New Guidance on Lululemon After CFO Addresses Markdown Issues

The apparel brand is down considerably from daily highs and, despite strong fundamentals, it's facing some issues.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Lululemon Athletica LULU opened higher but is down considerably from its daily highs. So, we must ask: Is LULU hot or not? Let's explore.

For the firm's fiscal first quarter, which ended on April 28, 2024, LULU posted a GAAP earnings per share (EPS) of $2.54 on revenue of $2.209 billion. The top-line print beat Wall Street by just a smidge, while reflecting year-over-year growth of 10.5%. The bottom-line number beat the consensus view by about $0.12 and compares well to the $2.28 reported a year ago for this quarter.

Comp sales increased 6% over the year-ago quarter, or 7% in constant currency. Within that number, comp sales in the Americas were flat, while international comp sales were up 25% (29% in cc). Americas-driven revenue did manage to eke out 3% growth, while internationally driven revenue saw a 35% (40% in constant currency) increase. Additionally, the board of directors authorized a $1 billion increase in the firm's share repurchase program. This brings the current remaining authorization up to $1.7 billion.

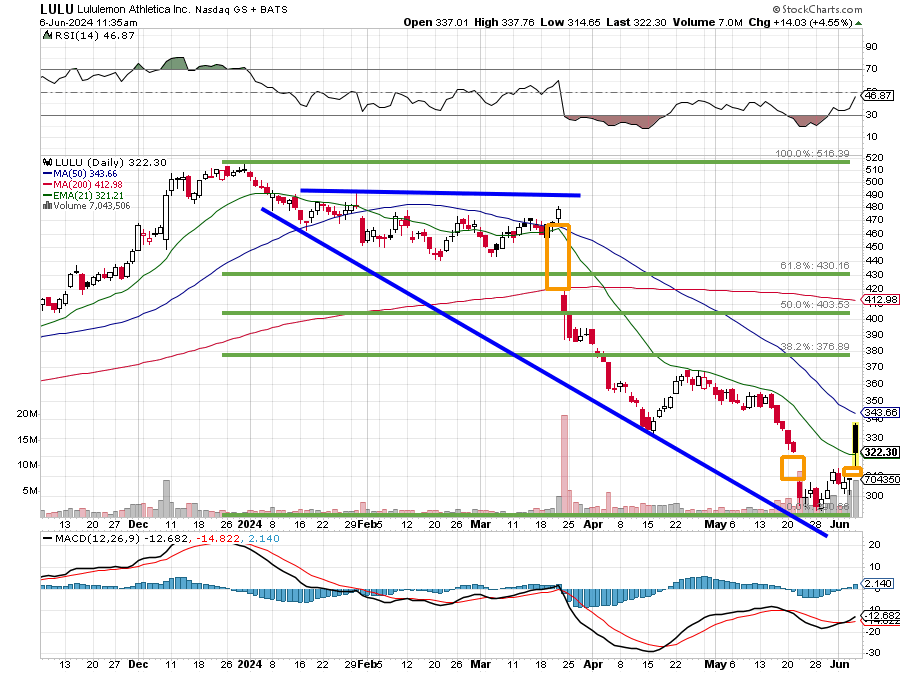

LULU Operations

As revenue grew 10.5% to $2.209 billion, the cost of goods sold increased 9.9% to $933.823 million. This left a gross profit of $1.275 billion (+10.7%), on a gross margin of 57.7%, which was up from 57.5% a year ago. Operating expenses printed at $842.426 million (+12.4%), leaving operating income of $432.642 million (+7.8%) as operating margin actually dropped from 20.1% to 19.6%. After factoring in other income, interest and taxes, net income landed at $321.421 million (+10.7%). This works out to a GAAP EPS of $2.54 once the share count is diluted, up from the year ago comp of $2.28.

LULU Guidance

For the current quarter, LULU sees net revenue of $2.4 billion to $2.42 billion, which was a little below expectation for something close to $2.45 billion. This would be good for growth of 9% to 10%. Diluted EPS is seen at $2.92 to $2.97, which is a problem. Wall Street was looking for something above $3 on that number.

For the full year, the firm expects net revenue to print between $10.7 billion and $10.8 billion, which is right in line with the consensus view for $10.75 billion. That would be good for growth of 11% to 12% inclusive of a 53rd week in the fiscal year. Exclusive of that week, growth should print up 10% to 11%. Operating margin is seen at roughly 23.3%, which is well above the margin posted for the just completed quarter. Diluted full-year EPS is projected at $14.27 to $14.47, which is well above the $14.10 to $14.15 that many on Wall Street were looking for. That improved profitability in the full year outlook, is largely why (along with the buyback) the shares popped overnight.

LULU Fundamentals

For the quarter reported, LULU generated operating cash flow of $127.524 million. Out of that number came capex spending of $130.681 million, leaving free cash flow of $-3.157 million. After that, the firm still spent $299.479 million in the repurchase of common stock. While this appears to be a case of mismanaged cash flows, as readers will see, the firm has the cash position to handle what it is doing. That said, increasing the current authorization seems unnecessary and perhaps was more showmanship than substance.

Looking at the balance sheet, the firm ended the period with a cash position of $1.901 billion, and inventories of $1.345 billion. This puts current assets at $3.768 billion. Current liabilities add up to $1.384 billion, including no short-term debt and $268.3 million in unredeemed gift cards, which is basically unearned revenue. That leaves the firm with quite a robust current ratio of 2.72 and a quick ratio of 1.75, which is outstanding for a retailer. Adjusted for those unearned revenues, these ratios rise to 3.38 and 2.17, respectively.

Total assets amount to $6.828 billion including goodwill of just $23.992 million, which is insignificant. Total liabilities ex-equity comes to $2.609 billion. This includes no long-term debt. That's right, the firm has no debt on the books whatsoever, and a nice cash pile. This is a very solid balance sheet.

What Does Wall Street Think About LULU?

This section is going to be pretty wild. Since these earnings were released last night, I have come across 11 highly-rated (four-plus stars at TipRanks) analysts that have opined on LULU. Interestingly, some well-known names such as Matthew Boss of JPMorgan did not make the four-star cut for this go-round. Across the 11 analysts, there are eight "buy" or buy-equivalent ratings, two "hold" or hold-equivalent ratings and one outright "sell" rating. One of the "buys" did not set a target price, so we are working with just 10 of those.

Across our 10 remaining analysts, the average target price for LULU is now $400.50 with a high of $470 (Dana Telsey of Telsey Advisory) and a low of $240 (Randal Konik of Jefferies). Once those two are omitted as potential outliers, the average target across the other eight rises to $411.88. Because you'd love to know, the average target across the "buys" is a whopping $434.71, but the average target across the non-buys is just $320.67.

My Thoughts on LULU

The balance sheet is exceptional. Nothing I do or write can take that away. The cash flows are not healthy. The guidance is mixed and what is positive there is dependent upon significantly-improved operating margin for the balance of the year. The increased buyback was completely unnecessary with so much remaining on the current authorization, especially when the repurchasing has to come out of the cash position because cash flow is not in a position to support such aggression. Then again, just because something is authorized does not mean that it has to happen.

Some troubling thoughts: LULU CFO Frank Meghan mentioned markdowns repeatedly during the call. LULU, as Jim Cramer pointed out in his morning show at CNBC, is a full-price brand. Something lost due to heavy inventories or inventory mismatches might be tough to regain. In one answer to an analyst last night, Meghan addressed the issue.

"In terms of U.S. product margin, I don't see that changing over the long term," he said. "We run a highly full-price business. We have no plans to change our strategy there. So I would view some of the current challenges with assortment and slightly higher markdowns as temporary."

Yikes.

"How anyone could actually RAISE a price target after this $LULU print is a complete mystery to me," Hedgeye retail analyst Brian McGough

Wow, tell us how you really feel.

To tell you the truth, I've come toward the end of this piece thinking that LULU might just be a short as well.

About the most optimistic take-away I have from looking this company over, save for the balance sheet, is that as the share price has collapsed from the highs of this past December, the valuation has collapsed with it. The stock now trades at 21-times forward-looking earnings, less than four-times sales and about nine-times book. Five months ago, LULU traded at 32-times forward-looking earnings, more than six-times sales and more than 16-times book. One might say that the stock is now fairly valued. Still, would you buy it today, as it has held at almost a five gain for the session?

Relative strength has improved, though I would not call it strong. The daily MACD has improved. There's a big, fat, unfilled gap way above, but also a lot of Fibonacci and moving average wood to cut if the stock ever runs that high again. The stock has retaken its 21-day EMA, which means the swing crowd is engaged. That said, LULU hit resistance this morning before reaching its 50-day SMA, which means that old-school portfolio managers have not yet bought in.

I Think...

Rather than shorting the equity outright, I would rather get long a $320/$315 bear out spread expiring tomorrow for a net debit of $1.65 or go out two weeks and get long a $320/$310 bear put spread expiring on June 21, 2024, for an outlay of roughly $3.50.

At the time of publication, Guilfoyle had no positions in any securities mentioned.