With a Focus on Microsoft's Growth, Here's How to Trade It Now

This balance sheet is somewhat complex, but free cash flow remains robust even in the age of AI. That's the key.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I've noticed in the wake of this week's 13-F filings that a number of funds took some profits on Microsoft MSFT but remain long the stock. I'm thinking... should we be doing the same? Truth is that I already did take a little something off of the ole fastball back in April. Not one of my better executions.

Even with that smallish reduction, Microsoft remains my most heavily weighted long position and I'm still up just less than 100% on the position even though I trade my shares on a first in, first out basis, so my least expensive purchases are no longer part of my net basis.

Some kind of news breaks with a Microsoft "mention" nearly every day, and multiple times a day. It gets difficult to keep up. Just this morning, there is the scare out of the EU that if the firm does not provide required information concerning the risks around using artificial intelligence to run the Bing search engine, that there could be fines forthcoming. On a positive note, Microsoft's planned partnership with French AO startup Mistral will not require an antitrust focused investigation in the UK.

Interestingly, discussion/social media platform provider Reddit RDDT was up over 10% early on Friday in response to news that the firm had announced a partnership with OpenAI, where OpenAI will gain access to Reddit's data and content to better train its AI models. OpenAI is backed by Microsoft. This is a change from earlier this year when Reddit had allowed Alphabet's (GOOG) Google to train its Gemini AI models using the platform's data and content.

Maybe even more interesting, on Thursday Microsoft started asking its China-based, machine learning and cloud computing workforce, believed to be between 700 and 800 individuals to relocate outside of China as tensions escalate between the US and China over new and advanced technologies.

These workers are being asked if they would like to move to the US, Ireland, Australia, or New Zealand. Guess Microsoft is expecting things to get worse regardless of who is elected in November or at least they see the risk involved in not being prepared.

Readers Will Recall That...

Microsoft reported the firm's fiscal third quarter financial results back on April 25th. Performance, as it always is, was good. This firm has been so remarkably consistent since CEO Satya Nadella took over the leadership role in 2014 after being with the firm since 1992.

Revenue generation had grown 17.1% to $61.858B. Playing inside baseball... product sales increased 9.6% to $17.08, while sales of services (& other) ran to $44.778B (+20.2%). The cost of that revenue grew 14.7% to $18,505B, leaving a gross profit of $43.353B (+18%) on a gross margin of 70.4%, which was up from 69.5%.

After accounting for operating expenses, which all grew at varied rates, operating income hit the tape at $27.581B (+23.4%). Once factoring in interest and taxes, net income printed at $21.939B, up 19.9% from the year ago comp, working out to a diluted GAAP EPS of $2.94 up from $2.45 a year ago.

Growth Where It Counts

While among the firm's business segments, Productivity and Business Processes grew sales 11.7%, and More Personal Computing grew sales 17.5%, the real action was in the Intelligent Cloud. That unit generated sales of $26.708B (+21%), which produced operating income of $12.513B (+32.1%).

Azure and the rest of the Microsoft cloud stole the show, growing revenue 31% over last year's quarter, and accelerating sequentially from 30% growth the previous quarter. The addition of AI services is helping with sales in this unit, with Microsoft's well-established relationship with and investment in OpenAI front and center.

During the call that day, CFO Amy Hood informed us that increased growth is being held back by capacity as the firm deals with "demand that exceeds our supply by a bit." Key here... Azure is growing faster than either Google Cloud or Amazon's AMZN AWS, despite being considerably larger than Google Cloud.

Under The Hood

For that period which ended March 31st, Microsoft generated operating cash flow of $31.917B. Out of that number came capex spending of $10.952B, necessarily growing about twice as fast as operating cash flow, due to the investment in AI. This left a free cash flow print of $20.965B, still up an impressive 18% year over year. The balance sheet remains in excellent shape. The firm's cash position stood at $80.021B.

Inventories were at a relatively insignificant $1.304B, putting current assets at $147.18B. Current liabilities added up to $118.525B including short-term debt of $22.784B, but also $41.888B in unearned revenue. That left the firm's current and quick ratios at 1.24 and 1.23, respectively. Once adjusted for unearned revenues, which we remember are not true financial obligations, these ratios rise to 1.92 and 1.90.

Total assets amounted to $484.275B including goodwill and other intangibles of $147.991B. At 30.6% of total assets, this is enough to watch, but not enough to worry. Total liabilities less equity came to $231.123B including $42.658B in long-term debt, and another almost $3B in unearned revenue.

This balance sheet is somewhat complex, but there is more than enough cash on hand to pay off the firm's entire debt-load and not feel stressed. In addition, free cash flow remains robust even in the age of AI. That's the key.

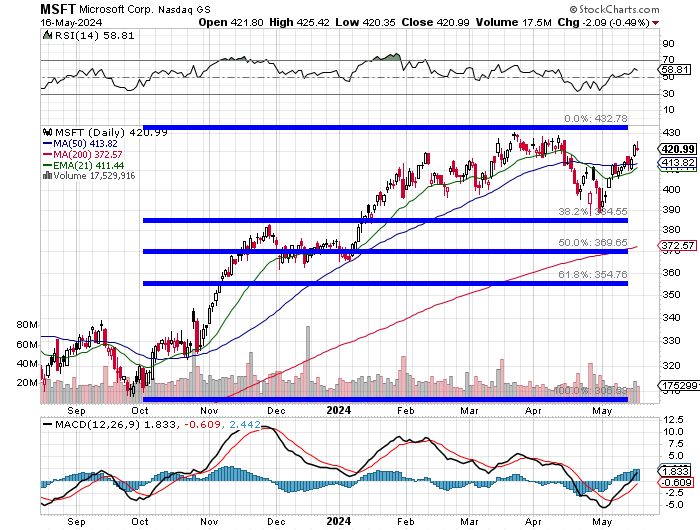

The Chart

Readers will see that the stock developed a basing period of consolidation from February into the present after the September into February rally. The area between the top of that rally and an almost perfect 38.2% Fibonacci retracement of the October into March rally, has formed a basing period of consolidation so precise, humans could not have done this.

Once again, thank your local algorithm for making technical analysis so much more accurate than ever. Though I am a big fan of the human race, it's hard to not thank the algorithmic traders who set it, forget it and read the sports section or watch kids on skateboards do stupid tricks on YouTube all day for being so darned predictable.

Relative strength has improved since late April as has the daily MACD (moving average convergence divergence) (big time). The 50-day SMA (simple moving average) had been our pivot, and that line was taken and held earlier this week. Therefore, at this time, we are going to adjust both our pivot and our target price.

Microsoft

New Target Price: $516, up from $497

Pivot: Top of base ($430), up from 50-day SMA.

Add: Down to base support ($388), up from $384

Panic: On a loss of the 200-day SMA ($374), up from $368

At the time of publication, Stephen Guilfoyle was long MSFT, AMZN equity.