Will This Marriage of Low Price and Dividends Stand the Test of Time?

Insider interest, an institutional investor increasing their stake, and a humongous shareholder payout. Sounds like a perfect match. But what's going on behind 'closed doors'?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

What if a stock under $10 and a dividend stock got married and had a baby? What would that baby look like?

Maybe B&G Foods BGS. Hmm... Let's have a look.

B&G Foods reported its first-quarter financial results last week. They missed on both the top and bottom lines. The stock sold off.

Wednesday morning, we learned that Stephen Sherrill, a B&G company director, had purchased 125K shares of the stock a couple of days after those earnings were released, with the stock still trading in the hole. We also learned through the company's 13F filing that Truist Financial had added to their still relatively small, long position in the stock during the fourth quarter.

B&G stock rallied on Wednesday in response. Let's take a look...

B&G Earnings

A week ago, B&G Foods posted adjusted first-quarter EPS of $0.18 (GAAP loss per share: $0.51) on revenue of $475.22M. As mentioned above, these results disappointed, as sales contracted 7.1%. The company made adjustments for a $70.58M goodwill impairment and $14.389M for the tax effects of the adjustment made.

After all is said and done, a net loss of $40.2M is adjusted to $14.4M. Adjusted EBITDA landed for the period reported at $75M, which was down 8.9%.

Segment Performance

Specialty generated sales of $154.729M (-4.9%), producing segment adjusted EBITDA of $37.192M (+1.9%).

Meals generated sales of $120.031M (-1.6%), producing segment adjusted EBITDA of $25.629M (-2.3%).

Frozen Vegetables generated sales of $104.887M (-16.9%), producing segment adjusted EBITDA of $7.83M (-25.1%).

Spices & Flavor Solutions generated sales of $95.576M (-5.4%), producing segment adjusted EBITDA of $28.669M (-6.6%).

Guidance

For the full year 2024, B&G Foods cut guidance across several metrics.

Net sales expectations were taken down to $1.955B to $1.985B from $1.975B to $2.02B.

Adjusted EBITDA was revised down to $300M to $320M from $305M to $325M.

Lastly, adjusted EPS was shaved for a nickel. What was $0.80 to $1.00, is now $0.75 to $0.95.

Balance Sheet

B&G Foods ended the period with a cash position of $42.46M, inventories of $560.589M and current assets of $785.321M. Current liabilities add up to $244.235M, including $22M in short-term debt. '

That leaves the company with a very healthy looking current ratio of 3.22 and a quick ratio of 0.92, which is not bad at all given the nature of the business.

Total assets amount to $3.361B, including $2.171B in goodwill and other intangibles. At almost 65% of total assets, I have to admit, I find this concerning. Total liabilities less equity comes to $2.579B including long-term debt of $2.014B.

I'm not going to lie to you. The firm is profitable. The current situation is clean. The longer-term health of the balance sheet is obviously in question as the lion's share of the assets are intangible and debt outweighs cash by about 47 to 1.

My Thoughts

The guidance is probably better than feared. I like the insider purchase. That's about it. The balance sheet is problematic. Most of B&G's businesses appear to be in decline.

Oh, one more positive thing. Did I mention the dividend? The company last cut the dividend in 2022. They may need to do so again someday, but that day may not be this year. In April, B&G paid out $0.19 per share to shareholders and has been making quarterly payments to shareholders since before the cows came home.

That comes out to an annual payout of $0.76. At recent price levels, this comes to a yield of 8.2%.

So, you have insider interest. You have an institutional investor increasing their stake, even if quite smallish, and you have a humongous shareholder payout. Food for thought.

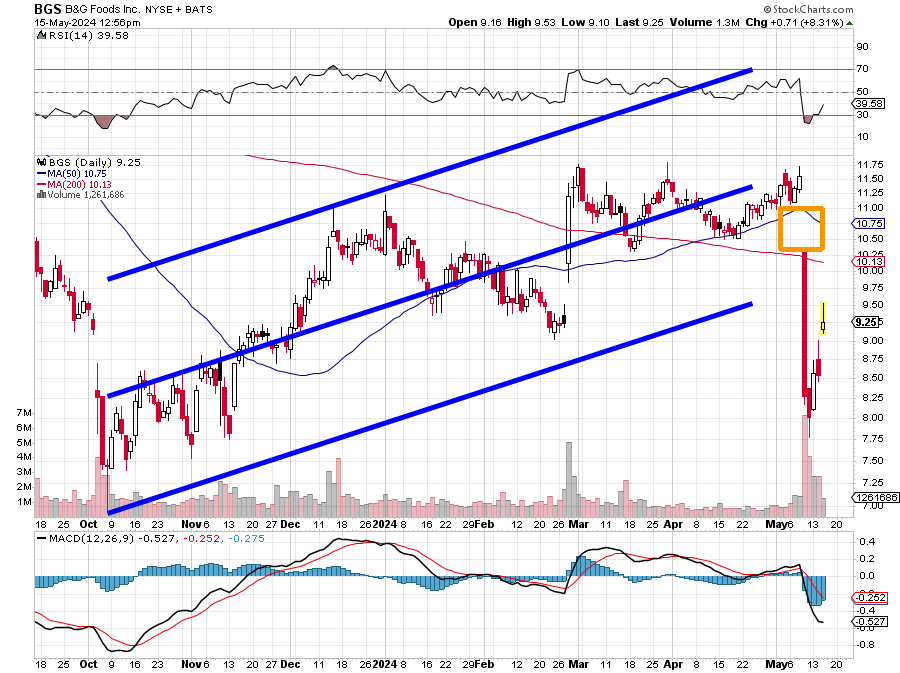

Readers will see in the chart above this week's sudden upside reversal after last week's collapse. There still remains an unfilled gap to the upside that needs the stock to trade at $11.28 to fill.

Relative Strength is starting to recover, but the daily Moving Average Convergence Divergence (MACD) is way behind. The stock needs to retake the 200-day simple moving average (SMA), currently $10.13, to get the October through early May rally back on track.

In the meantime, 8.2% is 8.2%. Beat that with T-Bills.

At the time of publication, Guilfoyle had no positions in any securities mentioned.