As Market Rotation Begins, Is a Monster Reversion Trade on the Way?

Given the nascent rotation we’re seeing in markets, here's what that might mean…and how investors can capitalize.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Tech stocks have led this market. Tech fund inflows have been enormous. But we’re seeing some tentative rotation behind the scenes. What does it mean? And will it continue?

What other stocks and sectors should you consider – beyond mega-cap, widely held names like Nvidia Corp. NVDA? See what a handful of MoneyShow expert contributors have to say.

Lucas Downey Mapsignals.com

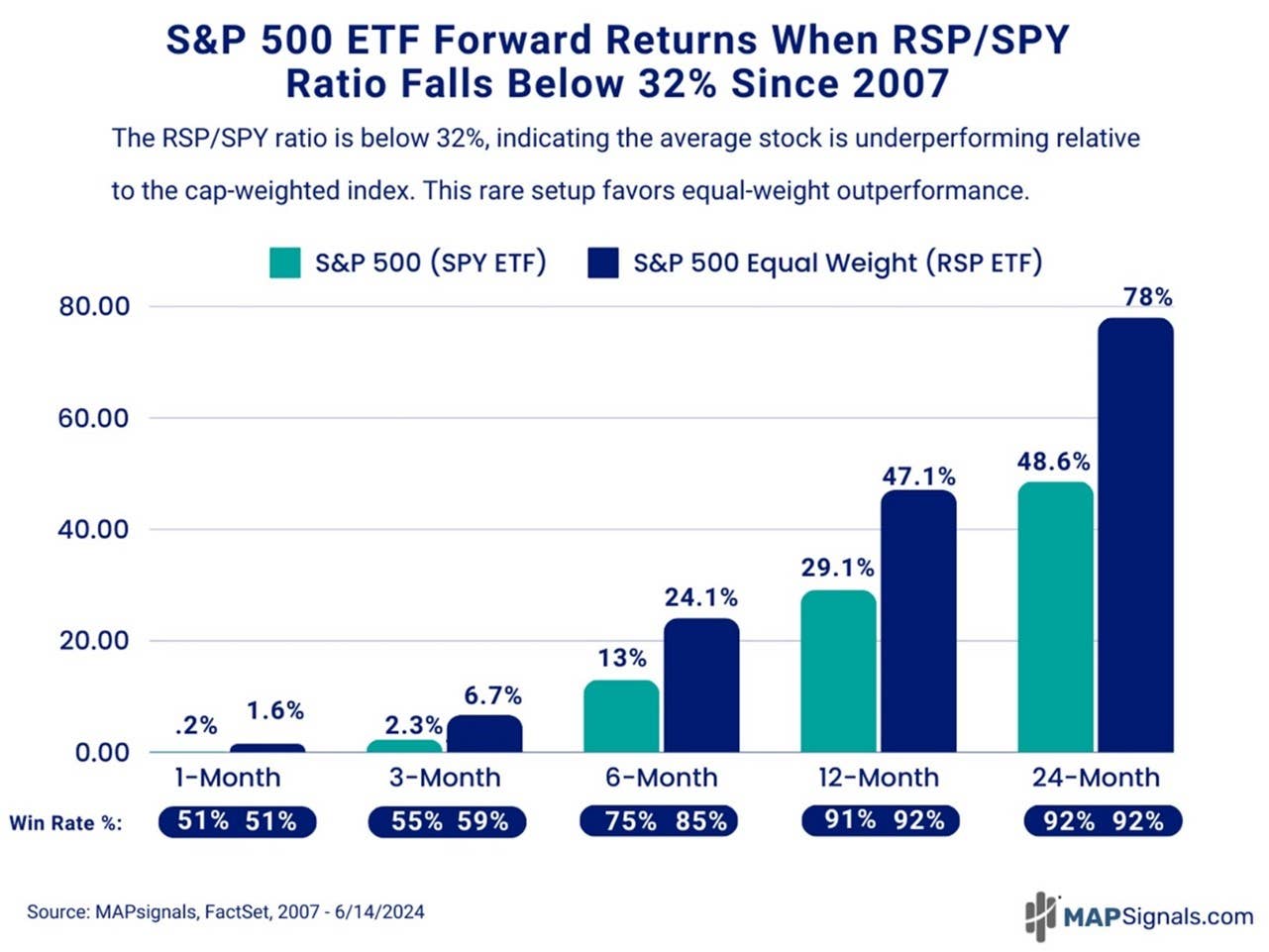

RSP and SPY: Get Ready for a Mean Reversion Trade for the AGES!

The appetite for stocks is off the charts…especially mega-cap tech names. This has caused market breadth readings to plummet. But don’t fret, because now’s the time to get ready for a monster reversion trade for the ages. That will help the Invesco S&P 500 Equal Weight ETF RSP, notes Lucas Downey, co-founder of Mapsignals.com.

Below we can see how the top stocks in the S&P 500, as tracked by the Invesco S&P 500 Top 50 ETF XLG, have gained 22.5% in 2024. That easily beats the S&P 500 ETF Trust SPY jump of 15.7% and dramatically crushes the RSP YTD performance of +5.1%.

But MAPsignals is all about bringing you evidence-based research that flies in the face of the talking-heads in the media. Before you bail out on your underperforming stocks, have a look at the following pieces of evidence suggesting you should sit tight. And if you’re bold, start buying the beaten-down dogs.

I went back and singled out all days when the RSP/SPY ratio fell below 32%. Basically, I needed to understand what we should expect for stocks going forward. That 32% threshold amounts to 201 trading dates that triggered during the Global Financial Crisis lows, the COVID crash lows, and the relative lows seen recently.

Here’s what happened next: The SPY did just fine. But the RSP was spectacular. When the RSP/SPY ratio fell to 32% or lower since 2007:

- Six months later, the S&P 500 jumped 13% while the S&P 500 Equal Weight basket soared 24.1%

- 12-months later, we saw gains of 29.1% for SPY and 47.1% gains for RSP

- 24-months after, we saw SPY jump 48.6% and RSP catapult 78%

Here’s the bottom line: The stock market rally can keep going. Better yet, all stocks should begin to participate in the coming months…and years. If history is a guide, we will be looking at a monster reversion trade where the equal weighted S&P will play catch up to the market bellwethers.

John Eade Argus Research

Energy: As Economic Backdrop Evolves, Consider This Promising Sector

May started strong and, after some wavering toward month-end, finished with a flourish, including the best stock week in 2024 to date. We are encouraged by the double-digit stock-market gain as of end-of-May – usually a reliable portent of a full-year, double-digit gain. Meanwhile, energy looks more attractive here, writes John Eade, president of Argus Research.

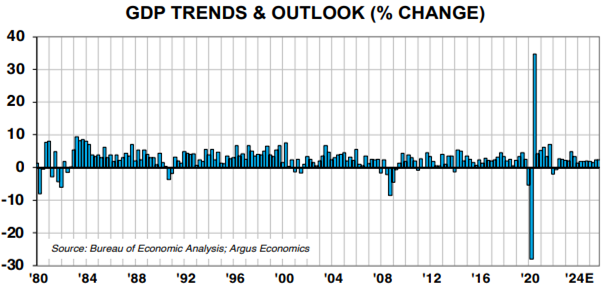

The latest report of first-quarter 2024 GDP showed growth of 1.3%, down from 3.4% growth in 4Q23. Personal consumption expenditures for 1Q24 increased 2%, down from 3.3% for 4Q23. All goods spending fell 1.9% in 1Q24, after rising 3% in 4Q23. PCE goods categories were strong in the holiday quarter. Post-holiday, consumers pulled back sharply amid the effects of multi-year inflation.

Outside GDP, economic indicators generally suggest deceleration, although growth continues at a subdued level. April retail sales were unchanged from March, extending the weak PCE performance in first-quarter GDP. US factory orders rose 1.6% in April, while durable goods orders rose 0.7%. Industrial production dipped 0.3% in April, and capacity utilization of 78.4% was 1.2 points below its long-run (1972-2023) average.

Given the realities of the current environment, we lowered our forecast for 2024 GDP growth to 1.8%, from a prior 2%. Our expectations for 2025 GDP growth are in the 2% range.

Still, five months into 2024, the market is showing impressive sector breadth. Unlike in 2023, the top growth-focused sectors are barely beating the market rather than trouncing it as they did a year earlier. Seven sectors are either tracking or beating the S&P 500.

Beyond summer, investors are bracing for what could be the most partisan election in the modern era. Yet they are simultaneously anticipating the first rate cut in this cycle, which would also be the first rate cut since the COVID-19 pandemic.

We have adjusted our recommended sector allocations, as we do each quarter at the beginning of March, June, September, and December. The following reflects our guidance for the calendar third quarter of 2024.

Although we use a quantitative, six-part, “blind” sector model, our sector recommendations tend to align with qualitative and fundamental dynamics in the market outlook. We have raised the Energy sector to recommended Market-Weight from recommended Under-Weight. Energy demand appears to have stabilized, as initial consumer euphoria over EVs has cooled, and global economic recovery has put petroleum supply and demand into relative balance.

Thomas Hayes Hedge Fund Tips

Nvidia: A Great Company? Yes. But Keep THIS in Mind Here...

Nvidia Corp. NVDA has been all the rage – and justifiably so. Since NVDA reported its Q1 2023 earnings and disclosed the huge demand for its AI chips, the stock has gone straight up. But what may go even higher in the short term can go a lot lower in a blink, counsels Tom Hayes, editor of Hedge Fund Tips.

NVDA is now worth $3.3 trillion. Revenues up 4x, margin expansion, etc. – it’s everything anyone could ever wish for. And as the stock went up, bulls exclaimed it’s getting “cheaper” because as earnings grew, the multiple came down.

But now we have a different landscape – one of decelerating growth. Quarterly revenue growth has gone from 88% to 34% to 18% and is on its way to single digits. Now the multiple is re-accelerating into slowing growth. Next quarter revenue growth guidance is just 7%.

All of the marginal buyers are in – sucking the last few retail buyers in with the lure of a split. History suggests a short-term bump after a split as we are seeing, but now institutional investors have a vast pool to distribute their shares in coming months. As the saying goes, “when the ducks are quacking, feed them.”

This does not change the fact that Nvidia is a great business with a great leader – which will play a role in the advance of AI technologies and productivity. It’s just going to be a heavy lift that it retains a perception of greater value than Amazon.com Inc. AMZN, Microsoft Corp. MSFT, or the entire German stock market capitalization (where it trades now).

NVDA is still a semiconductor company, which has never been a secular business – it’s cyclical. Always has been, always will be. As for 70%+ gross margins, as Bezos famously said, “your margin is my opportunity.”

NVDA has not cured cancer. There will be more and more competition going forward. Intel Corp.’s INTC Gaudi 3 is 50% faster than NVDA’s H100 and 40% more energy efficient. Advanced Micro Devices Inc. AMD is gunning for them. The game is just beginning and NVDA will be forced to share the pie as no buyer wants to be beholden to one company.

Remember: “Price is what you pay, value is what you get.” Caveat emptor at these levels.