Here's Where I See Upside as Warren Buffett Buys Sirius

I can see getting long on the satellite radio firm alongside Buffett and Berkshire.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

What do I know about Sirius XM Holdings SIRI? Do I have the satellite radio in my car? No. Do I use the app on my smartphone? Consistently. Do I listen through Amazon's AMZN Alexa? On and off all day long. Why? It's so convenient. Financial networks? CNBC, Fox Business and Bloomberg Radio are all on the app. So is the home and away broadcast for every NFL, MLB, NBA and NHL game, as well as a lot of college sports and other sports as well. That's key.

As a dual resident of the great state of Florida and the sad state of New York, this is how I keep up with my favorite sports teams when I am out of the market for those teams. Don't tell me to buy a sports package for my television. The last thing I want to do at night is sit in front of a TV and go into couch potato mode. Either I am working out with sports on the radio or I am doing homework that can actually make me some dough... with sports on the radio in the background. Safe to say, losing Sirius XM radio would impact my quality of life.

Today's News

Really, Friday night's news, but it made headlines this morning. Readers may recall that in Berkshire Hathaway's BRK.A, BRK.B 13-F disclosure back in August that the Warren Buffett led firm had more than tripled its stake in Sirius from the end of Q1 to the end of Q2.

In early September, Sirius began a new chapter in its history as a completely independent company after closing its transaction with Liberty Media LSXMA. At that time, the firm adjusted its outlook for its full-year free cash flow guidance to reflect a rough $70 million in closing costs and about $130 million associated with year-to-date outflows as Liberty Sirius XM. The firm also announced that it expected to pay a shareholder dividend of about $0.27 per quarter, which is currently good for a yield of roughly 3.85%.

On Friday night, Buffett's firm filed a Form-4 with the SEC that it had purchased more than $42 million worth of SIRI over three days from Wednesday to Friday, taking its long position to more than 110 million shares. That comes to a 32.5% stake in the firm's publicly-traded shares, according to Bloomberg News. Berkshire had filed with the SEC a week earlier, disclosing a three day run of purchases the week prior to last that totaled $86.73 million in stock.

Earnings

Sirius is expected to report on Halloween. Spooky. Scary. Wall Street is looking for a GAAP EPS of roughly $0.75 on revenue of $2.19 billion. That would be "good" for a 4% year-over-year contraction in revenue and compare to an EPS of $0.90 for the year-ago period.

So, why does Buffet like SIRI? It could be the steady free cash flow of close to $300 million per quarter. The balance sheet is not exceptional, though 44% of current liabilities are in the form of unearned revenues that are not financial obligations as long as the agreed upon goods or services are provided.

The stock does trade at ten-times forward earnings, and we did mention the somewhat beefy dividend yield. I don't think Sirius is going to make a killing. I think it is going to do exactly what investors like Buffet like to see. That is to produce cash consistently, while leaving room for growth in sales and/or appreciation in stock price through multiple expansion.

My Thoughts

I don't always make money when I mimic Buffet, though I very rarely get hurt by doing so. I have been hurt a few times taking the other side of a Buffet trade. For that reason and for the value-based reasons mentioned above, I can see getting long this name alongside Warren.

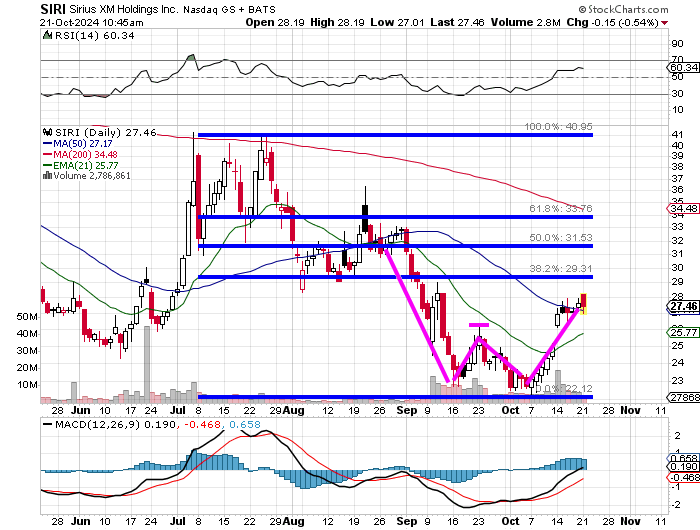

Readers will see that the stock was rejected at its 200-day SMA three times in July. The shares are now coming off of a double-bottom reversal and are closing in on the 38.2% Fibonacci retracement level of the selloff that followed that rejection.

Relative strength is solid, but nowhere near being technically overbought, while the daily MACD is close to being postured quite bullishly. We already have the 12-day EMA well above the 26-day EMA and the histogram of the 9-day EMA in positive territory. The 26-day EMA still stands ever so slightly in negative territory. Not perfect, but not bad either.

I am thinking that these shares can be bought if they can clear their own 50-day EMA. That's where there has been a battle for over a week now. Clear the 50-day, and the 200-day is back in play. Fail at the 50-day, and I think I wait for a chance at the 21-day EMA. Short the name on a failure at the 50-day line? When you already know Berkshire Hathaway has been a buyer at that level? No way, Jose. There's a reason I'm long BRK.B. I learned a long time ago to play on the same team as champions when given the chance.

At the time of publication, Guilfoyle was long BRK.B equity.