GM Is Spiking and I Have a New Price Target

A close review of the auto giant is a buy and I'm looking for a test at this level.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

General Motors GM spiked 4.05% on Monday. The stock is up another percent or so overnight. What did Ford Motor F do? Up a little on Monday. Down a little overnight. Nothing like what GM did. What about Tesla TSLA? Did GM CEO Mary Barra threaten to keep AI-integrated Apple AAPL devices out of GM facilities? No, and Tesla gave up 2.08% on Monday and was up small overnight. Nothing to compare there.

The United Auto Workers and GM announced Monday that the firm and the labor union had come to a tentative contract agreement particular to the Ohio plant designed to build electric vehicles for General Motors. The agreement impacts roughly 1,600 employees working at Ultium Cells which is a joint General Motors/LG Energy Solutions venture. The deal increases starting wages as well as top-end wages and workers will receive a $3,000 ratification bonus along with a suite of improved benefits.

Tuesday Morning

If a little labor market Kumbaya between GM and their workforce was not enough to entice investors, this morning GM announced that the firm's board of directors had approved a new authorization to repurchase up to $6 billion worth of common stock. General Motors went to sleep last night with a market cap of $54.25 billion, so the board has basically authorized the repurchase of more than 11% of the firm. The firm had $1.4 billion left under the previous $10 billion repurchase authorization that had been announced in November 2023, little more than half a year ago. It's safe to say that GM is aggressively trying to reduce share count.

Earnings

GM is still about six weeks out from reporting the firm's fiscal second quarter results. Readers may recall that in late April, General Motors posted first quarter results that decisively bet expectations for both the top and bottom lines. The firm also upped its guidance for net income, adjusted EBIT, automotive free cash flow and earnings per share.

Wall Street now looks for EPS of roughly $2.65 within a range spanning from $2.30 to $2.85. This will compare nicely to the $1.91 reported for the year ago bottom-line result. Revenue growth is seen at pedestrian at best, landing at roughly $45.1 billion, within a range spanning from $42.5 billion to $47.6 billion. The year ago, comp was $44.75 billion. Readers are reminded about the improved outlook for adjusted EBIT and free cash flow. There should be visible improvement in margin.

Fundamentals

For the fiscal first quarter, free cash flow printed at $369 million, while over the trailing four quarters at that time, the firm had generated free cash flow of $9.674 billion. The balance sheet was in better shape than many might expect at the end of the first quarter, sporting a current ratio of 1.16 and a quick ratio of 0.97. The sub-1 quick ratio is more than acceptable for this kind of inventory-focused industrial/retail operation.

The firm did have a cash position of $23.74 billion including some restricted cash, and about $35.598 billion in current debt. This does cause for me some concern as GM will likely be forced to refinance some shorter-term debt at elevated interest rates. The firm also has another $17.902 billion in longer-term debt.

My Thoughts

The quarter does appear to be going rather well for General Motors and Mary Barra. My sticking point is: Why refinance short-term debt at inflated rates and run a robust share repurchase program? It may have been more prudent and fiscally disciplined to use the free cash flow for the second quarter and perhaps beyond to try to whittle down the debt slated to mature this year and leave the old repurchase authorization in place. With $1.4 billion left on that authorization, I would think that reducing the current debt-load would take a higher spot of the slate of prioritization. That said, the technical picture is taking on a bullish appearance. Let's take a look...

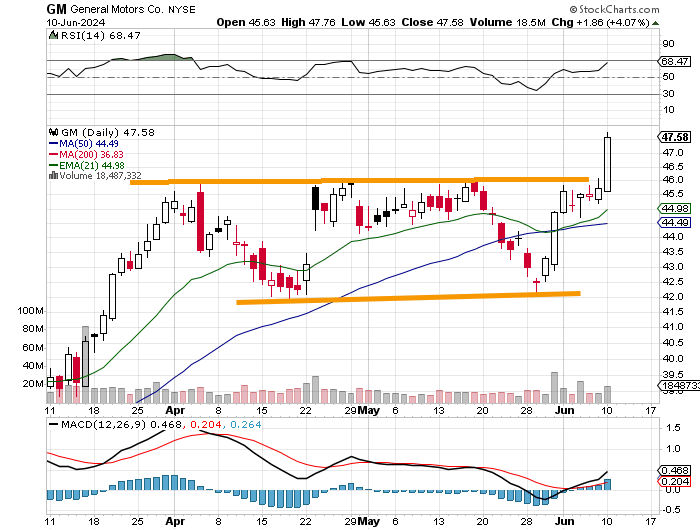

Readers will see that on Monday, GM broke out from a two-month basing period of consolidation with a $46 pivot. Relative strength is now in a very good place without being technically overbought, while the daily MACD is firing on all cylinders with the 12-day EMA above the 26-day EMA and the histogram of the nine-day EMA in positive territory.

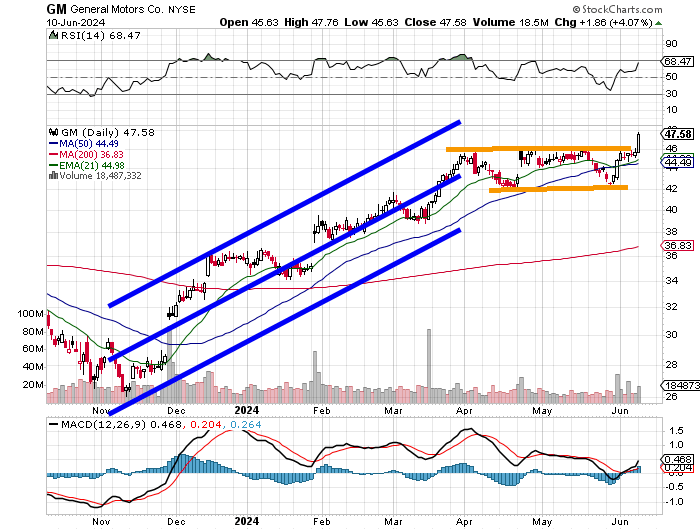

Zooming out a little, we see that consolidation had been both necessary and healthy in late March/early April. Now, we have a 200-day SMA sloping upward in chase of both the 21-day EMA and 50-day SMA. To me, the chart says that GM is a buy. I would prefer to see at least one test of that $46 level from above made and survived before I jump in. Should I see that, I think we are talking about a target price in the $55 area.

At the time of publication, Guilfoyle had no positions in any securities mentioned