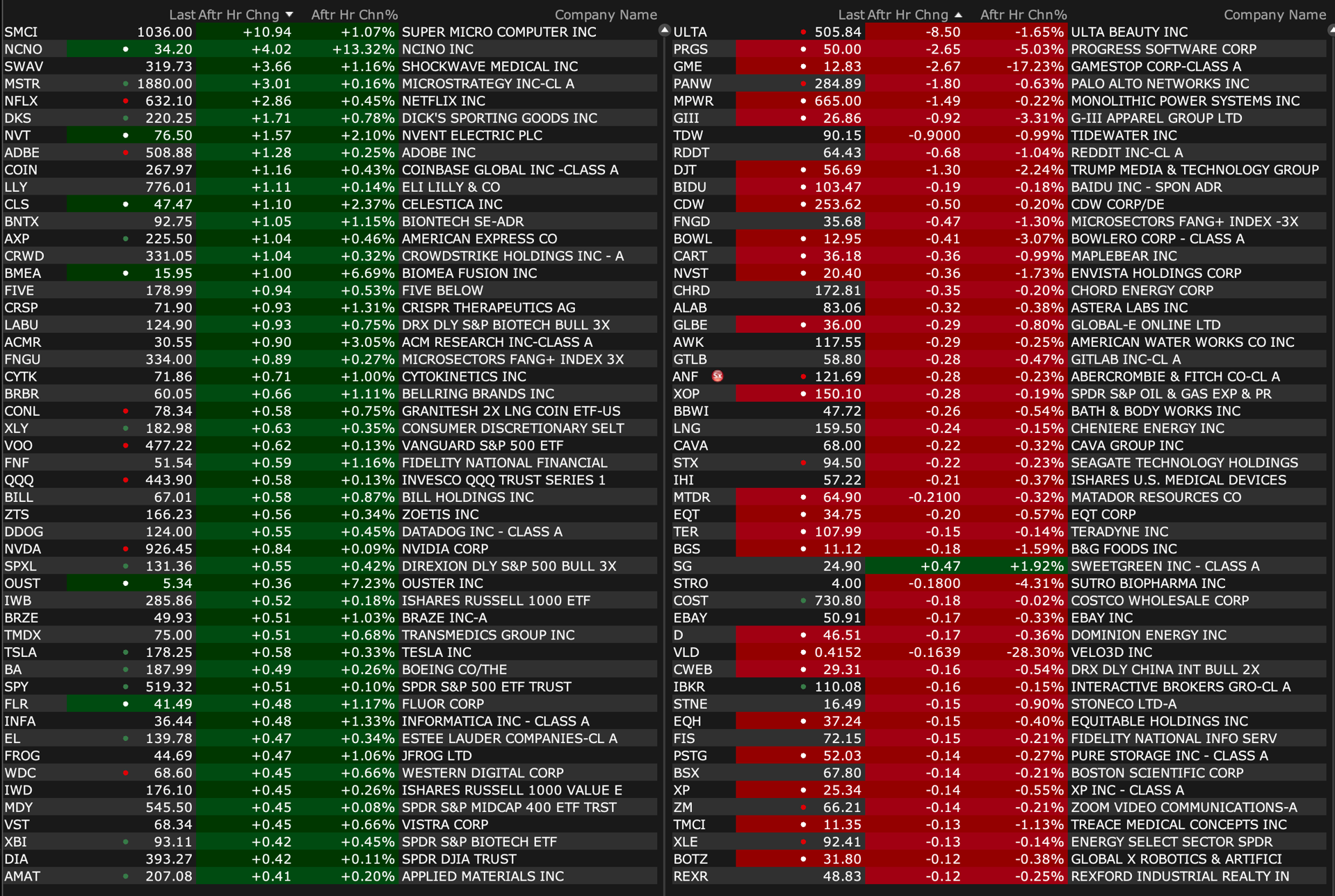

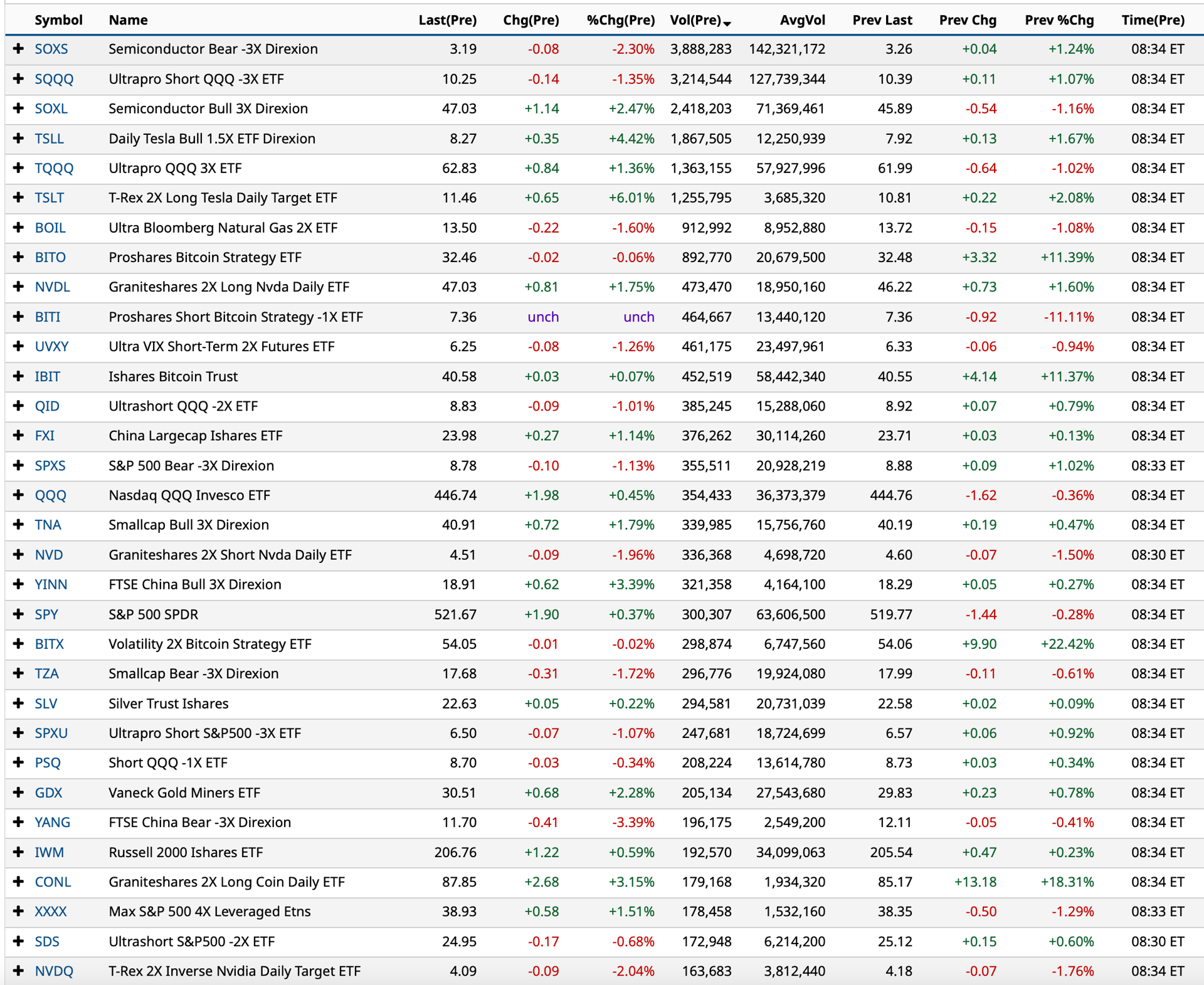

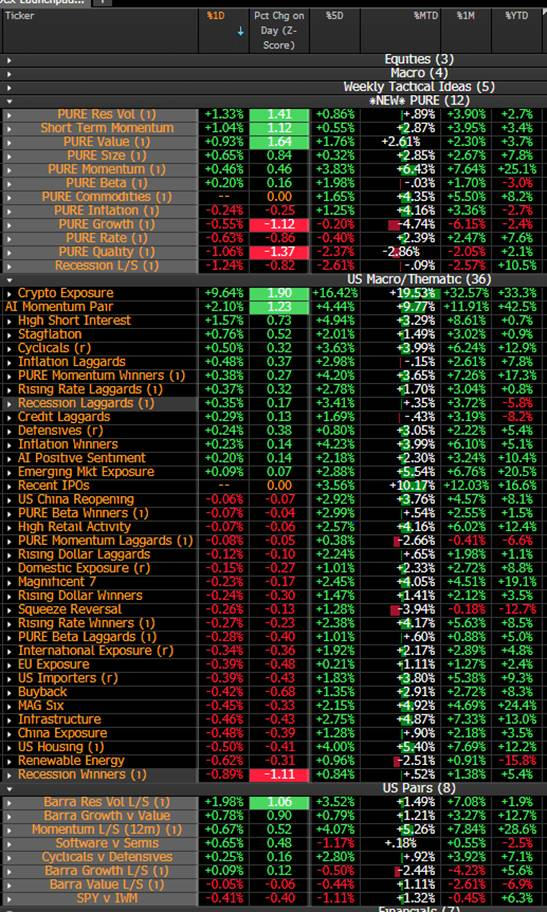

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Mar 26, 2024, 6:25 AM EDT

From JPMorgan:

Futs are higher with both Tech and small-caps outperforming, with bond yields lower and the front-end of the curve outperforming. It is unclear is yesterday’s moves were tied to month-end/quarter-end rebalancing but generally those flows occur before the last day of the period. Mag7 and Semis are higher pre-mkt with TSLA +3.2%. USD weakness continues but cmdty performance is mixed; gold approaching ATHs. Today’s macro data focus is on Durable/Cap Goods, Home price indices, Consumer Confidence, and regional activity indicators (Dallas, Philly, and Richmond). 5Y bond auction is $67bn so let’s see if it goes as smoothly as yesterday’s 2Y auction.

and...

EQUITY AND MACRO NARRATIVE: Yesterday, there was scant information to change the macro narrative with Fedspeak giving a range of cuts numbering from 1 to 3, advice on looking through the Jan/Feb inflation prints, and ultimately a view that the Fed exercise patience given the strength of the economy. The 2Y bond auction saw stronger demand relative to the previous 3 auctions and essentially traded flat to the market, trading up about half a basis point to digest. Much of the fireworks in markets were reserved for Semis where there were China-centric headlines for AMD, INTC, and MU; SMH closed -25bps on the day.

BY Doug Kass · Mar 26, 2024, 6:15 AM EDT

Coinbase COIN, illustrated around $216 last Tuesday, hit $283.48 yesterday.

BY Doug Kass · Mar 26, 2024, 6:08 AM EDT

BY Doug Kass · Mar 26, 2024, 5:57 AM EDT

Shorted more SPY at $522.00 and QQQ at $447.30, respectively.

BY Doug Kass · Mar 26, 2024, 5:48 AM EDT