Snowflake Could Be Headed Lower Before Seeing Gains

After narrowly beating Wall Street in its latest report, the cloud computing company has seen its share price dip.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Wednesday evening, after equities had rallied in response to a weaker-than-previously-reported labor market and a more-dovish-than-previously-known FOMC, AI data cloud provider Snowflake SNOW released the firm's fiscal second quarter financial results.

For the three-month period ended July 31, 2024, Snowflake posted an adjusted EPS of $0.18 (GAAP EPS: $-0.95) on revenue of $868.823 billion. These top- and adjusted bottom-line results both narrowly beat Wall Street's expectations, while the revenue print was good enough for year-over-year growth of 28.9%. Adjustments were made for stock-based compensation expense and the amortization of acquired intangibles.

The firm can boast a net revenue retention rate of 127% and 510 customers with trailing 12-month revenue contributions greater than $1 million. The firm now has 736 customers among the Forbes Global 2000 and a remaining performance obligation of $5.2 billion, which is up 48% over this time last year. Additionally, Snowflake has now authorized the repurchase of an additional $2.5 billion worth of common stock through March 2027.

Operations

As mentioned above, for the period reported, Snowflake generated revenue of $868.823 million (+28.9). Within that number, product driven revenue grew 29.5% to $829.25 million, while services and other revenue increased 17% to $39.573 million. The cost of revenue grew 31.9% to $288.078 million, leaving a gross profit of $580.7 (+27.5%) on a gross margin of 66.8%, down from 67.6%. Product specific gross margin ran at 72%, or an adjusted 76%.

Operating expenses increased 26.3% to $936.048 million, leaving a GAAP operating income/loss of $-355.303 million, down from $-285.407 million for the year-ago comp. Once adjusted, operating income printed at $43.7 million on an adjusted operating margin of 5%.

After accounting for interest and taxes, GAAP net income/loss attributable to shareholders came to $-316.899 million, down from last year's comp of $-226.867 million. That works out to $-0.95 per diluted share, down from $-0.69. Once adjusted, net income comes to $63.85 million, down from last year's comp of $80.743 million. This works out to an adjusted EPS of $0.19, down from $0.25.

Guidance

For the current quarter, the firm sees product-driven revenue of $850 million to $855 million, which at the midpoint would be good for annual growth of 22%. Consensus on Wall Street was for about $848 million. Adjusted operating margin is seen at 3%. For the full fiscal year, the firm is projecting product-driven revenue of $3.356 billion, up from prior guidance of $3.3 billion. This would be good for year-over-year growth of 26%. Consensus view had been for the original guidance of $3.3 billion. For the full year, the firm also sees adjusted product gross margin of 75%, an adjusted operating margin of 3% and a free cash flow margin of 26%.

Fundamentals

For the quarter reported, Snowflake generated operating cash flow of $69.865 million (-16% year over year). Out of this number came capex spending of $5.043 million and spending of $5.992 million on capitalized internal use software. That left free cash flow of $58.83 million (-14.8%). Out of that number, the firm, which does not pay shareholders a dividend, did repurchase $400 million worth of common stock. You know how I feel about returning more capital to shareholders than a firm has in free cash created. That said, the firm does have a large cash position, so this is not a foul.

Turning to the balance sheet, Snowflake ended the period with a cash position of $3.23 billion and current assets of $3.898 billion. Current liabilities add up to $2.465 billion, of which $1.848 billion is in the form of deferred revenue., which we know is not a true financial obligation. There is no short-term debt. That brings the firm's current ratio, at the headline, to a healthy enough 1.58. Once adjusted for deferred revenue, that ratio rises to an incredibly strong 6.32.

Total assets amount to $6.944 billion, including $286.538 million in goodwill. At 4% of total assets, this is of no concern. Total liabilities less equity comes to $2.807 billion. There is no long-term debt either. This is one very strong balance sheet.

Wall Street

Since these earnings were released last night, I have come across 18 highly-rated (four-plus stars at TipRanks) sell-side analysts that have opined on SNOW. After allowing for changes, across the 18 analysts, we have 13 "buy" or buy-equivalent ratings and five "hold" or hold-equivalent ratings. One of the "buys" and two of the holds did not set target prices, so we are working with just 15 of those.

The average target price across these 15 analysts is $176.40 with a high of $220 (Kash Rangan of Goldman Sachs) and a low of $130 (Mark Moerdler of Bernstein). After omitting those two as potential outliers, the average target across the remaining 13 rises ever so slightly to $176.62. For those with an interest, the average buy target is $181.75, and the average hold target (of just three) is an even $155.

My Thoughts

Was this a bad quarter? No. Are margins in decline? Seems so. Is the firm suffering from competition in the enterprise "big data" software as a service space? The still private Databricks is surely a competitive threat. Palantir PLTR is, in some ways, a competitor, providing a data-based generative AI platform that offers insight taken from an aggregation of data. They don't seem to directly compete though. That said, the big kids in the space such as Microsoft's MSFT Azure, Amazon's AMZN Athena and Oracle ORCL do offer many of the same warehousing and analytical services.

Other than that, growth is still strong, even if decelerating. Cash flows are positive. The guidance was not bad, but perhaps not quite what analysts had hoped for. The balance sheet is a beauty and may have to be relied upon should the business and the profitability of the business continue to slow just a bit.

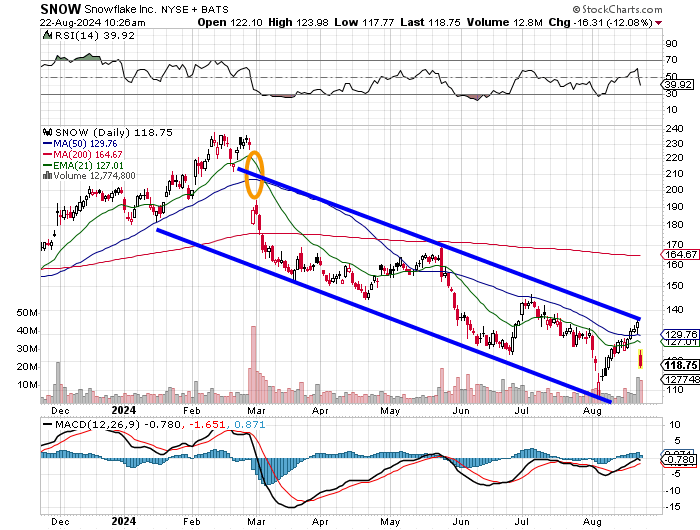

Readers will see that SNOW experienced a mini-double top reversal in February, leaving an unfilled gap in its wake that would require a print of $233 or higher to fill. Out of that came a downward sloping price channel that had tested breaking out of its moving range going into earnings only to see a sharp rejection in response to the numbers.

This morning, the stock has already given back its 50-day SMA, forcing some portfolio managers to reduce long-side exposure and its 21-day EMA, which got the swing crowd out. RSI is now much weaker and the daily MACD, which was headed toward bullishness, will take a turn for the worse.

My feeling? No promises, but should the downward moving range hold true as it has for six months now, this stock, which is clearly unloved at this point, could trade at $100 before it trades at $130.

At the time of publication, Guilfoyle was long PLTR, MSFT and AMZN equity.