It's Prudent to Reduce Microsoft Exposure

After an earnings miss for Microsoft, it's prudent to take some shares off.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It got pretty ugly on Tuesday evening, at least for the shares of Microsoft MSFT just after the release. The numbers for Azure and the Intelligent Cloud disappointed to a degree, and the algos went wild. However, after a solid call where CEO Satya Nadella and CFO Amy Hood calmed investors, along with an adjacent release by chip designer Advanced Micro Devices AMD, much of the damage had been contained by the time most of us ripped our greasy craniums way from those comfy but probably smelly things we call pillows.

Let us begin. For the firm's fiscal fourth quarter, which ended on June 30, 2024, Microsoft posted a GAAP EPS of $2.95 on revenue of $64.727 billion. These top- and bottom-line numbers both beat Wall Street's expectations while the sales print reflected annual growth of 15.1%.

Operations

Within revenue, which was up 15.1% to $64.727 billion, sales of services were up 31% to $51.51 billion, and product sales were down 21.6% to $13.217 billion. The cost of revenue was up 17.2% to $19.684 billion. This left a gross profit of $45.043 billion (+14.3%) on a gross margin of 69.6%. That was down from the year-ago comp of 70.1%, but did beat expectations.

Operating expenses grew 13.1% to $17.118 billion, leaving an operating income of $27.925 billion (+15.1%), also beating Wall Street. Operating margin dropped slightly to 43.1% from 43.2%, but also beat consensus. After accounting for interest and taxes, net income hit the tape at $22.036 billion (+9.7%), narrowly beating what Wall Street was looking for. This works out to $2.95 per diluted share, which was up from $2.69 for the year ago comp.

Segment Performance

- Intelligent Cloud generated revenue of $28.515 billion (+18.9%), which fell just short of expectations. The segment produces operating income of $12.859 billion (+22.1%), which beat expectations. Server Products and Cloud was up 21%. Azure and Other Cloud was up 29%, with 8% attributable directly to AI. Wall Street was looking for 30% growth here, which is the primary reason why the stock sold off hard just after Tuesday's closing bell. Enterprise Mobility grew 10%.

- Productivity and Business Processes generated revenue of $20.317 billion (+11.1%), which beat expectations. The segment produces operating income of $10.143 billion (+12.1%), which also beat expectations. Within the group, Office Commercial and Cloud increased 12%, Office Consumer and Cloud grew 3%, Microsoft 365 subscriptions were up 10%, LinkedIn was up 10%, and Dynamics and Cloud was up 16%.

- More Personal Computing generated revenue of $15.895 billion (+14.3%), which beat expectations. The segment produces operating income of $4.923 billion (+5.3%), which also beat expectations. Within the segment, Windows OEM grew 4%, Windows Commercial and Cloud grew 11%, Search and News Advertising was up 19%, and Devices decreased 11%. Xbox hardware tumbled 42%, but Xbox services grew 61%.

Guidance

The firm provided very granular current quarter guidance during the call, as it usually does. When broken out, the firm sees the Intelligent Cloud segment generating revenue of $28.6 billion to $28.9 billion, which would be growth of 18% to 20%. Within the Intelligent Cloud, Azure is seen growing 28% to 29%. Productivity and Business Processes is expected to drive revenue of $20.3 billion to $20.6 billion, which would be growth of 10% to 11%. More Personal Computing is seen generating revenue of $14.9 billion to $15.3 billion, which would be growth of 9% to 12%. Put all together, the firm is expecting to drive revenue of $63.8 billion to $64.8 billion, which was a little below what the street was looking for. That said, the guidance for the Intelligent Cloud, which is currently the most important segment for the stock, was a little ahead of expectations.

The Call...

CEO Satya Nadella said, "Our Microsoft Intelligent Data Platform provides customers with the broadest capabilities spanning databases, analytics, business intelligence, and governance along with seamless integration with all of our AI services. The number of Azure AI customers also using our data and analytics tools grew nearly 50% year-over-year.

"Copilot for Microsoft 365 is becoming a daily habit for knowledge workers, as it transforms work, workflow, and work artifacts. The number of people who use Copilot daily at work nearly doubled quarter-over-quarter, as they use it to complete tasks faster, hold more effective meetings, and automate business workflows and processes."

CFO Amy Hood, answering a question, added, "And, Mark, to answer the second half of your question on margin improvement, looking different than it did through the last cloud cycle. That's primarily for a reason I've mentioned a couple of times. We have a consistent platform. So because we're building to one Azure AI stack, we don't have to have multiple infrastructure investments. We're making one. We're using that internally first-party, and that's what we're using with customers to build on as well as ISVs. So, it does, in fact, make margins start off better and obviously scale consistently."

Fundamentals

For the period reported, Microsoft drove operating cash flow of $37.195 billion (+29.3%). Out of that number came capex spending of $13.873 billion, leaving free cash flow of $23.322 billion (+17.7%). Out of that number, the firm repurchased $4.21 billion worth of common stock for its treasury, while returning $5.574 billion in cash dividends to shareholders. The rest was put into debt repayment. Turning to the balance sheet, Microsoft ended the quarter with a cash position of $75.543 billion and inventories of just $1.246 billion. This left current assets at $159.734 billion. Current liabilities add up to $125.286 billion, including $8.942 billion in shorter-term debt, but also $57.582 billion in unearned revenue, which is not a true financial obligation.

This puts the firm's headline current ratio at a "good enough" 1.28. However, once adjusted for unearned revenue, that current ratio rises to a beastly 2.36. Inventories are so small; I don't think it's necessary to do a quick ratio. Total assets amount to $512.163 billion, including $146.817 billion in goodwill and other inventories. As large as that is, at 28.7% of total assets, it does not raise eyebrows. Total liabilities less equity comes to $243.686 including $42.688 billion in long-term debt. The debt-load seems like a lot, but the firm can pay it off out of pocket and has shown in the past quarter that reducing the debt-load is on its agenda. This balance sheet is in very good shape.

Wall Street

Since these earnings were released last night, I have found 14 highly-rated (four-plus stars at TipRanks) that have weighed in on MSFT. All 14 of these analysts rate the stock as either a "buy" or their firm's equivalent. One analyst did not set a target price. The average target across the other 13 is $495.15 with a high of $515 (Kash Rangan of Goldman Sachs) and a low of $47 (Mark Murphy of JP Morgan). Once omitting those two as potential outliers, that average target across the other eleven analysts barely rises to $495.63.

My Thoughts

Another very solid, very well-balanced quarter turned in by Microsoft. Was everything perfect? Not in the most utopian sense. Was everything at least "good"? Everything except gaming, in my opinion. Microsoft remains the AI leader in my opinion on the software side and on the enterprise side. That's going to require continuous spending, but it does look like Microsoft's customers, both commercial and on the consumer side are becoming increasingly dependent upon artificial intelligence in the daily completion of their tasks.

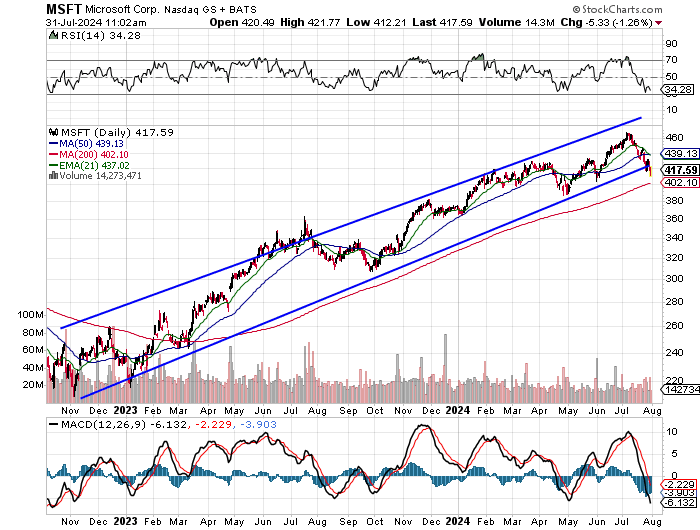

Microsoft has long been the most heavily-weighted single position on my book, with the recent exceptions of CrowdStrike CRWD and ServiceNow NOW that exploded post-earnings and had to be pared back just to keep them in line. Then CrowdStrike did a lot more paring back on its own, which is not central to this piece. The heavy weighting that has hovered at a rough 10% has served me well as folks can see in the above 18-month ascending price channel. That channel has cracked though. Even with this overnight into morning charge back towards last night's closing price. I see something else developing. Take a look at this:

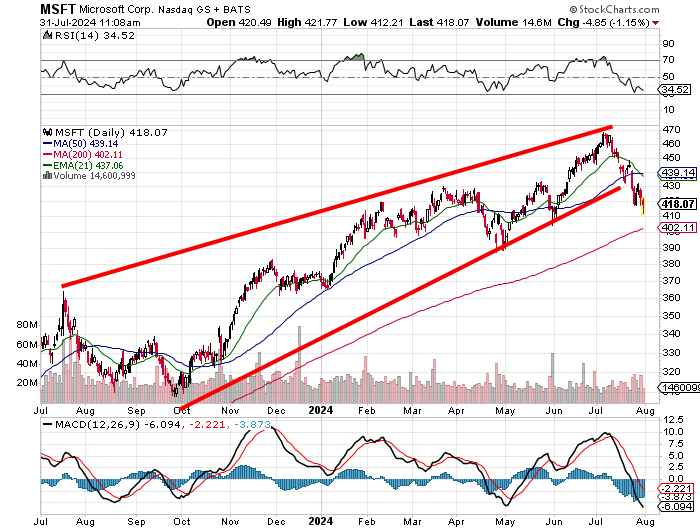

The price channel has morphed into a rising wedge, which is a pattern of bearish reversal. Relative strength remains weak. The daily MACD is extremely bearishly postured. The breakdown has started. The stock looks for support at its 200-day SMA as the 21-day EMA has slipped below the 50-day SMA. This will throw the swing traders a little bit offside.

While I intend to remain long MSFT and maintain its spot among my most heavily-weighted positions, I think it prudent to use this overnight-into-morning rally to take a few shares off and reduce this weighting to 8% or 9%, which is still very heavy. It's called risk management. The upside pivot becomes the 50-day SMA. The target becomes $505. However, should the 200-day SMA crack for real, I will be ready to take this position down to 5% of the portfolio.

More TheStreet Pro:

- The Most Important Thing I've Learned in 25 Years of Trading

- Day Trading Is Very Difficult: Here Are 6 Tips for Long-Term Success

- Everything You Ever Wanted to Know About the CNN Fear & Greed Index

At the time of publication, Guilfoyle was long MSFT, AMD, CRWD and NOW equity.