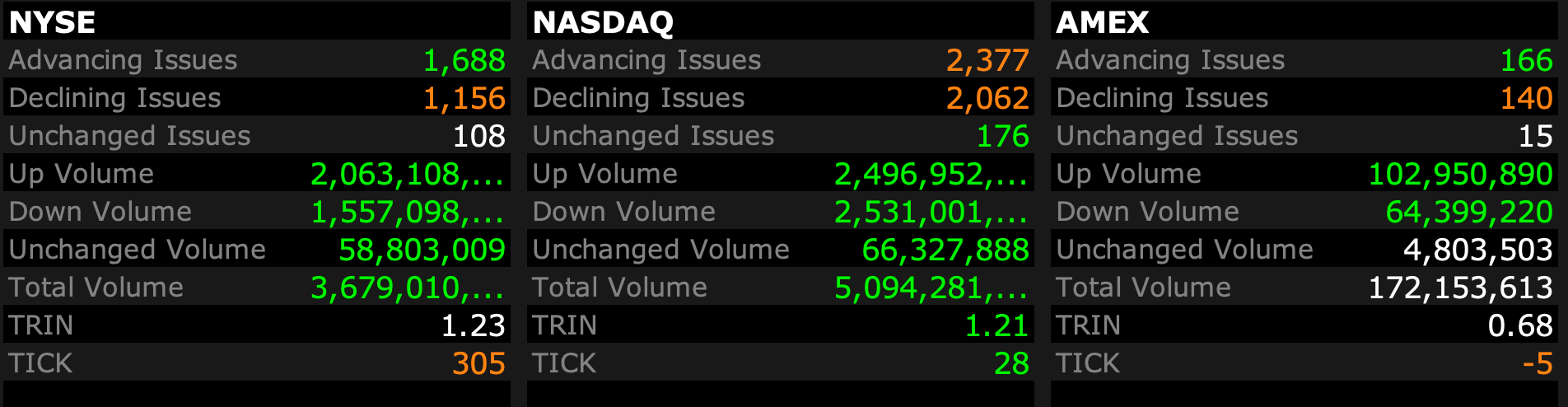

Market Internals on Close

Closing Volume/Breadth

- NYSE volume 410M shares, 7% below its one-month average;

- NASDAQ volume 4.16B shares, 3% below its one-month average;

BY Doug Kass · Feb 23, 2024, 4:33 PM EST

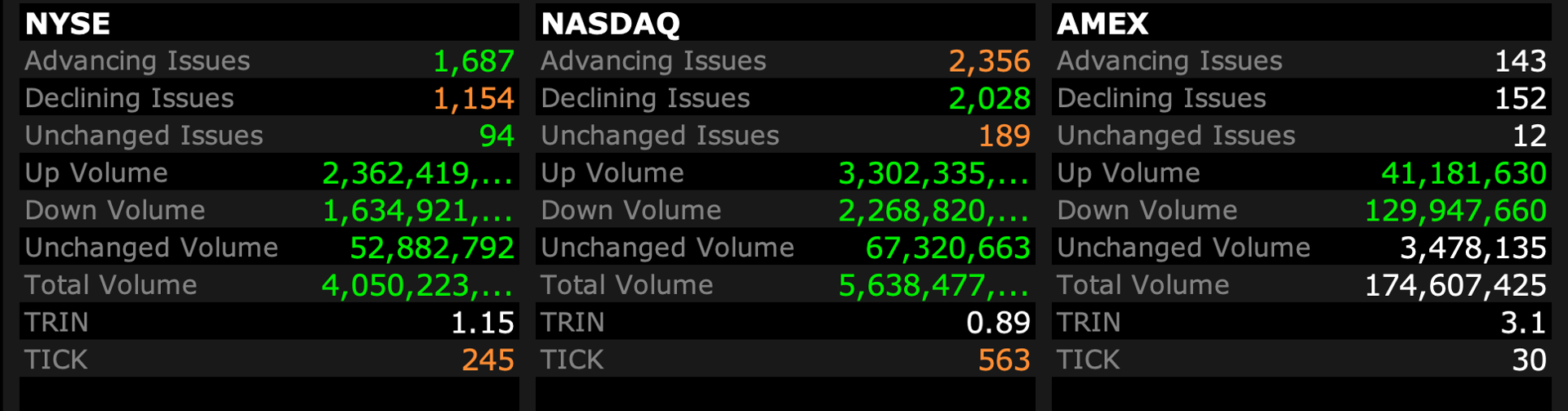

Closing Volume/Breadth

- NYSE volume 410M shares, 7% below its one-month average;

- NASDAQ volume 4.16B shares, 3% below its one-month average;

BY Doug Kass · Feb 23, 2024, 4:33 PM EST

B. Riley appears to be one of the walking dead!

BY Doug Kass · Feb 23, 2024, 3:30 PM EST

I have a 3:30 research call.

Thanks for reading my Diary this week - I hope it was value added.

Enjoy the weekend.

Be safe.

BY Doug Kass · Feb 23, 2024, 3:15 PM EST

I have added to my XLF short on strength today.

At the same time I am pairing the ETF with two regional bank buys which I will discuss next week upon completion of my research.

BY Doug Kass · Feb 23, 2024, 3:02 PM EST

Professor Galloway No Mercy No Malice... "Corporate Ozempic."

BY Doug Kass · Feb 23, 2024, 1:42 PM EST

Net, net I raised my short exposure on the early rally.

See you back at 2 pm.

BY Doug Kass · Feb 23, 2024, 12:45 PM EST

I have a short trip out of the office for a business meeting.

Back at around 2 pm.

BY Doug Kass · Feb 23, 2024, 12:30 PM EST

Selling some BMY at $51.65.

BY Doug Kass · Feb 23, 2024, 12:20 PM EST

Selling some JNJ at $161.87.

BY Doug Kass · Feb 23, 2024, 12:10 PM EST

I vividly remember the speculation in the Comments Section in late 2021 - that I vehemently cautioned about.

For what it is worth I have seen some of that over the last week... again.

Just saying.

BY Doug Kass · Feb 23, 2024, 11:48 AM EST

Major reversals in NVDA and others.

Standing pat with my positions.

BY Doug Kass · Feb 23, 2024, 11:18 AM EST

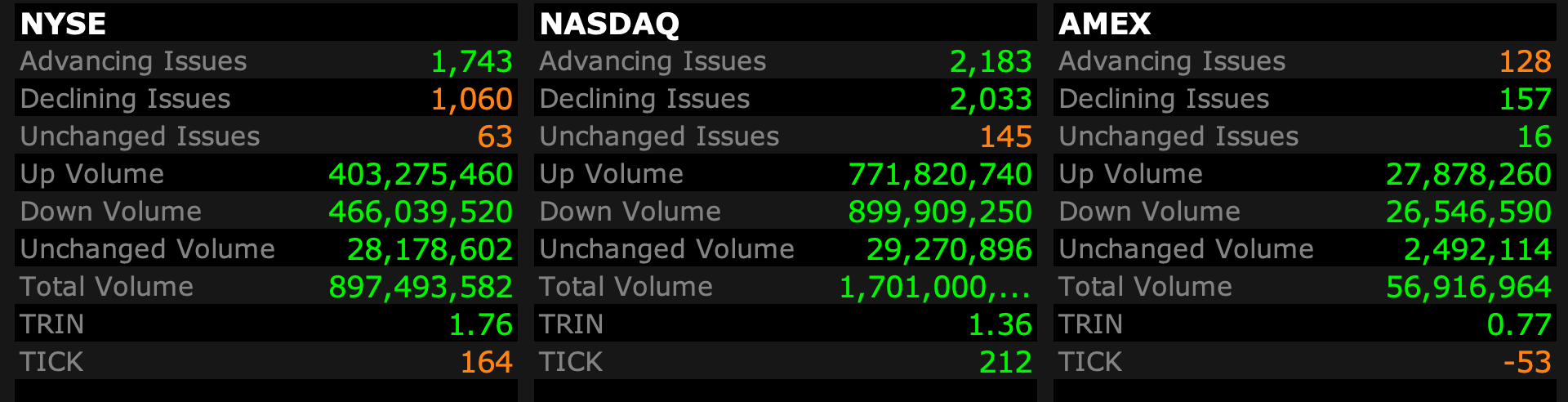

* At 10:45 am:

- NYSE volume 138M shares, 9% below its one-month average

- Nasdaq volume 1.53B shares, flat to its one-month average

- VIX down 3.65% to 14.01

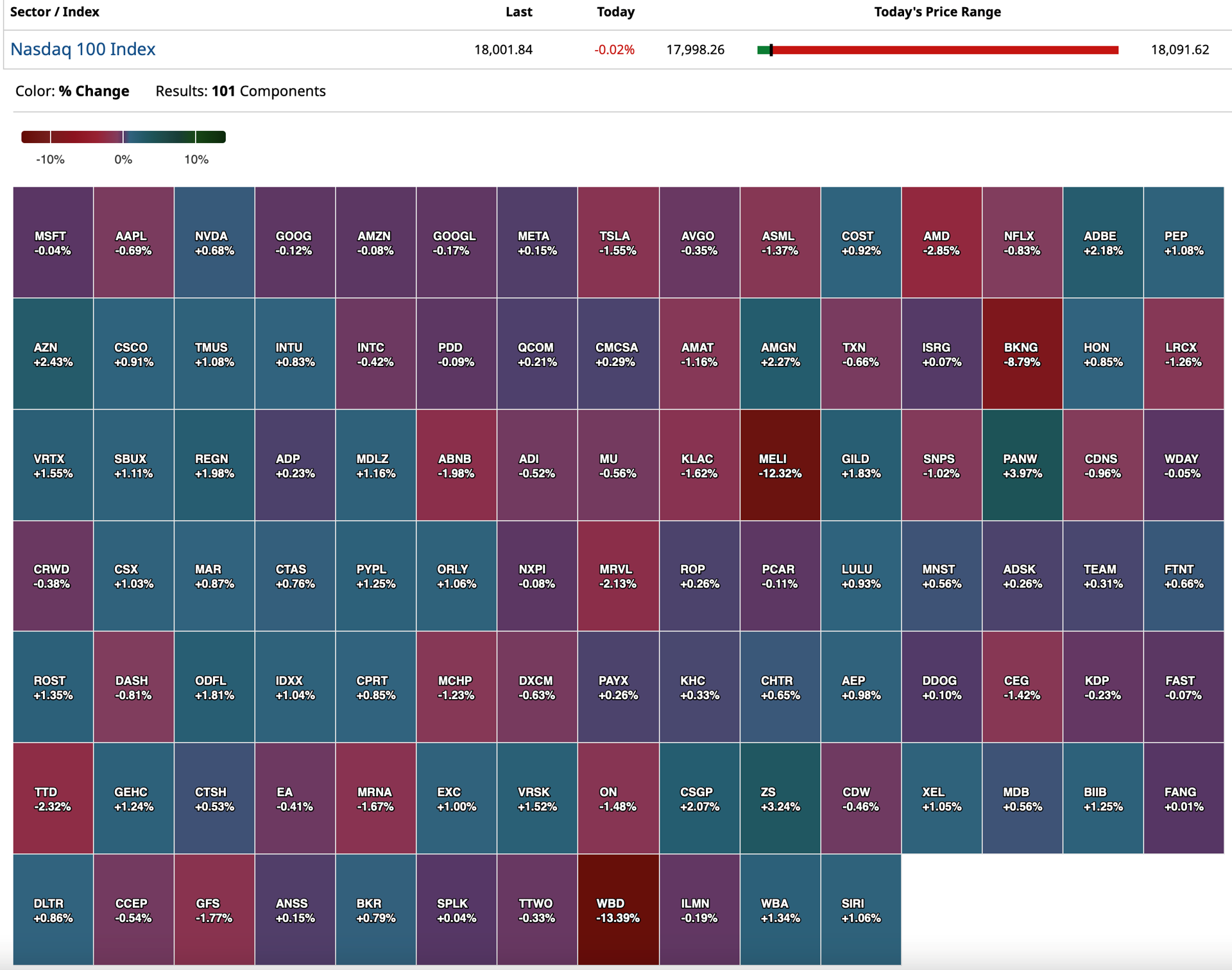

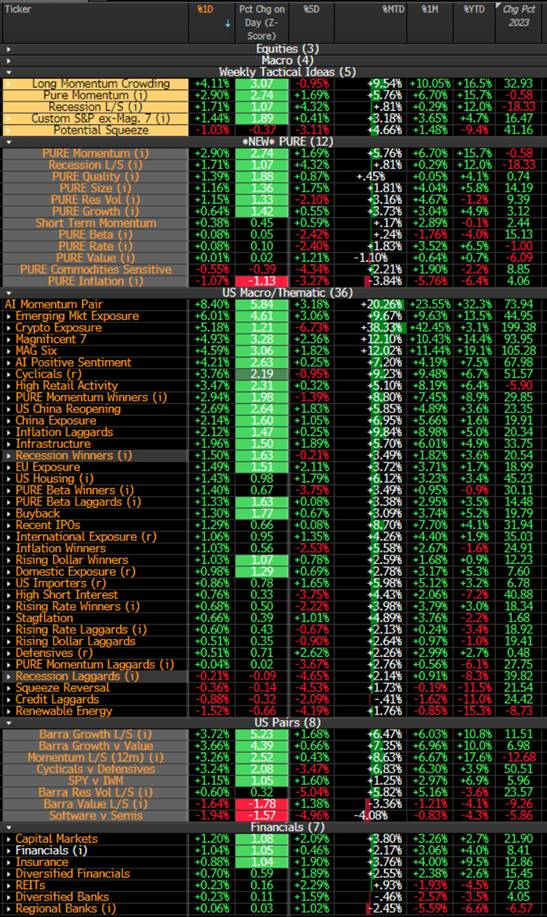

Nasdaq 100 Heat Map

BY Doug Kass · Feb 23, 2024, 10:56 AM EST

No trades today.

BY Doug Kass · Feb 23, 2024, 10:30 AM EST

* The core and fundamental relationship between interest rates (the ten year Treasury yield has risen by 50 bps in the last three weeks) and equities has been abandoned by investors

Source: Hedgeye

* Moreover, moderating global economic (from retail sales, to industrial production, to housing starts) and profit growth prospects (see Bookings Holdings discussion below) are being ignored by a market dominated by momentum-based investors and by the attractive prospects and embracing of AI (which may be now moving towards a mania)

* Fear and doubt have left Wall Street - abetted by market structure - as the animal spirits have taken over our markets

* As discussed frequently in my Diary market breadth continues weak - yesterday's breadth did not correspond to the magnitude of the rally in the senior Indexes:

Nor did the equal weighted S&P (+0.93%) or the Russell's (+0.55%) advances correspond to the size of the rally in the S&P (+2.1%) and Nasdaq (+2.9%) on Thursday.

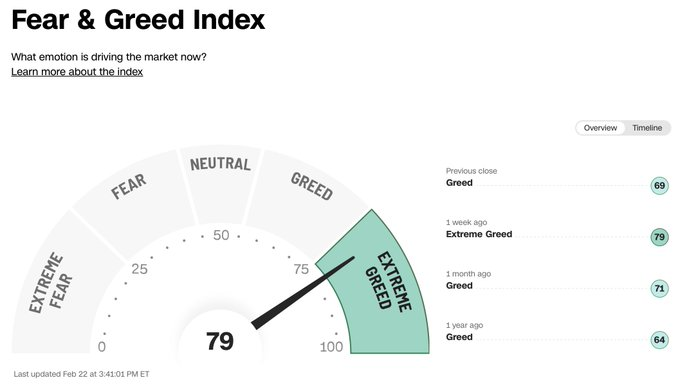

* Extreme greed has returned:

* Meanwhile, other bonafide concerns - "higher for longer" monetary policy, "stacked/cumulative" inflation has yet to be felt (but it will be!), political and geopolitical threats and, importantly the burgeoning U.S. deficit and rising debt load (and associated debt service) - have been pushed onto the back burner as emotion (FOMO) has become the dominate factor influencing investor sentiment and positioning

* The forward S&P price earnings ratio is now at 21x - at the same level of the January, 2022 market top

* Though traders/investors have voted, watch for the return of Buffett's "weighing machine" in the time ahead

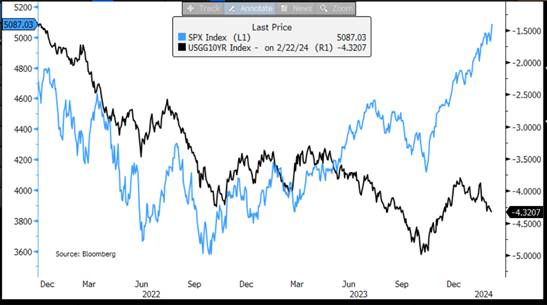

Spurred by Nvidia's NVDA strong fourth quarter earnings print (and its unprecedented share price climb, stocks further decoupled from macroeconomic influences (economic growth and interest rates) yesterday.

This decoupling - particularly in technology companies that have delivered strong earnings irrespective of the interest rate backdrop - has been the most conspicuous phenomenon thus far in 2024 and, arguably, has gone too far.

Specifically, the decoupling from rates, based on three measures (discussed below), has been ever more stretched as momentum-based traders/investors (in which buyers live higher) have piled into stocks coincident with a rise in animal spirits and the "fear of missing out" (FOMO).

This phenomenon, in turn, has taken every significant historical valuation metric above the 90%-tile - creating, in my view, an unattractive reward/risk proposition.

Since the first week of February (less than three weeks ago) the yield on the ten year US Treasury note has climbed by 50 basis points - from 3.85% to 4.35%.

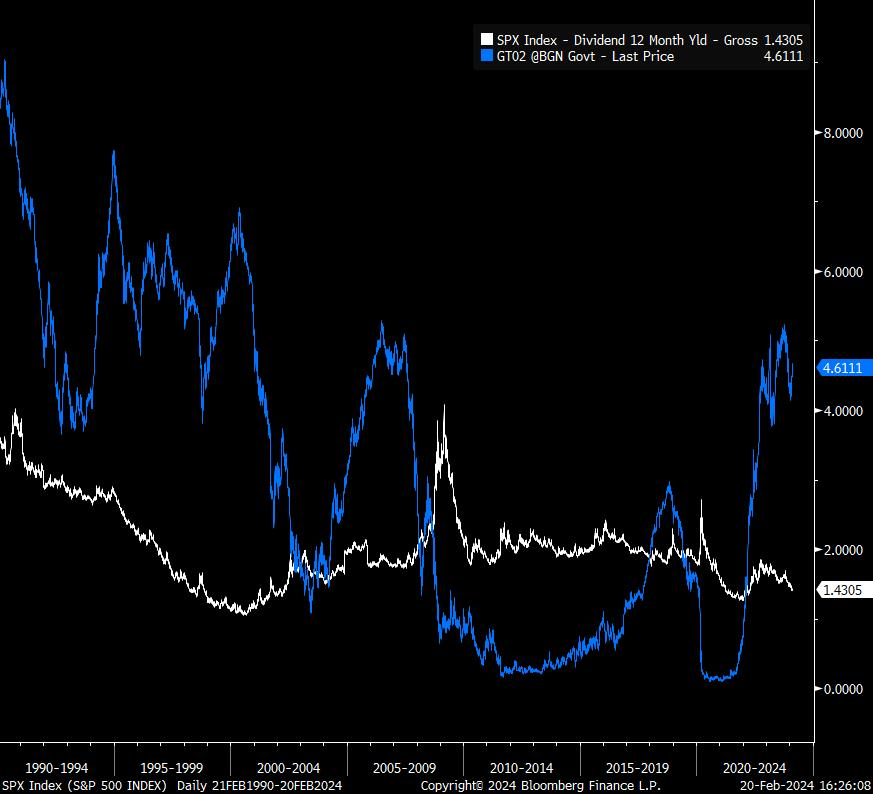

As a result, the equity risk premium has fallen to multi-decade lows, the spread between Treasury yields and the S&P Dividend Yield has moved to historical levels as has the difference between the S&P Index and real interest rates (inverted) moved to a record gap:

* U.S. equity risk premium - the premium that investors receive to compensate them for taking on additional risk in the stock market instead of treasuries - has fallen to its lowest level (and two standard deviations below normal) since the Dot Com Bubble:

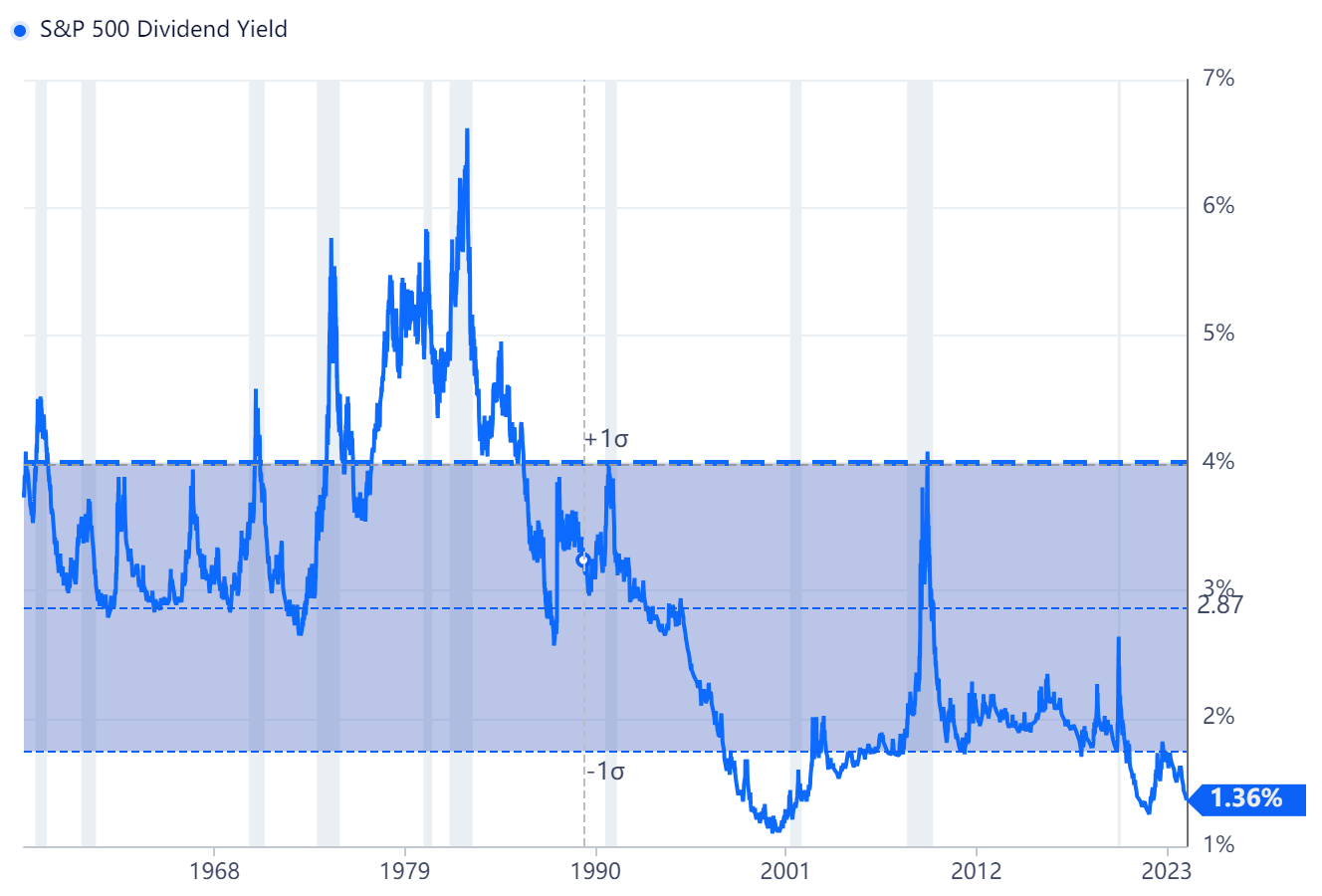

* The differential between the S&P dividend yield (1.36%) and Treasury yields has rarely been wider:

S&P Dividend Yield v. Two Year Treasury Note Yield

*Finally, here is another clear and unprecedented manifestation of the rate/equity decoupling:

S&P Index v. 10 Year Real Interest Rate (Inverted)

Nasdaq Index v. 10 Year Real Interest Rate (Inverted)

I won't spend much time in discussing the disappointing non technology earnings releases over the last few weeks but last night's disappointing Booking Holdings' EPS announcement was quite disappointing (the shares fell by -10% in the after hours) and could foreshadow broader company profit weakness (and reports) in 2024.

Here is the full release.

More from RBC:

What the bears liked.

1) Q1 room night guide +4-6% y/y, FY closer to 6-7% and U.S. room nights flat in Q4 (likely below EXPE). We believe EXPE's B2B business is likely growing ahead of leisure where BKNG doesn't really participate and then at some level, BKNG had been such a large share gainer through '22 (estimate as much as 20-30% delta between BKNG & EXPE RN growth at times) that a bit of reversion was inevitable at some point. We remain optimistic that with air, payments and a growing focus on merchandising in the U.S., BKNG still has the tools to get back to taking share though it appears this is on ice for the time being in pointing to a 9-10 pp decel in '24.

2) A bit less than 100 bps of FY EBITDA margin expansion (Street +140 bps). Clearly heavy marketing investments continue though we liked the commentary that direct mix was the primary driver ...

From Goldman Sachs:

Divergences And Lack of Broadening Continues

My recent post (Divergences Are Like Laxatives) on the weak breadth and market divergences remain concerning - though markets are unconcerned.

That article bears repeating:

BY Doug Kass · Feb 23, 2024, 9:30 AM EST

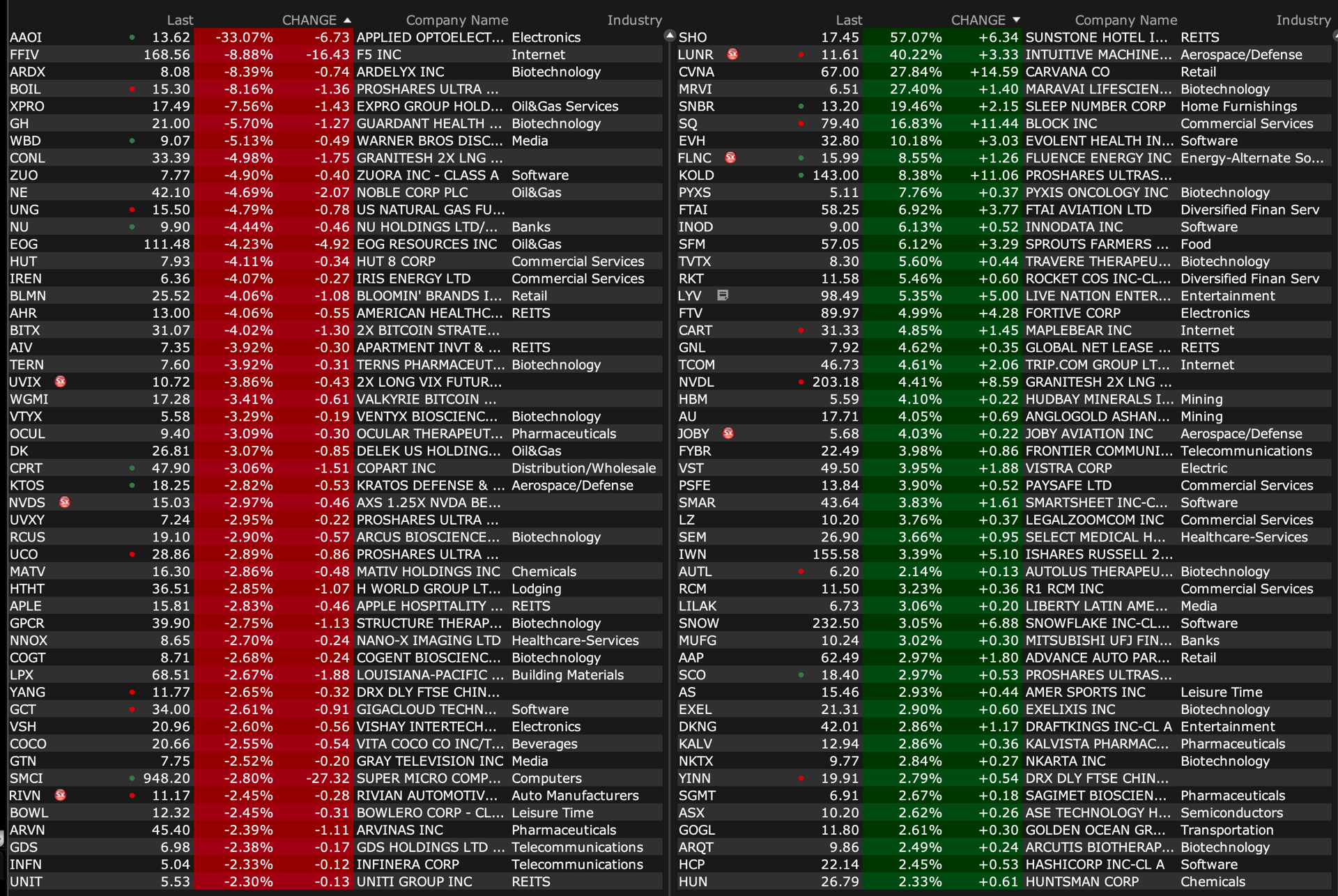

Upside

-LUNR +43% (private lunar lander Odysseus has successfully reached the moon and is transmitting data despite weak signal)

-CVNA +30% (earnings, guidance)

-MRVI +28% (earnings, guidance)

-KIND +21% (Board said to consider sale of company; reports prelim Q4, announces CEO change)

-SQ+17% (earnings, guidance)

-EXFY +11% (earnings, guidance)

-LZ +9.4% (earnings, guidance)

-UVE +7.9% (earnings)

-FLNC +7.8% (responds to misleading short seller report)

-RKT +7.5% (earnings, guidance)

-TVTX +7.1% (CSL Vifor and Travere Therapeutics announce sparsentan receives positive CHMP opinion for treatment of IgA nephropathy)

-FTAI +6.5% (earnings)

-LYV +5.7% (earnings, guidance)

-SPCE+4.8% (higher in sympathy with LUNR)

-HBM +4.1% (earnings, guidance)

-PLUG +3.5% (expands partnership with Uline to supply hydrogen and fuel cells at four additional sites)

-DKNG +3.3% (Barclays Raised DKNG to Overweight from Equal Weight, price target: $50 from $41)

-ATNM +3.1% (highlights improved survival with Iomab-B in TP53 Positive Relapsed Refractory Acute Myeloid Leukemia patients in SIERRA trial and other presentations at the 2024 Tandem Meetings)

-SHO +2.5% (earnings, guidance)

-WCC +2.5% (enters agreement to sell integrated supply business to Vallen Distribution for $350M)

-FOXA +2.2% (CitiGroup Raised FOXA to Buy from Neutral, price target: $35)

Downside

-AAOI-35% (earnings, guidance)

-VERO -24% (announces $1.2M registered direct offering priced at-the-market under Nasdaq rules)

-VICR -20% (earnings)

-INDI-19% (earnings, guidance)

-MODV -16% (earnings, guidance)

-ARDX -10% (earnings, guidance)

-GH -8.3% (earnings, guidance)

-BKNG -8.0% (earnings, guidance)

-PLL -7.5% (earnings)

-MELI -6.9% (earnings)

-GDYN -5.3% (earnings, guidance)

-OLED -4.6% (earnings, guidance)

-NE -4.2% (earnings, guidance)

-NU -4.2% (earnings)

-CPRT -4.0% (earnings)

-EOG -3.9% (earnings, guidance)

-WBD -3.8% (earnings, guidance)

-SMCI -3.2% (announces pricing of Private Offering of $1.5B of Convertible Senior Notes due 2029)

-VCYT -2.7% (earnings, guidance)

-ABNB-2.3% (lower in sympathy with BKNG)

-EXPE -2.2% (lower in sympathy with BKNG)

BY Doug Kass · Feb 23, 2024, 9:15 AM EST

At 8:31 am:

BY Doug Kass · Feb 23, 2024, 9:00 AM EST

At 8:34 am:

BY Doug Kass · Feb 23, 2024, 8:52 AM EST

BY Doug Kass · Feb 23, 2024, 8:36 AM EST

BY Doug Kass · Feb 23, 2024, 8:00 AM EST

There will be no "Futures" column as it is taking me a while to compile my opening missive.

BY Doug Kass · Feb 23, 2024, 7:49 AM EST

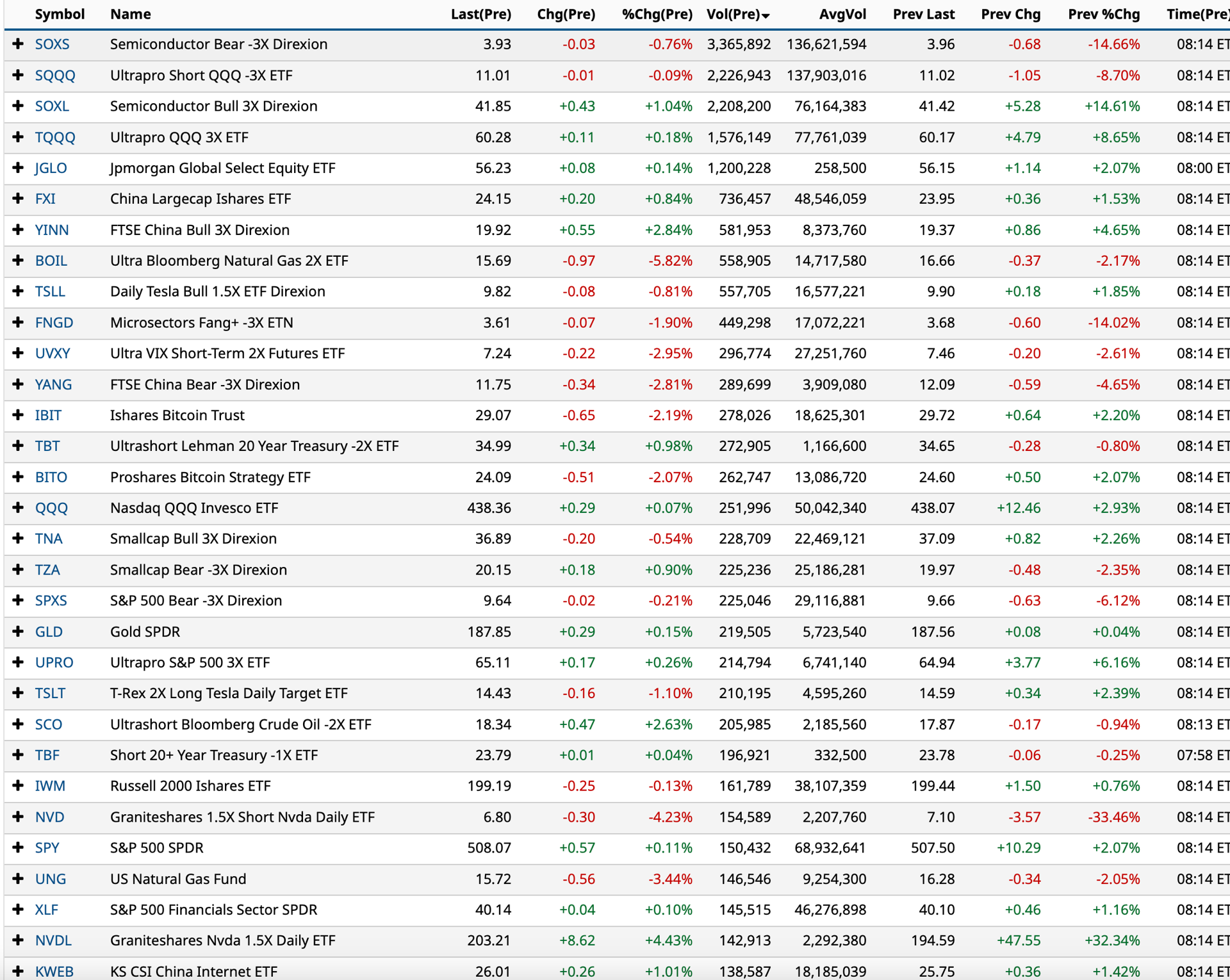

This table is a valuable resource for momentum-based short term traders:

BY Doug Kass · Feb 23, 2024, 6:50 AM EST

From JP Morgan:

US: Futs are modestly lower. NVDA has added another +2% pre-market, while most of other MegaCap Tech are lower: TSLA -1.1%, AAPL -41bp. Overnight, headlines are relatively quite. Bond yields are 2-3bp higher; USD is higher. Cmdtys are mixed: oil and ags are mostly lower, base metals are higher. We don’t have major economic data coming out today.

and...

EQUITY AND MACRO NARRATIVE: Yesterday, NVDA earnings drove the stock 16.4% higher. The bullish signal from the last MegaCap Tech earnings pushed SPX and NDX +3.0% and +2.1% higher on the day. Additionally, PMIs supported the growth-without-inflation narrative with a beat on the Mfg. side and easing Srvcs. Despite rising optimism in equities, yields have increased more than 45bp over the last three weeks amid rapid repricing in Fed rate cut expectation and hawkish labor and inflation data.

Jay suggests that the combination of less dovish path than their forecast and more neutral positions make the case that “yields have room to decline from current level in coming months”. However, with higher risk premium and a longer-than-expected QT runway, the team raises their YE rates forecast: 2y and 10y YE forecast increases from 3.25% to 3.80% and from 3.65% to 3.80%, respectively. Will the divergence between bonds and equities market continue? We wrote yesterday that we may see “further decoupling of stocks and yields since the Mag7 are proving to deliver on earnings expectations irrespective of the interest rate environment.”

BY Doug Kass · Feb 23, 2024, 6:40 AM EST

“One short-term swing trader’s bear market is another long-term trend follower’s oversold uptrend.” - David Lundgren

Bonus - Here are some great links:

BY Doug Kass · Feb 23, 2024, 6:30 AM EST

BY Doug Kass · Feb 23, 2024, 6:20 AM EST

From "Jazzy" Jeff Hirsch:

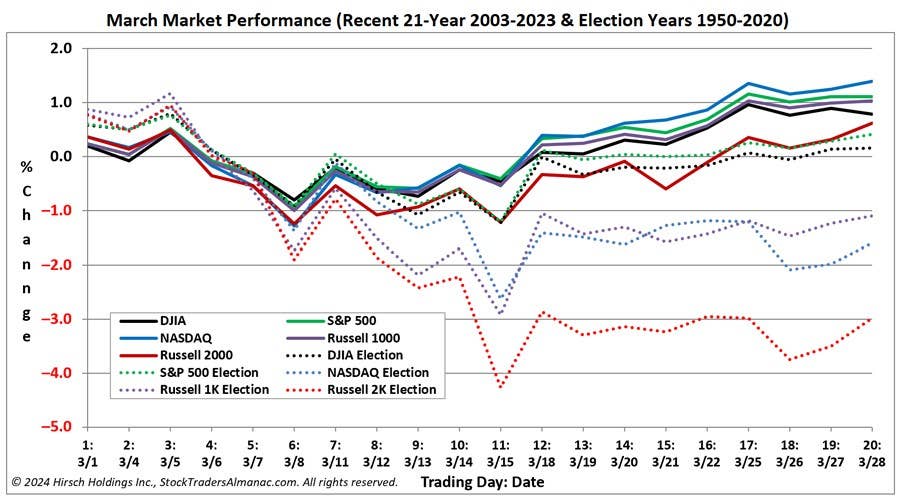

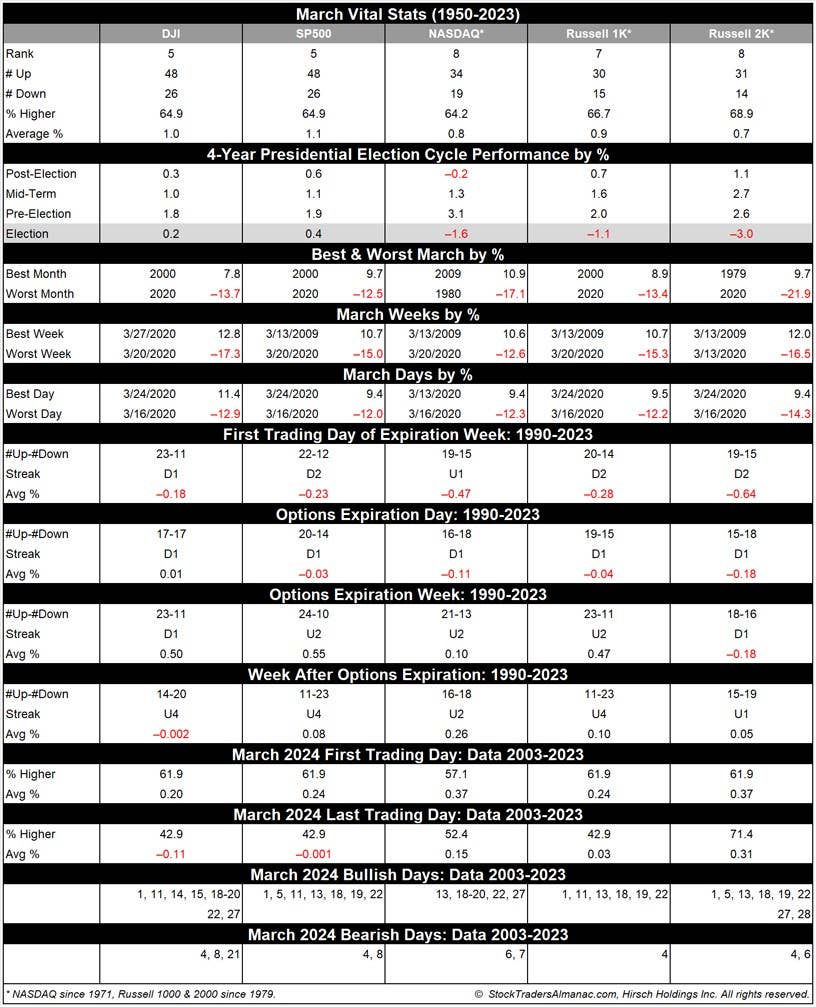

As part of the Best Six/Eight Months, March has historically been a solid performing month with DJIA, S&P 500, NASDAQ, Russell 1000 & 2000 all advancing more than 64% of the time with average gains ranging from 0.7% by Russell 2000 to 1.1% by S&P 500. Over the recent 21-year period, March has tended to open positively with gains accumulating over its first three trading days. A brief bout of weakness follows before all indexes begin moving modestly higher into mid-month through month’s end.

Julius Caesar failed to heed the famous warning to “beware the Ides of March” but investors have been served well when they have. Stock prices have had a propensity to decline, sometimes rather precipitously, during the latter days of the month. In March 2020, DJIA plunged nearly 4012 points (-17.3%) during the week ending on the 20th. Solid late-March gains in 2009 and again in 2020 have improved average second half of March performance, but the first half of the month still has more bullish days than the second half (see March 2024 Strategy Calendar).

March packs a rather busy docket. It is the end of the first quarter, which brings with it Quarterly Triple Witching and an abundance of portfolio maneuvers from The Street. March Triple-Witching Weeks have been quite bullish in recent years. But the week after is the exact opposite, DJIA down 22 of the last 36 years—and often down sharply. In 2018, DJIA lost 1413 points (–5.67%) Notable gains during the week after for DJIA of 4.88% in 2000, 3.06% in 2007, 6.84% in 2009, 3.05% in 2011 and a staggering 12.84% in 2020 are the rare exceptions to this historically poor performing timeframe.

March has a mixed track record in election years. Average performance is hammered lower by steep declines in 2020 and 1980. DJIA and S&P 500 have both advanced in 11 of the last 18 election-year Marchs, but the forementioned declines drag average performance to just 0.2% and 0.4% respectively. NASDAQ, Russell 1000 and Russell 2000 are hit even harder due to fewer years of data. Declines in 2020 were the result of the covid-19 pandemic while 1980’s losses can be attributed to surging inflation that peaked at 14.6%.

Saint Patrick’s Day is March’s sole recurring cultural event. Gains on Saint Patrick’s Day have been greater than the day before and the day after. Perhaps it’s the anticipation of the patron saint’s holiday that boosts the market and the distraction from the parade down Fifth Avenue that causes equity markets to languish. Or maybe it’s the fact that Saint Pat’s usually falls in historically bullish Triple-Witching Week.

Whatever the case, since 1950, the S&P 500 posts an average gain of 0.27% on Saint Patrick’s Day (or the next trading day when it falls on a weekend), a gain of 0.06% the day after and the day before averages a 0.12% advance. S&P 500 median values are 0.18% on the day before, 0.23% on Saint Patrick’s Day and 0.05% on the day after. In the ten years when St. Patrick’s Day fell on a Sunday, like this year, since 1950, the day before (Friday) produced an average gain of 0.18%, while Monday averaged –0.03% and the following Tuesday averaged –0.13%.

Good Friday and Easter are in March this year. Historically the longer-term track record of Good Friday (page 100 of STA 2024) is bullish with notable average gains by DJIA, S&P 500, NASDAQ and Russell 2000 on the trading day before. NASDAQ has advanced 21 of the last 23 days before Good Friday. Monday, the day after Easter has exactly the opposite record and is in the running for the worst day after of any holiday. It would not be surprising to see mixed results around Good Friday this year as the day before is also the last trading day of Q1 while the day after is the historically bullish first trading day of April.

BY Doug Kass · Feb 23, 2024, 6:10 AM EST

Wolf Street howls about the "frozen" housing market.

BY Doug Kass · Feb 23, 2024, 6:00 AM EST