Palantir Downgrade? Thanks a Lot!

PLTR can stand on its balance sheet alone. Here's my plan and why I'm bullish.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Say What? ... Brian White of Monness, Crespi, Hardt & Co. is a really good analyst. On that point, I have no argument. On Friday morning, however, White, who is rated five stars by TipRanks, downgraded Palantir Technologies PLTR. He cited worries clouding (no pun intended) the enterprise software space. After noting that software and big-data-type companies have been "largely downbeat" on recent calls, White cut PLTR from "neutral" to an outright "sell" rating with a $20 target price.

I am not knocking Brian White. I follow him and he is among the very best. That said, readers should know that he has been perpetually wrong on Palantir. White only upgraded PLTR from "sell" to "neutral" in late April. In fact, White downgraded PLTR from "buy" to "neutral" in July of 2021 when the stock was trading with a $9 handle and never placed a "buy" rating on the stock again. As of last night's close, PLTR was up 400% from January 2023. White would have had his followers sit that rally out. We all make mistakes. We all have one stock that we are not "good" at. Brian White is historically very not good at PLTR. In fact, he's been quite the opposite.

But Keep In Mind ... Other Opinions

Earlier this week, analyst Joseph Bonner of Argus Research, who is also rated five stars by TipRanks, initiated PLTR with a "buy" rating and a $29 target price. Bonner noted Palantir's long service to the U.S. defense and intelligence communities and has successfully expanded into the commercial side of the U.S. and global economies providing analytics, data management and other services to business partners in the private sector. Bonner sees the company's businesses continuing to grow both on the public and private sides.

Last Friday, I raised my target price from $29 to $31. I am not always correct, but the fact is that I had TheStreet's "Stocks Under $10" portfolio in Palantir since the stock was trading in the mid-single-digits and I have had a long position in my personal account since that Under $10 product was terminated as a stand-alone subscription vehicle, which allowed me to take on positions in the under $10 names. In short, I have some wood in the fire. These analysts generally cannot.

Fundamentals: Wow!

For the most recent quarter reported, Palantir generated operating cash flow of $129.579 million. We add to that number $21.719 million in employer payroll taxes related to the company's stock-based compensation expense, and then carve out the firm's capital expenditure spending of $2.664 million. That left Palantir with adjusted free cash flow of $148.634 million.

Looking at the balance sheet from March 31, Palantir ended that period with a cash position of $3.868 billion and current assets of $4.436 billion. Current liabilities added up to just $750.553 million, which included $237.634 million worth of deferred revenue, which is not a true financial obligation. There was no short-term debt on these books. That put the company's current ratio at an incredibly strong 5.91. Once we adjusted for deferred revenues, the current ratio rises to a stunning 8.65.

Total assets amounted to $4.807 billion. Palantir claimed no value for intangible assets, which we appreciate, but with a balance sheet like this, there is no need to try to puff up the asset side of the balance sheet. Total liabilities less equity comes to $945.907 million. There are some additional deferred revenues in there, but absolutely no long-term debt.

To repeat, Palantir had no debt of any kind.

Put bluntly, this balance sheet is a reason, in my opinion, to invest in this name, on its own merits regardless of the starts and fits that the business may go through or how the technicals line up. On that note, let's take a look at the technicals.

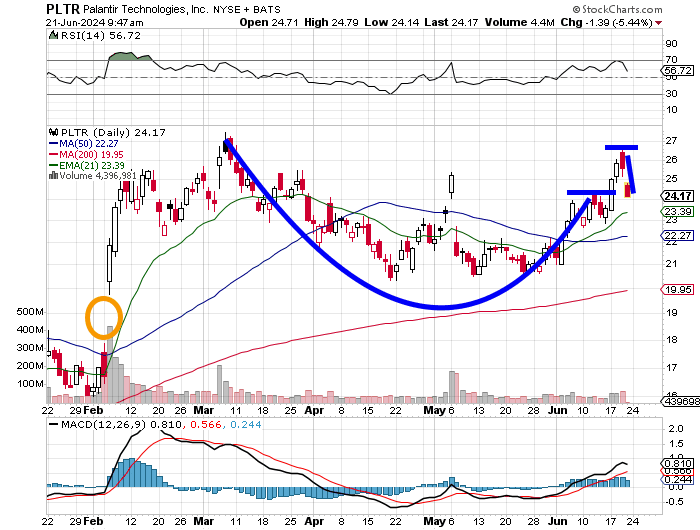

The Chart

A week ago, I showed readers that our descending triangle had morphed into a cup-with-a-handle pattern, which is often seen as a more bullish set-up. Readers will see that Relative Strength is off of the highs, but still solid. The daily moving average convergence/divergence is decisively more bullish than it was two weeks ago and still in a good spot even after this weakness that we are currently seeing.

What has happened is that the Monness downgrade after the breakout earlier in the week, extends where we add the handle. This increases our pivot and by extension, our target price. As a Palantir bull who is long the stock, I think Brian White may have done us a favor.

Palantir Play

Target Price: $32 (up from $31)

Pivot $26 (up from $24)

Add: down to the 200-day simple moving average (currently $20)

Panic: On a loss of that 200-day SMA.

At the time of publication, Guilfoyle was long PLTR equity.