Netflix Traders Hit the 'Sell' Button, But It's Not a Total Bust: How to Trade It

How about a dividend Netflix? Here's what comes next.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Some of you may remember that I had been short Netflix NFLX for quite some time. I managed the risk rather well for a while. I was ultimately forced to cover that position a couple of weeks ago by my own 8% rule. I know, the rule has saved me more often than it has hurt me.

That said, seeing Netflix selloff sharply like this overnight Thursday into Friday morning, is like rubbing salt into a wound. Back to reality. Need to remember that better people have bigger problems.

For the firm's first quarter, ended March 31st, Netflix posted a GAAP EPS of $5.28 on revenue of $9.37B. The top line print edged consensus view and was good enough for year over year growth of 14.8%, while the bottom-line number crushed expectations. Global paid memberships (subscriptions) grew by 9.33M to $269.6M.

The total of new subs amounted to growth of 16% from the year ago comp, and almost doubled Wall Street expectations. All good, right? Not so fast, my friends. Let's dig in.

Regional Sales Performance

UCAN (US & Canada)... generated revenue of $4.224B (+17%) on paid memberships of 82.66M (+2.53M), posting an average revenue per membership of $17.30 (+6.9%).

EMEA (Europe, Middle East & Africa)... generated revenue of $2.958B (+17.5%) on paid memberships of 91.73M (+2.92M), posting an average revenue per membership of $10.92 (+0.3%).

LATAM (Latin America)... generated revenue of $1.156B (+8.9%) on paid memberships of 47.72M (+1.72M), posting an average revenue per membership of $8.29 (-3.6%, but +16% in constant currency).

APAC (Asia Pacific)... generated revenue of $1.023B (+9.5%) on paid memberships of 47.5M (+2.16M), posting an average revenue per membership of $7.35 (-8.5%, but -4% in constant currency).

Operations

As revenue grew 14.8%, the cost of that revenue increased 3.6% to $4.977B, and operating expenses increased 7.1% to $1.761B. This left operating income of $2.633B (+53.6%, not a misprint) as operating margin improved from 21% all the way to 28.1%. After accounting for interest and taxes, net income landed at $2.332B (+78.7%, again... no misprint). This works out to a GAAP EPS of $5.28 once factoring for dilution.

Guidance

For the second quarter, Netflix is forecasting revenue of $9.491B, which would be good for year over year growth of 15.9% (or 21% in currency neutral terms), and better than the $9B to $9.25B that Wall Street was looking for. The firm also sees operating income of $2.52B (+38%) on an operating margin of 26.6%, up from 22.3% for Q2 2023. Earnings per share for the second quarter are projected at $4.68, which is above the $4.50 to $4.55 that Wall Street had in mind. That all seems well and good. Let's move on.

For the full year, Netflix now expects to see revenue growth of 13% to 15% and an operating margin of 25%. The operating margin would be up from previous guidance for 24%, but the revenue growth would be a deceleration from the 16% growth experienced in Q2 2023 and the roughly 16% growth experienced in Q1 2024. That's just one issue. If it were but one issue in isolation, it may have been overlooked. It was not.

The firm also announced that it will put a halt to the provision of quarterly membership growth numbers next year. The goal here is to evolve the way Wall Street judges the firm's performance from sheer subscription growth to the ability to produce and grow profitability and free cash flow.

How Wall Street is taking it now is that subscription growth must have peaked, and the firm is not going to be willing to provide contracting growth moving forward. Overnight, traders hit the "sell" button.

Fundamentals

For the period reported, Netflix generated operating cash flow of $2.213B. Out of that number came Capex spending of $75.714M, leaving free cash flow of $2.137B, which is more or less in line with Q2 2023. Out of this number, the firm repurchased $2B worth of common stock for the firm's treasury. Despite robust profitability and strong cash flows, the firm does not return cash to shareholders in the form of a dividend payout.

Moving on to the balance sheet, Netflix ended the quarter with a cash position of $7.046B and current assets of $9.921B. Current liabilities add up to $9.289B that includes short-term debt of $798.9M and deferred revenue of $1.469B. Deferred revenue, as we know, is not a true financial obligation. The firm's current ratio works out to 1.07, which passes muster, but just barely. However, once that current ratio is adjusted for those deferred revenues, it rises to a healthier looking 1.27.

Total assets amount to $48.828B, which includes no goodwill and no other intangibles. We appreciate that. Total liabilities less equity comes to $27.462B, including $13.217B in long-term debt. That's a lot, but not an immediate concern. What management could do, given that cash flows are strong... is not repurchase quite so many shares for its treasury, which benefits the C-suite far more than it does the retail investor and pay down some of that debt, while dishing out some cash to shareholders in the form of dividends.

Wall Street

This stock is highly followed. That's for sure. After weeding out all of the analysts rated at less than four stars (out of five) by TipRanks, I was left with 19 highly rated sell-side analysts that had opined on NFLX since Thursday night. Among those 19, we have 12 "buy" or buy-equivalent ratings and seven "hold" or hold-equivalent ratings. One of the "buys" and two of the "holds" did not set target prices, so we are working with 16 targets.

Across the 16 remaining analysts, the average target price is $665.56 with a high of $726 (Steven Cahill of Wells Fargo) and a low of $550 (Kannan Venkateshwar of Barclays). Once we exclude those two as potential outliers, the average across the other 14 analysts rises to $669.50.

Because you were probably going to ask if you've made it this far, the average "buy" target is $698.09, while the average "hold" target is an even $594.

My Thoughts

The business is running well. Surging subscriber growth that probably cannot be sustained. An almost solid balance sheet. Strong cash flows. The problem is probably in the valuation. My short was early, which made it wrong, but the idea was not out of left field.

The stock still trades at 35 times forward looking earnings, eight times sales and almost 13 times book. I know that I have mentioned it a few times already, but the announcement of a cash dividend would have gone a long way with shareholders. Not going there while doing this well was shortsighted.

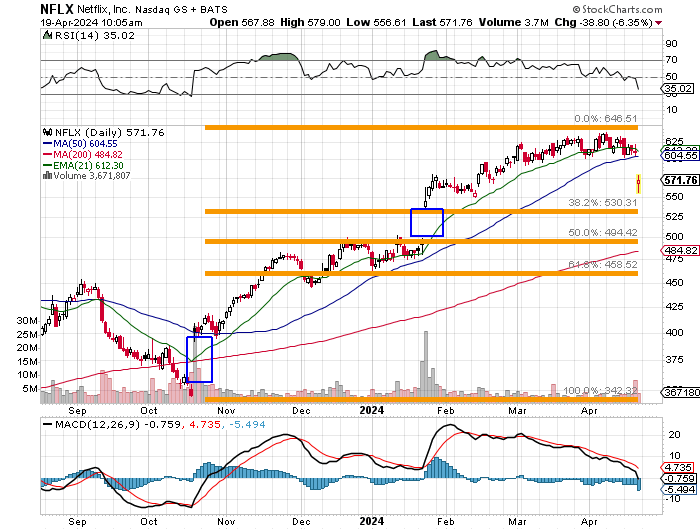

The stock traded sideways from early March into the present. Relative strength has gone from very strong to strong to neutral to now... weak. The daily MACD (moving average convergence divergence) went bearish in mid-February and has only gotten worse. It's now downright ugly. This morning, the stock surrendered its 50-day SMA (simple moving average) and its 21-day EMA (exponential moving average) in one fell swoop.

Where is support? The 38.2% Fibonacci retracement level of the October through April run, kicks in at a rough $530. The halfway back point kicks in at about $494. That level would also fill the gap created this past January. Do I think that the shares struggle for a little while? You know I do. That's how I was positioned. It's only my adherence to my code of discipline that I am flat these shares this morning.

Do I want to short it here? I do not. I am more thinking about where NFLX is a buy or I should say, where at a discount am I willing to be exposed to equity risk over time. The $495 July puts are currently paying a rough $9.85. That's interesting.

If I do make that sale though, I am going to want to cap the downside risk by purchasing a like amount of July $470 puts for about $6. The idea is that I hope the stock does not go that low and I can pocket the $3.85 net basis. The risk would be capped at a loss of $25 which is a lot, but at least it's capped. Cut the spread any tighter and the credit paid would not be attractive enough in my opinion.

At the time of publication, Stephen Guilfoyle had no position in the securities mentioned.