Rewiring My Nvidia Trade Outlook

True, I shed a third of my long-side exposure. Here's what I'm planning for that other two-thirds and why.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Readers of Market Recon and viewers of the "Claman Countdown" on Fox Business know that I took a third of my long side exposure to Nvidia NVDA off on Monday morning. Not that I don't love Nvidia and believe in "The Fonz" Nvidia CEO Jensen Huang. I do, and I do. One might deduce that by turning a third of my long-side exposure to the stock into cash, that two-thirds of my exposure to NVDA is still invested. Great math, if you came up with that.

This was, for me, simple risk management. I don't know how long this rotation out of artificial intelligence and AI-adjacent stocks, of which NVDA is the runaway leader, and into everything else will last. It's been a few days. It could stop now. It could go on for a lengthy period. Largely, the economy will likely let us know. If, as I suspect, economic growth slows, and after August, consumer level inflation accelerates to some degree, there will be at least a modestly stagflationary environment to deal with.

What will do well, or at least better than bad in that environment? Commodities, commodity-based exchange-traded funds, and in equities, probably utilities for their dividends, and elite tech, for their growth, operating and free cash flows, and clean balance sheets. While that does not sound so hot for the likes of you and I, it does sound like an environment in which stocks like Nvidia, even if they do not excel, can outperform. We are always ready to adapt. We always strive to excel in all things we do. The least we'll find satisfactory in our own performance, is outperformance.

Always faithful.

The Run, and the Sprint

Nvidia had already been hot. After the close on May 22, the company posted its first quarter financial performance. On both sales and profitability, Nvidia crushed expectations. Nvidia beat consensus for the revenue print by close to $1.5 billion. The stuff of fantasy. The stock had come in trading at an adjusted $94.95, but opened at an adjusted $106.32 the next morning and nearly hit $115 just a couple of days later. The race was on. Thanks to those earnings, thanks to healthy guidance, and perhaps mostly ... thanks to the announcement of a 10 for one stock split, which has since been implemented and is the reason the above prices are adjusted.

By the morning of last Thursday, before reversing lower, NVDA traded as high as $140.76. That's a 48.3% run in less than a month. I don't know if very many readers remember this, but in response to those earnings, I put a target price of $1,125 on the stock. That's a post-split $112.50, so taking something off of my position well above what had been my target price, isn't only understandable, it was actually tardy and a violation of my own code of discipline. Yes, it did make me a little extra dough. No, my ego does not handle a failure on my part to stay disciplined very well. Getting away with being sloppy once, will breed a more lax attitude. Being sloppy breeds failure.

Smart? If you're here, you're smart. Likely everyone contributing to and reading the material on this site easily qualifies for Mensa. We cannot always outsmart the kids to our left or right. We can always work harder. We can always maintain personal discipline.

Fundamentally Pretty Solid

Glancing at the fundamentals, for that first quarter, I see Nvidia generated operating cash flow of $15.345 billion, up 33.5% sequentially and up 427.1% from the year-ago comp. Out of that number came capital spending of $369 million and principal payments on property and equipment of an additional $40 million, which left free cash flow of $14.936 billion (+33.2% q/q and +465.1% y/y).

Looking at the balance sheet, the cash position stood at $31.438 billion (+9.4% in just three months) as inventories stood at $5.864 billion. That put current assets at $53.729 billion. Current liabilities added up to $15.223, including $1.25 billion in short-term debt. That worked out to current and quick ratios of 3.53 and 3.14, which is quite robust, but especially for a firm this size.

Total assets amounted to $77.072 billion, including goodwill and intangibles of just $5.439 billion. At 7% of total assets, that would be of no concern to folks like myself who take fundamental analysis seriously. Total liabilities less equity came to $27.93 billion, including $8.46 billion in long-term debt. Yes, at that time, the company could have paid off its entire debt-load out of cash and gotten more than $2 billion back in change. I love writing that.

Revised Strategy

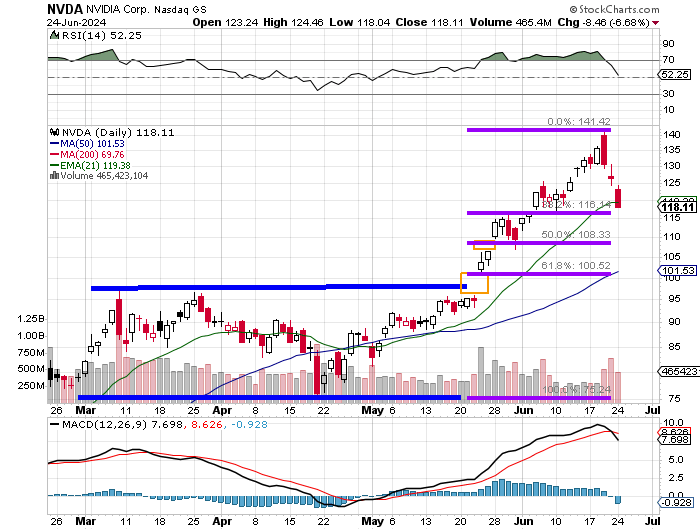

Let's take a look at the chart:

Readers will see that for NVDA, over just three days, Relative Strength has fallen out of bed and is now neutral. The daily moving average convergence/divergence indicator suffered a bearish cross-under by the 12-day exponential moving average through the 26-day EMA. These are fairly negative indicators. On the bullish, or at least supportive side, the stock closed at an almost precise 38.2% Fibonacci retracement level of the mid-April through last week's top move.

Even after seeing NVDA trading lower overnight, I would think that at least one more attempt at that Fib level could be in the cards. Should Nvidia hold there, not only will NVDA resume its northerly march, but the whole market-wide rotation could reverse.

Now, if that trap door opens, the 61.8% Fib level shows up at roughly par ($100). If the stock gets that far, the price will enter the unfilled gap created on May 23. To fill that gap, a tick at $96 or lower would be required. That is for now, my very worst-case scenario.

Nvidia Plan

Target Price: $125 (23.6% Fib level)

Pivot Point: $97

Add: From the half-way back point ($115) down to the gap fill ($96)

or on upside momentum above target $125. Target would then be adjusted.

Panic: Break of 78.6% Fibonacci level ($89)

At the time of publication, Guilfolye was long NVDA equity.