Poor Outlook for AppLovin After S&P 500 Dissapointment

The software provider seems to be building a bearish pattern after being denied entry into the power index.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Let's talk about AppLovin APP.

The AppLovin Corporation provides a software platform primarily made up of four key "solutions." These business units are AppDiscovery, MAX, Adjust and Wurl. App Discovery, powered by AXON AXON, matches advertiser demand with publisher supply through auctions at scale and at great speed. MAX utilizes an advanced in-app bidding technology that optimizes the value of a publisher's advertising inventory. Adjust is an analytics marketing platform, and Wurl is a connected television platform that provides advanced advertising and publishing solutions, while distributing streaming video content.

The company has grown wildly. For its third quarter, which was reported back in early November, AppLovin posted a GAAP EPS of $1.25 on revenue of $1.2 billion. These top- and bottom-line numbers both beat Wall Street, and that bottom-line print far exceeded Wall Street's estimates for the firm's profitability. This was just the firm's sixth consecutive profitable quarter, while revenue generation started to ramp significantly on a year-over-year basis late in 2023. Sales growth came to 38.8% for that most recent quarter.

For those about to ask, the fundamentals are strong. Free cash flow has been positive since 2022. The balance sheet, at least on a current basis, is quite robust. Longer-term, there is a bit of debt on the books that will have to be dealt with, but as I mentioned, the cash flows are there in addition to a cash position greater than $1 billion.

The Stock?

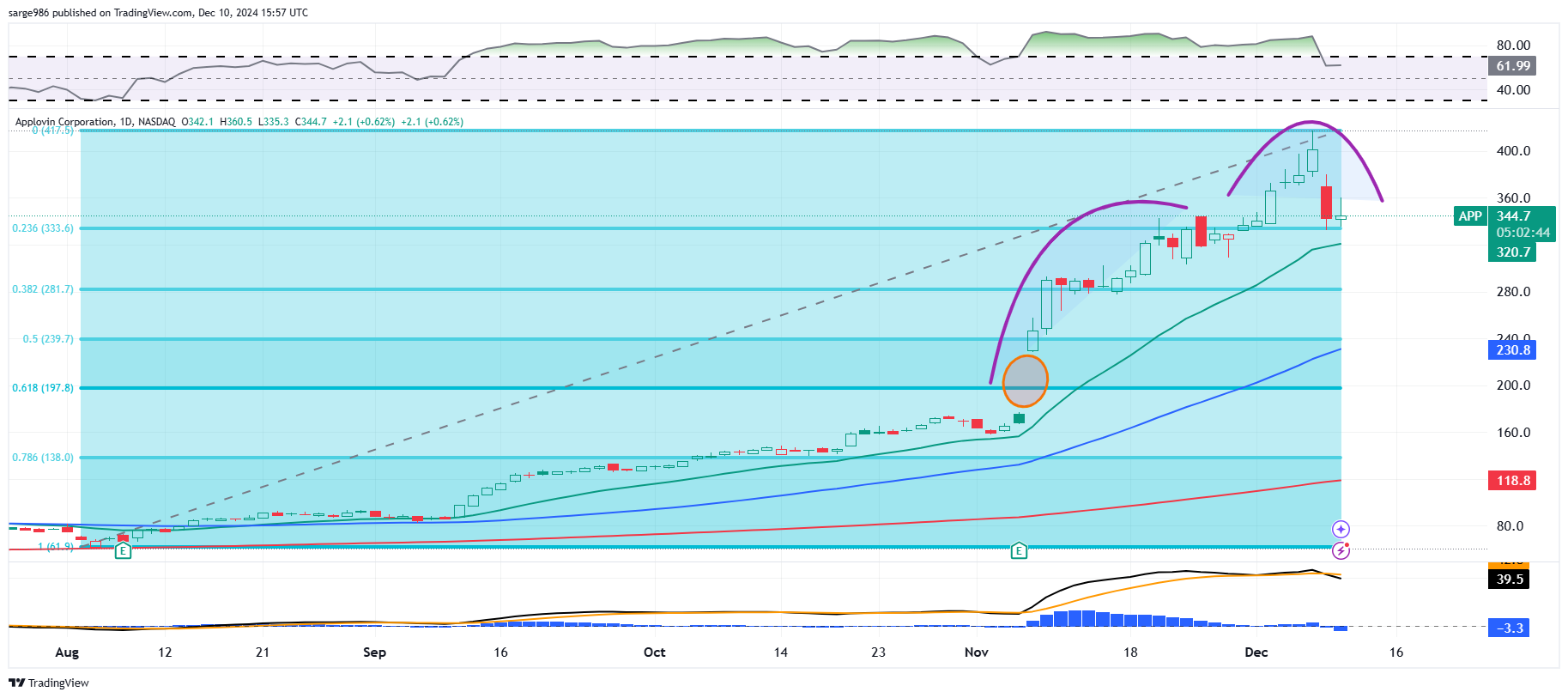

Had been out of control since rumors circulated that APP could be added to the S&P 500. The shares apexed on Friday at $417.64, up from an August low of $60.67 (+588%). However, the stock gave back 14.68% (down almost $59 per share) on Monday. Problem?

Denied!

The shares of AppLovin experienced their worst day of the year and in a couple of years after the firm was not included in the benchmark S&P 500 despite all of the incoming speculation. Apollo Global Management APO and Workday WDAY will be added to the S&P 500, according to Monday's press release, while Qorvo QRVO and Amentum Holdings AMTM will be deleted. Both of those names will be downsized to the S&P SmallCap 600.

To be eligible for the S&P 500, companies must have a market cap of at least $18 billion, must be profitable for the most recent quarter and for the most recent four quarters in the aggregate. The shares of prospective stocks must also be liquid, meaning that there must be sufficient monthly trading volume in the names. Another name that many thought would be added, that has also had a great year, but was not, is Coinbase Global COIN.

My Thoughts?

AppLovin is expensive. Not that this has stopped me before, when I believe in the narrative. Palantir PLTR comes to mind, but I believe in their mission and in the idea that what they provide to the U.S. government and commercial clients is fast becoming inelastic in terms of demand. This, I'm not so sure of. Would It really take much for this space to become significantly more crowded?

APP trades at 55-times forward-looking earnings, 122-times trailing 12-month earnings, 33-times sales and 144-times book. That's pretty steep. Less than 6% of the float is held in short positions, so the cavalry is not waiting to cover their positions.

On the positive side of the coin, readers will see that both on Monday and so far on Tuesday support has been found at the 23.6% Fibonacci retracement level of the entire August into December rally. In addition, Relative Strength is still strong, but no longer technically overbought.

Now, for the negative. The shares appear to be building what could be a bearish head-and-shoulders pattern that's about two-thirds of the way there. The daily MACD is now postured quite bearishly, with the nine-day EMA in negative territory and with the 12-day EMA now below the 26-day EMA. There is also an unfilled gap left over from early November that would need a tick as low as $177 to fill.

APP will get another shot at the S&P 500, so I don't expect the shares to head all the way back from where they came or even threaten to fill that early November gap anytime soon. That said, I think it is quite likely that APP will test its 21-day EMA and maybe its 50-day SMA from above. For that reason, I'm not even thinking of initiating anything on the long side until we see these shares trading in the mid-$320s.

At the time of publication, Guilfoyle was long PLTR equity.