Why Bulls Should Be Wary of Arm Holdings

The U.K.-based chip designer offers some reason for caution.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Wednesday evening, U.K.-based chip designer and developer Arm Holdings ARM released the firm's fiscal second quarter financial results. For the three-month period ended September 30, Arm Holdings posted an adjusted EPS of $0.30 (GAAP EPS: $0.10) on revenue of $844 million. These top- and bottom-line results both beat Wall Street's consensus view, while those sales reflected year-over-year growth of 4.7%.

Sales, once broken out, show 23% growth in royalty-driven revenue to $514 million and a 15% contraction in licensing and other sales to $330 million. Adjustments were made primarily for share-based compensation and for the amortization of acquisition related intangible assets.

Operations

As revenue grew 4.7% to $844 million, the cost of sales decreased 30.4% to $32 million. This left a gross profit of $812, which was up 6.85 from the year-ago comparison as gross margin improved from 94.3% to 96.2%. Total operating expenses decreased 18.3% to $748 million. That left a GAAP operating income of $64 million, from an operating loss of $156 million a year ago. After accounting for interest, non-operating income/losses and taxes, GAAP net income attributable to ordinary shareholders came to $107 million, up from the year-ago comparison of $-110 million. That works out to $0.10 per fully diluted share, up from $-0.11.

Fundamentals

For the period reported, Arm generated operating cash flow of just $6 million (not a misprint). Out of that came $53 million worth of capex spending, $7 million in the purchases of intangible assets and $11 million in payments on intangible asset-related obligations. That put free cash flow at $-65 million, down from $165 million for the similar year-ago period. For the first six months of the fiscal year, free cash flow stands at $-413 million, down from $19 million a year ago. ARM Holdings obviously does not return capital to shareholders.

Moving on to the balance sheet, Arm ended the quarter with a cash position of $2.358 billion and current assets of $4.064 billion. Current liabilities add up to $899 million including no short-term debt. That puts the firm's current ratio at a very healthy 4.52. Total assets amount to $8.086 billion, including goodwill and other intangibles of $1.825 billion. At 22.6% of total assets, this is not yet a problem. Total liabilities less equity comes to $2.074 billion. The firm has no traditional long-term debt on the books but does have $704 million in longer-term contract liabilities.

All in all, this is a very strong balance sheet.

Guidance

For the current quarter, Arm Holdings projects revenue of $920 million to $970 million with Wall Street looking for something like $945 million, which would be the midpoint of that range. The firm sees adjusted operating expenses at a rough $525 million and adjusted EPS at $0.32 to $0.36. Wall Street was looking for $0.34, so again, the guidance brackets the expectation.

For the full fiscal year, ARM sees revenue of $3.8 billion to $4.1 billion, which is where full-year guidance was three months ago. Consensus had been for $3.97 billion, so the midpoint is actually a mild disappointment. The firm sees full year adjusted EPS at $1.45 to $1.65, again, unchanged from three months ago and again, putting the midpoint below the $1.56 that Wall Street had in mind.

I see this guidance as slightly disappointing.

Wall Street

There's not a lot of opinion out there this morning on Arm Holdings. To this point, I have found ten highly-rated (four-plus stars at TipRanks) sell-side analysts that have opined on ARM. Across these ten analysts, after allowing for changes, there are eight "buy" or buy-equivalent ratings and two "hold" or hold-equivalent ratings. Three of the "buys" and one of the "holds" did not set a target price, leaving us just six of those to look at.

The average target price across the six remaining analysts is $157.33 with a high of $180 (Vivek Arya of Bank of America) and a low of $118 (Mehdi Hosseini of Susquehanna). Once omitting those two, the average target across the last four analysts rises to $161.50.

My Thoughts

I can't say that I am all that impressed with the firm's performance. Sure, the quarter beat expectations in terms of profitability and sales, but sales growth was modest at best. Operating cash flow was barely positive, and free cash flow was negative for the quarter, not to mention deeply negative for the past six months. What's so impressive about that?

What is impressive is the balance sheet. We can say that, without a doubt, this firm can survive on that balance sheet until it unscrews its other fundamentals. My disappointment comes from the fact that AI is mentioned 17 times in a two-page letter to shareholders, yet sales growth was just 4.7%, free cash flow was negative, the firm is not returning any capital to shareholders and the guidance was left where it was three months ago and landed slightly below Wall Street's expectations. Keep in mind, the stock trades at 93-times forward looking earnings. Nvidia NVDA, a designer truly cashing in on AI, trades at 51 times.

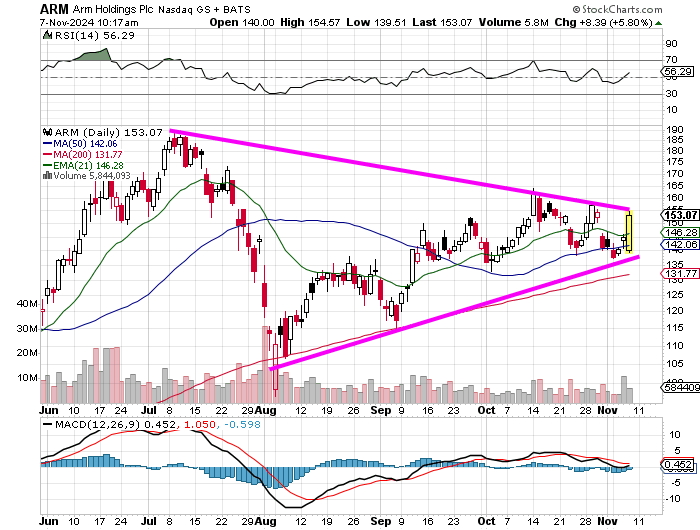

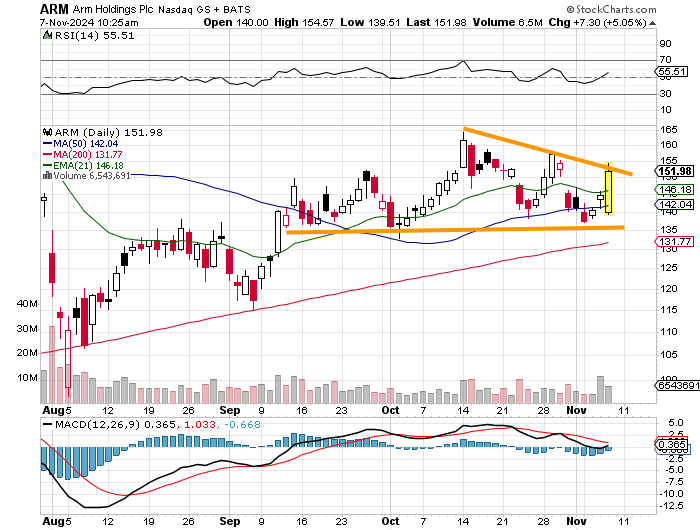

Readers will see that ARM has rallied on Thursday morning after opening on weakness. The stock has formed a giant pennant formation going back to July that appears to be coming to a close. As we know, this kind of activity often predates a volatile move. Relative strength is solid. The daily MACD is not quite bullish in posture but is getting closer.

The last sale is pressing up against that upper trendline. That, of course, could produce an upside breakout. However, should this be where resistance does show up, then the pattern is still intact. I will point out that within this pennant, there is a smaller, but more recent descending triangle pattern becoming apparent. This would be a bearish development.

This chart would be somewhat troubling to look at for the bulls. For this reason, and for the above mentioned "less than fantastic" fundamentals, I would not look to invest in Arm Holdings here. In fact, if I were to do anything, it would have more likely been a short-term trade from the short side. The reason why I will sit on my hands instead is that 11.5% of the float is already held in short positions and I do not short stocks where more than 8% of the float is already short. This one is going to be a pass for your old buddy. If I was long, I would sell some into this rally. Just a thought.

At the time of publication, Guilfoyle was long NVDA equity.