Is EchoStar’s Dish Network Deal for Real?

EchoStar jumped 21% on Thursday. Here's why and how it could be an opportunity.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Strolling through my little town, I notice that Dish Network satellite dishes are becoming harder to find. If you were a Dish Network subscriber ten years ago, there’s a good chance you’ve moved on from the Colorado-based subscription TV service.

You don’t hear much about Dish Network these days — and there's a good reason for that. In the battle for viewers, this satellite TV service is an also-ran.

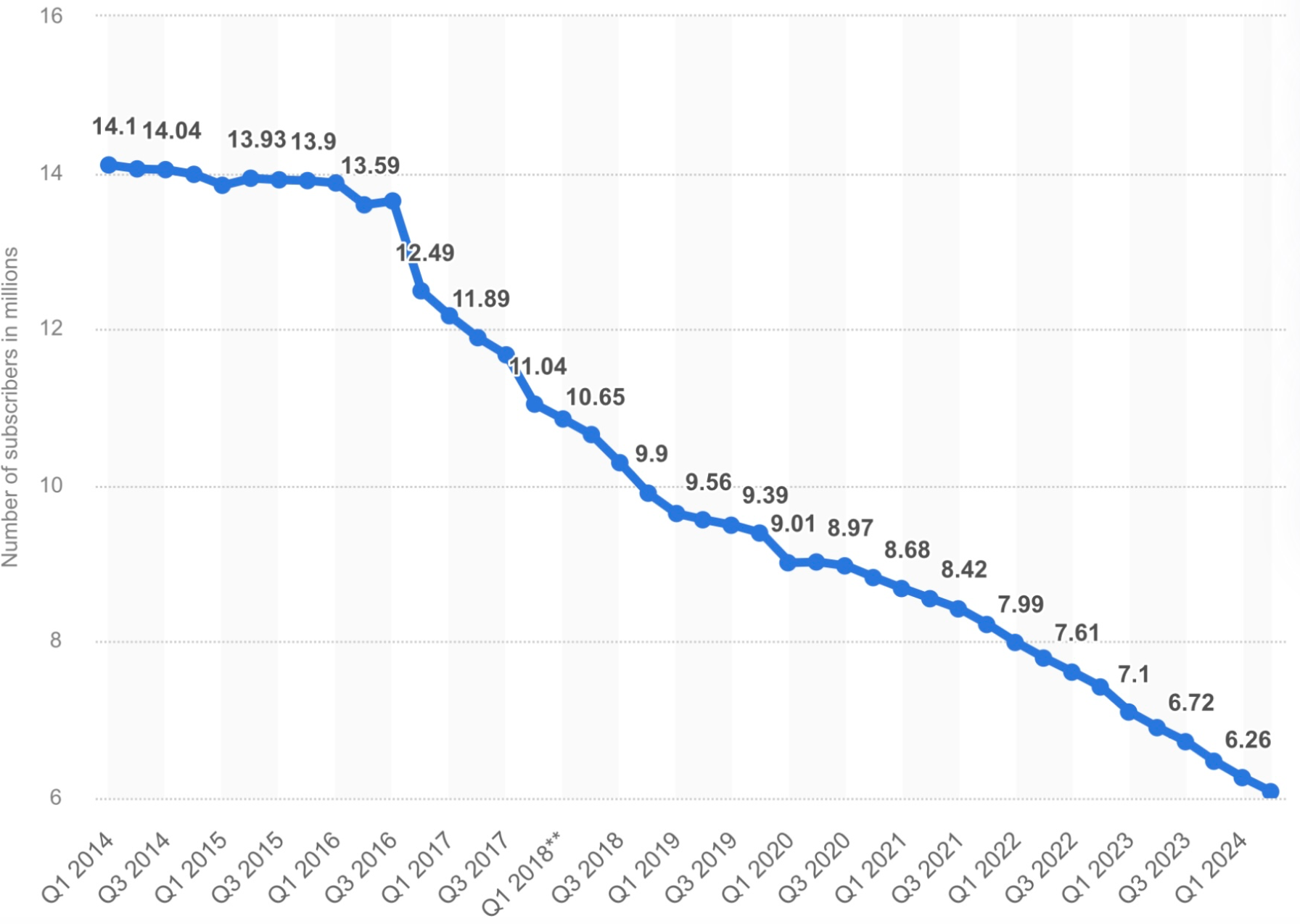

Ten years ago, Dish Networks had over 14 million subscribers. That figure has now dwindled to six million.

Dish Network, and its parent company EchoStar SATS, have taken a beating from providers such as Comcast CMCSA and Verizon VZ.

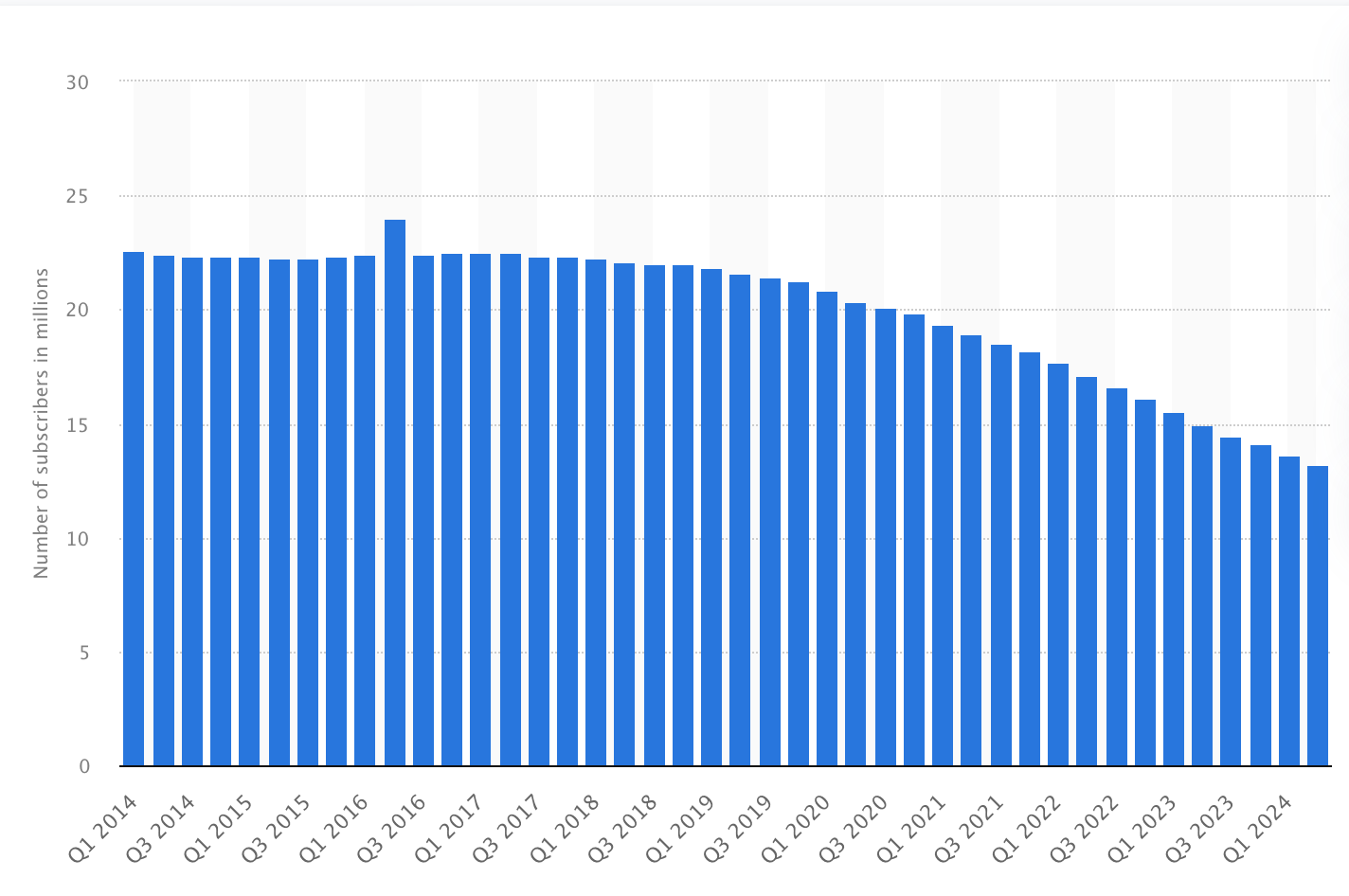

Those services are also losing subscribers, but not at the dramatic rate experienced by Dish Network. As seen below, Comcast subscribers are cutting the cord, but at a slower pace.

Based on this information, you can imagine my surprise when shares of EchoStar jumped 21% on heavy volume Thursday.

The catalyst behind the move was news that Dish Network is in talks to settle a lawsuit with its creditors. Terms of the settlement could include an extension on a $2 billion bond issued by Dish Network, which is scheduled to mature on November 15.

Whether or not Dish Network will survive in the long run is debatable. What cannot be denied is the fact that shares of EchoStar closed at a 52-week high on Thursday.

EchoStar is trading within a bullish channel (black lines). The stock has formed a series of higher lows (HL) and higher highs (HH), and is trading well above its 50-day (blue) and 200-day (red) moving averages.

One caveat: This is a trade, not a long-term investment. EchoStar has $24.87 billion in debt on its balance sheet, but had revenue of just $24.5 million in its recently-ended quarter. In the long run, heavily indebted companies have a poor track record as long-term investments.

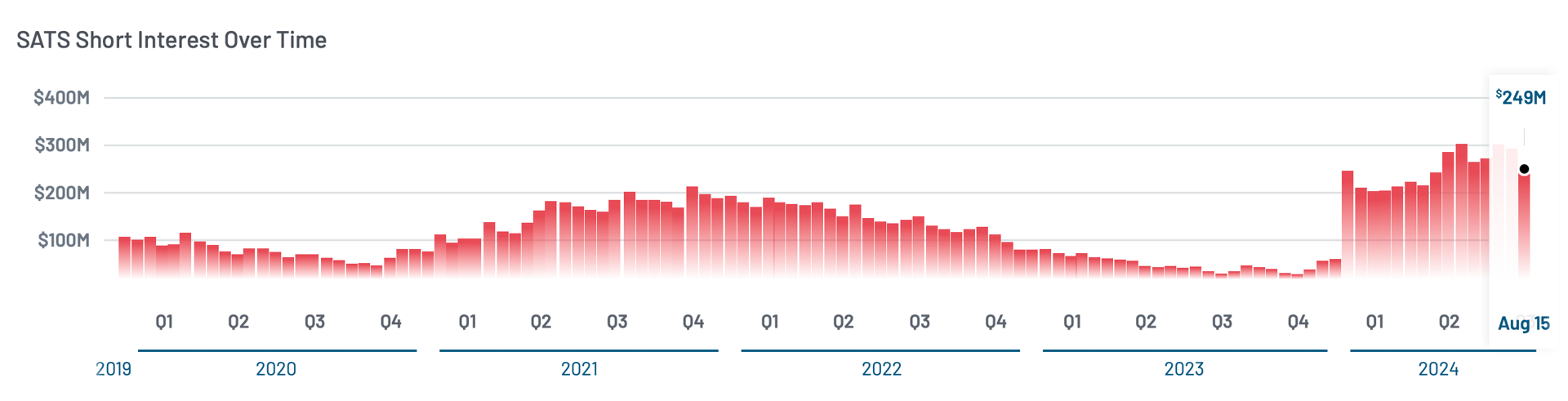

On the bright side, EchoStar’s strong move to the upside could see some follow-through. That’s because there is significant short interest in the stock.

In the above chart, we see that short interest in EchoStar escalated dramatically at the start of 2024, and is hovering near its highs.

We can think of shorts as future buyers. For some EchoStar shorts, the future is now.

In mid-November of last year, EchoStar short interest stood at 2.68 million shares, valued at nearly $27 million. By mid-August of this year, those figures had swelled to 13.98 million shares, with a value of $249 million.

I can't blame investors for shorting EchoStar. It's a debt-laden company that sells unpopular products.

For traders, EchoStar presents an opportunity on the long side, but only for a limited time.

At the time of publication, Ponsi was long SATS.