ServiceNow Is Still Rockin' With CEO Bill McDermott: Here's How to Trade It

The company has been an early adopter of generative AI capabilities and adapted to its big data, cloud-based workflow management software models.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

ServiceNow NOW released the firm's fourth quarter financial results on Wednesday evening and color me biased if you like as I am long the shares, but the firm is still rockin' and CEO Bill McDermott is still the coolest.

For the three month period ended December 31st, the cloud based, workflow management software company posted an adjusted EPS of $3.11 (GAAP EPS: $1.43) on revenue of $2.437B. That compares to year ago comps of $2.28 and $0.74, respectively, and shows revenue growth of 25.8%. Revenue growth has now accelerated on a year over year basis for four consecutive quarters. The lion's share of the adjustments made was again for stock-based compensation expense ($413M), which was partially offset by income tax adjustments and the release of a valuation allowance of some tax-deferred assets.

Subscription revenues grew 27% in the fourth quarter from the year ago comp to $2.365B. Current remaining performance obligations as of quarter and year's end landed at $8.6B, good for growth of 24%. The firm had 168 transactions of over $1M in net new ACV (annual contract value) during the quarter, up 33% over the same period last year. The company now has 1,897 total clients with more than $1M in ACV, which represents a 15% year over year growth in customers of that size.

Operations

As those (mostly subscription) revenues were growing 25.8%, total cost of revenue increased 24.3% to $516M, leaving gross profit of $1.921B (+26%) or adjusted gross profit of $2.007B (+25.4%). That makes for a gross margin of 78.8%, up from 70.6% a year ago (adjusted 82.4% down from 82.5%).

Operating expenses increased 20.5% to $1.615B, leaving an operating income that increased 74.2% to $270M or an adjusted $717M (+31.8%). After accounting for interest and taxes, net income wound up at $295M (+96.7%), which is how one gets to $1.43 per share. Adjusted net income printed at $643M (+38.6%), which works out to $3.11 per share.

Chairman & CEO Bill McDermott From the Conference Call...

"ServiceNow's Q4 performance is packed with milestones spanning the full breadth of our portfolio. With technology, customer, and creator, we now have three workflow businesses over $1 billion in ACV. We have 11 individual product lines with north of $250 million in ACV."

"Our core business is rock solid and growing. Our perimeter is growing. Our platform adoption is growing. We are, in fact, in a new era of business transformation powered by AI. This is unlocking massive opportunity in the enterprise software industry. And ServiceNow is extremely well-positioned, not only to lead this movement, but to define it."

CFO Gina Mastantuono From the Press Release...

"Once again we exceeded our topline growth and operating margin guidance metrics, showcasing ServiceNow's consistent and relentless focus on execution,"

"We ended Q4 with a 99% renewal rate, accelerating large new logo growth, and the strongest NNACV contribution for any new product family with the introduction of our Plus SKUs. The accelerating pace of investment in workflow automation and generative AI positions us well for another strong year and we are raising our outlook for 2024."

Guidance

For the first (current) quarter, subscription revenue is seen growing 24% to 24.5% to a range spanning from $2.51B to $2.515B, cPRO is seen growing 20% as operating margin is seen at 29%. For the full calendar 2024 year, subscription revenue is projected to increase 21.5% to 22% to a range spanning from $10.555B to $10.575B. This increases the midpoint of this range by $165M from previously given guidance. For the full year, subscription gross margin is seen at 84.5%, operating margin is seen at 29% and free cash flow margin is seen at 31%.

Fundamentals

For the quarter reported, ServiceNow generated operating cash flow of $1.605B. Out of that number came CapEx spending of $261M, leaving free cash flow of $1.344B. Out of that number, the firm repurchased $256M worth of common stock. The rest was used to pay taxes and further strengthen the firm's balance sheet.

Looking at that balance sheet, ServiceNow ended the quarter/year with a cash position of $4.877B and current assets of $7.777B. Current liabilities add up to $7.365B, including a whopping $5.785B in deferred revenue. As we know, deferred revenues are not financial obligations. So, on the surface, the firm's current ratio stands at 1.06, which would pass muster as is, but adjusted for those deferred revenue, the firm's current ratio rises to a beastly 4.92.

Total assets amount to $17.387B including $1.455B in goodwill and other intangibles. At 8.4% of total assets, this is more than fine. Total liabilities less equity comes to $9.759B, including $1.488B in long-term debt, which is something the firm could take care of more than three times over out of pocket if so desired. This balance sheet is golden.

Wall Street

Since these earnings were released last night, I have come across 22 highly rated (four stars plus at TipRanks) sell-side analysts that have opined on NOW.

After allowing for changes, among these analysts, we have 21 "buy" or buy-equivalent ratings and one "hold" rating (who raised his target price). One of our "buys" did not set a target, so we are working with 21 of those.

The average target price across the 21 analysts is now $883.48 with a high of $900 -twice (Mike Cikos of Needham and Bradley Sills of Bank of America) and a low of $750 (Joel Fishbein of Truist Financial). Once omitting one of those highs and that low as potential outliers, the average target across the other 19 comes to $889.63.

My Thoughts

I have long been a big fan of Bill McDermott. He's done wonders for my P/L and more than just once or twice. That does color opinion though we try to maintain objectivity. The stock does trade at 60 times forward looking earnings and more than 18 times sales. That's expensive in almost anyone's book.

The truth is that I have sold this stock in the past based on valuation and I have lived to regret those sales. Because I have been in and out of the stock over the past few years, I am "only" up 40% on this position. If I had never bobbed and weaved, thinking I was outsmarting Mr. Market, then we would be talking about a gain of multiple three figures in percentage terms.

ServiceNow is one of those names that has been an early adopter of generative AI capabilities and adapted to its big data, cloud-based workflow management software models. Its customers have obviously adapted right along with it.

There are a handful of stocks that are not moving on valuation or even fundamentals seen through the prism of decades in the business. These stocks are moving on momentum in the flow of capital and I do not think can be sold again until technically broken, which is certainly not the case here.

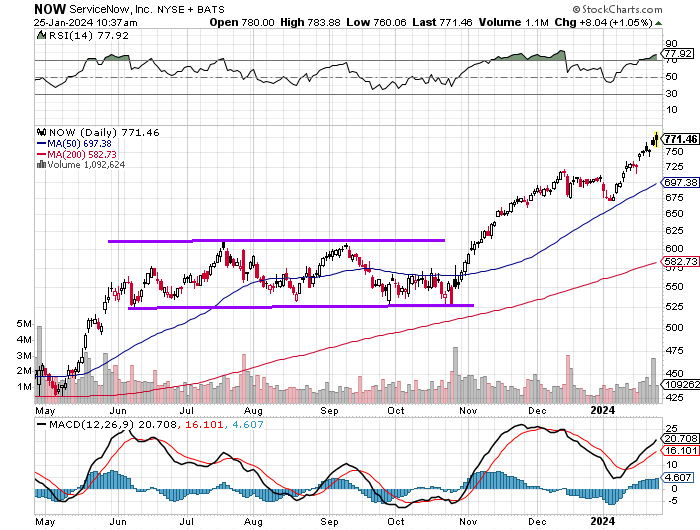

Looking back over the past nine months or so, readers will see that NOW consolidated from early June into late October and then burst past a $615 pivot to where it is now. Relative Strength is extended. Again. The daily MACD (moving average convergence divergence), looks extended as well.

Now is when we watch. Will the stock break or consolidate again? It needs to do one or the other. Consolidation in this environment is probably not enough of a catalyst for me to take my leave.

Forget about the 50 day SMA (simple moving average). That is where support for a basing period could show up. I'm not cutting unless the 200 day SMA cracks and that's all the way down at $582. So, I'll likely be here with Bill for a while unless the story changes dramatically. Check this out...

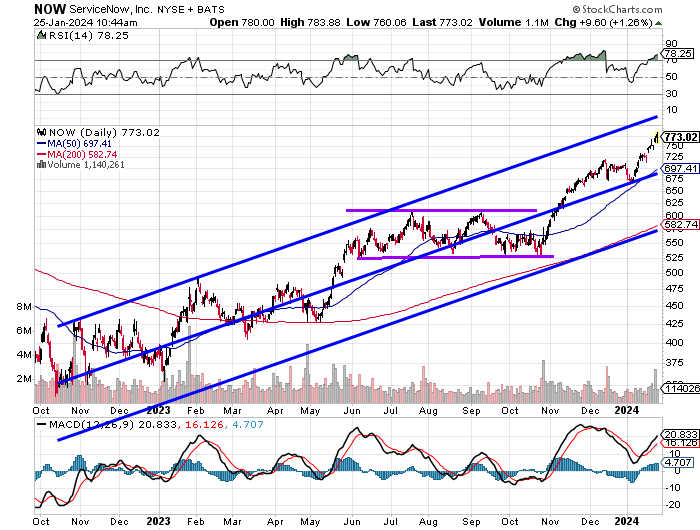

We pushed the chart out a little further. The entire rally going back to the lows of October fits neatly within this Raff Regression model. I almost used an Andrews' Pitchfork, but I think this shows the trend a little more clearly. I see the top of this model, let's call it $800 as a pivot. Resistance there, we'll need the 50 day line to step up.

However, if the stock takes $800 and that level holds on at least one retest? Then, we're talking target prices above $950.

At the time of publication, Stephen Guilfoyle was long NOW equity.