Why I'm Avoiding the Microsoft Dip Amid Mega Spending

I'm not as chipper as some other analysts when it comes to this Big Tech mega-cap.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Microsoft MSFT has been very, very, very good to me. On and off, Microsoft has been my most heavily-weighted long-side portfolio allocation for years. Sure, it has fallen from the top spot now and then, as names like Nvidia NVDA, CrowdStrike CRWD and SoFi Technologies SOFI (my current number one) have surpassed Microsoft due to their own stock price appreciation.

I had taken a little something off of at least the former two, as I felt they had gotten too large when they had surpassed MSFT. That saved me some nice dough, as that was just ahead of the problems that CrowdStrike had earlier this year. Overnight, though, I traded Microsoft as a day trader might, but intentionally left my long position smaller than it had been.

This is not the first time I have ever sold or "net-sold" shares of MSFT, as I have at times taken profits of joy. Wednesday night, though, was the first time in my long career that I took profits in MSFT because I was less confident in the firm. Not that I have lost confidence in CEO Satya Nadella. Nothing could be further from the truth. I am sure that he is the smartest man in the room most of the time that he stands in a room. Still, his job likely gets tougher from here. I thought moving to a reduced level of exposure might be prudent. As always, I reserve the right to change my mind once I am convinced that I may have made a mistake.

The Quarter

For the firm's fiscal first quarter, which ended September 30, Microsoft posted a GAAP EPS of $3.30 on revenue of $65.585 billion. The earnings print beat Wall Street decisively, as did the revenue print, which was good enough for year-over-year growth of 16.1%. This was the firm's greatest year-over-year acceleration in quarterly sales growth since the September quarter one year ago. Huzzah! I think.

Operations

Within that revenue print of $65.585 billion that was up 16.1%, sales of services increased 22.8% to $50.313 billion, while product sales contracted 1.7% to $15.272 billion. The cost of that revenue grew 23.3% to $20.099 billion, leaving a gross profit of $45.486 billion (+13.1%) on a gross margin that fell from 71.2% to 69.4%.

After baking in research and development; sales and marketing; and general and administrative expenses, GAAP operating income increased 13.6% to $30.552 billion as operating margin dropped from 47.6% to 46.6%. After accounting for interest, taxes and other income/losses, net income printed at $24.667 billion (+10.6%). This worked out to GAAP earnings of $3.30 per fully-diluted share.

Segment Performance

Productivity and Business Processes. generated sales of $28.317 billion (+12.3%), beating Wall Street, producing operating income of $16.516 billion (+15.5%), easily beating consensus. Within the sector, Microsoft 365 Commercial sales were up 16%, Microsoft 365 Consumer sales were up 7%, LinkedIn sales were up 9%, and Dynamics 365 sales were up 19%.

Intelligent Cloud generated sales of $24.092 billion (+20.4%), slightly beating Wall Street, producing operating income of $10.503 billion (+17.9%), which fell well short of consensus. Within the sector, Azure sales were up a strong 33%.

More Personal Computing generated sales of $13.176 billion (+16.8%), beating Wall Street, producing operating income of $3.533 billion (+15.5%), which fell well short of consensus. Within the sector, Windows OEM sales increased 2%, Search and Advertising grew 19%, and Gaming sales increased 43%.

Fundamentals

For the quarter reported, Microsoft generated operating cash flow of $34.18 billion. Out of that came capex spending of $14.923 billion (above expectations), which left free cash flow of $19.257 billion (-6.8% year over year). Out of that number, the firm repurchased $4.107 billion worth of common stock for its corporate treasury and paid out $5..574 billion in cash dividends to shareholders.

Guidance

The firm's current quarter guidance was a little sloppy, which contributed to the overnight selloff. As usual, Microsoft provides sector guidance for sales and we have to put the pieces together. Microsoft is projecting sales of $28.7 billion to $29 billion, bringing the midpoint above the $28.8 billion that Wall Street was looking for. Sales for the Intelligent Cloud are seen landing between $28.55 billion and $28.85 billion, putting the midpoint below estimates that were for $25.8 billion. Lastly, the More Personal Computing sector is expected to contribute sales of $13.85 billion to $14.25 billion, putting that midpoint way, way below the $15.1 billion that Wall Street was looking for.

Additionally, the firm projected that Azure would drive sales growth of 31% to 32%, which is an impressive rate of growth, but one that is decelerating, nonetheless. Put all the pieces together, and at the aggregate midpoint. Microsoft is projecting fiscal second quarter revenue of $68.6 billion with Wall Street looking for $69.8 billion. That's a fairly huge miss.

On top of all that, the firm did "warn" investors that capex spending is expected to rise on a sequential (quarter-over-quarter) basis based on the demands of its various cloud and AI business expansions.

Wall Street

Since these earnings were released on Wednesday night, I have come across 15 highly-rated (four-plus stars at TipRanks) that have opined on MSFT. After allowing for changes, there are 13 "buy" or buy-equivalent ratings and two "hold" or hold-equivalent ratings. Two of the "buys" and one of the "holds' did not bother setting target prices, leaving us with just 12 of those to work with.

The average target price across our remaining 12 analysts is an even $495 with a high of $550 (Brent Thill of Jefferies) and a low of $425 (Gil Lauria of DA Davidson). Kudos to Thill for rejoining the ranks of the highly rated. It's an uphill climb once lost, and it is nice to see him back up here. Once omitting those two as potential outliers, the average target price across the other 10 analysts rises to $496.50.

My Thoughts

From almost any other firm, this would be an excellent report, but Nadella has spoiled us. Since he took over and fixed Microsoft, the company has made all of the right moves and consistently outperformed expectations for both performance and guidance across the board. This time was different. Hopefully, this is a one or two off, but AI-spending is a heavy anchor to bear and the fruitful bounty on the other side of the rainbow had better be there. I do not doubt Nadella, I am just risk averse and I see this as a risky time for all of the mega-cap names who have been mega-spending.

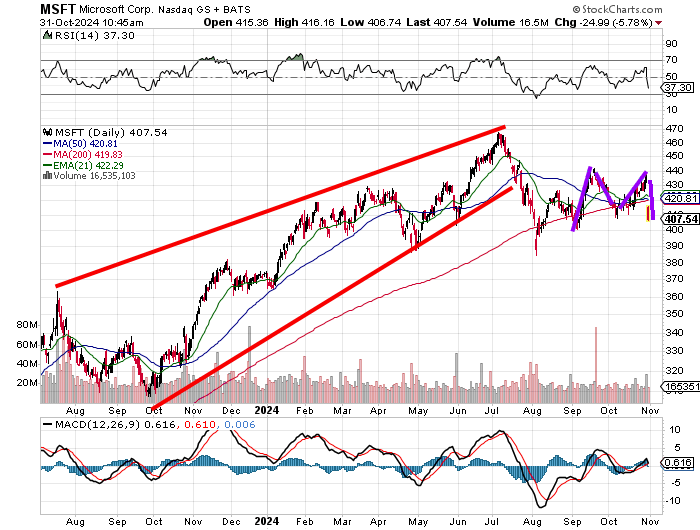

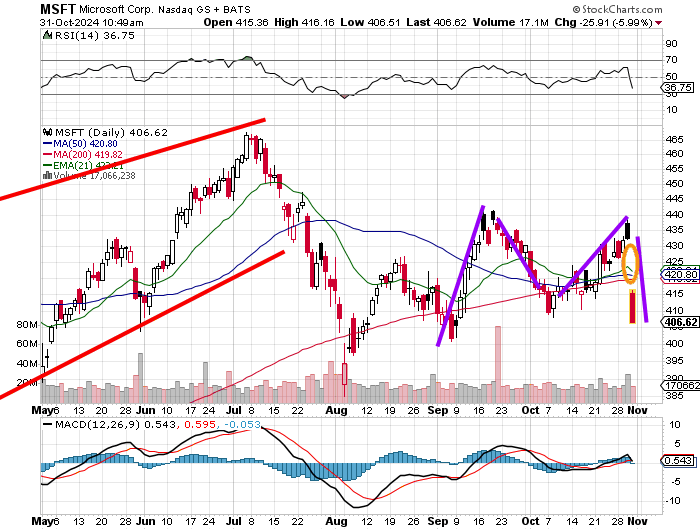

Readers will see that MSFT had come out of a rising-wedge pattern which is a pattern of bearish reversal over the summer. We had warned about this, when we last lightened up. That sell-off ensued and now the stock has put together another bearish pattern, which is the double-top pattern (in purple) that I have just drawn on this chart as I had not recognized it until last night's selling pressure had mounted. Let's zoom in.

Much easier to see now. As the gap (orange oval) is now visible, relative strength has dropped well below neutral levels, as the daily MACD suddenly emits bearish signals, with the 12-day EMA moving below the 26-day EMA and the histogram of the nine-day EMA dropping into negative territory.

As for the double-top pattern, the downside pivot now stands at $408. A close below this level opens the door to prices below $350, or at least a retest of the $385 low that was tested in both April and August.

Do I short MSFT? I am not that bold. Below $385, I am likely to buy back what I "net-sold" overnight. I believe that Nadella is one of the best CEOs in any business and one of the smartest people I have ever listened to. I do believe that he figures this out before some kind of worst-case scenario develops. That said, I am not interested in buying this dip just yet.

At the time of publication, Guilfoyle was long MSFT, CRWD, NVDA and SOFI equity.